Unlocking the Best PFCU Car Loan Rates: Your Ultimate Guide to Smart Auto Financing

Unlocking the Best PFCU Car Loan Rates: Your Ultimate Guide to Smart Auto Financing Carloan.Guidemechanic.com

Securing the right car loan can feel like navigating a complex maze. With countless options available, understanding where to find the most favorable terms is crucial. If you’re considering a credit union for your next vehicle purchase, you’ve likely heard of PFCU, or a similar local credit union. These member-focused institutions often provide competitive rates and personalized service that big banks simply can’t match.

This comprehensive guide is designed to demystify PFCU car loan rates, helping you understand how they work, what factors influence them, and how you can position yourself to secure the best possible deal. We’ll dive deep into everything from eligibility to the application process, ensuring you’re equipped with all the knowledge needed to make an informed decision. Our goal is to transform you into an expert on PFCU auto loans, empowering you to drive away with confidence.

Unlocking the Best PFCU Car Loan Rates: Your Ultimate Guide to Smart Auto Financing

What Exactly Are PFCU Car Loan Rates? Understanding the Credit Union Advantage

When we talk about "PFCU car loan rates," we’re referring to the interest rates and Annual Percentage Rates (APRs) offered by a specific credit union, such as Pennsylvania Federal Credit Union, or any local credit union designated by the "PFCU" acronym in your area. Unlike traditional banks, credit unions are non-profit financial cooperatives owned by their members. This fundamental difference often translates into significant benefits for borrowers.

Because their primary goal isn’t to maximize shareholder profits, credit unions frequently pass on their earnings to members through lower loan rates, higher savings rates, and reduced fees. This cooperative model is a key reason why many savvy car buyers turn to credit unions for their auto financing needs. The focus is squarely on member well-being, fostering a more supportive lending environment.

Based on my experience in the financial industry, credit unions like PFCU consistently offer some of the most attractive car loan rates on the market. Their commitment to community and member satisfaction is often reflected in their competitive loan products. It’s not just about the numbers; it’s about a relationship built on trust and mutual benefit.

Why Credit Unions Like PFCU Excel in Auto Lending

Credit unions, including PFCU, distinguish themselves in several key areas when it comes to car loans. Their member-centric approach means they often have more flexibility in their lending criteria compared to larger, more rigid financial institutions. This can be particularly beneficial for individuals who might have unique financial circumstances.

Furthermore, the personalized service at a credit union is often a refreshing change. You’re not just a number; you’re a member of a community. This often leads to a more supportive application process and readily available assistance should you have questions or need guidance throughout the life of your loan. This human touch can make a significant difference in your borrowing experience.

Deciphering the Factors That Influence Your PFCU Car Loan Rates

Understanding what goes into determining your specific PFCU car loan rate is crucial for effective planning. There isn’t a single, universal rate; instead, several key factors come into play, tailoring the offer to your individual financial profile. Being aware of these elements allows you to strategically improve your chances of securing the best possible terms.

It’s not just about what the credit union offers; it’s also about what you bring to the table as a borrower. Every piece of your financial puzzle contributes to the final rate you’re quoted. Let’s break down the most impactful elements that PFCU and other lenders consider.

Your Credit Score: The Cornerstone of Loan Approval

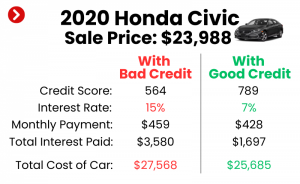

Your credit score is arguably the most significant factor influencing your PFCU car loan rates. This three-digit number, often a FICO score, serves as a snapshot of your creditworthiness, indicating how reliably you’ve managed past debts. A higher credit score signals lower risk to lenders, making you eligible for their most favorable rates.

Individuals with excellent credit scores, typically 720 and above, will almost always qualify for the lowest advertised rates. Those with good credit (670-719) will still receive competitive offers, while fair or poor credit scores may result in higher interest rates to offset the perceived increased risk. Proactively checking and improving your credit before applying is a smart move.

Loan Term: Shorter Terms Often Mean Lower Rates

The loan term, or the length of time you have to repay the loan, also plays a critical role in your interest rate. Generally, shorter loan terms (e.g., 36 or 48 months) come with lower interest rates because the lender’s money is at risk for a shorter period. While your monthly payments will be higher, the total interest paid over the life of the loan will be significantly less.

Conversely, longer loan terms (e.g., 60 or 72 months) typically carry higher interest rates. This is because the lender takes on more risk over an extended period. While longer terms offer lower monthly payments, they can lead to paying substantially more in total interest. Carefully consider the trade-off between monthly affordability and overall cost.

New vs. Used Vehicles: A Rate Differential

PFCU car loan rates often differentiate between financing a new car and a used car. Typically, new car loans tend to have slightly lower interest rates than used car loans. This is largely due to new cars holding their value better initially and generally being considered less risky collateral for the lender.

Used cars, on the other hand, often come with a slightly higher interest rate because they depreciate more rapidly and can have more unpredictable maintenance costs. The age and mileage of a used vehicle can further impact the rate. It’s important to clarify with PFCU whether their advertised rates apply to new or used vehicles, or both.

Down Payment: Your Financial Commitment

Making a substantial down payment on your car loan demonstrates your financial commitment and reduces the amount you need to borrow. This lowers the lender’s risk and can often result in a more favorable interest rate. A larger down payment means you’re financing less, which is always a good strategy.

Based on my experience, a down payment of at least 10-20% of the vehicle’s purchase price is generally recommended. It not only helps secure a better rate but also reduces your monthly payments and lessens the chance of being "upside down" on your loan, where you owe more than the car is worth. This is a common mistake to avoid.

Debt-to-Income (DTI) Ratio: Your Ability to Repay

Your debt-to-income (DTI) ratio is another crucial metric PFCU will evaluate. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have ample income to manage your existing debts and take on a new car loan comfortably.

Lenders prefer to see a DTI ratio below 36%, though some may accept up to 43% in certain circumstances. A high DTI ratio suggests you might be overextended financially, which could lead to a higher interest rate or even loan denial. Managing your existing debt before applying can significantly improve your chances.

Types of PFCU Auto Loans: Tailored to Your Needs

PFCU, like most credit unions, offers a variety of auto loan products designed to meet different member needs. Understanding these options is key to choosing the loan that best fits your situation, whether you’re buying a brand-new vehicle or refinancing an existing loan. Each type has specific characteristics and rate structures.

It’s not a one-size-fits-all approach when it comes to car financing. PFCU aims to provide flexible solutions, but it’s up to you to identify which loan category aligns with your current goals. Let’s explore the common types of auto loans you can expect to find.

New Car Loans

New car loans from PFCU are designed for financing brand-new vehicles straight from the dealership. These loans often come with the lowest interest rates due to the new car’s higher value and lower risk profile for the lender. Terms can range from short 36-month options to longer 72 or even 84-month terms.

Pro tips from us: While longer terms offer lower monthly payments, they significantly increase the total interest paid. Always consider the total cost of the loan, not just the monthly payment, when choosing a term for your new car. A good balance between affordability and minimizing interest is ideal.

Used Car Loans

PFCU also provides competitive used car loans, which are ideal for financing pre-owned vehicles. While rates might be slightly higher than for new cars, credit unions often offer better rates on used cars compared to traditional banks. The age and mileage of the used vehicle will play a role in the specific rate offered.

It’s important to note that some credit unions have limits on the age or mileage of a used car they will finance. Make sure to check PFCU’s specific criteria before you fall in love with a particular pre-owned vehicle. This ensures a smooth application process without unexpected hurdles.

Auto Loan Refinancing

If you currently have a car loan with another lender at a higher interest rate, PFCU’s auto loan refinancing options could be a game-changer. Refinancing involves taking out a new loan, often at a lower interest rate, to pay off your existing car loan. This can significantly reduce your monthly payments or the total interest you pay over time.

Based on my experience, refinancing is particularly beneficial if your credit score has improved since you first took out your original loan, or if market rates have dropped. It’s always worth exploring if you can save money, and PFCU is often a strong contender for competitive refinance rates. Don’t leave money on the table!

Lease Buyout Loans

For those who are currently leasing a vehicle and decide they want to purchase it at the end of the lease term, PFCU typically offers lease buyout loans. These loans allow you to finance the residual value of the car, effectively turning your leased vehicle into one you own outright.

The terms and rates for lease buyout loans are generally similar to those for used car loans. It’s a great option if you love your leased car and want to avoid potential excess mileage or wear-and-tear charges. Always compare the buyout price to the market value of the car to ensure it’s a financially sound decision.

Becoming a PFCU Member: Your Gateway to Competitive Rates

Before you can take advantage of PFCU car loan rates, you’ll need to become a member of the credit union. This is a fundamental difference from banks, where anyone can open an account. Credit unions have specific membership eligibility requirements, which are usually easy to meet.

Don’t let the membership requirement deter you; it’s a straightforward process that unlocks a world of financial benefits. PFCU, like many credit unions, strives to be inclusive while maintaining its member-owned structure.

Eligibility Requirements for PFCU Membership

Membership eligibility for PFCU typically falls into one of several categories. These often include:

- Geographic location: Living, working, worshipping, or attending school within a specific county or region.

- Employer affiliation: Being an employee of a select employer group (SEG) that partners with PFCU.

- Family relationship: Having an immediate family member who is already a PFCU member.

- Association membership: Being a member of a specific association or organization that has a relationship with the credit union.

Checking PFCU’s official website or contacting them directly will provide you with the most accurate and up-to-date eligibility criteria for your specific location. This is your first step towards accessing their excellent auto loan products.

The Membership Application Process

Once you confirm your eligibility, becoming a PFCU member is a simple process. You’ll typically need to open a savings account (often called a share account) with a small initial deposit, sometimes as low as $5. This deposit establishes your ownership share in the credit union.

You’ll also need to provide standard identification, such as a government-issued ID, Social Security number, and proof of address. The entire process can often be completed online or by visiting a local branch. Once you’re a member, you gain access to all of PFCU’s financial products and services, including their competitive car loans.

The PFCU Car Loan Application Process: A Step-by-Step Guide

Applying for a car loan can feel daunting, but breaking it down into manageable steps makes the process much smoother. PFCU aims to make the application as straightforward as possible for its members. Being prepared and knowing what to expect can significantly reduce stress and speed up approval.

Based on my experience, a well-prepared applicant often receives faster decisions and more favorable terms. Gather your documents, understand the requirements, and approach the process with confidence.

Step 1: Get Pre-Approved (Highly Recommended)

One of the most valuable pro tips from us is to get pre-approved for a car loan before you even set foot in a dealership. Pre-approval from PFCU gives you a clear understanding of how much you can afford to borrow, your potential interest rate, and your estimated monthly payment. It provides you with significant negotiating power at the dealership.

To get pre-approved, you’ll typically fill out an application form, either online or in person. PFCU will review your credit history, income, and debt-to-income ratio. Once approved, you’ll receive a pre-approval letter stating your maximum loan amount and interest rate, usually valid for a specific period (e.g., 30-60 days).

Step 2: Gather Necessary Documentation

When you’re ready to formally apply, or even during the pre-approval stage, PFCU will require certain documents to verify your identity, income, and financial stability. Common documents include:

- Proof of Identity: Driver’s license, state ID, or passport.

- Proof of Income: Recent pay stubs (2-3 months), W-2 forms, or tax returns if self-employed.

- Proof of Residence: Utility bill or lease agreement.

- Vehicle Information (if already selected): Make, model, year, VIN, and purchase price.

Having these documents readily available will expedite the application process. Common mistakes to avoid are not having all your documents organized, which can lead to delays.

Step 3: Complete the Application

Whether you’re applying online, over the phone, or in person at a PFCU branch, the application form will ask for detailed personal and financial information. Be sure to fill out all sections accurately and completely. Any discrepancies could raise red flags and slow down your approval.

The application will typically include questions about your employment history, current income, existing debts, and the specifics of the vehicle you intend to purchase. This information helps PFCU assess your repayment capacity and determine your final loan terms.

Step 4: Await Loan Decision and Finalize

After submitting your application, PFCU’s lending team will review your information. This usually involves a hard inquiry on your credit report. You’ll then receive a decision, which could be an approval, a request for more information, or a denial.

If approved, PFCU will provide you with the final loan terms, including the exact interest rate, APR, loan term, and monthly payment. Carefully review all the details before signing the loan agreement. Once finalized, the funds will be disbursed directly to the dealership or to you, depending on the arrangement.

Pro Tips for Securing the Best PFCU Car Loan Rates

While PFCU generally offers competitive rates, there are strategies you can employ to further enhance your chances of securing the absolute best deal. It’s about being proactive and presenting yourself as an ideal borrower. These tips are based on years of observing successful loan applications.

Don’t leave your car loan rate to chance. By implementing these strategies, you can potentially save hundreds, if not thousands, of dollars over the life of your auto loan. Every percentage point matters!

1. Boost Your Credit Score Before Applying

As previously mentioned, your credit score is paramount. Before you even consider applying, pull your credit report from all three major bureaus (Experian, Equifax, TransUnion) via AnnualCreditReport.com. Review it for any errors and dispute them immediately. Pay down existing credit card balances to lower your credit utilization.

Making all your payments on time and reducing your overall debt load will naturally improve your score. Even a 20-30 point increase can make a difference in the interest rate bracket you qualify for. For more in-depth advice, you might want to check out .

2. Save for a Significant Down Payment

A larger down payment is a powerful tool for securing better rates. It reduces the amount you need to borrow, which lowers the lender’s risk. Aim for at least 10-20% of the vehicle’s purchase price.

Beyond lowering your rate, a substantial down payment helps you build equity faster and reduces your risk of being upside down on your loan. This financial cushion is invaluable, offering peace of mind and long-term savings.

3. Choose the Right Loan Term for Your Budget and Goals

While longer loan terms offer lower monthly payments, they nearly always result in higher overall interest paid. Conversely, shorter terms mean higher monthly payments but less total interest.

Pro tips from us: Strive for the shortest loan term you can comfortably afford within your budget. This balance will minimize the total cost of your loan while keeping your monthly expenses manageable. Avoid the temptation of simply chasing the lowest monthly payment.

4. Get Pre-Approved from PFCU

Getting pre-approved by PFCU not only gives you a clear budget but also provides leverage at the dealership. You walk in knowing your financing terms, allowing you to focus purely on negotiating the car’s price, rather than being swayed by dealership financing offers that might not be as favorable.

This also allows you to compare PFCU’s pre-approval offer with any financing the dealership might present. Often, the credit union’s rates will be more competitive, empowering you to make the best financial choice.

5. Consider a Co-Signer (If Necessary)

If your credit score isn’t ideal, or if you’re a first-time borrower with limited credit history, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower interest rate. A co-signer shares responsibility for the loan, reducing the lender’s risk.

However, remember that co-signing is a serious commitment for both parties. If you, as the primary borrower, miss payments, it will negatively impact both your credit scores. Ensure open communication and a clear understanding of responsibilities if you go this route.

Common Mistakes to Avoid When Applying for a PFCU Car Loan

Even with the best intentions, it’s easy to fall into common traps when seeking auto financing. Being aware of these pitfalls can save you money, time, and stress. Based on my experience, these are some of the most frequent errors borrowers make.

Avoiding these missteps will position you for a smoother, more financially sound car loan experience with PFCU. It’s about being informed and strategic from start to finish.

1. Not Checking Your Credit Report Beforehand

Failing to review your credit report for errors or inconsistencies before applying is a common mistake. Errors, even small ones, can negatively impact your score and lead to a higher interest rate or even denial. Always dispute any inaccuracies you find.

Furthermore, not knowing your credit score means you’re going into the process blind. Knowing your score allows you to anticipate the rates you’re likely to qualify for and gives you time to make improvements if needed.

2. Focusing Only on the Monthly Payment

While a low monthly payment is appealing, it can be deceptive. Often, a very low monthly payment is achieved by extending the loan term significantly, which means you’ll pay much more in total interest over the life of the loan.

Common mistakes to avoid are not calculating the total cost of the loan (principal + total interest paid). Always consider the overall financial commitment, not just the immediate monthly outflow. Sometimes, a slightly higher monthly payment for a shorter term is the smarter financial choice.

3. Ignoring Hidden Fees and Charges

Always read the fine print of your loan agreement. Some lenders may include origination fees, application fees, or prepayment penalties. While credit unions like PFCU are generally known for transparency, it’s crucial to understand every charge associated with your loan.

Ask PFCU for a complete breakdown of all fees and charges. A lower interest rate might not be as good if it’s coupled with substantial upfront fees. Transparency is key to a fair deal.

4. Not Budgeting Properly for Car Ownership

A car loan payment is just one part of owning a vehicle. Many borrowers overlook other significant costs, such as insurance, fuel, maintenance, and registration fees. These expenses can quickly add up and strain your budget.

Pro tips from us: Create a comprehensive budget that includes all potential car ownership costs, not just the loan payment. This ensures you can comfortably afford your new vehicle without financial stress. A good rule of thumb is that your total car expenses (payment, insurance, fuel, maintenance) shouldn’t exceed 15-20% of your net monthly income.

5. Applying to Too Many Lenders at Once

While it’s smart to shop around for the best rates, applying to numerous lenders within a short period can negatively impact your credit score. Each "hard inquiry" on your credit report can cause a slight dip.

However, credit scoring models typically group multiple inquiries for the same type of loan (like a car loan) made within a 14-45 day window as a single inquiry. So, shop around but do it efficiently within a focused timeframe to minimize impact. This allows you to compare PFCU’s rates with other institutions effectively.

Beyond the Rate: Why PFCU Might Be Your Best Choice

While competitive PFCU car loan rates are a primary draw, there are other compelling reasons why choosing a credit union for your auto financing might be the best decision. The overall value proposition extends beyond just the numbers on a loan sheet.

Consider the holistic experience, the support you’ll receive, and the long-term benefits of being part of a member-owned financial institution. These intangible factors can greatly enhance your borrowing journey.

Personalized Member Service

One of the standout advantages of credit unions is their commitment to personalized service. You’re not just a transaction; you’re a valued member. This often means more attentive support, whether you have questions about your application or need assistance with your loan down the line.

Based on my experience, this level of service can make a significant difference, especially if you’re new to car financing or have unique circumstances. PFCU is likely to offer a more human-centric approach than larger, more impersonal banks.

Community Focus and Financial Education

Credit unions are deeply rooted in their communities and often invest in financial education for their members. They want to see you succeed financially, not just profit from your loans. This can translate into resources and advice that help you make better financial decisions overall.

This community focus means that PFCU is invested in the financial well-being of its members. They are often more willing to work with you during challenging times, offering flexibility that traditional banks might not.

Flexible Lending Options

Due to their member-owned structure, credit unions sometimes have more flexibility in their lending criteria. While credit score is always important, PFCU might be more willing to consider your overall financial picture, your relationship with the credit union, and other mitigating factors if your credit isn’t perfect.

This flexibility can be particularly beneficial for first-time buyers, those with a slightly less-than-perfect credit history, or individuals seeking refinancing solutions. For more information on the benefits of credit unions, you can visit the official National Credit Union Administration (NCUA) website.

Driving Away with Confidence: Your PFCU Car Loan Journey

Navigating the world of car loans can seem overwhelming, but with the right knowledge and a strategic approach, securing a great deal on your next vehicle is entirely achievable. PFCU car loan rates offer a compelling option for many, combining competitive pricing with the personalized service of a member-owned institution.

By understanding the factors that influence your rates, preparing thoroughly for the application process, and implementing our expert tips, you are now well-equipped to make informed decisions. Remember, a car loan is a significant financial commitment, and choosing a trusted partner like PFCU can make all the difference. Drive away not just with a new car, but with the peace of mind that comes from smart, well-researched financing.