Unlocking the Best Tfcu Car Loan Interest Rates: Your Ultimate Expert Guide

Unlocking the Best Tfcu Car Loan Interest Rates: Your Ultimate Expert Guide Carloan.Guidemechanic.com

Navigating the world of car financing can often feel like deciphering a complex code, especially when you’re focused on securing the most favorable terms. For many, the dream of a new or used vehicle hinges significantly on understanding and optimizing their car loan interest rates. If you’re considering a vehicle loan with Tfcu, comprehending their interest rates isn’t just a smart move – it’s a crucial step towards financial empowerment.

As an expert blogger and professional SEO content writer, my goal today is to provide you with an incredibly detailed, unique, and actionable guide. We’ll delve deep into everything you need to know about Tfcu car loan interest rates, from the fundamental factors that influence them to expert strategies for securing the best possible deal. This isn’t just an overview; it’s a comprehensive roadmap designed to equip you with the knowledge to make informed decisions and achieve your automotive dreams with confidence.

Unlocking the Best Tfcu Car Loan Interest Rates: Your Ultimate Expert Guide

What Exactly Are Tfcu Car Loan Interest Rates, and Why Do They Matter?

At its core, a car loan interest rate represents the cost of borrowing money from a lender like Tfcu to purchase a vehicle. It’s expressed as a percentage of the principal loan amount, and it’s essentially the fee you pay for the privilege of using their funds over a set period. Think of it as the rental cost for the money itself.

These rates are not static; they fluctuate based on a multitude of factors, both personal and economic. Understanding what influences your specific rate is paramount because it directly impacts your monthly payment and, more significantly, the total amount you will pay over the life of the loan. A seemingly small difference in interest rate can translate into hundreds, even thousands, of dollars saved or spent. This makes grasping Tfcu car loan interest rates a critical component of smart financial planning.

The Pillars of Influence: Factors Shaping Your Tfcu Car Loan Interest Rate

When Tfcu, or any financial institution, evaluates your application for an auto loan, they assess various elements to determine the level of risk involved. This assessment directly dictates the interest rate they offer. Based on my experience in the financial content space, here are the primary factors that significantly influence your Tfcu car loan interest rate:

Your Credit Score: The Ultimate Financial Report Card

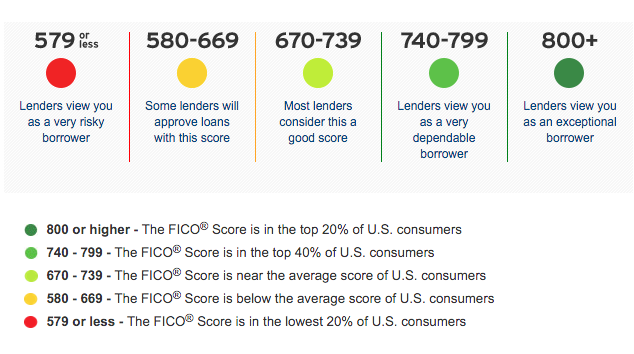

Your credit score is arguably the most significant factor in determining your interest rate. It’s a three-digit number that reflects your creditworthiness, essentially telling lenders how reliable you are at repaying debts. A higher credit score signals a lower risk to Tfcu.

For instance, an applicant with an excellent credit score (typically 720+) is likely to receive the lowest available Tfcu car loan interest rates. This is because their history demonstrates a consistent ability to manage and repay credit responsibly. Conversely, a lower credit score (below 620) suggests a higher risk, often resulting in substantially higher interest rates to compensate Tfcu for that perceived risk.

Pro tips from us: Before even approaching Tfcu for a car loan, obtain a copy of your credit report from all three major bureaus (Experian, Equifax, TransUnion). Review it meticulously for any inaccuracies or discrepancies. Disputing and correcting errors can potentially boost your score, leading to more favorable Tfcu auto loan terms.

The Loan Term: How Long Will You Be Paying?

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). This choice has a direct and often counter-intuitive impact on your interest rate. Generally, shorter loan terms tend to come with lower interest rates.

While a longer loan term might offer the allure of lower monthly payments, it usually means you’ll pay more in total interest over the life of the loan, and Tfcu may assign a slightly higher interest rate. This is because the longer the loan is outstanding, the greater the potential for unforeseen circumstances to affect your ability to repay, representing an increased risk for the lender. It’s a trade-off between monthly affordability and the total cost of borrowing.

Your Down Payment Amount: Skin in the Game

A down payment is the initial amount of money you pay upfront towards the purchase of the vehicle. It directly reduces the amount you need to borrow, thereby lowering the principal of your Tfcu car loan. From Tfcu’s perspective, a larger down payment signifies that you have more "skin in the game."

This reduces their financial exposure and often translates to a lower perceived risk. Consequently, applicants who make substantial down payments are frequently offered more attractive Tfcu car loan interest rates. It’s a clear signal of your commitment and financial stability.

Vehicle Type and Age: New vs. Used Dynamics

The type and age of the vehicle you intend to purchase also play a role in determining your interest rate. New cars often qualify for lower interest rates compared to used cars. This is primarily due to several factors.

New vehicles typically hold their value better initially, have fewer mechanical unknowns, and are easier for Tfcu to resell if they ever need to repossess them. Used cars, especially older models, present a higher risk due to potential mechanical issues and faster depreciation, leading to slightly higher Tfcu vehicle loan rates. The value of the collateral is a key consideration for any lender.

Debt-to-Income (DTI) Ratio: Your Financial Capacity

Your debt-to-income (DTI) ratio is a critical metric that lenders like Tfcu use to assess your ability to manage monthly payments. It’s calculated by dividing your total monthly debt payments by your gross monthly income. A low DTI ratio indicates that you have ample income to cover your existing debts and take on a new car loan payment.

A high DTI ratio, on the other hand, suggests that a significant portion of your income is already allocated to debt repayment, potentially making it challenging to afford additional monthly car loan payments. Lenders prefer applicants with lower DTI ratios, as they represent less of a risk of default, often qualifying them for more competitive Tfcu loan requirements and subsequently, better interest rates.

Market Conditions and Federal Reserve Rates: The Economic Pulse

Beyond your personal financial profile, broader economic forces also influence Tfcu car loan interest rates. The prevailing interest rate environment, largely influenced by the Federal Reserve’s monetary policy, sets a baseline for borrowing costs across the economy. When the Federal Reserve raises its benchmark interest rates, it generally becomes more expensive for financial institutions like Tfcu to borrow money.

This increased cost is then typically passed on to consumers in the form of higher interest rates on various loans, including car loans. Conversely, during periods of economic stimulus, when the Fed lowers rates, borrowing can become cheaper. Staying informed about these macroeconomic trends can help you time your car purchase strategically, though personal financial readiness should always take precedence.

The Tfcu Car Loan Application Process: A Step-by-Step Guide

Securing a car loan from Tfcu involves a structured process designed to ensure both you and the credit union are well-suited for the arrangement. Understanding this process can significantly streamline your journey.

Step 1: Research and Preparation

Before you even fill out an application, thoroughly research the car you want and understand its market value. Next, gather all necessary financial documents. This typically includes proof of income (pay stubs, tax returns), identification (driver’s license), proof of residency, and details about your current debts.

Common mistakes to avoid are: applying for a loan without knowing your budget or the car’s price. This can lead to loan amounts that are too high or too low for your actual needs, prolonging the process.

Step 2: Pre-Approval – Your Strategic Advantage

Many savvy car buyers start with pre-approval. This involves submitting a preliminary application to Tfcu to determine how much you can borrow and at what estimated interest rate before you even set foot in a dealership. Pre-approval gives you immense negotiating power at the dealership.

It transforms you from a mere shopper into a cash buyer, as you already have financing secured. This separation of car buying and loan negotiation is a pro tip from us, as it allows you to focus on getting the best price for the vehicle without the pressure of simultaneous financing discussions.

Step 3: Formal Application Submission

Once you’ve found your ideal vehicle and are ready to finalize, you’ll complete a formal Tfcu car loan application. This will require providing more detailed personal and financial information. Tfcu will then conduct a hard inquiry on your credit report.

This inquiry is a standard part of the lending process and is necessary for them to assess your creditworthiness accurately. Be honest and thorough in your application; any discrepancies can cause delays or even rejection.

Step 4: Reviewing the Loan Offer

If approved, Tfcu will present you with a loan offer detailing the principal amount, the interest rate, the loan term, and your monthly payment. Carefully review every aspect of this offer. Don’t hesitate to ask questions about any terms you don’t understand.

It’s crucial to understand the total cost of the loan, not just the monthly payment. This is where understanding Tfcu car loan interest rates truly pays off.

Step 5: Finalizing the Loan and Purchase

Once you’re satisfied with the terms, you’ll sign the loan documents. At this point, the funds are disbursed, and you can complete your vehicle purchase. Congratulations, you’re now the proud owner of a new vehicle!

Understanding Different Types of Tfcu Car Loans

Tfcu, like most financial institutions, offers a variety of auto loan products designed to meet different needs. While the core principles of interest rates remain, specific offerings might have nuances.

New Car Loans

These loans are specifically for brand-new vehicles purchased from a dealership. New car loans often come with the lowest Tfcu car loan interest rates due to the vehicle’s higher initial value and lower risk of immediate mechanical issues. Lenders see new cars as more reliable collateral.

Used Car Loans

Used car loans are for pre-owned vehicles. The interest rates on these loans can be slightly higher than new car loans, reflecting the increased risk associated with an older vehicle’s potential depreciation and maintenance costs. The rate will also depend heavily on the age and mileage of the used car.

Auto Loan Refinancing

If you already have a car loan with another lender or even with Tfcu, but your credit score has improved, or market rates have dropped, you might consider refinancing. Tfcu auto loan refinancing involves taking out a new loan to pay off your existing car loan, ideally at a lower interest rate or with more favorable terms. This can significantly reduce your monthly payments or the total interest paid over time.

How to Secure the Best Tfcu Car Loan Interest Rates

Getting a car loan is one thing; getting the best car loan interest rates is another. Here’s how you can position yourself for success:

1. Improve Your Credit Score

This cannot be stressed enough. A higher credit score is your golden ticket to lower interest rates. Pay all your bills on time, reduce your existing debt, and avoid opening multiple new credit accounts just before applying for a car loan. For a deeper dive into improving your credit score, check out our comprehensive guide on .

2. Save for a Larger Down Payment

As discussed, a larger down payment reduces the loan amount and signals financial strength to Tfcu. Aim for at least 10-20% of the vehicle’s purchase price if possible. This not only lowers your interest rate but also reduces your monthly payments and the total interest you’ll pay.

3. Shop Around (Even Within Tfcu)

While this article focuses on Tfcu, it’s always wise to compare offers. However, even within Tfcu, different loan products or promotions might be available. Speak to a loan officer about all your options and clearly state your financial goals. Don’t be afraid to ask if there are any special rates you might qualify for.

4. Negotiate (When Applicable)

While interest rates themselves are generally set based on risk profiles, there might be some room for negotiation on fees or specific terms, especially if you have an excellent credit history. With pre-approval in hand, you also have more leverage to negotiate the vehicle price, which indirectly impacts the total loan amount.

5. Leverage Pre-Approval

Armed with a pre-approval letter from Tfcu, you walk into the dealership with confidence. You know exactly how much you can spend and at what rate. This allows you to negotiate the car’s price more effectively, knowing your financing is already secured, which ultimately helps in securing optimal Tfcu vehicle loan rates.

Beyond the Interest Rate: Other Costs Associated with Tfcu Car Loans

While the interest rate is a major component, it’s not the only cost associated with your Tfcu car loan. Being aware of other potential expenses is crucial for a complete financial picture.

Fees and Charges

Some loans may include origination fees, documentation fees, or late payment fees. While Tfcu strives for transparency, always read the fine print. Understand what fees, if any, are built into your loan and how they might affect the total cost.

Insurance Requirements

Lenders typically require you to carry full coverage insurance (comprehensive and collision) on a financed vehicle until the loan is paid off. This protects their investment. Factor the cost of this insurance into your monthly budget, as it’s a non-negotiable expense.

Total Cost of the Loan

Always look at the total cost of the loan over its entire term, not just the monthly payment. This includes the principal amount, plus all accrued interest and any associated fees. A lower monthly payment over a longer term might seem appealing, but it often results in a significantly higher total cost due to more interest accumulation.

Pro Tips for Managing Your Tfcu Car Loan Effectively

Once you’ve secured your Tfcu car loan, effective management is key to financial success and potentially saving even more money.

- Set Up Auto-Pay: Based on my experience, setting up automatic payments is one of the easiest ways to ensure you never miss a payment. This safeguards your credit score and helps you avoid late fees. Many lenders even offer a slight interest rate discount for auto-pay enrollment.

- Make Extra Payments When Possible: Even small additional payments can make a big difference. Any extra amount you pay goes directly towards reducing your principal, which in turn reduces the total interest you’ll pay over the life of the loan. This is especially impactful in the early stages of your loan.

- Understand Your Loan Statement: Don’t just glance at the due date and amount. Take the time to understand where your payments are going – how much is principal, how much is interest, and if there are any fees. This transparency helps you stay in control of your financial journey.

- Consider Refinancing: If your credit score has improved significantly since you first obtained your loan, or if interest rates have dropped considerably, exploring Tfcu financial refinancing options could save you a substantial amount. Our article on offers further insights.

Common Myths About Car Loan Interest Rates Debunked

There are many misconceptions floating around about car loans and interest rates. Let’s clarify a few:

- Myth 1: The lowest monthly payment is always the best deal. As we’ve discussed, a low monthly payment often comes with a longer loan term, which means paying more in total interest. Always evaluate the overall cost.

- Myth 2: You need perfect credit to get a car loan. While excellent credit secures the best rates, Tfcu offers options for a range of credit scores. The key is understanding how your score impacts your rate.

- Myth 3: Dealerships always offer the best financing. While convenient, dealership financing isn’t always the cheapest. It’s vital to compare their offer with a pre-approval from Tfcu or other lenders. This comparison is how to get a car loan from Tfcu on your best terms.

Why Choose Tfcu for Your Car Loan?

Tfcu, as a credit union, often operates with a member-first philosophy. This can translate into competitive interest rates and personalized service that you might not find at larger, more impersonal banks. They are typically focused on serving their community and providing value to their members. This commitment often positions them as an excellent choice for individuals seeking fair and transparent car financing. Their approach to Tfcu loan requirements often considers individual circumstances.

Conclusion: Your Path to Informed Car Financing

Understanding Tfcu car loan interest rates is more than just knowing a number; it’s about mastering the financial landscape of your vehicle purchase. By thoroughly understanding the factors that influence your rate, diligently preparing your application, and proactively managing your loan, you empower yourself to make the smartest financial decisions.

Our expert guide has provided you with an in-depth look at every facet, from your credit score’s impact to the nuances of loan terms. Remember, securing a car loan is a significant financial commitment. Arm yourself with knowledge, leverage the expert tips we’ve shared, and approach Tfcu with confidence. Your journey to securing the best car loan rates Tfcu has to offer begins with being informed. Start planning today, get your credit in order, and drive away with the peace of mind that comes from a well-managed financial decision.