Unlocking the Mystery: A Comprehensive Guide to Interest Paid On Your Car Loan

Unlocking the Mystery: A Comprehensive Guide to Interest Paid On Your Car Loan Carloan.Guidemechanic.com

Buying a car is an exciting milestone for many, a symbol of freedom and independence. Yet, beneath the gleaming paint and new car smell lies a financial reality that often confuses and intimidates: the interest paid on your car loan. For many, it’s just a number on a monthly statement, but understanding this crucial component is key to making smart financial decisions and saving potentially thousands of dollars over the life of your loan.

As an expert blogger and professional SEO content writer, my mission today is to demystify car loan interest. This isn’t just about defining terms; it’s about empowering you with the knowledge to navigate the auto financing landscape confidently. We’ll delve deep into how interest works, what influences it, and most importantly, how you can significantly reduce the total amount you pay. By the end of this comprehensive guide, you’ll be an expert in your own right, ready to tackle your next car purchase with unparalleled financial acumen.

Unlocking the Mystery: A Comprehensive Guide to Interest Paid On Your Car Loan

What Exactly Is Interest Paid On A Car Loan?

At its core, interest is the cost of borrowing money. When you take out a car loan, a lender (like a bank, credit union, or dealership) provides you with the funds to purchase your vehicle. In return for this service, they charge you a fee, which is the interest. Think of it as rent for using their money.

This fee isn’t a one-time charge; it’s typically expressed as a percentage of the amount you’ve borrowed, calculated over the loan’s term. It’s what allows lenders to make a profit and covers the risk they take by lending you money. Without interest, there would be little incentive for financial institutions to offer loans.

Understanding interest is crucial because it directly impacts the total amount you will pay for your car, often adding a substantial sum beyond the vehicle’s sticker price. Ignoring it means potentially paying far more than necessary for your dream car.

The Core Components: Principal, Interest, and APR

To truly grasp how car loan interest works, we need to break down the key terms you’ll encounter. These aren’t just jargon; they are the pillars of your loan agreement.

Understanding the Principal

The principal is the initial amount of money you borrow from the lender to buy your car. If a car costs $25,000 and you put down a $5,000 down payment, your principal loan amount would be $20,000. This is the base figure upon which your interest is calculated.

Every monthly payment you make is split between reducing this principal amount and covering the interest charged. As you pay down the principal, the amount of interest you owe on the remaining balance typically decreases over time.

Dissecting the Interest Rate

The interest rate is the percentage that the lender charges you for borrowing the principal. It’s usually expressed as an annual percentage. For example, a 5% interest rate means you’ll pay 5% of your outstanding principal balance in interest over a year.

It’s important to note that the interest rate alone doesn’t tell the full story of your loan’s cost. While it’s a significant factor, other fees can contribute to the overall expense, which leads us to the next crucial term.

The All-Important APR (Annual Percentage Rate)

The Annual Percentage Rate (APR) is arguably the most critical number to look at when comparing car loan offers. Unlike the simple interest rate, the APR represents the true annual cost of your loan. It includes not only the interest rate but also any additional fees charged by the lender, such as origination fees, documentation fees, or processing fees.

Pro Tip from us: Always compare loan offers using their APR, not just the quoted interest rate. A loan might advertise a low interest rate, but if it has high associated fees, its APR could be higher than another loan with a slightly higher interest rate but no extra charges. Focusing on the APR gives you a complete picture of what you’ll actually pay each year.

How Is Interest On A Car Loan Calculated?

Most car loans use a simple interest calculation based on the declining balance of your loan. This means that interest is only charged on the remaining principal balance, which decreases with each payment you make. It’s not like compound interest on a credit card, where interest can be charged on previously accrued interest.

Here’s a simplified way to understand it: At the beginning of each payment period (usually monthly), the lender calculates the interest due for that period based on your current principal balance and your annual interest rate. This interest amount, along with a portion of your payment applied to the principal, makes up your total monthly payment.

Over the life of the loan, especially in the early stages, a larger portion of your monthly payment goes towards interest. As the principal balance shrinks, more of your payment starts going towards reducing the principal itself. This gradual shift is illustrated by an amortization schedule, which breaks down exactly how much of each payment goes to principal and interest. While complex calculations are usually done by lenders, understanding this declining balance concept is vital.

Key Factors Influencing Your Car Loan Interest Rate

Several variables play a significant role in determining the interest rate you’ll be offered for a car loan. Understanding these factors can help you position yourself for the best possible rates.

Your Credit Score: The Ultimate Game Changer

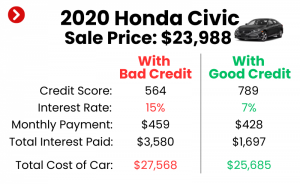

Your credit score is perhaps the single most influential factor in securing a favorable interest rate. Lenders use your credit score to assess your creditworthiness – essentially, how likely you are to repay the loan on time. A higher credit score (typically above 700) indicates a lower risk to lenders, which usually translates into lower interest rates.

Conversely, a lower credit score suggests a higher risk, leading lenders to charge a higher interest rate to compensate for that perceived risk. Based on my experience, even a difference of 50-100 points in your credit score can mean a significant difference in the total interest you’ll pay over the life of a car loan. This is why credit health is paramount.

Loan Term Length: Short vs. Long

The length of your loan, also known as the loan term, profoundly impacts your interest rate. Shorter loan terms (e.g., 36 or 48 months) typically come with lower interest rates because the lender’s money is tied up for a shorter period, reducing their risk. However, shorter terms also mean higher monthly payments.

Longer loan terms (e.g., 60, 72, or even 84 months) often have higher interest rates. While they offer the allure of lower monthly payments, you’ll end up paying significantly more in total interest over the life of the loan. It’s a trade-off between monthly affordability and overall cost.

Down Payment: Less Borrowed, Less Interest

Making a substantial down payment reduces the amount of money you need to borrow, which directly lowers the principal. A smaller principal means less interest will accrue over the loan term. Additionally, a larger down payment signals to lenders that you are a serious and responsible borrower, potentially qualifying you for better interest rates.

It also reduces the loan-to-value (LTV) ratio, which is another risk factor for lenders. The less they lend relative to the car’s value, the less risk they assume, often leading to more favorable terms.

Vehicle Type & Age: Risk Assessment

The type of vehicle you’re purchasing and whether it’s new or used can also influence your interest rate. New cars often qualify for lower rates due to manufacturer incentives and their higher resale value, which provides better collateral for the lender. Used cars, while generally cheaper upfront, might come with slightly higher interest rates because they are considered higher risk due to depreciation and potential mechanical issues.

Certain niche or luxury vehicles might also be subject to different rates based on market demand and resale value. Lenders assess the risk associated with the specific asset they are financing.

Lender Type: Banks, Credit Unions, Dealerships

Where you get your loan can make a big difference. Traditional banks, credit unions, and online lenders each have different lending criteria and rate structures. Credit unions, being non-profit, are often known for offering very competitive rates to their members. Online lenders can also be quite competitive due to lower overheads.

Dealership financing can be convenient, but it’s crucial to compare their offers with pre-approvals from other lenders. Dealerships often work with multiple financing sources and might mark up the interest rate as a profit center. Shopping around extensively is always a wise strategy.

Market Interest Rates: The Economic Climate

Broader economic conditions, particularly the prevailing interest rates set by central banks (like the Federal Reserve in the U.S.), influence car loan rates. When overall market rates are low, car loan rates tend to follow suit, and vice versa. These rates are beyond your control but understanding their impact helps contextualize the offers you receive.

It’s wise to keep an eye on economic forecasts if you’re planning a car purchase, as waiting for a period of lower rates could save you money. However, don’t let perfect be the enemy of good if you need a car now.

Strategies to Significantly Reduce the Interest Paid On Your Car Loan

Now that you understand what influences your interest rate, let’s explore actionable strategies to minimize the interest you pay on your car loan. These aren’t just theoretical; they are proven methods to keep more money in your pocket.

Boost Your Credit Score Before Applying

This is one of the most impactful steps you can take. Before you even start test driving, dedicate time to improving your credit score. Pay all your bills on time, reduce outstanding credit card balances, and avoid opening new credit accounts right before applying for a car loan. A higher score translates directly into lower interest rates.

Even small improvements can make a difference. Request a copy of your credit report to check for errors and dispute any inaccuracies, as these can negatively affect your score.

Make a Substantial Down Payment

As discussed, a larger down payment reduces your principal loan amount and signals financial responsibility to lenders. Aim for at least 10-20% of the car’s purchase price, if possible. Not only will you pay less interest, but you’ll also build equity in your vehicle faster and reduce the risk of being "upside down" on your loan (owing more than the car is worth).

This single action can shave hundreds, if not thousands, off your total interest paid over the life of the loan.

Choose a Shorter Loan Term (If Affordable)

While longer loan terms offer lower monthly payments, they invariably lead to paying more interest overall. If your budget allows, opt for the shortest loan term you can comfortably afford. A 48-month loan will almost always have a lower interest rate and significantly lower total interest paid than a 72-month loan for the same amount.

Balance your monthly payment comfort with the desire to minimize total interest. Sometimes, paying a little more each month upfront can save you a lot in the long run.

Shop Around Extensively for Lenders

Never take the first loan offer you receive, especially from a dealership. Get pre-approved for a loan from several different lenders – banks, credit unions, and online lenders – before you even step foot in a dealership. This way, you’ll know the best rate you qualify for and have a strong negotiating tool.

Common mistakes to avoid are letting the dealership "run your credit" without a pre-approval in hand. This can lead to multiple hard inquiries on your credit report, which can temporarily ding your score. Instead, present them with your best pre-approved offer and see if they can beat it.

Consider Refinancing Your Car Loan

If you’ve already taken out a car loan but your credit score has improved, market interest rates have dropped, or you initially received a high-interest rate due to limited credit history, refinancing could be an excellent option. Refinancing involves taking out a new loan, often with a lower interest rate, to pay off your existing car loan.

This can significantly reduce your monthly payments and the total interest paid. Just be sure to calculate any refinancing fees to ensure the savings outweigh the costs.

Pay More Than the Minimum Monthly Payment

Even if it’s just an extra $20 or $50 each month, paying more than your minimum required payment can have a dramatic effect on the total interest you pay. Since car loans are typically simple interest, any extra principal payment directly reduces the balance on which future interest is calculated.

This strategy shortens your loan term and reduces the total interest paid without the need for a formal refinance. Always ensure your extra payments are applied directly to the principal, not just towards future interest.

Understanding Your Car Loan Agreement: What to Look For

The loan agreement is a legally binding contract, and it’s essential to understand every clause before you sign. Don’t rush through it; ask questions if anything is unclear.

First, verify that the interest rate and APR match what was quoted to you. Remember, the APR is the more comprehensive figure. Look for any prepayment penalties, which are fees charged by some lenders if you pay off your loan early. Most car loans do not have these, but it’s crucial to confirm.

Also, be aware of late fees and other charges for missed payments. Understand the grace period, if any, for late payments. Pro tips from us include scrutinizing the total amount financed, including any add-ons like extended warranties or GAP insurance, as these can significantly inflate your principal and thus the interest you’ll pay. Ensure you only pay for what you truly need and understand.

The Long-Term Impact of Interest Paid On Car Loan

The interest you pay on a car loan isn’t just a short-term cost; it has long-term implications for your financial health. Over the course of a 5-7 year loan, interest can add thousands of dollars to the cost of your vehicle, significantly increasing your total cost of ownership. This money could have been used for other financial goals, such as saving for a down payment on a home, investing, or building an emergency fund.

Understanding this opportunity cost is critical. Every dollar spent on interest is a dollar not working for you. By minimizing interest, you free up more of your income for wealth-building activities, helping you achieve financial independence sooner. Furthermore, paying off your car loan efficiently means you build equity faster, providing more financial flexibility down the road.

FAQs About Interest Paid On Car Loan

Let’s address some common questions people have about car loan interest.

Q: Is car loan interest tax deductible?

A: Generally, no. For most consumers, interest paid on a personal car loan is not tax-deductible. However, there are exceptions. If you use your car solely for business purposes, the interest might be deductible as a business expense. Always consult with a tax professional for personalized advice.

Q: What is considered a "good" car loan interest rate?

A: A "good" interest rate is subjective and depends heavily on your credit score, the current market rates, and the loan term. For borrowers with excellent credit (720+ FICO), rates below 5% (and sometimes even below 3% for new cars with manufacturer incentives) are often considered very good. For those with average credit (620-680), rates might range from 6-10%. Anything significantly higher, especially into double digits, suggests a high-risk loan or that you need to improve your credit before borrowing.

Q: How can I calculate my total interest paid on a car loan?

A: The easiest way to estimate your total interest paid is to use an online car loan calculator. You’ll input the principal loan amount, interest rate, and loan term, and it will generate an amortization schedule showing the total interest. Alternatively, you can multiply your monthly payment by the total number of payments and then subtract the principal amount to get an approximation of the total interest paid.

Q: Does a higher down payment always reduce the total interest paid?

A: Yes, unequivocally. A higher down payment directly reduces the principal amount you need to borrow. Since interest is calculated on the principal, less principal means less interest will accrue over the life of the loan, regardless of the interest rate or term. It’s one of the most effective ways to save money.

Q: Can I get a 0% APR car loan?

A: Yes, 0% APR car loans exist, but they are typically offered by manufacturers on new cars as a special incentive. These offers are usually reserved for buyers with excellent credit scores and might apply only to specific models or shorter loan terms. While attractive, always compare them to other offers, as sometimes a cash rebate might be more beneficial than the 0% APR if you can secure a low interest rate elsewhere. For example, you might choose a $2,000 cash rebate over a 0% APR loan if your own bank offers you a 2% APR, leading to greater overall savings.

Conclusion: Empower Yourself Against Interest

Understanding the interest paid on your car loan isn’t just about financial literacy; it’s about financial empowerment. By grasping the fundamentals of principal, interest rates, and APR, and by actively implementing strategies to reduce your borrowing costs, you can save a significant amount of money over the life of your vehicle.

Remember, the goal is to not just buy a car, but to own it without unnecessary financial burden. Shop around, improve your credit, make a solid down payment, and always read the fine print. Armed with this comprehensive knowledge, you’re now better equipped to navigate the complexities of car financing, making choices that benefit your wallet and your long-term financial well-being. Don’t let interest be an afterthought; make it a central point of your car buying strategy and start saving today. For more trusted financial guidance, consider exploring resources from reputable sources like the Consumer Financial Protection Bureau (CFPB) to further enhance your understanding of financial products.