Unlocking the Road Ahead: A Deep Dive into FCCU Car Loan Rates

Unlocking the Road Ahead: A Deep Dive into FCCU Car Loan Rates Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is an exciting prospect. However, the path to ownership often involves navigating the complexities of car loans. For many, finding competitive rates and a trustworthy lender is paramount. This is where First Community Credit Union (FCCU) often shines, offering a member-focused approach to auto financing.

As an expert blogger and SEO content writer with years of experience in personal finance, I’ve seen firsthand how crucial it is for consumers to understand every facet of their loan options. This comprehensive guide will meticulously explore FCCU car loan rates, delving into what influences them, how to secure the best possible deal, and why a credit union might be your ideal financial partner. Our ultimate goal is to equip you with the knowledge to drive away with confidence, knowing you’ve made an informed decision.

Unlocking the Road Ahead: A Deep Dive into FCCU Car Loan Rates

Why Choose a Credit Union Like FCCU for Your Car Loan?

Before we dissect the intricacies of FCCU car loan rates, let’s understand the fundamental difference between a credit union and a traditional bank. This distinction often translates directly into more favorable terms for you, the borrower.

Understanding First Community Credit Union (FCCU):

FCCU operates on a unique principle: it’s a not-for-profit financial cooperative owned by its members. Unlike commercial banks that focus on maximizing profits for shareholders, credit unions like FCCU prioritize the financial well-being of their members. This philosophy often results in tangible benefits, including lower loan rates, higher savings rates, and reduced fees.

Based on my experience, this member-centric model fosters a more personalized and supportive lending environment. When you apply for an FCCU car loan, you’re not just a customer; you’re a co-owner, and that relationship can significantly impact your overall borrowing experience.

The Credit Union Advantage:

- Better Rates: Credit unions are frequently able to offer more competitive interest rates on loans, including auto loans, because they don’t have external shareholders demanding profits.

- Personalized Service: The focus on members often translates into more attentive and flexible customer service. They are often more willing to work with members facing unique financial situations.

- Community Focused: Credit unions are deeply rooted in their local communities, often reinvesting in local initiatives and understanding the specific needs of their members.

To access these benefits, you typically need to meet specific membership criteria, which usually involve living, working, or worshipping in a particular geographic area, or being affiliated with certain organizations. Checking FCCU’s membership requirements is the first step toward unlocking their competitive car loan rates.

Deconstructing FCCU Car Loan Rates: What Influences Them?

When you see advertised FCCU car loan rates, it’s important to understand that these are often "as low as" rates, meaning they apply to borrowers with excellent credit and specific loan terms. Several factors come into play when determining the actual interest rate you’ll be offered.

Pro tips from us: Never assume you’ll automatically qualify for the lowest advertised rate. Your personal financial profile is the key determinant.

Let’s break down the critical elements that FCCU, like any lender, will evaluate:

- Credit Score and History: This is arguably the most significant factor. A higher credit score signals lower risk to the lender, typically resulting in lower interest rates.

- Loan Term: The length of time you have to repay the loan impacts your rate. Shorter terms often come with lower rates, but higher monthly payments.

- Down Payment: A larger down payment reduces the amount you need to borrow and lessens the lender’s risk, which can lead to a better interest rate.

- Debt-to-Income (DTI) Ratio: This ratio indicates how much of your gross monthly income goes towards debt payments. A lower DTI shows you have more disposable income to cover your car loan.

- New vs. Used Vehicle: Rates for new cars are generally lower than for used cars, as new cars typically hold their value better initially and pose less risk to the lender.

- Vehicle Age and Mileage: For used cars, the age and mileage can significantly affect the loan rate. Older, higher-mileage vehicles often carry higher rates due to increased risk of mechanical issues and faster depreciation.

Understanding these variables is crucial for anyone seeking to secure the most favorable FCCU car loan rates.

Types of FCCU Car Loans: Tailored to Your Needs

FCCU offers a range of auto loan products designed to meet different member needs, whether you’re buying new, used, or looking to refinance an existing loan. Each type has its own nuances regarding rates and terms.

1. New Car Loans:

These loans are for brand-new vehicles straight from the dealership. Because new cars are less of a risk for lenders (they have predictable depreciation schedules and are under warranty), new car loan rates are typically the most competitive. FCCU aims to provide attractive rates to help you drive off the lot in your dream car.

2. Used Car Loans:

For those opting for a pre-owned vehicle, FCCU also offers used car loans. While rates for used cars are generally slightly higher than new car rates, they remain competitive. The specific rate will depend heavily on the vehicle’s age, mileage, and your personal creditworthiness. Many members find great value in purchasing a slightly used vehicle with excellent FCCU rates.

3. Refinancing Car Loans:

Perhaps you financed your car with another institution at a higher rate, or your credit score has significantly improved since you first took out the loan. FCCU’s refinancing options allow you to potentially lower your interest rate, reduce your monthly payments, or even shorten your loan term. This can lead to substantial savings over the life of your loan. Interested in understanding the nuances of car loan refinancing? We’ve covered it extensively in our article, .

4. Auto Loan Pre-Approval:

One of the smartest moves you can make is to get pre-approved for an FCCU car loan before you step foot in a dealership. Pre-approval gives you a clear understanding of how much you can afford and the interest rate you qualify for. This empowers you to negotiate with the dealership as a cash buyer, focusing on the vehicle price rather than getting swayed by their financing offers.

The FCCU Car Loan Application Process: A Step-by-Step Guide

Applying for a car loan can seem daunting, but FCCU strives to make the process as straightforward as possible for its members. Being prepared and understanding each step will significantly ease your journey.

1. Become an FCCU Member (If You Aren’t Already):

As a credit union, FCCU requires membership to access their loan products. This usually involves meeting specific eligibility criteria and opening a savings account with a small deposit. It’s a simple initial step that unlocks a world of member benefits.

2. Gather Your Documents:

Preparation is key. You’ll typically need to provide:

- Proof of Identity: Government-issued ID (driver’s license, passport).

- Proof of Income: Pay stubs, W-2 forms, tax returns, or bank statements.

- Proof of Residency: Utility bill or lease agreement.

- Vehicle Information: If you’ve already chosen a car, details like the VIN, make, model, and mileage will be needed.

- Existing Loan Information: If you’re refinancing, you’ll need details about your current auto loan.

3. Complete the Application:

FCCU offers various ways to apply: online, over the phone, or in person at one of their branches. The application will ask for personal, financial, and employment information. Be thorough and accurate to avoid delays.

4. Await Decision and Review Loan Offer:

Once your application is submitted, FCCU’s lending team will review your financial profile. They will then present you with a loan offer detailing your approved loan amount, interest rate, and terms. Carefully review all aspects of the offer, including the annual percentage rate (APR), monthly payment, and total interest paid over the loan term.

5. Finalize and Fund:

If you accept the offer, you’ll sign the necessary paperwork. FCCU will then disburse the funds directly to you, the dealership, or your previous lender (for refinancing). You’re then ready to enjoy your new ride!

Common mistakes to avoid are rushing the application or not having all your documents ready. This can lead to delays or even a less favorable outcome.

Key Factors Affecting Your FCCU Car Loan Rate: An In-Depth Look

Understanding the individual weight of each factor influencing your FCCU car loan rate empowers you to take proactive steps to secure the best deal. Let’s delve deeper into these critical elements.

Your Credit Score: The Cornerstone of Your Rate

Your credit score is a numerical representation of your creditworthiness. It tells lenders, including FCCU, how reliably you’ve managed debt in the past. A higher score signifies a lower risk of default.

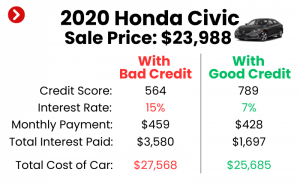

- Excellent Credit (780+): Borrowers in this range typically qualify for the lowest advertised FCCU car loan rates. They demonstrate a strong history of on-time payments and responsible credit use.

- Good Credit (670-779): Most borrowers fall into this category. You’ll likely receive competitive rates, though perhaps not the absolute lowest.

- Fair Credit (580-669): You may still qualify for an FCCU car loan, but the interest rate will be higher to compensate for the increased risk.

- Poor Credit (Below 580): Securing a car loan can be challenging with a poor credit score, and rates will be significantly higher. FCCU, as a member-focused institution, may offer options or guidance, but expect less favorable terms.

Pro Tip: Before applying, obtain a copy of your credit report from all three major bureaus (Experian, Equifax, TransUnion). Review it for errors and dispute any inaccuracies, as this could immediately boost your score. For a deeper dive into improving your credit score, check out our guide on . To get a comprehensive understanding of your credit report and scores, we recommend visiting a trusted source like Experian, Equifax, or TransUnion. You can get your free credit report annually at .

The Impact of Loan Term: Balancing Payments and Total Cost

The loan term refers to the duration over which you agree to repay the loan. This choice significantly affects both your monthly payment and the total interest you’ll pay.

- Shorter Loan Terms (e.g., 36 or 48 months): These typically come with lower interest rates because the lender’s money is tied up for a shorter period. Your monthly payments will be higher, but you’ll pay less interest overall and own your car outright sooner.

- Longer Loan Terms (e.g., 60 or 72 months): These terms offer lower monthly payments, making the car more "affordable" on a month-to-month basis. However, you’ll pay significantly more in total interest over the life of the loan, and your car may depreciate faster than you pay it off, leading to negative equity.

Based on my experience, many people focus solely on the monthly payment. While important, always consider the total cost of the loan. A slightly higher monthly payment on a shorter term often saves you thousands in interest.

The Power of a Down Payment: Reducing Risk, Improving Rates

A down payment is the initial amount of money you pay upfront for the car. It directly reduces the amount you need to borrow.

- Reduced Loan Amount: A larger down payment means a smaller principal loan amount, which translates to lower monthly payments and less interest paid overall.

- Lower Risk for Lender: By putting more money down, you demonstrate a stronger commitment to the purchase and reduce the lender’s exposure to risk, especially in the event of default or rapid depreciation. This reduced risk often results in a more favorable interest rate from FCCU.

- Avoid Negative Equity: A substantial down payment helps prevent you from owing more on your car than it’s worth (negative equity), particularly early in the loan term when depreciation is highest.

Pro tips from us: Aim for at least a 10-20% down payment, especially for new vehicles. For used cars, a larger down payment is even more beneficial due to potentially faster depreciation.

Debt-to-Income (DTI) Ratio: Your Financial Stability Indicator

Your DTI ratio is a percentage that compares your total monthly debt payments to your gross monthly income. Lenders use it to assess your ability to manage additional debt.

- Calculation: (Total Monthly Debt Payments / Gross Monthly Income) x 100

- Lender Preference: FCCU, like other lenders, prefers a lower DTI ratio. A DTI of 36% or less is generally considered ideal, with no more than 28% of that going towards housing costs. A high DTI indicates you might be overextended financially, increasing the perceived risk.

- Improving Your DTI: Pay down existing debts (credit cards, personal loans), avoid taking on new debt before applying for a car loan, or look for ways to increase your income.

Vehicle Type and Age: New vs. Used Car Rates

The type and age of the vehicle you intend to purchase play a role in the interest rate you’ll receive.

- New Car Rates: Generally lower due to several factors: new cars typically have higher resale value initially, come with manufacturer warranties, and are seen as less of a risk for mechanical failure.

- Used Car Rates: Tend to be slightly higher. This is because used cars have already depreciated, and their future reliability can be less predictable. The older and higher mileage a used car has, the higher the perceived risk, which often translates to a higher interest rate.

FCCU will assess the specific vehicle you’re interested in, alongside your personal financial profile, to determine the appropriate rate.

Maximizing Your Chances for the Best FCCU Car Loan Rates

Armed with an understanding of what drives FCCU car loan rates, let’s explore practical strategies to help you secure the most advantageous terms possible.

1. Know Your Credit Score (and Improve It):

As discussed, your credit score is paramount. Get your free credit report, review it thoroughly, and dispute any errors. If your score is less than ideal, take steps to improve it before applying: pay bills on time, reduce credit card balances, and avoid opening new credit accounts.

2. Get Pre-Approved by FCCU:

This is a powerful negotiation tool. A pre-approval tells you exactly how much you can borrow and at what rate. It allows you to shop for a car with confidence, knowing your financing is already in place. You can then focus on negotiating the vehicle’s price, separate from the financing.

3. Make a Substantial Down Payment:

The more money you put down upfront, the less you need to borrow, and the lower your monthly payments and total interest will be. A larger down payment also signals financial strength to FCCU, potentially qualifying you for a lower rate.

4. Opt for a Shorter Loan Term (If Feasible):

While longer terms mean lower monthly payments, shorter terms generally come with lower interest rates and save you money in the long run. Calculate what you can comfortably afford each month and choose the shortest term possible without straining your budget.

5. Consider a Co-Signer (Carefully):

If your credit score is a concern, a co-signer with excellent credit can help you qualify for a better rate. However, this is a significant responsibility for the co-signer, as they are equally liable for the loan. This decision should be made with careful consideration and clear communication.

6. Negotiate the Car Price Separately:

Never discuss financing until you’ve agreed on the final purchase price of the vehicle. Dealerships often try to roll these discussions together, which can make it harder to see where you’re getting the best deal. With FCCU pre-approval in hand, you control the financing aspect.

Common Mistakes to Avoid:

- Focusing Only on Monthly Payments: This can lead to longer loan terms and significantly more interest paid over time. Always look at the total cost of the loan.

- Applying to Too Many Lenders: Each hard inquiry on your credit report can slightly ding your score. Shop around, but do so within a focused timeframe (usually 14-45 days) to minimize the impact on your score.

- Not Reading the Fine Print: Always understand all terms and conditions of your loan agreement before signing.

Real-World Scenarios: How Rates Can Vary

Let’s illustrate how different profiles might experience FCCU car loan rates. These are hypothetical examples but reflect real-world lending scenarios.

Scenario 1: The Savvy Borrower

- Credit Score: 790 (Excellent)

- Down Payment: 20%

- Loan Term: 48 months

- Vehicle: New sedan

- Outcome: This borrower is likely to qualify for FCCU’s absolute lowest advertised rates, enjoying minimal interest payments and a quick path to ownership.

Scenario 2: The Average Borrower

- Credit Score: 690 (Good)

- Down Payment: 10%

- Loan Term: 60 months

- Vehicle: 3-year-old used SUV

- Outcome: This borrower will likely receive a competitive rate, but slightly higher than the savvy borrower. The longer term and used vehicle might add a percentage point or two to the rate, but still significantly better than subprime options.

Scenario 3: The Borrower Building Credit

- Credit Score: 620 (Fair)

- Down Payment: 5%

- Loan Term: 72 months

- Vehicle: 7-year-old used compact car

- Outcome: This borrower will face higher interest rates due to the lower credit score, minimal down payment, and older vehicle. While FCCU might still approve the loan, the monthly payments will be manageable, but the total interest paid will be considerably higher compared to the other scenarios. This borrower might consider a co-signer or focusing on credit improvement before purchasing.

These scenarios highlight the direct correlation between your financial profile and the FCCU car loan rates you’ll receive.

Frequently Asked Questions (FAQs) About FCCU Car Loans

Here are some common questions prospective borrowers have regarding FCCU car loans:

- How long does it take to get approved for an FCCU car loan?

Often, pre-approvals can be processed quickly, sometimes within hours or one business day, especially if you apply online and have all necessary documents ready. - Can I get an FCCU car loan with bad credit?

While challenging, FCCU’s member-first approach means they might be more willing to work with you than traditional banks. Options like a co-signer or smaller loan amounts might be available, but expect higher rates. - What if I’m not an FCCU member yet?

You can typically apply for membership and a loan simultaneously. Membership is usually a quick process involving opening a basic savings account. - Does FCCU offer GAP insurance?

Many credit unions, including FCCU, offer Guaranteed Asset Protection (GAP) insurance, which covers the difference between what you owe on your car and its actual cash value if it’s totaled or stolen. It’s often a smart consideration. - Can I apply for an FCCU car loan for a private party sale?

Yes, FCCU often provides financing for vehicles purchased from private sellers, not just dealerships. The process might require additional documentation for the vehicle’s title and condition.

Driving Forward with Confidence

Securing a car loan is a significant financial decision, and understanding every aspect of the process is crucial. First Community Credit Union stands out as a strong contender for auto financing, primarily due to its member-focused philosophy, which often translates into competitive FCCU car loan rates and personalized service.

By diligently preparing your finances, understanding the factors that influence your rate, and strategically navigating the application process, you can significantly increase your chances of securing the best possible terms. Remember, an informed borrower is an empowered borrower. Take the time to build your credit, save for a down payment, and get pre-approved.

With FCCU, you’re not just getting a loan; you’re gaining a financial partner dedicated to helping you achieve your goals. Drive confidently knowing you’ve made a smart choice for your vehicle and your wallet. Start your journey today by exploring FCCU’s offerings and taking control of your auto financing experience.