Unlocking the Dream: Your Ultimate Guide to Securing a 1.9 APR Car Loan

Unlocking the Dream: Your Ultimate Guide to Securing a 1.9 APR Car Loan Carloan.Guidemechanic.com

The thought of buying a new car often brings with it the excitement of a fresh start, new adventures, and the open road. But beneath the shiny paint and comfortable interiors lies a critical financial decision: how to finance it. For many, the ultimate goal is to secure a 1.9 APR Car Loan, a rate so appealing it can significantly reduce the total cost of ownership and make that dream vehicle a more affordable reality.

A 1.9 APR (Annual Percentage Rate) car loan represents an exceptionally low borrowing cost, placing it squarely in the "prime" category of auto financing. It’s the kind of rate that turns heads and can save you thousands over the life of your loan. But is it truly within reach, and what does it take to qualify for such a coveted offer? This comprehensive guide will demystify the 1.9 APR car loan, providing you with the expert insights and actionable steps needed to navigate the financing landscape successfully.

Unlocking the Dream: Your Ultimate Guide to Securing a 1.9 APR Car Loan

We’ll dive deep into what this rate means for your wallet, explore the crucial factors influencing your eligibility, and walk you through a step-by-step process to maximize your chances of approval. Get ready to transform your car buying experience from a daunting task into an empowering journey towards financial savviness.

Understanding APR: More Than Just a Number

Before we embark on the quest for a 1.9 APR car loan, it’s essential to grasp what APR truly signifies. Many people use "interest rate" and "APR" interchangeably, but there’s a subtle yet significant difference that can impact your total loan cost.

APR vs. Interest Rate: The Key Distinction

The interest rate is the percentage a lender charges you for borrowing money, typically expressed annually. It’s the core cost of the loan itself. However, the Annual Percentage Rate (APR) provides a more comprehensive picture of your borrowing costs.

APR includes not only the interest rate but also any additional fees or charges associated with the loan, such as administrative fees, origination fees, or other lender-specific costs. By bundling these into a single percentage, APR offers a standardized way to compare the true cost of different loan offers. A lower APR always means a lower overall cost of borrowing.

The Significance of a 1.9% APR in Today’s Market

A 1.9% APR car loan is considered an outstanding rate, especially in an environment where interest rates can fluctuate. This low figure means that for every $10,000 you borrow, you’re paying only $190 in interest annually, assuming no other fees are rolled in beyond what’s reflected in the APR. Compared to rates of 5%, 7%, or even higher, the savings are substantial.

Based on my experience, securing such a low APR can dramatically reduce your monthly payments and the total amount you repay over the loan term. It’s a clear indicator that you are a highly desirable borrower in the eyes of lenders, signaling minimal risk. This is why it’s often seen as the "holy grail" of car financing.

Is a 1.9 APR Car Loan Realistic for You? Factors Influencing Eligibility

While the 1.9 APR car loan is highly desirable, it’s not universally accessible. Lenders reserve these prime rates for borrowers who present the lowest risk. Understanding the key factors that influence your eligibility is the first step toward positioning yourself for success.

Your Credit Score: The Ultimate Gatekeeper

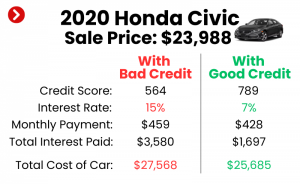

Your credit score is arguably the most critical factor in securing a low APR car loan. Lenders use this three-digit number to assess your creditworthiness – your history of repaying debts responsibly. To qualify for a 1.9% APR, you’ll almost certainly need an "excellent" credit score.

Typically, an excellent credit score falls in the range of 780 to 850 on the FICO scale. Scores in this bracket indicate a consistent track record of on-time payments, low credit utilization, and a healthy mix of credit accounts. Without a strong credit profile, lenders perceive a higher risk, and consequently, offer higher interest rates.

Debt-to-Income Ratio (DTI): A Measure of Affordability

Lenders don’t just look at your ability to repay past debts; they also scrutinize your current financial capacity. Your Debt-to-Income (DTI) ratio is a crucial metric that compares your total monthly debt payments to your gross monthly income. A low DTI indicates that you have ample income left after covering your existing obligations, making new debt more manageable.

For prime rates like 1.9% APR, lenders generally prefer a DTI ratio of 36% or less, though some might go slightly higher for exceptionally strong credit profiles. A high DTI suggests you might be stretched thin financially, increasing the risk of default in the lender’s eyes. Ensuring your DTI is healthy demonstrates your financial stability.

Loan Term: Shorter Paths to Lower Rates

The length of your loan, known as the loan term, also plays a significant role in determining your APR. Generally, shorter loan terms often come with lower interest rates. This is because a shorter term reduces the lender’s exposure to risk over time.

For instance, a 36-month or 48-month loan is more likely to qualify for a 1.9% APR than a 72-month or 84-month loan. While shorter terms mean higher monthly payments, they also mean less interest paid over the life of the loan. It’s a trade-off between monthly affordability and total cost.

Down Payment: Reducing Lender Risk and Your Loan Amount

Making a substantial down payment is one of the most effective ways to lower your loan amount and, by extension, potentially qualify for a better APR. A larger down payment reduces the amount you need to borrow, which decreases the lender’s risk. It also demonstrates your financial commitment to the purchase.

Lenders use a metric called Loan-to-Value (LTV) ratio, which compares the loan amount to the car’s value. A high down payment results in a lower LTV, making your loan more attractive to lenders. Aiming for 10-20% or more as a down payment can significantly strengthen your application for a 1.9 APR car loan.

Vehicle Type & Age: New Car Perks

While it’s possible to find low APRs on used cars, promotional rates like 1.9% APR are most commonly offered on new vehicles. This is often due to manufacturer incentives designed to boost sales of specific models. New cars also hold their value better initially and have less mechanical uncertainty, making them less risky collateral for lenders.

Used car loans typically carry slightly higher interest rates due to the vehicle’s depreciation and potential for unforeseen maintenance issues. If your heart is set on a 1.9 APR, focusing your search on new cars, particularly those with current manufacturer promotions, might be your best bet.

Pro tips from us: Always check your credit report from all three major bureaus (Equifax, Experian, and TransUnion) well in advance of applying for a loan. Look for any errors and dispute them promptly, as even small inaccuracies can negatively impact your score.

The Journey to Securing a 1.9 APR Car Loan: A Step-by-Step Guide

Securing a premium rate like 1.9% APR requires a strategic approach. It’s not just about asking for it; it’s about preparing yourself to be the ideal candidate. Follow these steps to maximize your chances.

Step 1: Credit Health Check-up and Optimization

Your credit score is your most powerful tool. Before you even start looking at cars, pull your credit reports from AnnualCreditReport.com. Review them meticulously for any discrepancies or errors that could be dragging your score down.

If you find errors, dispute them immediately with the respective credit bureau. Beyond corrections, actively work on improving your score: pay all bills on time, reduce existing debt, and avoid opening new credit accounts in the months leading up to your car loan application. A strong credit score is non-negotiable for a 1.9 APR.

Step 2: Budgeting and Down Payment Strategy

Knowing what you can truly afford is paramount. Create a detailed budget that accounts for your monthly income, fixed expenses, and variable costs. This will help you determine a comfortable monthly car payment that won’t strain your finances.

Simultaneously, start saving aggressively for a down payment. The more you put down, the less you borrow, and the more attractive you appear to lenders. A significant down payment also reduces your Loan-to-Value (LTV) ratio, which is favorable for securing lower rates.

Step 3: Get Pre-Approved (Multiple Lenders)

One of the smartest moves you can make is getting pre-approved for a loan before stepping into a dealership. Pre-approval gives you a clear understanding of the interest rate you qualify for based on your credit profile. It also provides leverage during negotiations, as you’ll have an external offer to compare against the dealership’s financing.

Apply to multiple lenders – banks, credit unions, and online lenders – within a short timeframe (typically 14-45 days, depending on the scoring model). Multiple inquiries within this "rate shopping" window are usually treated as a single hard inquiry on your credit report, minimizing the impact on your score. This allows you to compare offers and find the most competitive rate.

Step 4: Dealership vs. External Lenders: Weighing Your Options

With your pre-approval in hand, you’re ready to compare financing options. Dealerships often offer attractive promotional rates, sometimes even 0% APR, especially on new vehicles. These are typically manufacturer-backed incentives designed to clear inventory.

However, don’t assume the dealership’s offer is always the best. Compare it meticulously with your pre-approved offers from external lenders. Sometimes, a dealership might offer a slightly higher APR but give you a better deal on the car’s purchase price, or vice-versa. Common mistakes to avoid are accepting the first offer without comparison or focusing solely on the monthly payment without understanding the full loan terms.

Step 5: Negotiating & Finalizing the Loan

Once you’ve decided on a car and secured the best financing offer (ideally a 1.9 APR car loan!), it’s time to finalize the paperwork. Read the loan agreement thoroughly before signing. Understand all terms, conditions, and any potential fees.

Be wary of last-minute add-ons like extended warranties, paint protection, or credit insurance, which can inflate your total loan amount and negate the benefit of a low APR. If you want these products, negotiate them separately and ensure they are genuinely valuable to you. Your focus should be on the agreed-upon vehicle price and the 1.9 APR loan terms.

Unlocking Special 1.9 APR Car Loan Offers: Manufacturer Incentives

A significant number of 1.9 APR car loan opportunities come directly from auto manufacturers. These are not standard rates offered by every bank but special promotions designed to stimulate sales of specific models.

How Manufacturer Incentives Work

Automakers often collaborate with their captive finance arms (e.g., Toyota Financial Services, Honda Financial Services) to offer ultra-low interest rates, sometimes as low as 0% or 1.9% APR, on new vehicles. These incentives are typically tied to specific models, model years, or even trim levels that the manufacturer wants to sell quickly. They are a powerful tool to attract buyers, especially during slower sales periods or when new models are about to be released.

These offers are usually for a limited time and might require specific loan terms, such as 36 or 48 months. They are almost exclusively for buyers with excellent credit, as the manufacturer is essentially subsidizing the interest rate to make the car more appealing.

When and Where to Find These Deals

To find these coveted 1.9 APR car loan deals, keep an eye on manufacturer websites, local dealership advertisements, and reputable automotive news sites. They are often advertised prominently during major holiday sales events (e.g., Memorial Day, Fourth of July, year-end sales) or at the end of a model year.

It’s worth noting that sometimes these low APR offers are mutually exclusive with other incentives, such as cash rebates. You might have to choose between a low APR and a cash discount, so calculate which option saves you more money overall.

What If You Don’t Qualify for 1.9 APR? Alternatives and Improvement Strategies

While a 1.9 APR car loan is the gold standard, not everyone will qualify immediately. Don’t be discouraged if your initial offers are higher. There are still excellent alternatives and strategies to improve your financial standing for future opportunities.

Aiming for Competitive, Not Just Prime, Rates

If 1.9% APR isn’t on the table, focus on securing the lowest competitive rate available to you. Even an APR of 3-5% is considered very good for many borrowers, especially on used cars or with good (but not excellent) credit. Every percentage point you save on interest adds up over the life of the loan.

Compare offers from multiple lenders diligently. A small credit union might offer a slightly better rate than a large bank, or vice-versa. Explore all avenues to find the most favorable terms for your specific credit profile.

Strategies for Future Improvement

Even if you accept a higher APR now, your financial journey doesn’t end there. You can actively work on improving your credit score and financial health. Pay all your bills on time, every time. Reduce your credit card balances to lower your credit utilization. Avoid opening new lines of credit unnecessarily.

Over time, as your credit score improves and your financial situation stabilizes, you may become eligible for a lower APR. This brings us to the next crucial strategy: refinancing.

For more strategies on improving your credit score, check out our guide on . This article provides detailed, actionable advice to help you build a stronger credit profile over time.

The Fine Print: What to Watch Out For

Even with a fantastic 1.9 APR car loan, it’s vital to read and understand every detail of your loan agreement. Lenders are required to disclose all terms, but it’s your responsibility to scrutinize them.

Hidden Fees and Charges

While APR aims to be comprehensive, some fees might still be separate or less obvious. Look out for:

- Prepayment penalties: Though rare with simple interest auto loans, some older or less conventional loans might charge a fee for paying off your loan early. This can negate some of the benefits if you plan to pay it off ahead of schedule.

- Late payment fees: Understand the grace period and associated charges for missed payments.

- Documentation fees (Doc Fees): These are common at dealerships but can vary wildly. While often non-negotiable, knowing what you’re paying for is important.

Understanding Loan Disclosures

The loan disclosure statement will outline your total loan amount, total interest paid, monthly payment, and the final APR. Take the time to confirm these numbers match your understanding and expectations. Don’t hesitate to ask questions if anything is unclear.

Ensuring you comprehend the full scope of your financial commitment protects you from unexpected costs down the line. Understanding your rights as a consumer is crucial. The Consumer Financial Protection Bureau (CFPB) offers excellent resources on auto loans, including guides on what to look for in your loan agreement: . This external resource provides valuable, unbiased information to empower you as a borrower.

Real-World Scenarios and Case Studies

To illustrate the impact of credit and strategy on securing a 1.9 APR car loan, let’s look at a few hypothetical scenarios.

Scenario A: The Ideal Borrower

Sarah has an excellent credit score of 810, a low DTI of 25%, and a steady income. She has saved a 20% down payment for a new sedan and is looking for a 48-month loan term. She applied for pre-approval at three different credit unions and found a manufacturer-backed 1.9% APR offer at the dealership. Because her financial profile is impeccable, she easily qualifies for the 1.9 APR car loan, resulting in low monthly payments and significant interest savings.

Scenario B: Good Credit, Slightly Higher Rate

Mark has a good credit score of 720, a DTI of 38%, and a 10% down payment for a slightly used SUV. While he doesn’t qualify for the promotional 1.9% APR on new cars, his strong credit still allows him to secure a competitive 3.5% APR from an online lender. He plans to make extra payments to reduce his principal faster and aims to refinance in a year if his credit score improves further.

Scenario C: Fair Credit, Building Towards Better Rates

Jessica has a fair credit score of 650, has some student loan debt, and is purchasing her first car. She has a modest 5% down payment. She receives loan offers ranging from 7% to 9% APR. While not ideal, she understands that by making all payments on time and improving her credit utilization, she can work towards refinancing to a lower APR in the future. She chooses a reliable used car within her budget and commits to improving her financial habits.

Refinancing Your Car Loan to a Lower APR

Even if you don’t secure a 1.9 APR car loan from the outset, refinancing offers a powerful second chance. This process involves taking out a new loan to pay off your existing car loan, ideally at a lower interest rate.

When is Refinancing a Good Idea?

Refinancing is particularly beneficial if:

- Your credit score has significantly improved since you took out your original loan.

- Interest rates have dropped in the market.

- You initially accepted a high APR due to limited options or urgency.

- You want to change your loan term (e.g., shorten it to pay less interest, or lengthen it to lower monthly payments).

By securing a lower APR, you can reduce your monthly payments, decrease the total interest paid over the life of the loan, or both. It’s a smart financial move that can save you hundreds, if not thousands, of dollars.

How to Qualify for a Lower APR Through Refinancing

The qualification process for refinancing is similar to your initial car loan application. Lenders will review your credit score, DTI, and the value of your vehicle. To secure a significantly lower rate, ideally approaching that coveted 1.9 APR, you’ll need to demonstrate improved creditworthiness. This means a higher credit score, a stable income, and a good payment history on your current auto loan.

Considering refinancing? Our comprehensive article on can help guide your decision, offering detailed steps and considerations for this important financial move.

Conclusion: Your Path to a 1.9 APR Car Loan is Clear

Securing a 1.9 APR car loan is an achievable goal for many, but it requires diligent preparation, a solid understanding of financial principles, and strategic execution. It’s not just about finding a good deal; it’s about being a strong, low-risk borrower that lenders are eager to finance.

By focusing on an excellent credit score, a healthy debt-to-income ratio, a significant down payment, and exploring all available lender options, you significantly enhance your chances. Remember to scrutinize all loan documents and understand every detail before committing.

Whether you qualify for a 1.9 APR car loan from the start or work towards it through strategic credit improvement and refinancing, the knowledge gained from this guide empowers you. Drive away with confidence, knowing you’ve made a financially sound decision for your new vehicle. Your journey to smart car financing starts now!