Unlocking the Dream: Your Credit Score For 0 Interest Car Loan

Unlocking the Dream: Your Credit Score For 0 Interest Car Loan Carloan.Guidemechanic.com

Imagine driving off the lot in a brand-new car, knowing you won’t pay a single cent in interest on your loan. This isn’t just a fantasy; it’s the reality for a select group of car buyers who qualify for a 0% APR (Annual Percentage Rate) car loan. These coveted deals can save you thousands over the life of your loan, making your dream car even more attainable.

However, securing a 0 interest car loan isn’t a walk in the park. It requires more than just wanting a great deal; it demands an impeccable financial profile, with your credit score playing the starring role. In the competitive world of auto financing, lenders reserve these premium offers for their lowest-risk customers.

Unlocking the Dream: Your Credit Score For 0 Interest Car Loan

As an expert blogger and professional SEO content writer, I’ve delved deep into the nuances of auto financing. Based on my experience and extensive research, this comprehensive guide will unpack everything you need to know about qualifying for a 0 interest car loan. We’ll explore the specific credit score requirements, other crucial eligibility factors, and actionable strategies to position yourself for success. Get ready to transform your car buying experience!

The Allure of 0% APR Car Loans: What Makes Them So Desirable?

A 0% APR car loan, often marketed as "no interest financing," means exactly what it sounds like: you pay back only the principal amount of the loan, with no additional cost for borrowing the money. This contrasts sharply with standard car loans, where interest can add a significant sum to your total vehicle cost over several years. The appeal is undeniable, offering substantial savings.

For example, on a $30,000 car loan at 5% APR over five years, you would pay approximately $3,950 in interest. With a 0% APR loan, that $3,950 stays in your pocket. This makes 0% APR deals incredibly attractive, as they drastically reduce your overall financial burden. You can allocate those saved funds towards a larger down payment, higher trim level, or simply keep them for other expenses.

These special financing offers are typically promotional deals provided by car manufacturers, often in collaboration with their captive finance companies (e.g., Toyota Financial Services, Honda Financial Services). They are designed to stimulate sales, particularly for new models or to clear out inventory at the end of a model year. While they sound too good to be true, they are legitimate offers for those who meet the stringent qualifications.

The Cornerstone: Your Credit Score Explained

Before we dive into the specific credit score for 0 interest car loan requirements, let’s establish a foundational understanding of what a credit score is and why it holds so much weight in lending decisions. Your credit score is a three-digit number, primarily calculated by models like FICO and VantageScore, that summarizes your creditworthiness. It acts as a quick snapshot for lenders, indicating how reliably you’ve managed debt in the past.

Lenders use your credit score as a primary tool to assess risk. A higher score signifies a lower risk of default, making you a more attractive borrower. Conversely, a lower score suggests a higher risk, which typically leads to higher interest rates or even loan denial. This risk assessment is critical because lenders want to ensure they will be repaid.

Your credit score is influenced by several key factors: your payment history (the most impactful), the amount of debt you owe (credit utilization), the length of your credit history, new credit applications, and your credit mix (types of credit accounts). Understanding these components is the first step toward strategically managing your credit for optimal financial opportunities. Don’t just know your score; understand what it means and how it’s built.

What Credit Score Do You REALLY Need for a 0% APR Car Loan?

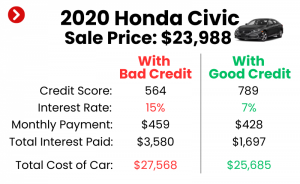

This is the million-dollar question for many car buyers. While there isn’t a single, universally published magic number, our expert insights suggest that to qualify for a 0 interest car loan, you will almost certainly need an excellent credit score. This generally means a FICO score of 740 or higher, with many lenders specifically looking for scores in the 760-800+ range.

Lenders offering 0% APR deals are looking for borrowers who present virtually no risk of default. An excellent credit score indicates a long history of responsible credit management, including consistent on-time payments, low credit utilization, and a diverse, well-managed credit portfolio. These top-tier borrowers are considered "prime" or "super prime" customers. Anything less than excellent credit, even what might be considered "very good" (e.g., 700-739), often won’t make the cut for these exclusive offers.

Based on my experience in the financial industry, dealers and manufacturers offering these deals are not just looking for a high number; they’re looking for the quality of the credit history behind that number. This includes a substantial length of credit history (often 5+ years), no recent delinquencies, bankruptcies, or foreclosures, and a very low debt-to-income ratio. It’s not merely about having a good credit score for a car loan; it’s about having one of the best.

Common mistakes to avoid are assuming that a "good" credit score (typically 670-739) will suffice, or that a single high score is enough without a solid history to back it up. These 0% APR offers are reserved for the financial crème de la crème, those who have proven themselves to be exceptionally reliable borrowers over an extended period. If your score falls below this elite tier, don’t despair, but adjust your expectations accordingly.

Beyond the Score: Other Factors Lenders Consider for 0% APR

While an excellent credit score is paramount, it’s not the only piece of the puzzle. Lenders scrutinize several other factors to determine your eligibility for a 0 interest car loan. These additional criteria ensure that even with a stellar credit score, you have the overall financial stability to manage the loan.

One critical factor is your debt-to-income (DTI) ratio. This ratio compares your total monthly debt payments to your gross monthly income. Lenders prefer a low DTI, typically under 36%, indicating that you’re not overextended financially and have ample income to cover new loan payments. A high DTI, even with a great credit score, can signal potential difficulty in managing additional debt.

Stable employment and a consistent income are also non-negotiable. Lenders want to see a reliable income stream, often requiring proof of employment for at least two years with the same employer. This demonstrates your ability to make regular payments without interruption. Freelancers or those with erratic income might find it more challenging to qualify, even with a high credit score, due to perceived income instability.

A significant down payment can also bolster your application. While not always strictly required for 0% APR, putting down a substantial amount (e.g., 20% or more) reduces the loan amount and the lender’s risk. This can sometimes tip the scales in your favor, especially if your credit profile is on the border of "excellent."

Furthermore, the type of vehicle and loan term often play a role. 0% APR offers are almost exclusively for new cars, specific models, or models the manufacturer is trying to move quickly. You’ll rarely find these deals on used vehicles. Moreover, these offers usually come with shorter loan terms, typically 36 or 48 months, sometimes up to 60 months. Longer loan terms (e.g., 72 or 84 months) are almost never associated with 0% APR, as they increase the lender’s risk over time.

Finally, the depth and breadth of your credit history are important. It’s not enough to have a high score for a short period. Lenders prefer to see a well-established credit history with various types of accounts (credit cards, mortgages, previous auto loans) managed responsibly over many years. This demonstrates a consistent pattern of financial discipline.

Strategies to Improve Your Credit Score for a 0% APR Car Loan

If your credit score isn’t quite in the "excellent" range yet, don’t lose hope. Building and improving your credit is a marathon, not a sprint, but consistent effort can lead to significant gains. Proactive credit management is key to positioning yourself for the best financing deals, including that elusive 0 interest car loan.

The first step is to check your credit report regularly. You can obtain your free credit report annually from each of the three major credit bureaus (Experian, Equifax, and TransUnion) through a trusted source like AnnualCreditReport.com. Review these reports meticulously for any errors or inaccuracies. Disputing and correcting mistakes can sometimes provide an immediate boost to your score.

Secondly, and most crucially, pay all your bills on time, every time. Payment history is the single most influential factor in your credit score. Even one late payment can have a significant negative impact. Set up automatic payments, reminders, or use budgeting apps to ensure you never miss a due date. This demonstrates reliability to potential lenders more than anything else.

Next, reduce your credit utilization ratio. This refers to the amount of credit you’re using compared to your total available credit. Keep your credit card balances as low as possible, ideally below 30% of your credit limit across all cards. For an excellent credit score, aiming for under 10% is even better. Paying down existing debt significantly lowers your utilization, signaling responsible borrowing.

Avoid opening too many new credit accounts in a short period, especially in the months leading up to a car loan application. Each new credit application results in a hard inquiry on your credit report, which can temporarily ding your score. Too many inquiries can make you appear risky to lenders.

Lastly, maintain a good credit mix and let your credit history age. Having a combination of different types of credit (e.g., credit cards, installment loans) shows you can manage various financial products responsibly. The longer your credit accounts have been open and in good standing, the better it looks to lenders. Patience is key here; building a robust credit history takes time and consistent good behavior.

Pro tips from us: Consider setting up payment alerts on your phone or email to ensure you never miss a deadline. If you’re just starting your credit journey, a secured credit card can be an excellent tool to build positive payment history without much risk. For a deeper dive into improving your credit, check out our guide on .

Navigating the 0% APR Landscape: Tips for Success

Even with an excellent credit score, securing a 0% APR car loan requires strategic planning and careful negotiation. These deals are designed to benefit the dealer and manufacturer as much as the buyer, so it’s essential to approach them with a clear understanding of the process.

Shop around and compare offers from different dealerships and manufacturers. 0% APR deals are often limited to specific models or trim levels and can vary by region or even by month. Don’t assume that one dealer’s offer is the only one available. Research current manufacturer incentives online before you even step foot on a lot.

Get pre-approved for a traditional car loan from your bank or credit union before visiting the dealership. This serves two purposes: it gives you a strong negotiating position, as you’ll know your lowest achievable interest rate, and it provides a backup plan if you don’t qualify for the 0% APR offer. Having pre-approval demonstrates your seriousness and financial preparedness. If you’re exploring different financing paths, our article on offers valuable insights.

Always read the fine print meticulously. Sometimes, a 0% APR offer might come with conditions, such as a higher vehicle price or reduced room for negotiation on the car itself. Dealers might be less willing to discount the car’s sticker price if they’re already losing potential interest revenue on the loan. Ensure the overall deal, including the vehicle price and any fees, is still competitive.

Be realistic about your qualifications. If your credit score is borderline or falls below the excellent threshold, don’t get fixated solely on 0% APR. While the allure is strong, pursuing an unattainable deal can lead to multiple hard inquiries on your credit, which can negatively impact your score. Focus on securing the lowest possible interest rate that aligns with your current credit profile.

A common mistake is getting so excited about the 0% APR that you overlook the actual price of the car. Sometimes, a dealer might offer 0% APR but be unwilling to budge on the car’s price. You might find a better overall deal by taking a slightly higher, but still low, interest rate on a car that’s significantly discounted. Always calculate the total cost of ownership, not just the interest rate.

What If You Don’t Qualify for 0% APR?

It’s important to remember that not everyone will qualify for a 0 interest car loan, even with good credit. If you don’t meet the stringent requirements, don’t despair! There are still many excellent financing options available that can save you money.

Firstly, focus on securing the lowest achievable interest rate for which your credit profile qualifies. This often means exploring options beyond manufacturer financing. Credit unions, for example, are renowned for offering competitive interest rates to their members. Banks and online lenders also provide a wide range of car loan products.

Even if you don’t get 0% APR, a low-interest conventional loan is still a fantastic financial win. Every percentage point you save on interest translates into more money in your pocket. Continue to prioritize building and maintaining excellent credit for future purchases. Your efforts will pay off over time, opening doors to even better financial products down the line.

Consider putting down a larger down payment to reduce your loan amount and potentially secure a lower interest rate. A larger down payment also builds equity faster and reduces your monthly payments. For guidance on navigating other financing options, explore our article on .

Conclusion

Securing a 0 interest car loan is indeed a financial achievement, offering substantial savings and making car ownership more affordable. However, it’s a privilege reserved for those with exceptional financial discipline and an impeccable credit score. Typically, a FICO score of 740 or higher, often well into the 760-800+ range, is the gateway to these coveted deals.

Beyond the credit score, factors like a low debt-to-income ratio, stable employment, and a healthy down payment all contribute to your eligibility. By understanding these requirements and proactively managing your credit, you can position yourself as a prime candidate for the best financing options available.

Remember, whether you qualify for 0% APR or a very low-interest conventional loan, the ultimate goal is smart financial decision-making. Always compare offers, read the fine print, and consider the total cost of the vehicle. By taking control of your credit and being an informed buyer, you can unlock incredible savings and drive away with confidence. Your journey to a smarter car purchase starts with a strong credit foundation!