Unlocking the Best RBC Car Loan Rates: Your Expert Guide to Smart Vehicle Financing

Unlocking the Best RBC Car Loan Rates: Your Expert Guide to Smart Vehicle Financing Carloan.Guidemechanic.com

Securing the right car loan can feel like navigating a complex maze, especially when you’re looking for competitive rates and a trusted lender. For many Canadians, the Royal Bank of Canada (RBC) stands out as a prominent choice. As an expert blogger and professional SEO content writer, I understand the nuances of vehicle financing, and today, we’re diving deep into everything you need to know about RBC car loan rates.

This comprehensive guide isn’t just about quoting numbers; it’s about empowering you with knowledge. We’ll explore what influences these rates, how to optimize your application, and common pitfalls to avoid. Our goal is to equip you with the insights necessary to drive away with not just a new car, but also a smart financial decision.

Unlocking the Best RBC Car Loan Rates: Your Expert Guide to Smart Vehicle Financing

The Foundation: Understanding RBC Car Loans

RBC, one of Canada’s largest financial institutions, offers a robust suite of lending products, and car loans are no exception. They provide financing solutions for a wide array of vehicle purchases, whether you’re eyeing a brand-new model, a reliable used car, or even looking to refinance an existing loan. Their extensive network and long-standing reputation make them a go-to for many Canadians seeking vehicle financing.

Choosing a major bank like RBC for your car loan often comes with the assurance of stability and a diverse range of options. They are well-equipped to handle various financial situations, offering both fixed and variable interest rate options, and flexible repayment schedules designed to fit different budgets. This flexibility is a key reason why so many turn to them.

However, understanding the mechanics behind their offerings, especially the interest rates, is crucial. It’s not just about the advertised rate; it’s about the rate you qualify for, and that’s where our expertise comes into play.

What Exactly Influences Your RBC Car Loan Rate?

This is perhaps the most critical section for anyone looking to secure a favourable loan. Your interest rate isn’t pulled out of thin air; it’s a carefully calculated figure based on several interconnected factors. Based on my experience in the financial industry, understanding these elements is your first step towards getting the best possible deal.

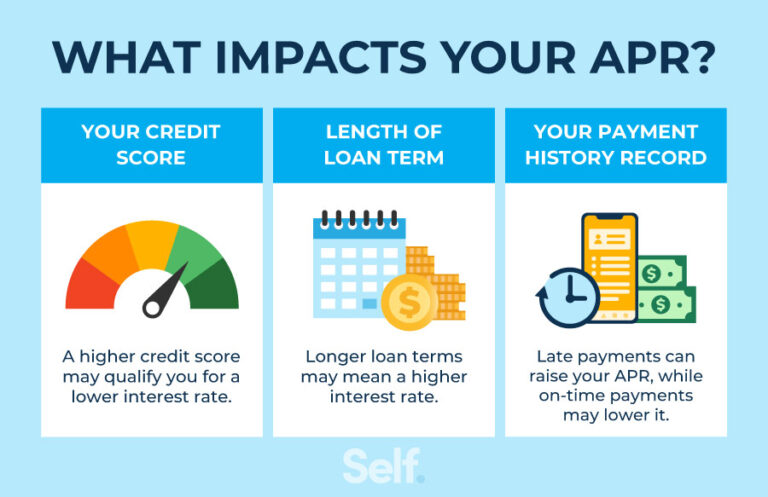

1. Your Credit Score and History

Without a doubt, your credit score is the single most significant determinant of your car loan interest rate. Lenders like RBC use this three-digit number to assess your creditworthiness – essentially, how likely you are to repay your loan on time. A higher credit score signals lower risk to the lender, which translates directly into lower interest rates.

A strong credit history, characterized by consistent on-time payments, low credit utilization, and a diverse mix of credit, is highly beneficial. Conversely, a history of missed payments, defaults, or high debt levels will push your score down, leading to higher rates as RBC tries to mitigate their perceived risk. It’s a fundamental principle of lending.

2. The Loan Term (Length of Repayment)

The loan term refers to the period over which you agree to repay your loan, typically measured in months (e.g., 48, 60, 72, or even 84 months). Generally, shorter loan terms come with lower interest rates. This might seem counterintuitive at first, as shorter terms mean higher monthly payments.

However, from the lender’s perspective, a shorter term means less time for economic conditions to change and less overall risk. You’re also paying back the principal faster, reducing the total interest accrued. While longer terms offer lower monthly payments, they often carry higher interest rates and mean you pay more over the life of the loan.

3. Your Down Payment Amount

Making a substantial down payment can significantly impact your RBC car loan rate. A larger down payment reduces the amount you need to borrow, which inherently lowers the lender’s risk. When you have more equity in the vehicle from day one, you’re less likely to default on the loan.

This reduced risk often translates into a more attractive interest rate offer. Furthermore, a larger down payment means smaller monthly payments, making the loan more manageable for you financially. It’s a win-win situation if you have the funds available upfront.

4. The Type of Vehicle You’re Buying

The specific car you’re purchasing also plays a role in your interest rate. New vehicles typically qualify for lower interest rates compared to used vehicles. This is primarily because new cars generally have a higher resale value and are less likely to require immediate costly repairs, making them a more secure asset for the lender.

Used vehicles, especially older models or those with high mileage, carry more risk for the lender due to potential maintenance issues and faster depreciation. Lenders factor in the vehicle’s age, mileage, make, and model when assessing the loan’s risk profile, which in turn influences the rate they offer.

5. Current Market Interest Rates

Beyond your personal financial profile, the broader economic environment and the Bank of Canada’s benchmark interest rate play a significant role. When the Bank of Canada raises its overnight rate, it typically leads to higher borrowing costs across the board, including for car loans. Conversely, when rates drop, car loan rates tend to follow suit.

RBC, like all financial institutions, operates within this larger economic framework. While they offer competitive rates, these rates are always influenced by the prevailing market conditions. Keeping an eye on these trends can help you decide the best time to apply.

Navigating the RBC Car Loan Application Process

Applying for an RBC car loan is a straightforward process, but being prepared can make it even smoother. Based on my experience, having all your documentation in order beforehand can significantly speed up approval.

Here’s a step-by-step breakdown:

- Research and Pre-approval: Before you even step foot in a dealership, it’s wise to research the car you want and get a pre-approval from RBC. A pre-approval gives you a clear idea of how much you can borrow and at what rate, putting you in a stronger negotiating position with sellers.

- Gather Your Documents: You’ll typically need personal identification (driver’s license, passport), proof of income (pay stubs, employment letter, tax assessments), and details about the vehicle you intend to purchase (if known).

- Complete the Application: You can apply for an RBC car loan online, over the phone, or in person at an RBC branch. The application will ask for your personal, financial, and employment details. Be honest and accurate with all information provided.

- Credit Check: RBC will perform a credit check as part of the application process. This will temporarily impact your credit score, but it’s a necessary step for any loan application.

- Review the Offer: If approved, RBC will present you with a loan offer outlining the interest rate, loan term, monthly payments, and any associated fees. Take your time to thoroughly review all terms and conditions.

- Finalize the Loan: Once you accept the offer, you’ll sign the necessary paperwork, and the funds will be disbursed. This can often be done directly with the dealership if they have a partnership with RBC.

Pro tips from us: Always read the fine print. Understand all charges, including any potential prepayment penalties or administrative fees, before signing on the dotted line. Transparency is key to a healthy financial relationship.

Strategies to Secure the Best RBC Car Loan Rates

Now that you understand what influences your rates, let’s talk strategy. You have more control than you might think over the rate you ultimately receive.

1. Boost Your Credit Score

This is your most powerful lever. Before applying for a car loan, take steps to improve your credit score. This could include:

- Paying bills on time: Consistency is paramount.

- Reducing existing debt: Especially high-interest credit card debt.

- Checking your credit report for errors: Disputing any inaccuracies can quickly boost your score.

- Avoiding new credit applications: Too many inquiries in a short period can lower your score.

Even a small improvement in your credit score can translate into significant savings on interest over the life of your loan. for more in-depth strategies.

2. Save Up for a Larger Down Payment

As discussed, a larger down payment reduces the amount borrowed and signals lower risk to RBC. Aim for at least 10-20% of the vehicle’s purchase price if possible. This not only helps with the interest rate but also reduces your monthly payments and the total interest paid over the loan term.

Consider delaying your purchase for a few months to accumulate more savings for a down payment. The long-term financial benefits often outweigh the wait.

3. Opt for a Shorter Loan Term

While higher monthly payments can be daunting, choosing the shortest loan term you can comfortably afford will almost always result in a lower interest rate and less total interest paid. Calculate different scenarios to find the sweet spot between manageable payments and interest savings.

Sometimes, a slightly higher monthly payment for a shorter duration can save you thousands of dollars in interest over the years.

4. Shop Around (Even with RBC)

Even if you’re set on RBC, it’s wise to get pre-approvals from a few different lenders. This allows you to compare offers and ensure RBC is giving you their most competitive rate. You can then use these offers as leverage, showing RBC that you have other options.

Remember, a pre-approval doesn’t commit you to a loan, but it gives you a powerful negotiation tool.

5. Consider a Co-Signer

If your credit score isn’t ideal, or if you’re a new borrower with limited credit history, having a co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower interest rate. A co-signer essentially guarantees the loan, taking on the responsibility if you default.

However, ensure both parties understand the full implications and responsibilities of co-signing a loan.

Common Mistakes to Avoid When Applying for an RBC Car Loan

Based on my years of observing borrowers, there are recurring errors that can derail your application or lead to less favorable terms. Awareness is your best defense.

- Not checking your credit score beforehand: Many people apply without knowing their credit standing, leading to disappointment or higher rates. Always get your free credit report and score before applying.

- Focusing solely on monthly payments: While important, fixating only on the monthly amount can lead to choosing longer loan terms with higher overall interest costs. Always consider the total cost of the loan.

- Ignoring the total cost of the car: Beyond the loan, remember to factor in insurance, maintenance, fuel, and registration. A cheap car loan doesn’t mean a cheap car if other costs are high.

- Applying to too many lenders at once: Multiple hard credit inquiries in a short period can negatively impact your credit score. Be strategic with your applications.

- Not being honest on your application: Providing inaccurate information can lead to rejection or even legal consequences. Always be truthful.

Pros and Cons of Choosing RBC for Your Car Loan

Like any financial product, an RBC car loan comes with its own set of advantages and potential drawbacks.

Pros:

- Trusted Brand: RBC is a well-established and reputable financial institution, offering peace of mind.

- Competitive Rates: They generally offer competitive interest rates, especially for borrowers with good credit.

- Flexible Terms: A variety of loan terms are available to suit different budgets and repayment preferences.

- Convenience: Easy application process, often integrated with dealerships, and existing RBC customers may find it even smoother.

- Customer Service: Access to their extensive branch network and customer support.

Cons:

- Strict Credit Requirements: Like most major banks, RBC may have stricter credit score requirements compared to some alternative lenders.

- Less Flexibility for Bad Credit: Borrowers with poor credit might find it challenging to qualify for their best rates or even get approved.

- Potential for Less Personalized Service: Due to their size, the loan process might feel less personalized than with a smaller, local credit union.

Beyond the Rate: Other Important Considerations

While the interest rate is crucial, it’s not the only factor to consider when evaluating an RBC car loan.

- Fees and Charges: Inquire about any administrative fees, application fees, or early repayment penalties. Some lenders charge a fee if you pay off your loan ahead of schedule.

- Prepayment Options: Can you make extra payments or pay off the loan early without penalty? This flexibility can save you a lot in interest.

- Customer Service and Support: How accessible and helpful is RBC’s customer service if you have questions or issues during your loan term?

- Insurance Requirements: Understand any specific insurance requirements RBC might have for the financed vehicle.

Comparing RBC with Other Lenders

While this article focuses on RBC, it’s always smart to have a broader perspective. Credit unions, online lenders, and even dealership financing can offer alternatives. Credit unions often provide very competitive rates, especially for their members, due to their not-for-profit structure. Online lenders can be quick and convenient, sometimes catering to a wider range of credit scores. Dealership financing can be convenient but may not always offer the absolute best rates unless there’s a special manufacturer promotion.

RBC’s strength lies in its blend of competitive rates, stability, and comprehensive service, making it a strong contender, particularly for those with good to excellent credit. Their wide range of financial products also means you can often consolidate your banking relationships. for a deeper dive into all your options.

Pro Tips from an Expert

- Get Pre-Approved: This cannot be stressed enough. It empowers you to negotiate like a cash buyer and clarifies your budget.

- Understand Your Budget: Don’t just focus on the car price; factor in insurance, fuel, maintenance, and parking. A car loan is just one part of vehicle ownership.

- Negotiate the Car Price First: Try to finalize the vehicle’s price before discussing financing. This prevents the dealership from moving numbers around to make you think you’re getting a deal.

- Be Patient: Don’t rush into a decision. Take your time to compare offers, read contracts, and ensure you’re comfortable with the terms.

Frequently Asked Questions About RBC Car Loan Rates

To further enhance your understanding, here are answers to some common questions:

Q: What is a typical RBC car loan interest rate?

A: RBC car loan interest rates vary significantly based on your credit score, the loan term, the vehicle type, and current market conditions. While they advertise starting rates, your individual rate could be anywhere from a low single digit percentage for excellent credit to a higher double digit percentage for those with less ideal credit. It’s crucial to get a personalized quote.

Q: Can I get an RBC car loan with bad credit?

A: It can be more challenging to secure an RBC car loan with bad credit, and if approved, the interest rate will likely be significantly higher. RBC, as a major bank, tends to favour borrowers with stronger credit profiles. In such cases, a co-signer or exploring specialized subprime lenders might be necessary. Improving your credit before applying is always the best approach.

Q: Does RBC offer fixed or variable interest rates for car loans?

A: RBC typically offers both fixed and variable interest rate options for car loans. A fixed rate remains the same throughout the loan term, providing predictable monthly payments. A variable rate can fluctuate with market conditions, meaning your payments could go up or down. Most borrowers prefer fixed rates for the stability they offer.

Q: How long does it take to get approved for an RBC car loan?

A: The approval time for an RBC car loan can vary. If you apply online and have all your documents ready, you might receive a conditional approval within minutes or a few hours. A full approval, especially if additional documentation is required, could take a day or two. Applying in person or through a dealership might also expedite the process.

Q: Can I refinance my existing car loan with RBC?

A: Yes, RBC offers options to refinance your existing car loan. Refinancing can be beneficial if interest rates have dropped, your credit score has improved, or you want to change your loan term. It allows you to potentially secure a lower interest rate, reduce your monthly payments, or pay off your loan faster. It’s worth exploring if your financial situation has changed since you first took out your loan. and details on their refinancing options.

Conclusion: Drive Away with Confidence

Navigating the world of car loans doesn’t have to be daunting. By understanding the factors that influence RBC car loan rates, strategically preparing your application, and avoiding common pitfalls, you can significantly improve your chances of securing a favourable deal. This comprehensive guide has aimed to provide you with the expert insights needed to make an informed decision, ensuring your vehicle purchase is not just exciting, but also financially sound.

Remember, the goal isn’t just to get a car loan, but to get the right car loan for your unique financial situation. Armed with this knowledge, you are now better equipped to approach RBC, or any lender, with confidence and clarity. Happy driving!