Unlocking the Best Jfcu Car Loan Rates: Your Ultimate Guide to Smart Auto Financing

Unlocking the Best Jfcu Car Loan Rates: Your Ultimate Guide to Smart Auto Financing Carloan.Guidemechanic.com

The dream of a new car – the fresh scent, the smooth ride, the promise of new adventures – is exhilarating. But often, the excitement quickly turns to apprehension when faced with the complex world of auto financing. Securing a car loan can feel like navigating a maze, especially when you’re aiming for the most favorable terms. This is where understanding your options, particularly with institutions like Jfcu, becomes paramount.

Based on my experience in the automotive and financial sectors, many car buyers overlook the distinct advantages offered by credit unions. Jfcu, like many member-owned financial institutions, often provides competitive rates and a more personalized service compared to traditional banks. Our mission today is to demystify Jfcu car loan rates, providing you with a super comprehensive, in-depth guide that empowers you to make informed decisions and drive away with the best possible deal.

Unlocking the Best Jfcu Car Loan Rates: Your Ultimate Guide to Smart Auto Financing

This article will serve as your pillar content, diving deep into everything you need to know about Jfcu auto financing. We’ll explore the factors influencing your rates, walk you through the application process, and share expert strategies to secure the most advantageous terms. By the end, you’ll be equipped with the knowledge to confidently approach your next car purchase, ensuring it’s both exciting and financially sound.

Why Consider Jfcu for Your Car Loan? The Credit Union Advantage

Before we delve into the intricacies of Jfcu car loan rates, it’s crucial to understand why a credit union might be your best bet for auto financing. Unlike traditional banks, which are for-profit entities, credit unions like Jfcu are not-for-profit financial cooperatives owned by their members. This fundamental difference translates into tangible benefits for you, the borrower.

Because their primary goal isn’t to maximize shareholder profits, Jfcu often passes savings directly to its members. This frequently manifests in the form of lower interest rates on loans, including car loans, and higher returns on savings accounts. It’s a member-centric model designed to benefit the community it serves.

Furthermore, credit unions are known for their personalized service. You’re not just an account number; you’re a member of a financial family. This means more flexible lending criteria in some cases, and a willingness to work with you to find solutions that fit your unique financial situation. For a major purchase like a car, having that kind of support can make all the difference.

Decoding Jfcu Car Loan Rates: The Key Influencing Factors

Understanding what influences your Jfcu car loan rates is the first step towards securing a favorable deal. These rates aren’t pulled out of thin air; they are carefully calculated based on a combination of personal financial data and market conditions. Let’s break down the most critical factors.

1. Your Credit Score: The Cornerstone of Loan Rates

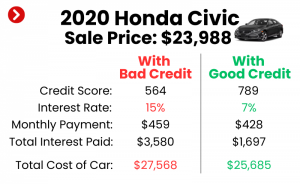

Without a doubt, your credit score is the single most significant determinant of the interest rate you’ll be offered on a Jfcu car loan. This three-digit number, primarily generated by models like FICO and VantageScore, provides lenders with a snapshot of your creditworthiness. It tells them how reliably you’ve managed debt in the past.

A higher credit score signals to Jfcu that you are a low-risk borrower, meaning you have a strong history of making payments on time and managing your credit responsibly. Consequently, lenders are more willing to offer you lower interest rates, as they perceive a reduced chance of default. Conversely, a lower credit score indicates a higher risk, which typically results in higher interest rates to compensate the lender for that perceived risk.

Pro tips from us: Before even thinking about applying for a car loan, pull your credit report and check your score. Many services offer free credit score checks, and you’re entitled to a free report from each of the three major credit bureaus annually via AnnualCreditReport.com. Review it for errors and understand where you stand.

Common mistakes to avoid are: Not knowing your credit score before applying. This leaves you unprepared and unable to negotiate effectively, potentially accepting a higher rate than you deserve.

2. Loan Term: Balancing Monthly Payments and Total Cost

The loan term, or the length of time you have to repay the loan, directly impacts both your monthly payment and the total interest you’ll pay over the life of the loan. Jfcu, like other lenders, typically offers various loan terms, ranging from short periods like 36 months to longer stretches such as 72 or even 84 months.

Generally, shorter loan terms come with higher monthly payments but result in less interest paid overall, making the total cost of the car lower. This is because the money is borrowed for a shorter duration. Conversely, longer loan terms offer lower monthly payments, which can seem attractive for budgeting, but they accrue significantly more interest over time, increasing the total cost of the vehicle.

Finding the right balance depends on your financial comfort zone. Based on my experience, it’s often wise to choose the shortest loan term you can comfortably afford, minimizing the total interest paid. However, don’t stretch your budget so thin that you risk missing payments.

3. Down Payment: Reducing Risk and Your Overall Cost

Making a substantial down payment on your car loan is one of the smartest financial moves you can make. A down payment is the initial sum of money you pay upfront towards the purchase price of the vehicle, reducing the amount you need to borrow from Jfcu.

From the lender’s perspective, a larger down payment significantly reduces their risk. If you default on the loan, they have less money to recoup. This reduced risk often translates into more favorable Jfcu car loan rates for you. For the borrower, a larger down payment means lower monthly payments, less interest paid over the life of the loan, and potentially avoiding being "upside down" on your loan (owing more than the car is worth).

Pro tips from us: Aim for at least a 10-20% down payment on a new car, and potentially more for a used car. This not only secures better rates but also provides immediate equity in your vehicle.

4. Vehicle Type: New vs. Used Car Loans

The type of vehicle you intend to purchase – whether it’s brand new or pre-owned – can also influence the Jfcu car loan rates you receive. Lenders often view new car loans as slightly less risky than used car loans. This is primarily because new cars typically have a clear, higher market value, are less prone to immediate mechanical issues, and their depreciation curve is more predictable at the outset.

Used cars, while often more affordable upfront, can carry a higher perceived risk due to their age, mileage, and potential for unforeseen repairs. Consequently, interest rates on used car loans might be marginally higher than those for new vehicles. However, Jfcu will still offer competitive rates for used vehicles, especially if they are newer models with lower mileage.

5. Debt-to-Income Ratio (DTI): Your Financial Capacity

Your debt-to-income (DTI) ratio is a crucial metric Jfcu will consider when evaluating your loan application. It represents the percentage of your gross monthly income that goes towards paying your monthly debt obligations. Lenders use this ratio to assess your capacity to take on additional debt, such as a car loan.

To calculate your DTI, simply add up all your monthly debt payments (credit cards, student loans, mortgage, etc.) and divide that sum by your gross monthly income. For example, if your total monthly debt payments are $1,000 and your gross monthly income is $4,000, your DTI is 25%. A lower DTI indicates that you have more disposable income to cover new loan payments, making you a more attractive borrower.

Pro tips from us: Jfcu typically looks for a DTI below 36-43%, though this can vary. If your DTI is on the higher side, consider paying down existing debts before applying for a car loan to improve your chances of securing better rates.

The Jfcu Car Loan Application Process: A Step-by-Step Guide

Navigating the application process for a Jfcu car loan doesn’t have to be daunting. By understanding each step, you can streamline the experience and move closer to driving your new vehicle.

1. The Power of Pre-Approval

One of the most valuable steps you can take is seeking pre-approval for your car loan with Jfcu. Pre-approval means Jfcu has conditionally agreed to lend you a specific amount of money at a certain interest rate, based on your financial information, before you even choose a car. This is a game-changer in the car buying process.

With a Jfcu pre-approval in hand, you transform into a cash buyer at the dealership. You’ll know your budget precisely, allowing you to focus on finding the right car without the pressure of negotiating financing on the spot. This also provides significant leverage when negotiating the vehicle’s price, as you’re not beholden to the dealership’s financing options.

2. Gathering Your Essential Documents

Once you’re ready to apply, whether for pre-approval or a direct loan, Jfcu will require certain documents to verify your identity, income, and financial stability. Having these ready beforehand will expedite the process.

Typically, you’ll need:

- Proof of Identity: A valid driver’s license or state-issued ID.

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2 forms, or tax returns if you’re self-employed.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Vehicle Information: If you’ve already chosen a car, details like the VIN, make, model, and mileage will be needed. For pre-approval, this might not be required initially, but it will be for final loan approval.

3. Submitting Your Application

Jfcu offers various convenient ways to submit your loan application. You can typically apply online through their website, visit a local branch in person for personalized assistance, or sometimes even apply over the phone. Choose the method that best suits your comfort and schedule.

The application itself will ask for personal details, employment history, income information, and your consent to pull your credit report. Be thorough and accurate; any discrepancies could cause delays or issues.

4. Loan Approval & Closing

After submitting your application, Jfcu will review your information, including your credit report and DTI. This evaluation process usually takes a few hours to a few days, depending on the complexity of your application. Once approved, Jfcu will present you with a loan offer outlining the interest rate, loan term, monthly payment, and any associated fees.

Carefully review all the terms and conditions. If everything looks good, you’ll proceed to finalize the paperwork. This involves signing the loan agreement, which legally binds you to the terms. At this point, the funds will be disbursed, either directly to you (for pre-approval) or to the dealership.

Maximizing Your Chances for the Best Jfcu Car Loan Rates

Securing the lowest possible Jfcu car loan rates isn’t just about having a good credit score; it’s about strategic planning and proactive financial management. Here are some actionable steps you can take.

1. Continuously Improve Your Credit Score

While we’ve already touched upon this, it bears repeating: a healthy credit score is your best friend in the loan application process. Make a conscious effort to pay all your bills on time, every time. This includes credit cards, utility bills, and any existing loan payments. Payment history accounts for a significant portion of your credit score.

Additionally, keep your credit utilization low (the amount of credit you’re using compared to your total available credit). Try to keep it below 30%. Regularly monitor your credit reports for errors and dispute any inaccuracies promptly, as these can negatively impact your score.

2. Save for a Larger Down Payment

The more you can put down upfront, the better. As discussed, a larger down payment reduces the loan amount, lowers your monthly payments, and signals less risk to Jfcu. This often results in more attractive interest rates.

Consider setting up a dedicated savings fund specifically for your car down payment. Even a few extra hundred or thousand dollars can make a noticeable difference in your Jfcu car loan rates and overall financial burden.

3. Consider a Shorter Loan Term

If your budget allows, opting for a shorter loan term can significantly reduce the total interest you pay and might even qualify you for a slightly lower interest rate from Jfcu. While the monthly payments will be higher, the long-term savings can be substantial.

Carefully calculate what you can truly afford each month without straining your budget. It’s better to have a slightly longer term with comfortable payments than to struggle with high payments and risk missing them.

4. Explore Co-Signer Options

If your credit score isn’t ideal, or if you’re a first-time car buyer with limited credit history, considering a co-signer can be a viable strategy. A co-signer is someone with excellent credit who agrees to take legal responsibility for the loan if you fail to make payments.

Having a strong co-signer can significantly improve your chances of approval and help you secure more favorable Jfcu car loan rates. However, this is a serious commitment for the co-signer, as their credit will also be impacted if payments are missed. Discuss the implications thoroughly before proceeding.

5. Become a Jfcu Member (If You Aren’t Already)

To take advantage of Jfcu car loan rates, you’ll need to be a member. If you’re not already, look into their membership requirements. Credit unions typically have specific eligibility criteria, such as living or working in a certain area, being affiliated with a particular employer or organization, or having a family member who is already a member. Joining is usually a straightforward process, often requiring just a small initial deposit into a savings account.

Refinancing Your Existing Car Loan with Jfcu

Perhaps you already have a car loan but are looking for better terms. Refinancing your existing car loan with Jfcu could be an excellent strategy to lower your monthly payments, reduce your interest rate, or even shorten your loan term.

When is refinancing a good idea?

- Your credit score has improved: If your credit score has significantly increased since you first took out your loan, you’re likely eligible for better rates.

- Interest rates have dropped: Market interest rates fluctuate. If current rates are lower than your original loan rate, refinancing can save you money.

- You want to lower your monthly payment: Extending your loan term (though this might increase total interest) can reduce your monthly burden.

- You want to shorten your loan term: If your financial situation has improved, you might be able to afford higher payments to pay off the loan faster and save on interest.

The refinancing process with Jfcu is similar to applying for a new loan. You’ll submit an application, provide financial documents, and Jfcu will assess your eligibility and offer new terms. If approved, Jfcu will pay off your old loan, and you’ll begin making payments to Jfcu under the new, hopefully more favorable, terms.

Common Mistakes to Avoid When Applying for a Car Loan

Even with all the right information, missteps can happen. Based on my experience, here are some common pitfalls to steer clear of during your car loan journey.

- Not Checking Your Credit Score: As mentioned, this is fundamental. Going in blind can lead to accepting unfavorable terms out of ignorance.

- Skipping Pre-Approval: Without pre-approval, you lose significant negotiation power at the dealership and might feel pressured into less ideal financing options offered on-site.

- Focusing Only on Monthly Payments: While important for budgeting, fixating solely on the monthly payment can lead to longer loan terms and significantly more interest paid over time. Always consider the total cost of the loan.

- Ignoring Additional Fees: Be aware of any origination fees, documentation fees, or other charges that might be added to your loan. Always ask for a full breakdown of costs.

- Applying to Too Many Lenders at Once: Each "hard inquiry" on your credit report can slightly lower your score. While credit scoring models often group multiple auto loan inquiries within a short period (usually 14-45 days) as a single inquiry, spreading them out too much or applying for other types of credit simultaneously can be detrimental.

Beyond the Rates: What Else Jfcu Offers

While competitive Jfcu car loan rates are a primary draw, credit unions often provide a holistic financial experience that extends beyond just the loan itself. These added benefits can enhance your overall car ownership journey.

Many Jfcu branches pride themselves on offering personalized service. You can speak directly with loan officers who understand your local community and are often willing to work with you to find flexible solutions. This can be invaluable, especially if your financial situation is unique.

Jfcu might also offer financial education resources, helping members better manage their budgets, understand credit, and plan for future financial goals. Furthermore, they may provide additional products like GAP insurance (Guaranteed Asset Protection) or extended warranty options directly through their lending department, offering convenience and potentially better rates than those found at dealerships.

Pro Tips from an Expert Blogger

Having navigated countless financing scenarios, I can offer a few more insights to ensure you’re fully prepared.

- Negotiate with Confidence: Armed with your Jfcu pre-approval, you have a strong position. Don’t be afraid to negotiate the car’s price. Remember, the dealer makes money on both the sale and the financing, so separate the two as much as possible.

- Read the Fine Print: Before signing anything, meticulously review every detail of your Jfcu loan agreement. Understand the interest rate, term, monthly payment, and any prepayment penalties (though these are rare with credit unions). If you have questions, ask until you’re satisfied.

- Don’t Rush the Decision: Buying a car is a significant financial commitment. Take your time, compare offers, and ensure you’re comfortable with the terms. Don’t let high-pressure sales tactics rush you.

- Budget for Ownership Costs: Beyond the loan payment, remember to budget for insurance, fuel, maintenance, and potential repairs. A car loan is just one piece of the total cost of ownership. For more detailed insights into managing your car’s ongoing expenses, you might find our article on "Understanding Car Loan Terms: A Comprehensive Guide" incredibly helpful.

Conclusion: Drive Away Confidently with Jfcu

Securing a car loan is a crucial step in your vehicle ownership journey, and understanding Jfcu car loan rates is your key to unlocking the best possible deal. By focusing on your credit score, making a solid down payment, choosing an appropriate loan term, and meticulously preparing for the application process, you put yourself in a prime position for success.

Jfcu, with its member-centric approach and competitive offerings, stands as an excellent choice for auto financing. Their commitment to favorable rates and personalized service can make your car buying experience not just manageable, but truly advantageous.

Don’t let the financing process intimidate you. Empower yourself with knowledge, leverage the benefits of a credit union like Jfcu, and drive away in your dream car with confidence and peace of mind. Start your journey today by exploring Jfcu’s offerings – your ideal car loan might be closer than you think. For further strategies on improving your financial standing for future loans, be sure to check out our expert advice on "Boosting Your Credit Score for Better Rates."