Unlocking the Mystery: How Applying For A Car Loan Affects Your Credit Score – The Ultimate Guide

Unlocking the Mystery: How Applying For A Car Loan Affects Your Credit Score – The Ultimate Guide Carloan.Guidemechanic.com

Buying a car is a significant life event for many, often accompanied by the excitement of a new ride and the practical considerations of financing. For most people, securing a car loan is a necessary step. But as you navigate the world of interest rates, down payments, and monthly installments, one crucial question often looms large: How does applying for a car loan affect your credit score?

This isn’t a simple yes or no answer. The impact is multifaceted, encompassing immediate, short-term dips and long-term opportunities for growth. As an expert blogger and professional SEO content writer, I’m here to demystify this complex relationship. We’ll delve deep into every nuance, providing you with a comprehensive understanding that will empower you to make informed financial decisions. Our goal is to equip you with the knowledge to apply for a car loan confidently, strategically, and with your credit health in mind.

Unlocking the Mystery: How Applying For A Car Loan Affects Your Credit Score – The Ultimate Guide

The Initial Impact: Your Credit Score and the Application Process

When you decide to apply for a car loan, the first interaction your credit score has with the process is typically through a credit inquiry. This is where the immediate effects begin. Understanding the different types of inquiries is paramount to comprehending the initial ripple on your credit profile.

Hard Inquiries: The Necessary Credit Check

A hard inquiry, also known as a "hard pull," occurs when a lender checks your credit report to make a lending decision. This happens when you formally apply for new credit, whether it’s a car loan, a mortgage, a credit card, or even some rental agreements. The lender needs to assess your creditworthiness to determine the risk associated with lending you money.

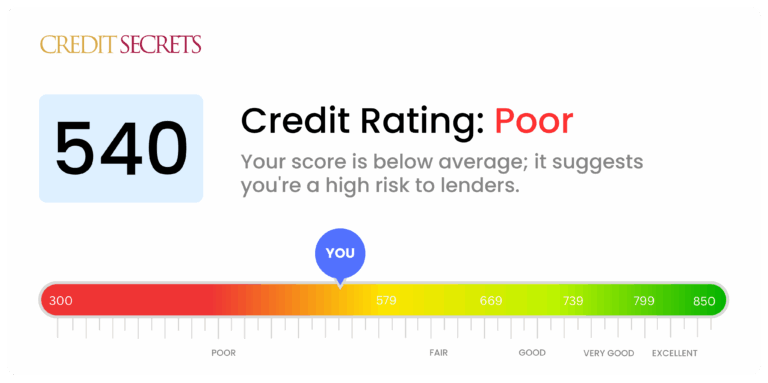

Based on my extensive experience in consumer finance, a single hard inquiry typically causes a small, temporary dip in your credit score, usually by a few points (around 2-5 points). This slight decrease is because applying for new credit signals a potential increase in your debt load, which credit scoring models interpret as a slightly elevated risk. While it might seem negligible, it’s a factor to be aware of.

These inquiries remain on your credit report for two years, though their impact on your score typically diminishes after a few months. It’s crucial to understand that these are a standard part of the lending process. You cannot apply for a loan without one.

Soft Inquiries: For Your Eyes Only (Mostly)

In contrast to hard inquiries, a soft inquiry, or "soft pull," does not impact your credit score. These occur when you check your own credit score or report, or when a potential lender pre-screens you for an offer (like those unsolicited credit card mailers). These inquiries are often used for informational purposes and are not associated with a specific application for new credit.

You might encounter a soft inquiry if you use an online tool to get a preliminary idea of what car loan rates you might qualify for, or if you use a service that provides credit monitoring. From a professional perspective, always opt for pre-qualification methods that involve soft pulls when you’re just exploring options, as they provide valuable insights without affecting your score.

The "Shopping Around" Window: A Smart Strategy

One of the most critical pieces of information when considering how apply for car loan affect credit score is the "shopping around" window. Credit scoring models, particularly FICO and VantageScore, are designed to recognize that consumers shop for the best rates when seeking a significant loan like a car loan or a mortgage. They don’t want to penalize you for being a smart consumer.

For this reason, multiple hard inquiries for the same type of loan within a concentrated period are often treated as a single inquiry. This "shopping around" window typically ranges from 14 to 45 days, depending on the scoring model used. This means you can apply with several different auto lenders within this timeframe, and your score will likely only take one hit. This is a pro tip from us: consolidate your car loan applications to a short window to minimize credit score impact.

This strategic approach allows you to compare interest rates and loan terms from various lenders without unduly harming your credit score. It empowers you to secure the most favorable deal possible, potentially saving you thousands of dollars over the life of the loan. Don’t be afraid to get multiple quotes, but do so efficiently within the recognized timeframe.

Beyond the Initial Dip: How a Car Loan Can Help Your Credit Score (Long-Term Benefits)

While the initial application might cause a slight, temporary dip, the long-term effects of a responsibly managed car loan can be overwhelmingly positive for your credit score. This is where a car loan truly shines as a credit-building tool.

Payment History: The Cornerstone of Your Credit Score

Your payment history is by far the most significant factor in your credit score, accounting for approximately 35% of your FICO score. This means consistently making your car loan payments on time, every single month, is incredibly powerful. Each on-time payment demonstrates your reliability as a borrower and builds a strong foundation of positive credit behavior.

Based on my experience, diligently meeting your payment obligations for a car loan can significantly boost your credit score over time. It shows lenders that you are responsible and trustworthy, making you a more attractive candidate for future loans and credit products. Conversely, even a single late payment can have a devastating effect, potentially dropping your score by dozens of points and staying on your report for up to seven years.

Credit Mix: Diversifying Your Credit Portfolio

Your credit mix, which accounts for about 10% of your FICO score, refers to the different types of credit you manage. This typically includes revolving credit (like credit cards) and installment credit (like car loans, mortgages, or student loans). Having a healthy mix of both shows lenders that you can responsibly manage various forms of debt.

Adding an installment loan, such as a car loan, to a credit profile that primarily consists of revolving credit cards can be very beneficial. It demonstrates your ability to handle different financial commitments, which is a positive signal to credit bureaus. This diversification strengthens your credit profile and can contribute to a higher overall score.

Credit Utilization: A Different Kind of Debt

Credit utilization, which makes up about 30% of your FICO score, primarily applies to revolving credit. It measures how much of your available credit you are using. For example, if you have a credit card with a $10,000 limit and a $3,000 balance, your utilization is 30%. Keeping this low (ideally below 30%) is crucial for a good score.

Installment loans, like car loans, work differently. While they represent a debt, they are not typically factored into your credit utilization ratio in the same way as revolving credit. You borrow a fixed amount and pay it back over time. The balance decreases with each payment, but it doesn’t fluctuate like a credit card balance. This means a car loan generally won’t negatively impact your credit utilization, unlike maxing out a credit card.

Potential Negative Impacts and How to Avoid Them

While a car loan can be a powerful credit-building tool, it also carries potential risks. Understanding these pitfalls and actively avoiding them is just as important as knowing the benefits.

Late Payments or Defaults: A Credit Score Catastrophe

This cannot be stressed enough: consistently making your car loan payments on time is paramount. A single late payment (typically 30 days or more past due) can severely damage your credit score. Multiple late payments or, worse, a loan default, will send your score plummeting and significantly hinder your ability to obtain future credit.

Common mistakes to avoid are underestimating your monthly budget or failing to set up automatic payments. From a professional perspective, always prioritize your car loan payments. Missing them not only hurts your credit but can also lead to repossession of your vehicle, creating an even larger financial and logistical headache.

Taking on Too Much Debt: The Debt-to-Income Ratio

Even if you make all your payments on time, taking on an excessively large car loan can negatively impact your financial health and future borrowing capacity. Lenders look at your debt-to-income (DTI) ratio, which compares your total monthly debt payments to your gross monthly income. A high DTI can signal that you are overextended.

While a car loan itself doesn’t directly lower your credit score based on DTI, a high DTI can make it challenging to qualify for other loans (like a mortgage) in the future. It indicates that a significant portion of your income is already committed to debt, leaving less room for new obligations. Always ensure your car payment is comfortably within your budget and doesn’t push your DTI into an unhealthy range. For more on managing your financial ratios, check out our article on .

High Interest Rates: The Hidden Strain

Securing a car loan with a very high interest rate can also pose a subtle threat to your credit health. While the rate itself doesn’t directly impact your score, a high rate means a larger portion of your monthly payment goes towards interest, not the principal. This results in higher overall payments, which can strain your budget.

When financial strain hits, the likelihood of missing payments increases. This is a common pitfall we observe. Always strive for the lowest possible interest rate by improving your credit score beforehand and shopping around effectively. A manageable payment is key to successful credit building.

Preparing Your Credit for a Car Loan: Proactive Steps

Before you even start browsing car dealerships, taking proactive steps to prepare your credit can significantly improve your chances of approval, secure a better interest rate, and ultimately enhance your credit-building journey.

1. Check Your Credit Report and Score

This is the golden rule of any major credit application. Obtain copies of your credit report from all three major bureaus (Experian, Equifax, and TransUnion) and check your credit score. You are entitled to a free credit report from each bureau annually via AnnualCreditReport.com.

Review your reports meticulously for any errors or inaccuracies. Common mistakes include incorrect addresses, misspelled names, or even accounts that don’t belong to you. Disputing and correcting these errors can often lead to an immediate boost in your credit score. Understanding your current score also gives you a realistic expectation of the rates you might qualify for.

2. Improve Your Credit Score (If Needed)

If your credit score isn’t where you want it to be, take steps to improve it before applying for a car loan. This is crucial, and based on years of observing credit behavior, it can save you thousands in interest over the life of the loan. Focus on these key areas:

- Pay Down Existing Debt: Especially high-interest credit card debt. Lowering your credit utilization will positively impact your score.

- Make All Payments On Time: Set up reminders or automatic payments for all your bills. Payment history is paramount.

- Avoid Opening New Credit Accounts: Don’t apply for new credit cards or loans in the months leading up to your car loan application. New inquiries and accounts can temporarily depress your score.

- Keep Old Accounts Open: The length of your credit history (another 15% of your FICO score) is important. Don’t close old, paid-off credit card accounts, even if you don’t use them, as this shortens your average account age.

For a deeper dive into boosting your credit, check out our guide on .

3. Know Your Budget and Down Payment Capabilities

Before approaching lenders, establish a realistic budget for your car purchase. This isn’t just about the monthly payment; it includes insurance, fuel, maintenance, and potential repairs. A common mistake we see is people only focusing on the car’s price.

Consider how much you can comfortably afford as a down payment. A larger down payment reduces the amount you need to borrow, which can lead to lower monthly payments and potentially a better interest rate. It also signals to lenders that you are a less risky borrower.

4. Get Pre-Approved Before You Shop

Pro tips from us: Before you even start browsing cars at a dealership, get pre-approved for a loan from your bank, credit union, or an online lender. Pre-approval gives you a clear understanding of the maximum loan amount you qualify for and the interest rate you can expect.

Having a pre-approval in hand gives you significant leverage when negotiating with dealerships. You’re no longer just a buyer; you’re a buyer with financing already secured. This allows you to focus on negotiating the car’s price, rather than being swayed by dealership financing offers that might not be in your best interest. Remember to do this within your "shopping around" window.

The "Sweet Spot": When Does a Car Loan Truly Benefit Your Credit?

A car loan truly benefits your credit score when it’s approached and managed responsibly. The "sweet spot" for credit building occurs under these conditions:

- Strategic Application: You’ve checked your credit, improved it if necessary, and conducted multiple loan inquiries within the permissible "shopping around" window to secure the best rate.

- Affordable Loan: The loan amount and monthly payments are well within your budget, ensuring no financial strain.

- Consistent On-Time Payments: You make every single payment on time, every month, without fail. This is the single most impactful action.

- Credit Mix Diversification: The car loan adds a healthy installment loan to your credit profile, especially if you previously only had revolving credit.

When these elements align, your car loan transforms from just a way to finance a vehicle into a powerful engine for building and enhancing your creditworthiness.

Conclusion: Navigating the Road to a Better Credit Score

Applying for a car loan is a significant financial decision with a dynamic impact on your credit score. While the initial hard inquiry might cause a slight, temporary dip, the long-term potential for credit building is immense – provided you manage the loan responsibly. By understanding the mechanics of hard inquiries, leveraging the "shopping around" window, and consistently making on-time payments, you can transform a car loan into a powerful tool for improving your financial health.

Remember, preparation is key. Check your credit, understand your budget, and get pre-approved to put yourself in the strongest possible position. A car loan isn’t just about getting from point A to point B; it’s also about navigating the road to a stronger, more reliable credit score. Drive responsibly, both on the road and with your finances!

We encourage you to share your experiences with car loans and credit scores in the comments below. What strategies have worked for you? For more detailed information on how credit scores are calculated and what factors influence them, refer to trusted sources like FICO at FICO.com.