Unlocking the Dream: Your Comprehensive Guide to Achieving a 1 Percent Car Loan

Unlocking the Dream: Your Comprehensive Guide to Achieving a 1 Percent Car Loan Carloan.Guidemechanic.com

The idea of a 1 percent car loan often sounds like a mythical creature – rare, elusive, and almost too good to be true. In today’s competitive automotive market, securing financing with such an incredibly low interest rate can feel like hitting the jackpot. But is it genuinely achievable? And if so, what secret formula do you need to unlock this coveted financial deal?

As an expert blogger and professional in the world of personal finance and automotive insights, I’m here to demystify the 1 percent car loan. This comprehensive guide will delve deep into the realities, the requirements, and the strategic steps you need to take to position yourself for the absolute best car loan rates available. We’ll explore everything from credit scores to negotiation tactics, ensuring you have all the knowledge to drive away with a deal that truly benefits your wallet. Get ready to transform your understanding of car financing and potentially save thousands over the life of your vehicle loan.

Unlocking the Dream: Your Comprehensive Guide to Achieving a 1 Percent Car Loan

The Allure and Reality of the 1% Car Loan: Is It a Myth or a Masterpiece?

Let’s address the elephant in the room: can you actually get a 1 percent car loan? The short answer is yes, it is possible, but it’s far from common. These ultra-low rates are typically not standard offerings from banks or credit unions for just any borrower. Instead, they usually emerge under very specific circumstances, often tied to promotional offers.

These incredibly attractive rates are primarily manufacturer incentives. Car manufacturers, keen to boost sales of particular models, especially during slower sales periods or for outgoing models, will subsidize interest rates. This means they effectively pay a portion of the interest on your behalf to the lender, making the rate incredibly low for the consumer. It’s a powerful marketing tool designed to move inventory.

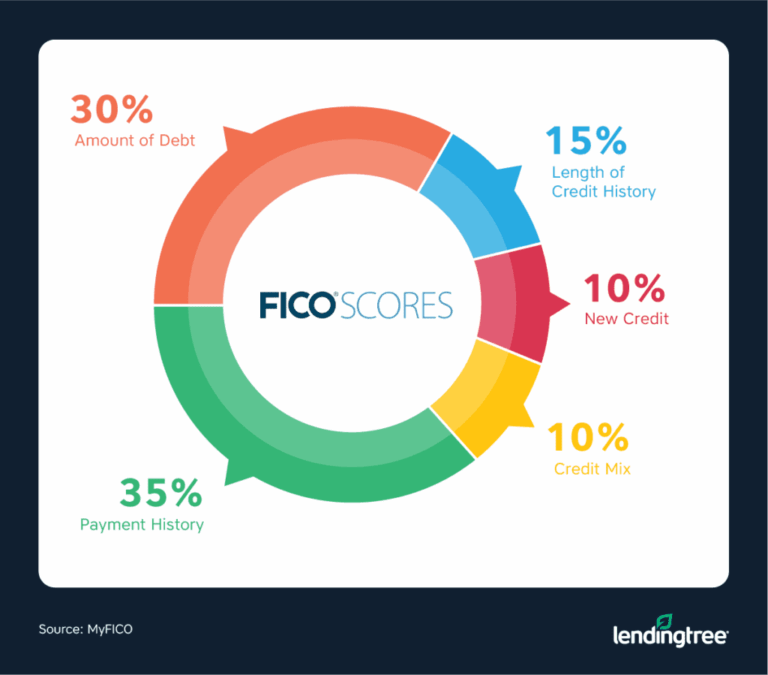

However, these deals are usually not open to everyone. They come with stringent eligibility criteria, most notably requiring an impeccable credit score. We’re talking about borrowers with excellent credit histories, often FICO scores in the high 700s or 800s. Without such a robust credit profile, these promotional rates will likely remain out of reach.

What Factors Truly Drive Your Car Loan Interest Rate?

Understanding what influences your car loan interest rate is paramount, whether you’re aiming for 1 percent or simply the best possible rate. Many variables come into play, each contributing to the final number you’re offered. Based on my experience, overlooking any of these factors can lead to significantly higher costs over the loan term.

Your credit score stands as the single most influential factor. Lenders use this three-digit number to assess your creditworthiness and the likelihood of you repaying your debt. An excellent credit score signals minimal risk, opening the door to the most competitive rates. Conversely, a lower score implies higher risk, prompting lenders to charge more to compensate for that perceived risk.

The loan term, or how long you take to repay the loan, also plays a crucial role. Generally, shorter loan terms, such as 36 or 48 months, tend to come with lower interest rates. Lenders prefer shorter terms because their money is tied up for a shorter period, reducing their exposure to risk. While a longer term might offer lower monthly payments, it almost always results in a higher overall interest rate and more total interest paid.

Your down payment significantly impacts the interest rate you’re offered. A larger down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk. When you put down a substantial amount, you demonstrate a greater commitment to the purchase and a stronger financial position. This often translates into better interest rates.

The type of vehicle you’re financing can also affect the rate. New cars typically qualify for lower interest rates compared to used cars. This is because new cars generally hold their value better initially and present less risk to the lender if repossession becomes necessary. Used cars, especially older models, carry more depreciation risk and can be seen as higher risk assets, leading to slightly higher rates.

Finally, the current market interest rates, influenced by the Federal Reserve, also set the baseline. When the Fed raises rates, borrowing costs generally increase across the board, including car loans. Conversely, when rates drop, car loans can become more affordable. This macroeconomic environment is beyond your control, but it’s important to be aware of how it impacts financing options.

How to Position Yourself for the Lowest Possible Rate (Even if Not 1%)

While a 1 percent car loan is an ambitious target, preparing yourself to secure the lowest possible rate is a realistic and highly beneficial goal. This involves strategic planning and proactive steps that demonstrate your financial responsibility to lenders. Pro tips from us: The preparation phase is just as important as the negotiation itself.

The most critical step is to improve your credit score. Before you even start looking at cars, pull your credit report from all three major bureaus (Equifax, Experian, TransUnion) and review them for accuracy. Dispute any errors immediately, as even small inaccuracies can negatively impact your score. Focus on paying all your bills on time, as payment history is the largest component of your credit score. Additionally, try to reduce any existing debt, especially high-interest credit card balances, to lower your credit utilization ratio. Avoid applying for new credit in the months leading up to your car loan application, as new inquiries can temporarily ding your score.

Saving for a larger down payment is another powerful strategy. Aiming for at least 20% of the vehicle’s purchase price is ideal. A significant down payment not only reduces the amount you need to borrow but also reduces the lender’s risk. This financial commitment shows you are serious and financially stable, often leading to more favorable interest rates. It also helps you avoid being "upside down" on your loan, where you owe more than the car is worth, a common mistake to avoid.

Choosing a shorter loan term can dramatically reduce the total interest you pay. While a 72-month or 84-month loan might offer seemingly low monthly payments, the cumulative interest can be astronomical. Opting for a 36-month or 48-month loan, if your budget allows for the higher monthly payment, will result in a much lower interest rate and significantly less interest paid over time. It’s a direct trade-off between monthly affordability and total cost.

Perhaps one of the common mistakes to avoid is only relying on dealership financing. While dealerships often have competitive offers, especially for promotional rates, it’s crucial to shop around for lenders before you visit the dealership. Obtain pre-approvals from multiple banks, credit unions, and online lenders. This not only gives you a benchmark rate but also empowers you during negotiations with the dealership. When you walk in with a pre-approval, you’re a cash buyer in the dealer’s eyes, giving you leverage. For more insights on financial preparation, you might find our article on Smart Strategies for Boosting Your Credit Score Before a Major Purchase helpful.

Finally, always be prepared to negotiate. While interest rates are largely determined by your credit and market conditions, there can still be some room for negotiation, especially with dealership financing. If you have pre-approvals, use them as leverage to ask the dealer to beat or match the lowest rate you’ve found. Don’t be afraid to walk away if the deal isn’t right for you.

The Pros and Cons of Ultra-Low Interest Rates

Securing an ultra-low interest rate, such as 1 percent, comes with a multitude of benefits that can significantly impact your financial well-being. However, it’s also important to be aware of potential downsides or caveats that might accompany such an attractive offer. Understanding both sides ensures you make a fully informed decision.

On the positive side, the most obvious benefit is a significantly lower total cost of ownership. With minimal interest accruing, the vast majority of your monthly payments go directly towards paying down the principal balance of the car. This means you’re essentially paying almost the exact sticker price for the vehicle, rather than adding thousands in interest over time. This leaves more money in your pocket, which can be saved, invested, or used for other essential expenses.

Furthermore, a low interest rate allows you to build equity in your car much faster. Since less of each payment is consumed by interest, your ownership stake in the vehicle grows more rapidly. This is particularly advantageous if you ever need to sell or trade in the car before the loan is fully paid off, reducing the risk of being "upside down" on your loan. It also provides a sense of financial savvy and accomplishment, knowing you’ve secured an exceptional deal.

However, these ultra-low rates often come with restrictive terms. They are typically reserved for specific new car models, sometimes even particular trim levels, that the manufacturer is trying to push. This means you might not be able to apply this fantastic rate to the exact car you truly want or need. You might feel pressured to choose a vehicle simply because it qualifies for the 1 percent offer, rather than one that best fits your lifestyle and budget.

Another significant drawback is the exclusivity. As mentioned, these rates almost invariably require an impeccable credit score, often excluding a large segment of the car-buying population. If your credit isn’t in the top tier, you won’t qualify, regardless of how appealing the offer seems. Additionally, sometimes these super low interest rates might be offered in lieu of other incentives, such as cash rebates or dealer discounts. It’s crucial to calculate whether taking the 1 percent rate or a larger cash discount (and financing at a slightly higher rate) results in a lower overall cost for you. Always do the math to compare offers thoroughly.

Beyond the Interest Rate: Other Crucial Loan Considerations

While the interest rate is undeniably important, focusing solely on this number can lead to overlooking other critical aspects of your car loan. A truly smart borrower understands that the overall cost and terms of the loan are determined by several intertwined factors. Pro tips from us: Always read the fine print!

One of the most common points of confusion is the difference between the Annual Percentage Rate (APR) and the interest rate. The interest rate is simply the cost of borrowing the principal amount. The APR, however, is a more comprehensive measure of the cost of your loan, as it includes not only the interest rate but also any additional fees charged by the lender, such as origination fees, documentation fees, or other closing costs. Always compare APRs when evaluating loan offers, as this provides a truer picture of the total cost. You can learn more about how the Consumer Financial Protection Bureau advises on understanding auto loans at their official website here.

Be vigilant about various loan fees that lenders might impose. These can include application fees, processing fees, or even charges for specific services. While some fees are standard, others might be negotiable or could be avoided by choosing a different lender. Always ask for a full breakdown of all fees associated with the loan before signing any documents. Don’t be shy about questioning anything you don’t understand or that seems excessive.

Another crucial consideration is whether your loan includes any prepayment penalties. Some lenders charge a fee if you pay off your loan early, effectively penalizing you for being financially responsible. If you anticipate having extra funds to pay down your loan faster, ensure your loan agreement allows for early repayment without any additional charges. This flexibility can save you money in the long run.

Finally, be wary of optional add-ons that dealers often present at the financing stage. These can include extended warranties, GAP insurance, paint protection, or credit life insurance. While some of these might offer value, many are overpriced and can significantly inflate your loan amount, leading to more interest paid. Evaluate each add-on carefully, research its true cost and benefit, and never feel pressured to accept something you don’t genuinely need or want. For a deeper dive into these additional costs, our article on Understanding Car Loan Fees and Hidden Costs can provide more valuable insights.

Is Refinancing an Option for a Lower Rate?

Even if you didn’t secure an ultra-low interest rate initially, refinancing your car loan can be a powerful strategy to reduce your monthly payments and the total interest paid. This option is particularly appealing if your financial circumstances have improved since you first financed your vehicle. Based on my experience, many people overlook this valuable opportunity.

You should consider refinancing if your credit score has significantly improved since you took out the original loan. A better credit score signals lower risk to new lenders, making you eligible for more competitive rates. Similarly, if market interest rates have dropped since your initial purchase, you might be able to secure a lower rate through refinancing. Another common scenario is if you simply rushed into a loan without proper research and ended up with a higher-than-average rate.

Refinancing essentially means taking out a new loan to pay off your existing car loan. The new loan will typically have a different interest rate and potentially a new loan term. The process usually involves applying with various lenders, comparing their offers, and then completing the paperwork for the new loan. Once approved, the new lender pays off your old loan, and you begin making payments to the new lender under the new, hopefully more favorable, terms.

The benefits of refinancing can be substantial. A lower interest rate translates directly to less money spent on interest over the life of the loan. This can either reduce your monthly payments, freeing up cash flow, or allow you to pay off the loan faster by keeping your payments the same but directing more towards the principal. However, be mindful of any fees associated with the new loan and ensure that extending the loan term doesn’t inadvertently lead to paying more interest in the long run, even with a lower rate.

Driving Away with Confidence: Your Path to a Smarter Car Loan

The quest for a 1 percent car loan, while challenging, is a testament to the power of informed decision-making in personal finance. We’ve uncovered that these ultra-low rates are indeed real, often driven by manufacturer incentives and reserved for those with impeccable credit scores. However, even if 1 percent remains just out of reach, the strategies discussed here empower you to secure the absolute best rate possible for your individual circumstances.

Remember, preparation is key. Cultivating a strong credit profile, saving for a substantial down payment, and meticulously shopping around for lenders are non-negotiable steps. Beyond the interest rate, a savvy borrower always scrutinizes the APR, understands all associated fees, avoids prepayment penalties, and judiciously evaluates optional add-ons. By doing so, you’re not just getting a car loan; you’re securing a financial agreement that aligns with your long-term goals.

Ultimately, your goal isn’t just to get a car; it’s to acquire it on the most favorable terms possible. By applying the insights from this guide, you’re well-equipped to navigate the complexities of auto financing with confidence and expertise. Drive away not just with a new vehicle, but with the satisfaction of making a truly smart financial decision.

Have you ever secured an incredibly low car loan rate? What strategies worked best for you? Share your experiences and tips in the comments below!