Unlocking the Road Ahead: A Deep Dive into "Loan A Car Meaning" and Smart Vehicle Financing

Unlocking the Road Ahead: A Deep Dive into "Loan A Car Meaning" and Smart Vehicle Financing Carloan.Guidemechanic.com

The desire for personal mobility often leads us to consider purchasing a car. For many, a significant upfront cash payment simply isn’t feasible. This is where the concept of "loaning a car" comes into play – a phrase that, while seemingly straightforward, encompasses a complex and crucial aspect of modern vehicle acquisition. Far from simply borrowing a friend’s ride, understanding the true "loan a car meaning" is the first step toward making an informed financial decision that puts you in the driver’s seat of your own vehicle.

As an expert in auto finance and a seasoned blogger, I’ve witnessed countless individuals navigate the exciting yet often confusing world of car loans. My goal with this comprehensive guide is to demystify the entire process, providing you with the knowledge and confidence to secure the best possible financing for your next car. We’ll explore not just what it means, but how it works, what to watch out for, and how to succeed.

Unlocking the Road Ahead: A Deep Dive into "Loan A Car Meaning" and Smart Vehicle Financing

What Exactly Does "Loan A Car" Mean? The Core Concept Explained

When we talk about "loaning a car" in the context of vehicle acquisition, we are primarily referring to taking out a loan to purchase an automobile. It’s about securing the necessary funds from a lender to cover the cost of a vehicle, which you then repay over a set period, typically with interest. This isn’t about someone lending you their car; it’s about a financial institution lending you money to buy your own car.

The process essentially turns a large, immediate expense into manageable monthly payments. Instead of needing tens of thousands of dollars available in cash, you pay a smaller sum each month until the original loan amount, plus any accrued interest, is fully satisfied. This fundamental understanding is critical for anyone considering vehicle ownership.

Based on my experience, many people initially confuse this with short-term car rentals or personal loans that might be used for other purposes. However, a car loan is specifically structured for vehicle acquisition, often using the car itself as collateral. This distinction is vital for understanding the terms and conditions you’ll encounter.

The Anatomy of a Car Loan: Key Components You Need to Know

To truly grasp the "loan a car meaning," you must understand its core components. These elements dictate your financial commitment and the overall cost of borrowing.

1. The Principal Amount

This is the initial sum of money you borrow from the lender. It covers the purchase price of the car, minus any down payment you make, and potentially includes taxes, fees, and the cost of any extended warranties or add-ons you finance. The principal is the foundation upon which all other calculations are built.

2. The Interest Rate (APR)

The interest rate is essentially the cost of borrowing money, expressed as a percentage of the principal. It’s the profit the lender makes for providing you with the funds. The Annual Percentage Rate (APR) includes not just the interest rate but also other fees associated with the loan, giving you a more complete picture of the annual cost. A lower APR means less money paid over the life of the loan.

Pro tip from us: Don’t just look at the monthly payment; always compare the APR across different loan offers. A seemingly low monthly payment over a very long term can hide a high overall cost due to interest.

3. The Loan Term

This refers to the duration over which you agree to repay the loan. Loan terms are typically expressed in months, such as 36, 48, 60, 72, or even 84 months. A longer loan term will result in lower monthly payments, but you’ll pay more in total interest over the life of the loan. Conversely, a shorter term means higher monthly payments but less total interest.

4. Monthly Payments

This is the fixed amount you pay back to the lender each month. It comprises a portion of the principal and a portion of the interest. These payments are crucial for budgeting and must be made consistently and on time to avoid penalties and negative impacts on your credit score.

5. Collateral

In most standard car loans, the vehicle itself serves as collateral. This means that if you fail to make your payments as agreed (default on the loan), the lender has the legal right to repossess the car to recover their losses. This is a significant aspect of securing a car loan and underscores the importance of responsible borrowing.

Different Paths to "Loan A Car": Understanding Loan Types

Not all car loans are created equal. Knowing the various types available can help you choose the option that best fits your financial situation and needs.

1. Direct Loans from Banks or Credit Unions

This is often considered the most traditional route. You apply for a car loan directly with a financial institution (your bank, a local credit union, or an online lender) before you even set foot in a dealership. If approved, you receive a pre-approval letter or a check for a certain amount. This essentially makes you a "cash buyer" at the dealership, giving you strong negotiating power on the vehicle’s price.

Based on my experience, securing a direct loan first is almost always a smarter move. It separates the financing negotiation from the car price negotiation, reducing pressure and often leading to better terms.

2. Dealership Financing (Indirect Loans)

When you arrange financing through the car dealership, they act as an intermediary. They submit your loan application to several different lenders (banks, credit unions, or their own captive finance companies like Ford Credit or Toyota Financial Services). The dealership then presents you with an offer, which may include a markup on the interest rate to cover their services.

While convenient, this method can sometimes lead to less favorable terms if you don’t shop around beforehand. It’s often where common mistakes are made, as buyers can be swayed by the excitement of a new car and less focused on the loan details.

3. New Car Loans vs. Used Car Loans

The type of car you purchase—new or used—will significantly impact your loan terms.

- New Car Loans typically offer lower interest rates and longer terms because new vehicles are less risky for lenders (they have a clear value and are less likely to break down immediately).

- Used Car Loans generally come with higher interest rates and shorter terms. Used cars are perceived as higher risk due to their age, mileage, and potential for unforeseen mechanical issues. The value of a used car also depreciates more rapidly.

4. Auto Loan Refinancing

Refinancing means replacing your existing car loan with a new one, usually with different terms. People often refinance to:

- Secure a lower interest rate, thus reducing their monthly payments or total interest paid.

- Change the loan term (e.g., extend it for lower payments or shorten it to pay off faster).

- Remove a co-signer from the loan.

Refinancing can be a smart move if your credit score has improved significantly since you first took out the loan, or if interest rates have dropped.

The Car Loan Process: Your Step-by-Step Journey to Ownership

Navigating the car loan process can seem daunting, but breaking it down into manageable steps makes it much clearer. From years of analyzing auto finance, I’ve found these steps to be crucial for a smooth and successful experience.

Step 1: Determine Your Budget and Needs

Before you even glance at a car, decide how much you can truly afford. This isn’t just about the monthly loan payment; it includes insurance, fuel, maintenance, and potential repair costs. Create a realistic budget that accounts for all these expenses.

Step 2: Check and Improve Your Credit Score

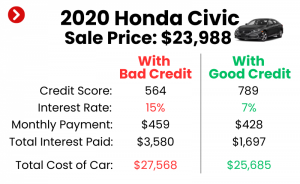

Your credit score is perhaps the single most influential factor in determining your loan’s interest rate. Lenders use it to assess your creditworthiness and risk. A higher score (generally 700+) will unlock the best rates.

Pro tip: Get a copy of your credit report from all three major bureaus (Experian, Equifax, TransUnion) well in advance. Correct any errors and, if possible, take steps to improve your score, such as paying down other debts or making all payments on time. (For more detailed strategies on improving your credit, you might find our article on "Boosting Your Credit Score for Big Purchases" incredibly helpful.)

Step 3: Get Pre-Approved for a Loan

This is a critical step that empowers you. Apply for a loan with several lenders (banks, credit unions, online lenders). Pre-approval gives you a concrete offer, including an interest rate and maximum loan amount, before you start car shopping. This sets a benchmark for any offers you receive from dealerships.

Step 4: Shop for Your Car (and Negotiate!)

With pre-approval in hand, you’re now equipped to shop for a car. Focus on negotiating the vehicle’s price, knowing you already have your financing secured. Treat your pre-approval as your "cash in hand."

Step 5: Finalize the Loan and Understand the Paperwork

Once you’ve chosen your car and agreed on a price, you’ll finalize the loan. This involves signing a mountain of paperwork. Common mistakes to avoid are rushing through this stage or failing to read every single document. Pay close attention to:

- The Promissory Note: Your promise to repay the loan.

- The Loan Agreement: Details the terms, conditions, interest rate, and payment schedule.

- Truth in Lending Disclosure: Summarizes key loan terms, including the APR and total finance charges.

- Security Agreement: States that the car is collateral for the loan.

Ensure the final numbers match what you agreed upon.

Key Factors Influencing Your Car Loan Terms

Several variables come into play when lenders determine your eligibility and the terms of your "loan a car" agreement. Understanding these factors can help you position yourself for the most favorable outcome.

1. Your Credit Score and History

As mentioned, this is paramount. A strong credit history demonstrates your reliability as a borrower. Lenders look for consistent on-time payments, a low debt-to-income ratio, and a diverse credit mix. Conversely, late payments, defaults, or bankruptcies will signal higher risk, leading to higher interest rates or even loan denial.

2. Your Down Payment

The amount of money you pay upfront significantly impacts your loan. A larger down payment reduces the principal amount you need to borrow, which in turn means lower monthly payments and less total interest paid over the life of the loan. It also reduces the risk for the lender, potentially securing you a better interest rate.

Pro tips from us: Aim for at least a 20% down payment for new cars and 10% for used cars if possible. This helps mitigate depreciation and reduces the risk of being "upside down" on your loan (owing more than the car is worth).

3. The Loan Term (Length of Repayment)

While longer terms offer lower monthly payments, they come with a hidden cost: significantly more interest paid over time. Shorter terms, though demanding higher monthly payments, result in substantial savings on interest and allow you to own your car free and clear much faster.

4. The Interest Rate (APR) Offered

This is the direct cost of borrowing. Rates vary widely based on your creditworthiness, the lender, the loan term, and current market conditions. Shopping around and comparing multiple APR offers is crucial for securing the best deal.

5. Your Debt-to-Income (DTI) Ratio

Lenders assess your DTI ratio to understand your capacity to take on new debt. It compares your total monthly debt payments to your gross monthly income. A lower DTI indicates you have more disposable income to cover new loan payments, making you a less risky borrower.

6. The Vehicle’s Age and Value

Newer, lower-mileage vehicles typically qualify for better loan terms due to their higher resale value and lower perceived risk. Older, higher-mileage vehicles may face higher interest rates and shorter terms, reflecting the increased risk of mechanical issues and faster depreciation. (For a deeper understanding of how vehicle value changes over time, our blog post on "Understanding Car Depreciation: What Every Buyer Needs to Know" offers valuable insights.)

The Upside of "Loaning a Car": Benefits of Financing Your Vehicle

While the financial commitment is substantial, financing a car offers several compelling advantages for many individuals.

1. Accessibility to Reliable Transportation

For most people, paying cash for a car, especially a new or higher-end model, is simply not an option. Car loans make reliable transportation accessible, allowing individuals to commute to work, transport family, and fulfill essential daily tasks without waiting years to save. This immediate access to personal mobility can significantly improve quality of life and career opportunities.

2. Building and Improving Your Credit History

Successfully managing a car loan is an excellent way to build a strong credit history. Consistent, on-time payments demonstrate financial responsibility to credit bureaus, which can positively impact your credit score. A good credit score opens doors to better terms on future loans (mortgages, personal loans) and other financial products.

3. Spreading Out a Large Expense

A car purchase represents a significant financial outlay. Financing allows you to spread this cost over several years, making it more manageable within your monthly budget. This prevents you from depleting your savings or delaying other important financial goals.

4. Immediate Ownership and Use

Unlike leasing, where you never truly own the vehicle, a car loan grants you ownership from day one (though the lender holds the title until the loan is paid off). This means you have the freedom to customize your car, drive unlimited miles, and build equity in the asset over time.

Navigating the Downside: Potential Pitfalls and Risks

Understanding the "loan a car meaning" also involves recognizing the potential downsides and risks associated with vehicle financing. Being aware of these can help you make more prudent decisions.

1. Accumulating Significant Debt

Taking on a car loan means adding a substantial monthly debt payment to your financial obligations. Over-borrowing or choosing a vehicle that’s too expensive for your budget can strain your finances, making it difficult to save or manage other expenses.

2. High Interest Rates and Total Cost

Poor credit, a small down payment, or a long loan term can lead to high interest rates, dramatically increasing the total amount you pay for the car over time. What initially seems like an affordable monthly payment can balloon into thousands of extra dollars in interest.

3. Vehicle Depreciation

Cars begin to depreciate the moment they leave the lot. This means their value decreases over time. When you finance a car, you’re paying off a loan on an asset that is continuously losing value. This dynamic is crucial to understand.

4. Negative Equity (Being "Upside Down")

This occurs when you owe more on your car loan than the car is currently worth. It’s a common problem, especially with small down payments and long loan terms. If your car is totaled or stolen while you have negative equity, your insurance payout might not cover the remaining loan balance, leaving you to pay the difference out of pocket. Gap insurance can protect against this.

5. Repossession Risk

As the car serves as collateral, failing to make your payments can lead to the lender repossessing your vehicle. This not only results in the loss of your car but also severely damages your credit score, making it difficult to secure future loans.

Pro Tips for Securing the Best Car Loan Deal

Based on my extensive background in finance, here are actionable strategies to ensure you get the most favorable terms when you "loan a car."

- Shop Around for Lenders: Never settle for the first loan offer. Contact multiple banks, credit unions, and online lenders. Compare their APRs, terms, and fees. This competition forces lenders to offer their best rates.

- Boost Your Credit Score: As emphasized earlier, a higher credit score is your golden ticket to lower interest rates. Take proactive steps to improve it before applying.

- Make a Substantial Down Payment: The more you pay upfront, the less you borrow, which means lower payments and less interest. It also reduces your risk of negative equity.

- Understand All Terms and Fees: Read the fine print! Don’t just focus on the monthly payment. Understand the total cost of the loan, including all fees, interest, and any penalties for late payments or early payoff.

- Negotiate the Car Price Separately from the Loan: This is a crucial strategy. Secure your financing first (pre-approval), then use that leverage to negotiate the best possible price for the vehicle. This prevents the dealer from masking a high car price with seemingly good loan terms.

- Avoid Unnecessary Add-ons: Dealerships often push extras like extended warranties, rustproofing, or fabric protection. While some might be useful, many are overpriced and can significantly inflate your loan amount. Only agree to what you genuinely need and understand.

Common Mistakes to Avoid When Loaning a Car

To truly master the "loan a car meaning," you must also be aware of the pitfalls that trap many unsuspecting buyers.

- Focusing Only on the Monthly Payment: This is perhaps the biggest mistake. A low monthly payment can be achieved by extending the loan term for a very long time, leading to significantly more interest paid overall. Always consider the total cost of the loan.

- Not Getting Pre-Approved: Walking into a dealership without pre-approval puts you at a disadvantage. You lose negotiating power and might accept less favorable financing terms offered by the dealer.

- Ignoring the Total Cost of Ownership: Beyond the loan payment, remember to factor in insurance, fuel, maintenance, and registration. A car that seems affordable on paper might be a budget-buster once all costs are considered.

- Extending the Loan Term Too Much: While a 72- or 84-month loan might offer a tempting low monthly payment, you’ll pay a lot more in interest and risk being upside down on your loan for a longer period. Try to keep loan terms to 60 months or less.

- Skipping the Fine Print: As an expert, I can’t stress this enough. Every line in the loan agreement matters. Rushing through it can lead to costly surprises down the road. Take your time, ask questions, and ensure you understand everything before signing.

When is Loaning a Car the Right Choice for You?

Deciding whether to "loan a car" is a personal financial decision. It’s the right choice if:

- You have financial stability: A steady income and a clear budget that can comfortably accommodate the monthly payments, insurance, and other car-related expenses.

- You need reliable transportation: Your lifestyle or job requires a dependable vehicle, and you don’t have the immediate cash to purchase one outright.

- You can manage payments responsibly: You have a history of making on-time payments and are committed to adhering to the loan agreement to build positive credit.

- You’ve done your homework: You’ve researched, compared offers, and understand all aspects of the loan before committing.

Remember, a car loan is a serious financial commitment. It’s not just about getting the keys; it’s about responsibly managing debt for years to come.

Conclusion: Driving Forward with Confidence

Understanding the "loan a car meaning" is far more than a simple definition; it’s a foundational lesson in personal finance and smart consumerism. It’s about recognizing that you’re not just buying a vehicle, but entering into a legally binding agreement that requires careful consideration, diligent research, and responsible management.

By internalizing the components of a loan, exploring different financing avenues, and applying the expert tips shared here, you empower yourself to make informed decisions. You move from being a passive borrower to an active participant, capable of securing favorable terms and avoiding common pitfalls. So, as you prepare to hit the road in your next vehicle, remember that the journey to ownership begins with a clear understanding of your financial choices. Drive wisely, plan carefully, and enjoy the freedom that comes with making a smart car loan decision.

External Resource: For more general information on understanding loans and credit, the Consumer Financial Protection Bureau (CFPB) offers excellent resources: https://www.consumerfinance.gov/ (Please note: This is a placeholder link to a reputable financial organization. In a live blog, ensure the specific page linked is highly relevant to general loan education).