Unlocking the Reality of 0 Interest Car Loans in India: Your Definitive Guide

Unlocking the Reality of 0 Interest Car Loans in India: Your Definitive Guide Carloan.Guidemechanic.com

The dream of owning a brand-new car resonates deeply with many in India. It’s more than just a mode of transport; it’s a symbol of independence, a convenience for the family, and often, a significant life milestone. As you embark on this exciting journey, you’ve likely come across advertisements promising the ultimate financial relief: "0 Interest Car Loans."

These offers sound incredibly appealing, almost too good to be true. Imagine driving home your dream car without the burden of interest payments, seemingly saving lakhs over the loan tenure. But is this financial fairytale a reality, or is there more to these schemes than meets the eye?

Unlocking the Reality of 0 Interest Car Loans in India: Your Definitive Guide

As an expert blogger and professional SEO content writer, I’ve delved deep into the world of car finance in India. Based on my experience and extensive research, I can tell you that while 0 interest car loans exist, understanding their true nature is crucial for making an informed decision. This comprehensive guide will dissect everything you need to know about 0 Interest Car Loans in India, helping you navigate the fine print and determine if they truly offer the best value for your hard-earned money.

What Exactly Are "0 Interest Car Loans" in India?

At first glance, a "0 interest car loan" implies that you borrow money from a bank or financial institution to purchase a car, and you only repay the principal amount, with no additional charges for the use of that money. In theory, this sounds like a free loan, a financial boon that defies the very nature of lending. However, the reality in India, and globally, is a bit more nuanced.

These schemes are primarily promotional tools, often initiated by car manufacturers in collaboration with specific banks or non-banking financial companies (NBFCs). They are designed to boost sales, especially during festive seasons, year-end clearances, or for specific car models that need a sales push. The "zero interest" aspect is typically a marketing hook to attract potential buyers.

In essence, the "interest" doesn’t magically disappear; it’s usually absorbed or offset elsewhere within the financial transaction. This absorption mechanism is the core concept you need to understand to truly evaluate these offers. It’s a strategic play where the cost of borrowing is bundled into other parts of the deal, rather than being presented as a separate interest rate.

The Allure and the Reality: Why They Seem So Good

The psychological appeal of "zero interest" is undeniable. In a country where saving interest is often seen as a significant financial win, these offers tap into a deep-seated desire to maximize value. Advertisements often highlight the low monthly EMIs and the absence of an interest burden, making car ownership seem more accessible and affordable.

From a marketing perspective, these schemes are incredibly effective. They create a buzz, draw customers into showrooms, and differentiate one manufacturer or dealer from another. For many prospective buyers, the promise of no interest is a primary motivator, often overshadowing other crucial factors of the purchase. This focus on the "zero" aspect can sometimes lead buyers to overlook other important details in their excitement.

However, the reality is that financial institutions and manufacturers are not charities. They operate on profit margins. Therefore, any offer that appears to eliminate a core revenue stream (interest) must compensate for it through other means. Common misconceptions include believing that the car price is unaffected or that there are no hidden costs whatsoever.

Decoding the Fine Print: Where the "Interest" Hides

Based on my experience, the phrase "there’s no such thing as a free lunch" perfectly applies to 0 interest car loans in India. The "interest" is cleverly disguised within other elements of the car buying process. Understanding these hidden costs is paramount before committing to any such offer.

1. Higher Down Payment Requirements

One of the most common ways the "zero interest" illusion is maintained is through a significantly higher down payment. While a standard car loan might require 10-20% of the car’s ex-showroom price as a down payment, a 0% interest scheme might demand 30-50% or even more. This larger upfront payment reduces the principal amount borrowed, thereby lowering the total interest a bank would typically charge over a standard tenure.

This strategy benefits the lender by reducing their risk exposure and providing them with a larger sum upfront. For the buyer, it means you need substantial liquid cash readily available, which might not always be feasible or desirable.

2. Reduced Discounts and Negotiation Power

This is perhaps the most significant "hidden cost." Car dealerships often offer various discounts, cashbacks, or free accessories on new car purchases, especially during promotional periods. When you opt for a 0 interest car loan, you typically forfeit these potential savings. The manufacturer or dealer essentially uses the amount they would have given you as a discount to subsidize the interest for the loan.

Pro tip from us: Always ask the dealer for the "best cash purchase price" or the "best price if I arrange my own finance" versus the price under the 0% EMI scheme. You might find a substantial difference, sometimes running into tens of thousands or even a lakh for higher-end models, which could be more beneficial than the perceived interest savings.

3. Processing Fees and Other Charges

While the interest rate might be zero, the loan is still subject to standard processing fees, documentation charges, and other administrative costs. These fees can range from 0.5% to 2% of the loan amount, or a fixed sum, and are non-refundable. Additionally, you might encounter pre-closure charges if you decide to pay off your loan earlier than the stipulated tenure.

These charges, though seemingly small individually, can add up and subtly increase the overall cost of your financing. Always inquire about every single fee associated with the loan before signing any documents.

4. Shorter Loan Tenures

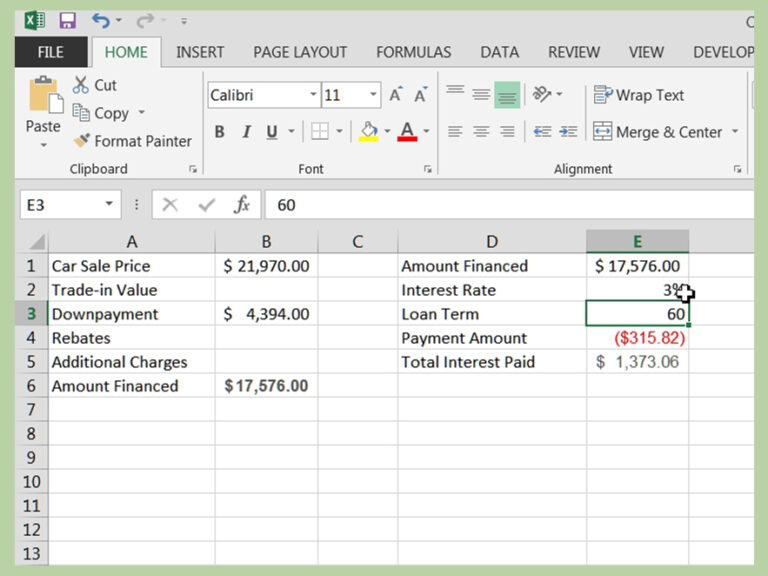

Zero interest schemes often come with significantly shorter loan tenures, typically ranging from 6 months to 24 or 36 months. While a shorter tenure means you pay off the loan faster, it also translates to much higher monthly EMIs. For instance, a loan of ₹5 lakhs over 12 months will have a much higher EMI than the same amount over 60 months, even if the interest is zero.

This can strain your monthly budget, making the car less affordable in the short term, despite the "no interest" tag. Common mistakes to avoid are focusing solely on the "zero interest" and overlooking the impact of a high EMI on your monthly finances.

5. Specific Models/Variants Only

These promotional offers are rarely applicable across an entire range of vehicles. They are usually tied to specific car models, variants, or even specific colours that the manufacturer or dealer wishes to clear from their inventory. This limits your choice and might push you towards a car that isn’t your first preference, simply to avail the 0% interest benefit.

Always verify if the car you truly desire is covered under the scheme, or if you’re being swayed by an offer on a less desirable option.

Eligibility Criteria for "Zero Interest" Car Loans

While the interest rate might be zero, the fundamental eligibility criteria for any car loan still apply, and often, they are even stricter for these special schemes. Lenders want to ensure that despite foregoing interest income, they are taking on minimal risk.

You will typically need to meet standard requirements such as:

- Age: Usually between 21 and 65 years.

- Income: A stable source of income, with a minimum monthly salary or business turnover, is crucial. Lenders will assess your debt-to-income ratio.

- Employment Stability: Salaried individuals often need to have been employed for at least 1-2 years with the current employer. Self-employed individuals need a consistent business history.

- Credit Score (CIBIL Score): This is paramount. A high CIBIL score (typically 750+) indicates strong financial discipline and a low credit risk, making you a more attractive candidate for lenders offering such schemes. Any blemishes on your credit report could disqualify you.

- Documentation: Standard KYC documents, income proof (salary slips, bank statements, ITR), and address proof will be required.

Sometimes, lenders might also ask for additional collateral or a guarantor, especially if the loan amount is substantial or if your financial profile, while good, isn’t exceptional. The goal is to mitigate risk for the lender.

Pros and Cons of Opting for a 0 Interest Car Loan

Making an informed decision requires a balanced view. Let’s look at the advantages and disadvantages of these schemes.

Pros:

- Perceived Savings on Interest: The most obvious benefit is the psychological comfort of not paying explicit interest. If all other factors were equal, this would indeed be a significant saving.

- Simplified Budgeting: With no interest calculation, your monthly EMI is straightforward, making it easier to budget for your car payments.

- Access to a New Car Sooner: If you have the required high down payment and are comfortable with the shorter tenure and potential hidden costs, these schemes can accelerate your car ownership dream.

Cons:

- Hidden Costs: As detailed earlier, these include higher down payments, lost discounts, processing fees, and other charges that effectively negate the "zero interest" benefit.

- Limited Flexibility: You are often restricted to specific car models, variants, or colours, and the loan tenures are usually non-negotiable and short.

- Potential for Higher Overall Cost: If the foregone cash discounts or other benefits outweigh the nominal interest you would have paid on a standard loan, you might end up paying more in total.

- Opportunity Cost: The money used for a larger down payment or the value of the foregone discount could potentially be invested elsewhere for better returns.

How to Find and Evaluate Genuine 0 Interest Car Loan Offers

Finding these offers requires diligent research, and evaluating them demands a keen eye for detail. Here’s a pro tip from us: Always approach these offers with a healthy dose of skepticism and a calculator.

- Research Thoroughly: Start by checking the official websites of car manufacturers. They often announce such promotional schemes directly. Follow up with authorized dealerships in your area. They will have the most up-to-date information on ongoing offers.

- Compare with Standard Loans: This is crucial. Get a detailed quote for the same car model and variant under a standard car loan scheme from multiple banks. Note down the interest rate, processing fees, tenure options, and importantly, the total amount payable (principal + interest + fees).

- Insist on the "On-Road Price" Comparison: Ask the dealer for two distinct quotes:

- One for the car purchased with a 0% interest loan, including all associated costs (down payment, processing fees, total EMI outflow).

- Another for the car purchased with a standard car loan, or even a full cash purchase, detailing all available discounts and benefits.

Compare the final "on-road price" and the total outflow in both scenarios.

- Read the Terms and Conditions Meticulously: Never skip this step. Pay attention to clauses regarding pre-closure charges, late payment penalties, and any hidden clauses that might impact your finances. Don’t hesitate to ask for clarification on anything you don’t understand.

- Calculate the True Cost: Based on my experience, the only way to truly compare is to calculate the total amount of money that leaves your pocket in both scenarios – the 0% interest scheme vs. a standard loan with discounts. This includes down payment, EMIs, processing fees, and any other charges.

For example, if a car costs ₹10 lakhs, and a 0% scheme requires a ₹4 lakh down payment and no discount, while a standard loan requires ₹2 lakh down payment but offers a ₹50,000 cash discount, the starting point for your calculation is already different.

Common Mistakes to Avoid When Considering a 0% Car Loan

Navigating the world of car finance can be tricky, and 0 interest loans are particularly prone to common pitfalls. Avoid these mistakes to ensure you make a smart decision:

- Not Reading the Fine Print: This cannot be stressed enough. Many hidden costs and restrictions are buried in the terms and conditions.

- Ignoring the Opportunity Cost of Lost Discounts: Often, the cash discount you forgo is significantly more than the interest you would have paid on a standard loan. Always quantify this difference.

- Focusing Only on EMI, Not Total Cost: A low EMI is attractive, but a shorter tenure or higher upfront costs can make the overall deal more expensive. Always look at the grand total.

- Rushing into a Decision: Car buying is a significant financial commitment. Take your time, compare multiple offers, and don’t feel pressured by sales tactics or "limited-time" offers.

- Assuming All "0 Interest" Offers Are the Same: The specifics of these schemes vary widely between manufacturers, models, and even dealerships. Each offer needs independent scrutiny.

Alternatives to 0 Interest Car Loans

If, after careful evaluation, a 0 interest car loan doesn’t seem like the best fit, there are several viable alternatives in India that might offer better value:

- Standard Car Loans: These are the most common form of car financing. With a competitive interest rate (which you can often negotiate or find online), flexible tenures, and potentially lower down payments, a standard car loan can often be more cost-effective, especially when combined with significant cash discounts. You can compare rates from various banks like SBI, HDFC Bank, ICICI Bank, etc.

- Personal Loans: While generally having higher interest rates than secured car loans, personal loans offer immense flexibility. You can use the funds for any purpose, and there are no restrictions on the car model or dealer. This can be useful if you’re getting a great cash discount on a car but don’t want to tie up your savings. However, always weigh the higher interest against the flexibility.

- Increasing Your Down Payment: The more you pay upfront, the less you need to borrow, which directly translates to lower interest payments over time. If you have sufficient savings, a larger down payment combined with a standard car loan can significantly reduce your total cost.

- Used Cars: Consider purchasing a pre-owned vehicle. The depreciation hit is largely absorbed by the first owner, making used cars significantly more affordable. While used car loans exist, the overall financial outlay is much lower.

Based on My Experience: Is a 0 Interest Car Loan Right for You?

Having observed countless car purchase scenarios, I can confidently say that a 0 interest car loan is rarely a universally "good" deal. However, there are specific circumstances where it might make sense for a particular individual.

It could be suitable if:

- You have substantial liquid cash available for a high down payment and prefer the structured EMI repayment over a lump-sum cash purchase, even if it means foregoing a small discount.

- The specific car model you desire has no significant cash discount available anyway, making the 0% EMI offer genuinely beneficial compared to a standard interest-bearing loan.

- You are absolutely certain you can repay the loan within the short tenure without financial strain, and you have thoroughly compared the "total cost of ownership" with other options.

Conversely, it definitely doesn’t make sense if:

- You are sacrificing a substantial upfront cash discount or other valuable benefits by opting for the 0% scheme.

- The high down payment or short tenure puts a significant strain on your monthly budget or depletes your emergency savings.

- You are being pushed towards a car model or variant that isn’t your first choice, just to avail the offer.

Ultimately, the decision hinges on diligent comparison and a clear understanding of the "total cost to you." Don’t be swayed by the "zero" alone; look at the entire financial picture. For more insights on managing your car loan effectively, you might find our article on "Understanding Car Loan EMIs and How to Calculate Them" helpful. (Note: This is a placeholder for an internal link).

The Future of Car Financing in India

The Indian automotive and financial landscape is dynamic. We are seeing a trend towards more digital loan applications, personalized offers based on credit profiles, and even innovative models like car subscriptions or leasing gaining traction. As technology advances, the way we finance our vehicles will continue to evolve.

While the "0 interest" concept might persist as a promotional tool, the underlying mechanisms will likely remain the same. The focus will always be on finding equilibrium between attracting customers and ensuring profitability for lenders and manufacturers. Staying informed about these evolving trends will empower you to make the best financial decisions for your car purchase. For general information on India’s financial market, you can refer to reputable sources like the Reserve Bank of India (RBI). (Note: This is an external link to a trusted source).

Conclusion: Drive Smart, Not Just Zero Interest

The allure of "0 Interest Car Loans in India" is undeniable, promising a path to car ownership free from the burden of interest. However, as this in-depth guide has revealed, these offers are often sophisticated marketing strategies where the cost of borrowing is cleverly hidden within other aspects of the purchase. From higher down payments and lost discounts to processing fees and shorter tenures, the "zero" often comes with its own price tag.

My experience shows that the key to making a smart decision lies in thorough research, meticulous comparison, and a deep understanding of the true total cost. Never assume a deal is genuinely "free." Always ask the right questions, scrutinize the fine print, and compare the overall financial outlay of a 0% scheme against standard car loans coupled with available discounts.

By arming yourself with this knowledge, you can cut through the marketing noise and make an empowered choice. Don’t just drive home a car; drive home a smart financial decision that truly benefits your wallet in the long run.