Unlocking the Best PenFed Car Loan Rates: A Comprehensive Guide for Savvy Buyers

Unlocking the Best PenFed Car Loan Rates: A Comprehensive Guide for Savvy Buyers Carloan.Guidemechanic.com

Navigating the world of car loans can feel like a complex journey, filled with jargon, varying rates, and a multitude of lenders. For many, the dream of a new or pre-owned vehicle is often tethered to securing the most favorable financing terms. In this landscape, credit unions often stand out as beacons of competitive rates and member-centric service. Among them, Pentagon Federal Credit Union, widely known as PenFed, has established itself as a formidable player, consistently offering attractive auto loan options.

As an expert blogger and professional SEO content writer who has meticulously analyzed countless lending options, I understand the critical importance of not just finding a loan, but finding the right loan. This comprehensive guide is designed to be your ultimate resource, delving deep into everything you need to know about PenFed car loan rates. We’ll explore how they work, what factors influence them, and critically, how you can position yourself to secure the absolute best deal. Our goal is to empower you with the knowledge to make an informed decision, ensuring your next car purchase is both exciting and financially sound.

Unlocking the Best PenFed Car Loan Rates: A Comprehensive Guide for Savvy Buyers

Why PenFed Stands Out in the Auto Loan Landscape

Based on my extensive experience evaluating financial institutions, PenFed consistently emerges as a top contender for auto financing. They aren’t just another bank; they operate as a credit union, which fundamentally shifts their operational philosophy. This means they are member-owned and not-for-profit, often translating directly into more favorable rates and terms for their members compared to traditional commercial banks.

Their commitment to providing competitive PenFed car loan rates is evident across their product offerings. Whether you’re eyeing a brand-new model, a reliable used vehicle, or looking to refinance an existing loan, PenFed typically offers some of the most attractive options in the market. This focus on member benefit, combined with a strong financial foundation, makes them a go-to choice for many savvy car buyers.

Understanding PenFed Car Loan Rates: The Core Factors at Play

When you apply for an auto loan with PenFed, several key elements converge to determine the interest rate you’ll be offered. It’s not a one-size-fits-all scenario; rather, it’s a personalized assessment based on your financial profile and the specifics of the vehicle you intend to purchase. Understanding these factors is crucial for maximizing your chances of securing the most competitive PenFed auto loan rates.

1. Your Credit Score: The Ultimate Rate Decider

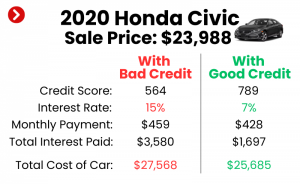

Without a doubt, your credit score is the single most influential factor in determining your car loan interest rate. Lenders, including PenFed, use this three-digit number as a quick snapshot of your creditworthiness. A higher credit score signals to them that you are a responsible borrower with a history of timely payments, thus posing a lower risk.

Conversely, a lower credit score suggests a higher risk, often resulting in higher interest rates to compensate the lender for that perceived risk. PenFed, like most lenders, categorizes applicants into tiers based on their FICO or VantageScore. Those in the "excellent" or "very good" tiers (typically 740+) will consistently qualify for the lowest advertised PenFed car loan rates, while those in lower tiers will see progressively higher rates. Pro tip from us: Always check your credit score and report before you even start shopping for a car or a loan. This gives you time to correct any errors and understand where you stand.

2. The Loan Term: Balancing Monthly Payments and Total Interest

The length of your loan, known as the loan term, plays a significant role in both your monthly payment and the total interest you’ll pay over the life of the loan. PenFed offers a range of terms, typically from 36 months up to 84 months, sometimes even longer for specific products. Shorter loan terms, such as 36 or 48 months, usually come with lower interest rates because the lender’s risk is spread over a shorter period.

However, shorter terms also mean higher monthly payments. Conversely, longer loan terms (e.g., 72 or 84 months) reduce your monthly payment, making the car more "affordable" on a month-to-month basis. The trade-off, however, is that you’ll pay significantly more in total interest over the life of the loan due to the extended repayment period and often slightly higher interest rates. It’s a delicate balance between what you can comfortably afford each month and minimizing your overall cost.

3. New vs. Used Vehicle: Age and Depreciation Matter

Generally, loans for new cars tend to have lower interest rates compared to used car loans. This isn’t arbitrary; it’s rooted in the lender’s risk assessment. New cars typically hold their value better in the initial years, are less prone to mechanical issues, and are easier to repossess and resell if a borrower defaults. This lower risk for the lender translates into better rates for you.

Used car loans, particularly for older vehicles or those with high mileage, carry a higher perceived risk. The vehicle’s value depreciates faster, and the likelihood of mechanical problems increases, potentially making it harder for the lender to recover their investment if something goes wrong. PenFed, like other lenders, will factor in the age and mileage of a used car when determining its rates, often having different rate tiers based on these specifics.

4. Loan Amount and Down Payment: Your Equity in the Deal

The total amount you borrow, relative to the car’s value, also influences your rate. If you’re borrowing a substantial amount without a significant down payment, the lender’s exposure is higher. A larger down payment reduces the loan amount and increases your equity in the vehicle from day one, signaling greater financial commitment and reducing the lender’s risk.

Based on my analysis, making a sizable down payment (typically 10-20% of the vehicle’s price) can not only lower your monthly payments but also potentially qualify you for better PenFed car loan rates. It shows financial stability and reduces the loan-to-value (LTV) ratio, which lenders view favorably.

5. PenFed Membership & Relationship: Exclusive Benefits

As a credit union, PenFed values its members and often rewards loyalty. While specific programs can change, sometimes having a long-standing relationship, maintaining other accounts (like checking or savings), or setting up direct deposit with PenFed can indirectly influence your eligibility for their best rates or special offers. This isn’t always an explicit rate discount, but a strong relationship can sometimes make a difference in the overall approval process and the terms you’re offered.

Types of PenFed Car Loans and Their Rate Implications

PenFed offers a versatile suite of auto loan products, each tailored to different purchasing scenarios. Understanding these options is key to finding the best fit for your needs and securing optimal PenFed auto loan rates.

1. New Car Loans: For the Latest Models

PenFed’s new car loans are designed for vehicles that are typically current model year or up to one or two model years old, with very low mileage. These loans often feature the most competitive interest rates due to the lower risk associated with brand-new assets. Terms can vary, but PenFed usually offers flexible repayment schedules that can go up to 84 months or sometimes even longer for high-value vehicles.

When applying for a new car loan, PenFed will consider factors like the manufacturer’s suggested retail price (MSRP) and any discounts or rebates. Securing pre-approval for a new car loan from PenFed can give you significant leverage at the dealership, allowing you to focus on negotiating the vehicle price rather than the financing.

2. Used Car Loans: Great Value, Specific Considerations

PenFed’s used car loans cater to those looking for excellent value in the pre-owned market. While rates for used cars are generally slightly higher than new car rates, PenFed remains highly competitive. Crucially, they often have specific criteria for used vehicles, such as age and mileage limits (e.g., vehicles no older than 7-8 years and with fewer than 100,000-125,000 miles).

The older the vehicle or the higher its mileage, the greater the perceived risk, which can translate into slightly higher interest rates or shorter available loan terms. However, if you’re purchasing a relatively new used car (e.g., 1-3 years old), you might still qualify for rates very close to those offered for new vehicles.

3. Auto Loan Refinancing: Lower Your Payments, Save Money

One of the most valuable services PenFed offers is auto loan refinancing. This option is perfect if you already have a car loan but believe you could secure a better interest rate or more favorable terms. Common reasons for refinancing include an improved credit score since your original loan, a significant drop in market interest rates, or a desire to lower your monthly payments by extending the loan term.

Based on my experience, many individuals overlook the potential savings from refinancing. PenFed’s competitive PenFed refinance rates can significantly reduce your total interest paid and free up cash flow each month. The process is straightforward: you apply for a new loan with PenFed to pay off your existing loan, ideally at a lower rate.

4. Lease Buyout Loans: Turning a Lease into Ownership

For those currently leasing a vehicle, PenFed also offers lease buyout loans. If you’ve enjoyed your leased car and want to purchase it at the end of your lease term, PenFed can finance the residual value (the agreed-upon purchase price at the end of the lease). This allows you to avoid returning the car and potentially paying excess mileage or wear-and-tear fees.

The rates for lease buyout loans are typically comparable to used car loan rates, as you are essentially financing a pre-owned vehicle. This can be an excellent option for maintaining continuity with a vehicle you already know and trust.

The PenFed Car Loan Application Process: A Step-by-Step Guide

Applying for a PenFed car loan is a streamlined process designed for efficiency, but understanding each step can help you navigate it smoothly. From eligibility to final approval, here’s what to expect.

1. PenFed Membership: Your First Step

Since PenFed is a credit union, you must become a member to access their financial products, including auto loans. Traditionally, PenFed’s membership was restricted to military personnel, Department of Defense employees, and certain government contractors. However, they have expanded their eligibility criteria significantly. Today, virtually anyone can join by making a small, one-time donation (often $17) to an organization like the National Military Family Association or Voices for America’s Troops.

This simple step unlocks access to all their competitive rates and services. Pro tip: Don’t let the membership requirement deter you; it’s usually very easy to fulfill and well worth the benefits.

2. Gather Your Documents: Be Prepared

Before you apply, having your financial documents organized will expedite the process. PenFed will typically require:

- Proof of Identity: Government-issued ID (driver’s license, passport).

- Proof of Income: Pay stubs, W-2s, tax returns (if self-employed).

- Employment Verification: Employer’s contact information.

- Vehicle Information: If you’ve already chosen a car, details like VIN, make, model, and mileage are needed. For pre-approval, you might just need an estimated loan amount.

- Existing Loan Information: If refinancing, your current loan statements.

Common mistakes to avoid here include providing incomplete or outdated documentation, which can cause significant delays in your application.

3. The Online Application: Quick and Convenient

PenFed offers a robust online application portal, allowing you to apply from the comfort of your home. The application asks for personal details, financial information, and your desired loan amount and term. It’s generally intuitive, guiding you through each section.

During this process, PenFed will perform a hard inquiry on your credit report. This is a normal part of the lending process, and while it might temporarily dip your score by a few points, the impact is usually minimal and short-lived, especially if you apply for all your auto loans within a concentrated "shopping window" (typically 14-45 days, depending on the credit scoring model).

4. Pre-Approval: Your Negotiating Powerhouse

One of the most valuable aspects of the PenFed application process is the ability to get pre-approved. A pre-approval means PenFed has reviewed your credit and financial situation and has conditionally approved you for a specific loan amount at an estimated interest rate. This is incredibly powerful because it separates the financing negotiation from the car price negotiation at the dealership.

With a PenFed pre-approval in hand, you walk into the dealership as a cash buyer, knowing exactly how much you can spend and what your interest rate will be. This eliminates the need to rely on the dealer’s financing and empowers you to focus purely on getting the best price for the vehicle.

Comparing PenFed Rates to Other Lenders: The Smart Buyer’s Strategy

While PenFed consistently offers competitive PenFed car loan rates, it’s always wise to compare them against other lenders. As an expert, I cannot stress this enough: shopping around is the single best strategy for securing the lowest possible interest rate.

Generally, credit unions like PenFed often beat traditional banks and dealership financing in terms of rates. Banks, being for-profit entities, tend to have slightly higher overheads and profit margins built into their rates. Dealership financing can sometimes offer promotional rates (e.g., 0% APR), but these are typically reserved for buyers with impeccable credit on specific new models and often come with trade-offs like foregoing cash rebates.

Pro tips from us: Always get at least three loan offers – one from a credit union like PenFed, one from a national bank, and one from a local bank or another credit union. This allows you to see the full spectrum of what’s available for your specific credit profile. Use online loan comparison tools, but always verify the rates directly with the lender, as advertised rates are often for the most creditworthy borrowers. For current PenFed auto loan rates, you should always check their official website directly, as rates can fluctuate based on market conditions: PenFed Auto Loan Rates.

Maximizing Your Chances for the Best PenFed Car Loan Rates

Even if you have a decent credit score, there are proactive steps you can take to enhance your eligibility for the absolute lowest PenFed auto loan rates. These strategies focus on improving your financial profile and presenting yourself as an ideal borrower.

1. Improve Your Credit Score

This is paramount. If you have time before needing a loan, work on improving your credit. Pay all bills on time, reduce outstanding credit card balances, and avoid opening new credit accounts unnecessarily. For a deeper dive into improving your credit score, check out our article on (Internal Link Placeholder). A higher score directly translates to lower rates.

2. Reduce Your Debt-to-Income (DTI) Ratio

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders use this to assess your ability to take on new debt. A lower DTI ratio (ideally below 36-40%) indicates that you have more disposable income to comfortably manage a new car payment. Pay down other debts, if possible, before applying for a car loan.

3. Make a Substantial Down Payment

As discussed, a larger down payment reduces the loan amount and increases your equity from the start. This lowers the lender’s risk and can help you qualify for better rates. Aim for at least 10-20% of the vehicle’s purchase price.

4. Choose a Shorter Loan Term (If Affordable)

While longer terms mean lower monthly payments, they often come with higher interest rates and significantly more total interest paid. If your budget allows, opting for a shorter loan term (e.g., 48 or 60 months instead of 72 or 84) can often secure you a lower interest rate.

5. Consider a Co-Signer (With Caution)

If your credit score is borderline or you’re just starting to build credit, having a co-signer with excellent credit can help you qualify for better rates. However, be aware that a co-signer is equally responsible for the loan, and any missed payments will negatively impact both your credit scores. This should only be considered with someone you trust implicitly and who understands the full implications.

Beyond the Rate: Other PenFed Auto Loan Benefits

While competitive PenFed car loan rates are a primary draw, the credit union offers additional benefits that enhance the overall borrowing experience. These often contribute to why members choose PenFed time and again.

PenFed typically boasts no application fees, which can save you a small but noticeable amount upfront. Their loan terms are often very flexible, allowing borrowers to choose a repayment schedule that aligns with their financial situation. Furthermore, as a credit union, PenFed is known for its member-centric customer service. Based on many reviews and my own observations, they generally provide excellent support throughout the application and repayment process, which can be a significant comfort for borrowers. Online account management tools are also typically robust, allowing you to easily manage your loan, make payments, and access statements digitally.

Common Mistakes to Avoid When Applying for a PenFed Car Loan

Even with all the right information, missteps can happen. Based on my experience in the lending industry, here are some common mistakes to actively avoid when seeking your PenFed auto loan:

- Not Checking Your Credit Score First: As mentioned, this is foundational. Don’t go into the application process blind. Knowing your score allows you to set realistic expectations and address any issues beforehand.

- Applying for Too Much Loan: Just because you’re approved for a certain amount doesn’t mean you should borrow it all. Overextending yourself can lead to financial strain down the road. Focus on what you need and what you can comfortably afford.

- Ignoring the Total Cost of the Loan: It’s easy to get fixated on the monthly payment, but the total interest paid over the loan term is equally, if not more, important. A slightly higher monthly payment on a shorter term often saves you thousands in the long run.

- Not Understanding All Loan Terms: Read the fine print! Understand any potential prepayment penalties (though these are rare with credit unions like PenFed), late fees, and what happens if you miss a payment.

- Failing to Get Pre-Approved: This is a powerful tool. Without pre-approval, you lose significant negotiating leverage at the dealership and risk being swayed into less favorable financing options. If you’re weighing your options between buying new or used, our detailed comparison in (Internal Link Placeholder) might help you decide which loan type is best.

Frequently Asked Questions (FAQs) About PenFed Car Loans

To round out our comprehensive guide, here are answers to some commonly asked questions about PenFed car loans:

Q: Do I have to be military to join PenFed?

A: No, not anymore. While PenFed has deep roots in the military community, their membership eligibility has expanded. You can typically join by making a small, one-time donation to a qualifying military-support organization (e.g., National Military Family Association).

Q: How long does PenFed pre-approval take?

A: PenFed’s online pre-approval process is generally very quick. In many cases, you can receive an instant decision. However, if your application requires manual review or additional documentation, it might take 1-2 business days.

Q: Can I refinance a car loan I already have with PenFed?

A: Yes, absolutely. PenFed offers competitive auto loan refinancing options. If your current loan is with another lender, or even if it’s with PenFed but your credit score has significantly improved, you might be able to secure a better rate or more favorable terms by refinancing.

Q: What credit score do I need for the best PenFed car loan rates?

A: While PenFed works with a range of credit scores, to qualify for their absolute lowest advertised rates, you’ll generally need an excellent credit score, typically 740 FICO or higher. Borrowers with good credit (670-739) can still expect very competitive rates, while those with fair credit may see higher rates but often still better than traditional banks.

Conclusion: Driving Towards Your Best Car Loan with PenFed

Securing a car loan is a significant financial decision, and choosing the right lender can impact your budget for years to come. Pentagon Federal Credit Union consistently stands out as a top-tier option, offering competitive PenFed car loan rates, flexible terms, and a member-focused approach that often surpasses traditional banks. Their commitment to providing value, combined with a straightforward application process, makes them an attractive choice for new car loans, used car loans, and refinancing alike.

By understanding the factors that influence your interest rate, preparing your financial profile, and diligently shopping around, you can significantly increase your chances of securing the best possible PenFed auto loan rates. Don’t settle for the first offer; empower yourself with knowledge and strategy. With PenFed, you’re not just getting a loan; you’re gaining a financial partner dedicated to helping you achieve your automotive dreams on favorable terms. Take the next step, explore their offerings, and drive confidently into your next vehicle purchase.