Unlocking the Loan Labyrinth: What Is The Longest Car Loan You Can Get?

Unlocking the Loan Labyrinth: What Is The Longest Car Loan You Can Get? Carloan.Guidemechanic.com

Buying a car is a significant financial decision, and for many, securing the right car loan is a crucial step. As monthly payments become a primary concern, the temptation to extend the loan term to reduce those payments can be incredibly strong. But just how long can you really stretch out a car loan? What is the longest car loan you can get, and more importantly, is it a wise financial move?

As expert bloggers and professional SEO content writers, we delve deep into the world of car financing. We understand the allure of lower monthly payments, but also the potential pitfalls. This comprehensive guide will explore the maximum car loan terms available, dissect their pros and cons, and provide you with the insights needed to make an informed, financially sound decision.

Unlocking the Loan Labyrinth: What Is The Longest Car Loan You Can Get?

Understanding Car Loan Terms: The Foundation

Before we discuss the absolute maximum, let’s establish a baseline. A car loan term refers to the length of time you have to repay the loan, typically expressed in months. Common car loan terms have historically ranged from 36 to 60 months (3 to 5 years). These terms balance manageable monthly payments with a reasonable total interest paid over the life of the loan.

However, in recent years, as vehicle prices have steadily climbed, lenders have adapted by offering extended loan terms. This shift aims to keep new and even late-model used cars within reach for a broader range of buyers. The idea is simple: spread the total cost over a longer period, and your monthly payments shrink.

The Upper Limit: How Long Can Car Loans Really Get?

The direct answer to "What is the longest car loan you can get?" is complex, as it depends on several factors, including the lender, your creditworthiness, and the vehicle itself. However, based on current market trends and our extensive experience, we can identify the typical maximums.

84-Month (7-Year) Car Loans: The New Standard for Extended Terms

For most consumers with good credit, an 84-month car loan has become a widely available option. This seven-year term is offered by many banks, credit unions, and even dealership finance departments. It represents the most common "extended" loan term you’ll encounter today.

Lenders are generally comfortable with 84-month terms for newer vehicles, especially those with strong resale value. This term length significantly lowers monthly payments compared to a 60-month or 72-month loan, making more expensive vehicles seem affordable.

96-Month (8-Year) Car Loans: Less Common, But Possible

While less prevalent than 84-month options, 96-month car loans are increasingly being offered by some lenders, particularly for high-value new vehicles. These eight-year terms are a relatively new development in the auto finance landscape. They push the boundaries of traditional car loan durations.

Qualifying for a 96-month loan typically requires excellent credit and a stable financial history. Lenders offering these terms are taking on a longer-term risk, so they will scrutinize your application more thoroughly.

Beyond 96 Months: Rare and Often Risky

Loans exceeding 96 months, such as 100 or even 120 months (over 8 years), are exceptionally rare. When they do appear, they are often tied to very specific circumstances, such as extremely high-value luxury vehicles or niche lenders specializing in such products.

From our perspective, such extended terms carry substantial risks for the borrower, which we will detail shortly. While technically possible in very limited scenarios, they are not a common or recommended path for the average car buyer.

Why Would Someone Want an Extended Car Loan? The Allure of Lower Payments

The primary driver behind the demand for extended car loan terms is simple: affordability. As vehicle prices continue to rise, many buyers find that a traditional 60-month loan results in monthly payments that strain their budget. An extended term provides a seemingly immediate solution.

Lower Monthly Payments: This is the most significant benefit. By spreading the total cost of the car over a longer period, each individual payment becomes smaller. This can free up cash flow for other expenses or allow a buyer to afford a more feature-rich or expensive vehicle that would otherwise be out of reach. Based on my experience, many buyers gravitate towards longer terms primarily for the immediate relief of a smaller monthly outlay.

Access to Better Vehicles: A lower monthly payment can open the door to a newer, safer, or more luxurious vehicle. Buyers might upgrade from a basic model to one with advanced safety features, better fuel economy, or enhanced comfort, believing the extended term makes it financially viable.

Budget Flexibility: For some, the reduced monthly payment offers greater financial flexibility. It can help maintain a healthier emergency fund or allow for investments in other areas, even if the total cost of the car increases over time. This perceived flexibility can be very attractive to budget-conscious consumers.

The Hidden Costs and Major Downsides of Long Car Loans

While the appeal of lower monthly payments is undeniable, it’s crucial to look beyond the surface. Extended car loans come with significant financial drawbacks that can accumulate over time. Common mistakes to avoid are focusing solely on the monthly payment without considering the long-term financial implications.

1. Significantly More Interest Paid: This is arguably the most critical disadvantage. When you extend the loan term, you are paying interest for a longer period. Even if the interest rate is the same, the total amount of interest paid over an 84-month loan will be substantially higher than on a 60-month loan for the same principal amount.

Pro tips from us: Always calculate the total cost, not just the monthly payment. A lower monthly payment can mask a much larger overall expenditure. This hidden cost can add thousands of dollars to the total price of your vehicle.

2. Higher Risk of Being Upside Down (Negative Equity): This is a very common and dangerous trap with long car loans. Most cars depreciate rapidly, especially in the first few years. With an extended loan, your car’s value often depreciates faster than you pay down the principal.

Being "upside down" or having "negative equity" means you owe more on the car than it’s worth. This becomes a problem if your car is totaled in an accident (your insurance payout might not cover the remaining loan balance) or if you want to trade it in before the loan is paid off (you’ll have to roll the negative equity into your next loan, compounding the problem).

3. Longer Period of Debt: An 84-month or 96-month loan means you’ll be making car payments for seven or eight years. That’s a substantial portion of your financial life tied to one asset. This prolonged debt can hinder your ability to save for other financial goals, such as a down payment on a home, retirement, or your children’s education.

4. Increased Maintenance Costs: As your car ages, it will inevitably require more maintenance and repairs. With a long loan term, you could be making car payments on a vehicle that is well past its warranty period and is starting to incur significant repair costs. Imagine still making car payments on a 7 or 8-year-old vehicle that needs a major transmission overhaul. This scenario is all too common.

5. Limited Flexibility for Upgrading: If your financial situation or family needs change, you might want to upgrade your vehicle sooner than anticipated. With a long loan, you’re often locked into your current car due to the negative equity issue. Trading in a vehicle with negative equity means you’ll either have to pay the difference out of pocket or roll it into your next loan, creating a cycle of debt.

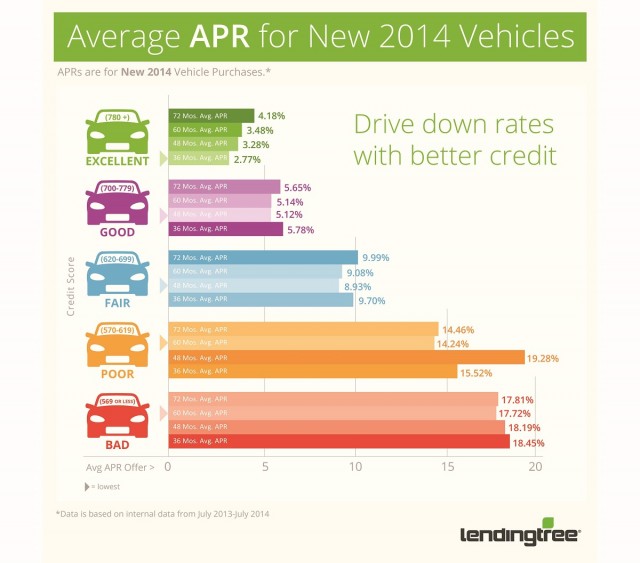

6. Potentially Higher Interest Rates: While not always the case, some lenders may charge a slightly higher Annual Percentage Rate (APR) for extended loan terms. This is because a longer term represents a greater risk for the lender. Even a small increase in the APR, compounded over many years, can significantly inflate the total interest paid.

Who Qualifies for the Longest Car Loans?

Lenders are typically more cautious when approving extended car loan terms due to the increased risk involved. To qualify for an 84-month or 96-month loan, you generally need to present a very strong financial profile.

Excellent Credit Score: A high credit score (typically 720+) is almost always a prerequisite. It demonstrates a history of responsible borrowing and repayment, reassuring lenders that you are a low-risk borrower over a longer period.

Stable Income and Low Debt-to-Income Ratio: Lenders want to see a consistent and sufficient income stream to comfortably cover the extended monthly payments, even if they are lower. A low debt-to-income (DTI) ratio indicates that your existing debt obligations are manageable, leaving room for the new car payment.

Newer Vehicles: Extended terms are almost exclusively offered for new or very late-model used vehicles. Lenders are less likely to finance an older car for 7-8 years because its value will depreciate too quickly, and the risk of mechanical failure (and thus, non-payment) increases. The vehicle’s value serves as collateral, and lenders prefer collateral that holds its value.

Substantial Down Payment: While not always mandatory, making a significant down payment (e.g., 20% or more) can greatly improve your chances of approval for an extended term. A larger down payment reduces the amount financed, lowers the lender’s risk, and helps mitigate the negative equity problem.

Factors Influencing Your Loan Term Options

Beyond your personal financial profile, several other elements can impact the car loan terms available to you. Understanding these can help you navigate the financing process more effectively.

Lender Policies: Not all lenders offer the same maximum loan terms. Some banks or credit unions might cap their terms at 72 months, while others extend to 84 or even 96 months. It’s always wise to shop around and compare offers from multiple institutions.

Vehicle Type and Value: As mentioned, newer, higher-value vehicles are more likely to qualify for extended terms. A luxury SUV might be approved for 84 months, while a compact sedan might only go up to 72 months, even with the same borrower.

Market Conditions and Interest Rates: The overall economic climate and prevailing interest rates can influence loan terms. In periods of low-interest rates, lenders might be more willing to offer longer terms. Conversely, rising rates could lead to more conservative lending practices.

Loan Amount: Sometimes, a higher loan amount can make extended terms more justifiable for lenders, as it allows them to spread out their risk and potential profit over a longer duration.

Making an Informed Decision: Is an Extended Loan Right for You?

Deciding on a car loan term requires careful self-assessment and a look at your future financial landscape. An extended loan isn’t inherently "bad," but it’s often more expensive in the long run.

Financial Assessment: Scrutinize your budget. Can you genuinely afford a shorter loan term with higher monthly payments? If so, it’s almost always the more financially prudent choice due to less interest paid and quicker equity build-up. For a deeper dive into budgeting for a car, check out our guide on .

Future Plans: How long do you realistically plan to keep this car? If you typically trade in vehicles every 3-5 years, an 84-month loan is likely a poor fit, as you’ll almost certainly be in a negative equity position when you want to upgrade.

Emergency Fund and Stability: Do you have a robust emergency fund? Are you in a stable career with predictable income? Extended loans require a long-term commitment. Any significant financial setback during that period could make payments challenging.

Opportunity Cost: Consider what you could do with the money saved on interest if you chose a shorter term. Could that money be invested, put towards a down payment on a home, or used to pay off higher-interest debt?

As seasoned financial observers, our expertise suggests that while extended terms offer immediate payment relief, they often come at a significant long-term cost. Evaluate your financial situation thoroughly before committing to a long-term car loan.

Strategies to Mitigate the Risks of Long Car Loans

If an extended car loan is your only viable option to afford the vehicle you need, there are strategies you can employ to minimize its downsides.

1. Make Extra Payments Whenever Possible: Even small additional payments can make a big difference. Direct any extra money you have (e.g., tax refunds, bonuses, or even an extra $50 per month) directly towards the principal balance. This reduces the total interest paid and helps you pay off the loan faster.

2. Refinance When Rates Drop or Credit Improves: Keep an eye on interest rates and your credit score. If rates decrease significantly or your credit score improves after a year or two, you might be able to refinance your loan to a lower interest rate or even a shorter term, saving you money.

3. Purchase GAP Insurance: Guaranteed Asset Protection (GAP) insurance is highly recommended for extended car loans, especially if you make a small down payment. It covers the difference between what you owe on your loan and your car’s actual cash value if it’s totaled or stolen. This protects you from being stuck with negative equity after an unfortunate event.

4. Choose a Reliable Vehicle: If you’re committing to an 84-month loan, select a car with a strong reputation for reliability and low maintenance costs. You don’t want to be making payments on a car that’s constantly in the shop.

5. Make a Substantial Down Payment: As always, the more you put down upfront, the better. A larger down payment reduces your loan amount, lessens the impact of depreciation, and helps you avoid or minimize negative equity.

Alternative Approaches to Car Financing

If the prospect of a very long car loan feels daunting, consider these alternatives:

Shorter Terms with Higher Payments: If your budget allows, opting for a 36, 48, or 60-month loan will save you a substantial amount in interest and get you out of debt faster.

Buying a Less Expensive Car: Re-evaluate your needs versus wants. A slightly less expensive vehicle might allow you to comfortably afford a shorter loan term, saving you money in the long run.

Saving Up a Larger Down Payment: Delaying your purchase slightly to save a larger down payment can significantly reduce your loan amount and, consequently, your monthly payments and total interest.

Leasing: For some, leasing might be an alternative. While it doesn’t lead to ownership, it typically offers lower monthly payments for a newer car and allows for frequent upgrades. Explore the pros and cons of leasing versus buying in our comprehensive article: .

For more insights on responsible borrowing and managing your finances, you might find valuable information from the Consumer Financial Protection Bureau (CFPB) on their website at consumerfinance.gov.

Conclusion: Navigating the Longest Car Loan Terms Wisely

In summary, the answer to "What is the longest car loan you can get?" typically ranges from 84 months (7 years) to 96 months (8 years), with rare instances extending further. While these extended terms offer the immediate benefit of lower monthly payments, they come with significant financial drawbacks, including substantially more interest paid, a higher risk of negative equity, and a prolonged period of debt.

As professional SEO content writers and expert bloggers, our ultimate advice is to approach extended car loans with caution and a clear understanding of the long-term implications. Always prioritize the total cost of the loan over just the monthly payment. If an extended term is necessary, implement strategies to mitigate the risks, such as making extra payments and securing GAP insurance.

Making an informed decision about your car loan term is paramount to your financial well-being. Drive smart, not just far.

What are your experiences with car loan terms? Share your thoughts and questions in the comments below!