Unlocking the Driver’s Seat: Your Ultimate Guide to Maximizing Your Odds of Car Loan Approval

Unlocking the Driver’s Seat: Your Ultimate Guide to Maximizing Your Odds of Car Loan Approval Carloan.Guidemechanic.com

Dreaming of a new set of wheels, but feeling a little daunted by the car loan process? You’re not alone. The journey to car ownership often begins with securing financing, and understanding the odds of car loan approval is your first, most crucial step. It’s not just about filling out an application; it’s about presenting yourself as a reliable borrower.

This comprehensive guide is designed to demystify car loan approvals, offering you an insider’s look at what lenders truly prioritize. We’ll delve deep into every factor, from your credit score to your employment history, providing actionable insights to significantly boost your chances. By the time you finish reading, you’ll be equipped with the knowledge and strategies to navigate the financing landscape with confidence and drive away in your dream car.

Unlocking the Driver’s Seat: Your Ultimate Guide to Maximizing Your Odds of Car Loan Approval

The Foundation: What Lenders Really Look For in a Car Loan Applicant

When you apply for a car loan, lenders aren’t just looking at a number; they’re assessing your overall financial reliability and your ability to repay the debt. They want to minimize their risk, and several key factors come into play. Understanding these elements is fundamental to improving your odds of car loan approval.

Based on my experience in the automotive and financial industries, these are the pillars upon which every car loan decision rests. Let’s break them down one by one, explaining not just what they are, but why they matter so much.

1. Your Credit Score: The Unofficial Report Card of Your Financial Life

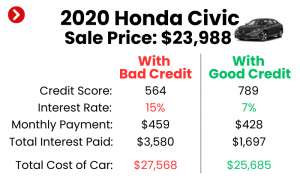

Your credit score is arguably the most influential factor in determining your car loan approval odds and the interest rate you’ll be offered. This three-digit number, typically ranging from 300 to 850 (FICO and VantageScore are the most common models), is a snapshot of your creditworthiness. A higher score signals less risk to lenders.

Generally, scores above 660 are considered good, while those above 720 are excellent. Lenders use this score to quickly gauge your history of managing debt. A strong score demonstrates a consistent pattern of timely payments and responsible credit use.

For instance, someone with an excellent credit score (760+) will almost always receive better interest rates and more favorable terms than someone with a fair (600-650) or poor (below 600) score. This translates directly into lower monthly payments and significant savings over the life of the loan. It’s truly the "big kahuna" of car loan approval factors.

2. Your Credit History: More Than Just a Number

While your credit score provides a quick overview, lenders also scrutinize your full credit history. This detailed report reveals the story behind the score, including your payment history, the types of credit you’ve used, and the length of your credit relationships. They want to see consistent, positive behavior over time.

A history of on-time payments, especially on previous car loans or similar installment loans, is a huge plus. It shows you’re capable of handling a significant monthly obligation. Conversely, late payments, defaults, or bankruptcies will significantly diminish your approval odds and likely result in higher interest rates, if approved at all.

Lenders also look at your credit mix – a healthy blend of revolving credit (credit cards) and installment loans (mortgages, student loans) demonstrates versatility in managing different types of debt. The longer your positive credit history, the better, as it provides a more robust picture of your financial habits.

3. Debt-to-Income Ratio (DTI): Are You Overextended?

Your Debt-to-Income (DTI) ratio is a crucial metric that tells lenders how much of your gross monthly income goes towards paying your existing debts. It’s calculated by dividing your total monthly debt payments by your gross monthly income. For example, if your debts (rent/mortgage, credit card minimums, student loan payments) total $1,500 and your gross income is $5,000, your DTI is 30%.

Lenders use DTI to assess your capacity to take on additional debt, like a new car loan. A high DTI indicates that a large portion of your income is already committed, making it riskier for you to manage another payment. Most lenders prefer a DTI of 36% or less, though some might go up to 43% for well-qualified borrowers.

A lower DTI signifies that you have more disposable income available to comfortably cover your car loan payments. This significantly boosts your confidence in your ability to repay and, consequently, your odds of car loan approval. It’s a direct indicator of financial breathing room.

4. Income Stability and Employment History: Can You Keep Paying?

Lenders want assurance that you have a steady, reliable source of income to make your monthly payments. Your employment history provides this confidence. They typically look for at least two years of consistent employment with the same employer or within the same industry. Frequent job changes, especially if they involve significant gaps or career shifts, can raise red flags.

Proof of income, such as recent pay stubs, W-2 forms, or tax returns, will be required. For self-employed individuals, a longer history of consistent income (often two years of tax returns) is usually needed to demonstrate stability. The higher and more stable your income, the more comfortable lenders will be with extending you a loan.

A stable job history indicates financial responsibility and a predictable income stream. This significantly reduces the perceived risk for the lender, making your application much more appealing.

5. Down Payment: Skin in the Game

Making a down payment on a car loan is one of the most effective ways to improve your odds of car loan approval, especially if your credit isn’t perfect. A down payment reduces the amount you need to borrow, thereby lowering the lender’s risk. It also demonstrates your commitment to the purchase and your ability to save.

From the lender’s perspective, a substantial down payment means less money financed and a lower loan-to-value (LTV) ratio. If you were to default, the car’s value would more easily cover the outstanding loan amount. Pro tips from us: aiming for at least 10-20% of the vehicle’s purchase price is ideal.

Not only does a down payment boost your approval chances, but it also results in lower monthly payments and less interest paid over the life of the loan. It’s a win-win situation that shows financial prudence.

6. Vehicle Age and Value: The Collateral Factor

The car itself plays a role in the approval process because it serves as collateral for the loan. Lenders consider the vehicle’s age, mileage, and overall market value. Newer, lower-mileage vehicles generally hold their value better and are easier to finance. This is because their depreciation curve is more predictable, and they’re less likely to require immediate costly repairs that could strain your budget.

Older vehicles or those with very high mileage can be harder to finance, as their resale value is lower and their risk of mechanical issues is higher. Some lenders have restrictions on the maximum age or mileage they will finance. They want to ensure that the collateral (the car) is sufficient to cover the loan amount if you default.

Therefore, choosing a vehicle that aligns with your financial profile and the lender’s risk assessment can subtly yet significantly impact your approval.

Boosting Your Odds: Practical Strategies for Higher Car Loan Approval Chances

Now that you understand what lenders are looking for, let’s explore actionable strategies to enhance your application. These steps can proactively improve your financial standing and present you as an ideal candidate, dramatically increasing your odds of car loan approval.

1. Get Pre-Approved: Your Secret Weapon

One of the most powerful steps you can take is to get pre-approved for a car loan before you even set foot in a dealership. Pre-approval involves a lender reviewing your financial information and offering you a conditional loan amount and interest rate. This doesn’t commit you to that lender, but it gives you a firm offer in hand.

The benefits are numerous. First, it clarifies your budget, so you know exactly how much car you can afford. Second, it gives you significant negotiating power at the dealership, as you already have financing secured. Third, it reduces the stress of the car-buying process, allowing you to focus on finding the right vehicle.

Common mistakes to avoid are applying to too many lenders at once, which can slightly ding your credit score. Instead, apply to 2-3 reputable lenders within a 14-day window; credit bureaus often count these as a single inquiry for score calculation.

2. Improve Your Credit Score: The Long Game Pays Off

If your credit score isn’t where you want it to be, taking steps to improve it can dramatically boost your approval odds and secure better rates. This isn’t an overnight fix, but consistent effort yields significant rewards. Start by obtaining a copy of your credit report from all three major bureaus (Experian, Equifax, TransUnion) and check for errors. Dispute any inaccuracies immediately.

Focus on paying all your bills on time, every time. Payment history is the biggest factor in your score. Reduce your credit card balances to lower your credit utilization ratio (the amount of credit you’re using compared to your total available credit), ideally keeping it below 30%. Avoid opening new credit accounts unnecessarily, as this can temporarily lower your score. For more on improving your credit score, check out our guide on .

Even a modest improvement in your score can move you into a better rate tier, saving you thousands over the life of the loan. This due diligence is a direct investment in your financial future.

3. Save for a Larger Down Payment: The Power of Savings

As discussed, a larger down payment signals financial stability and reduces lender risk. If you’re not in a rush to buy a car, take the time to save up a significant down payment. Aim for 10-20% of the vehicle’s purchase price, or even more if you can manage it.

This strategy is particularly effective if you have a lower credit score, as it helps offset some of the perceived risk. It also means you’ll be borrowing less money, resulting in smaller monthly payments and less interest accumulating over time. A larger down payment can often be the deciding factor in pushing your application from denial to approval.

It’s a tangible demonstration of your financial discipline and commitment. This "skin in the game" shows lenders you’re serious about your obligation.

4. Reduce Existing Debt: Lighten Your Load

Before applying for a car loan, take a critical look at your existing debts. Actively working to pay down credit card balances, personal loans, or other outstanding obligations can significantly improve your DTI ratio. A lower DTI indicates that you have more income available to manage new loan payments, making you a more attractive borrower.

Prioritize high-interest debts first to maximize your impact. This strategy not only improves your car loan approval chances but also frees up more of your monthly income for other financial goals. It’s a smart move for your overall financial health, not just for car loan approval.

This strategic debt reduction directly addresses a key lender concern: your capacity to comfortably handle new financial commitments.

5. Consider a Co-signer: A Helping Hand

If you have limited credit history or a less-than-perfect credit score, adding a co-signer with excellent credit can dramatically improve your odds of car loan approval. A co-signer essentially guarantees the loan, promising to make payments if you default. This significantly reduces the lender’s risk.

However, choosing a co-signer is a serious decision. Pro tips from us: Ensure your co-signer fully understands their responsibility, as the loan will appear on their credit report, and their credit will be impacted if you miss payments. It should be someone you trust implicitly and who trusts you equally.

While a co-signer can open doors, it’s not a decision to be taken lightly due to the shared financial and credit responsibility. Only consider this option if you are absolutely confident in your ability to make every payment on time.

6. Choose the Right Vehicle: Practicality Over Aspiration

While it’s tempting to eye that luxury sedan or high-performance SUV, choosing a vehicle that aligns with your financial reality can significantly impact your approval odds. Lenders are more comfortable financing reasonably priced, reliable vehicles, especially for borrowers with less robust financial profiles.

An overly expensive car, particularly if it’s outside the norm for your income level, can make lenders wary. They might perceive it as an irresponsible financial decision, regardless of your other qualifications. Opting for a more affordable, practical vehicle reduces the loan amount, thereby lowering your monthly payments and overall risk. If you’re unsure about budgeting for a new car, our detailed article on can help.

This strategic choice demonstrates financial maturity and a realistic approach to car ownership.

The Application Process: What to Expect and How to Prepare

Once you’ve taken steps to improve your financial standing, the next phase is the actual application. Knowing what to expect and having your documents ready will make the process smoother and more efficient.

1. Gather Your Documents: Be Prepared

Lenders will require various documents to verify your identity, income, and residence. Having these ready beforehand will expedite the application. Common requirements include:

- Proof of Identity: Driver’s license, state ID, or passport.

- Proof of Income: Recent pay stubs (usually 1-2 months), W-2 forms, tax returns (especially for self-employed individuals).

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Social Security Number: For credit checks.

- Vehicle Information: (If you’ve already chosen a car) VIN, make, model, year, mileage.

Being organized shows responsibility and allows the lender to process your application without delays.

2. Shop Around for Lenders: Don’t Settle for the First Offer

Just as you’d shop for the best car, you should shop for the best loan. Don’t limit yourself to the dealership’s financing, though it can be convenient. Explore options from:

- Banks: Your personal bank might offer competitive rates.

- Credit Unions: Often known for lower interest rates and more personalized service for their members.

- Online Lenders: Many online platforms specialize in car loans and can offer quick approvals.

Comparing offers will ensure you get the most favorable terms and interest rate, saving you money in the long run.

3. Understand Loan Terms: APR, Loan Term, and Total Cost

Before signing any agreement, thoroughly understand the loan terms. Pay close attention to:

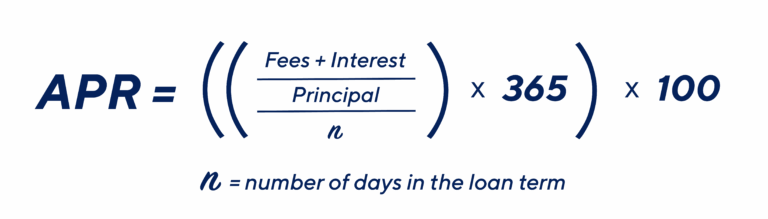

- Annual Percentage Rate (APR): This is the true cost of borrowing, including interest and any fees. A lower APR means lower overall costs.

- Loan Term: The length of time you have to repay the loan (e.g., 48, 60, 72 months). Longer terms mean lower monthly payments but more interest paid over time.

- Total Cost of the Loan: Calculate how much you’ll pay in total over the loan’s life, including principal and interest.

Don’t be afraid to ask questions until you fully grasp every detail.

4. Read the Fine Print: Avoid Surprises

Always read the entire loan agreement carefully before signing. Look for any hidden fees, prepayment penalties (fees for paying off the loan early), or balloon payments. Common mistakes to avoid are rushing through this critical step or relying solely on verbal assurances.

Ensure that all terms discussed and agreed upon are explicitly written in the contract. If something seems unclear, ask for clarification. This diligence protects you from unexpected costs and ensures you fully understand your commitment.

Navigating Challenges: What if Your Car Loan Application is Denied?

Even with the best preparation, sometimes applications are denied. This isn’t the end of the road; it’s an opportunity to learn and strategize for future success.

1. Understand the Denial Reason: Your Legal Right

If your loan application is denied, the lender is legally required to provide you with an Adverse Action Notice. This notice will explain the specific reasons for the denial. It might be due to a low credit score, high DTI, insufficient income, or a short credit history.

Understanding the precise reason is crucial. It pinpoints the area you need to work on, making your next application more targeted and successful. Don’t just accept "denied"; demand the "why."

2. Steps to Take After Denial: Re-evaluate and Reapply

Once you know why you were denied, you can formulate a plan.

- Improve the Identified Weakness: If it was your credit score, focus on paying down debt and making on-time payments. If it was DTI, work on reducing other debts or increasing your income.

- Consider a Co-signer: If suitable, this could be the solution.

- Lower Your Expectations: Perhaps the car you applied for was too expensive. Consider a more affordable vehicle.

- Save More for a Down Payment: A larger down payment can often sway a lender.

Don’t reapply immediately to the same lender without addressing the underlying issues, as repeated denials can negatively impact your credit score. Take a few months to implement changes.

3. Alternative Options (with Caution):

If traditional loans remain out of reach, a few alternatives exist, but they come with caveats:

- "Buy Here, Pay Here" Dealerships: These dealerships offer in-house financing, often without stringent credit checks. However, they typically charge very high interest rates and may have unfavorable terms. Use these only as a last resort and read every line of the contract.

- Secured Personal Loans: You might be able to get a personal loan secured by another asset (like savings) and use that to buy a car. This still requires good credit for reasonable rates.

- Save Up to Buy Cash: The most financially sound option is to save until you can purchase a reliable used car outright. This avoids interest entirely.

Exercise extreme caution with "buy here, pay here" options, as they can quickly lead to a cycle of debt if not managed carefully.

Pro Tips for Long-Term Financial Health and Car Ownership

Securing a car loan is just the beginning. Responsible car ownership involves ongoing financial management.

- Budgeting for Car Payments: Ensure your car payment (including insurance, fuel, and maintenance) fits comfortably within your monthly budget. A good rule of thumb is that your total car expenses shouldn’t exceed 10-15% of your gross monthly income.

- Maintaining Good Credit Post-Loan: Continue to make all your payments on time, not just your car loan. This builds a strong credit history, which will be beneficial for future financial endeavors, such as a mortgage or other loans.

- Refinancing Options: If your credit score significantly improves after a year or two of on-time car loan payments, consider refinancing your car loan. You might qualify for a lower interest rate, which can save you a substantial amount of money over the remaining loan term.

By consistently demonstrating financial responsibility, you not only manage your current car loan effectively but also pave the way for a more secure financial future.

Conclusion: Driving Towards Your Automotive Dreams with Confidence

The journey to car ownership doesn’t have to be fraught with anxiety. By understanding the key factors influencing the odds of car loan approval and proactively implementing smart financial strategies, you can significantly enhance your chances. From meticulously managing your credit score and history to making a substantial down payment and diligently researching lenders, every step you take brings you closer to securing the best possible loan terms.

Remember, knowledge is power. Armed with the insights from this comprehensive guide, you are now equipped to approach the car loan process with confidence, make informed decisions, and ultimately, drive away in the car that suits your needs and your budget. Your financial future, and your new car, await!