Unlocking the Road Ahead: Your Comprehensive Guide to Getting a Car Loan with Bad Credit

Unlocking the Road Ahead: Your Comprehensive Guide to Getting a Car Loan with Bad Credit Carloan.Guidemechanic.com

Navigating the world of car loans can feel like a daunting journey, especially when your credit history isn’t sparkling. Many people believe that bad credit automatically slams the door shut on their dreams of owning a vehicle. However, based on my extensive experience in the financial and automotive sectors, I can confidently tell you that this simply isn’t true. While it presents unique challenges, securing a car loan with bad credit is absolutely possible.

This in-depth guide is designed to empower you with the knowledge, strategies, and confidence needed to successfully secure an auto loan, even if your credit score has seen better days. We’ll explore the realities of bad credit car loans, common pitfalls to avoid, and actionable steps you can take to drive off the lot in your new (or new-to-you) car. Our ultimate goal is to provide real value, helping you understand not just if you can get a loan, but how to get the best possible terms.

Unlocking the Road Ahead: Your Comprehensive Guide to Getting a Car Loan with Bad Credit

Understanding the Landscape: What Bad Credit Really Means for Car Loans

Before diving into solutions, it’s crucial to understand what "bad credit" signifies in the eyes of a lender. Your credit score is essentially a three-digit report card on your financial reliability. It tells lenders how likely you are to repay borrowed money.

Typically, FICO scores range from 300 to 850, and VantageScore also uses a similar range. A score generally below 620 is often considered "subprime" or "bad credit." This range signals to lenders that you might have a history of late payments, defaults, bankruptcies, or high credit utilization.

Why Lenders Are Wary

From a lender’s perspective, a low credit score indicates a higher risk. They see a greater chance that you might default on your loan, leading to financial loss for them. This increased risk often translates into less favorable loan terms for you, such as higher interest rates and potentially larger down payment requirements.

However, it’s important to remember that not all lenders operate with the same criteria. Some specialize in working with individuals who have less-than-perfect credit, understanding that everyone deserves a second chance or encounters financial difficulties. This is where your strategy becomes paramount.

The Good News: Getting a Car Loan with Bad Credit Is Attainable

Let’s be clear: getting a car loan with bad credit isn’t a myth. While it might require more effort and a different approach than someone with excellent credit, countless individuals successfully secure auto financing every day despite their credit history. The key is setting realistic expectations and understanding the factors that can significantly improve your chances.

Setting Realistic Expectations

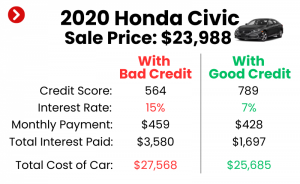

Firstly, you might not qualify for the absolute lowest interest rates advertised. Those rates are typically reserved for borrowers with prime or super-prime credit scores. Expect a higher Annual Percentage Rate (APR) due to the increased risk lenders are taking.

Secondly, the type of car you can afford might be different. Lenders may be more comfortable approving loans for more moderately priced vehicles, as this reduces their potential loss if you default. Focus on reliability and affordability over luxury when starting your search.

Key Strategies to Dramatically Boost Your Chances of Approval

Securing a car loan with bad credit requires a proactive and strategic approach. Based on my experience, the more prepared and informed you are, the better your outcomes will be. Here are some indispensable strategies:

1. Know Your Credit Score and History Inside Out

This is your starting point. Before you even think about stepping onto a car lot or applying for a loan, pull your credit reports from all three major bureaus (Experian, Equifax, and TransUnion). You are entitled to a free report from each once a year via AnnualCreditReport.com.

Review these reports meticulously for any errors or inaccuracies. Disputing and correcting errors can potentially boost your score relatively quickly. Understanding what negative items are affecting your score will also help you explain your situation to a lender, showing that you are aware and responsible.

2. Save Up a Substantial Down Payment

One of the most powerful tools you have when seeking a car loan with bad credit is a significant down payment. Lenders view a larger down payment as a sign of your commitment and ability to manage finances. It also reduces the amount you need to borrow, thereby lowering the lender’s risk.

Pro tips from us: Aim for at least 10-20% of the car’s purchase price. Not only does this improve your approval chances, but it also lowers your monthly payments and reduces the total interest paid over the life of the loan. A larger down payment can also help you avoid being "upside down" on your loan (owing more than the car is worth) early on.

3. Consider a Co-signer with Good Credit

If you have a trusted friend or family member with a strong credit history, asking them to co-sign your loan can significantly improve your chances of approval and potentially secure a lower interest rate. A co-signer essentially guarantees to repay the loan if you default, mitigating the lender’s risk.

However, this decision should not be taken lightly. Common mistakes to avoid are not fully understanding the co-signer’s responsibility. If you miss payments, it impacts their credit score, and they are legally obligated to pay the debt. Ensure both parties understand the implications fully before proceeding.

4. Create a Realistic Budget and Stick to It

Before even looking at cars, determine what you can genuinely afford for a monthly car payment, including insurance, fuel, and maintenance. Lenders will assess your debt-to-income (DTI) ratio to ensure you aren’t overextending yourself. A DTI of 43% or less is generally preferred.

Showing a lender that you have a clear understanding of your financial limits and a stable income to support the payments demonstrates responsibility. This financial prudence can go a long way in swaying a lender’s decision, even with a lower credit score.

5. Shop Smart: Get Pre-approved Before Visiting Dealerships

Many lenders, including banks, credit unions, and online providers, offer pre-approval processes. Getting pre-approved means a lender has reviewed your financial information and provisionally agreed to lend you a certain amount at a specific interest rate. This is a "soft inquiry" that doesn’t hurt your credit score.

Armed with a pre-approval, you become a cash buyer at the dealership, giving you significant negotiation power. It also helps you set a clear budget and avoids the pressure of dealership finance departments pushing you into less favorable terms. It’s a proactive step that puts you in control.

6. Explore Different Lender Types

Not all lenders are created equal, especially when it comes to bad credit car loans. Diversifying your search can uncover better opportunities.

Subprime Lenders and Special Finance Dealerships

These lenders specialize in working with borrowers who have low credit scores. They understand the challenges and have financing programs tailored for such situations. While their interest rates might be higher, they are often more willing to approve loans. Many dealerships have "special finance" departments dedicated to these types of loans.

Credit Unions

Credit unions are member-owned financial institutions often known for more flexible lending criteria and lower interest rates compared to traditional banks, even for those with bad credit. If you’re a member or qualify for membership, this can be an excellent option.

Online Lenders

A growing number of online lenders specialize in bad credit auto loans. They often have streamlined application processes and can provide quick decisions. However, always research their reputation and read reviews before applying.

Buy Here, Pay Here (BHPH) Dealerships

BHPH dealerships finance loans in-house, meaning they are both the seller and the lender. They often approve buyers with very poor credit, as they focus more on your income stability than your credit score.

While convenient, BHPH loans typically come with significantly higher interest rates, shorter repayment terms, and limited vehicle selection. Pro tips from us: Use BHPH as a last resort, and always read the fine print carefully, as they can sometimes lead to predatory lending practices.

Preparing Your Application: What Lenders Want to See

Once you’ve identified potential lenders, you’ll need to prepare a comprehensive application. Lenders want to see stability and an ability to repay the loan.

Essential Documents and Information

Be ready to provide:

- Proof of Income: Recent pay stubs (typically 1-2 months), tax returns (if self-employed), or bank statements showing consistent deposits.

- Proof of Residency: Utility bills, lease agreements, or mortgage statements to verify your address.

- Identification: A valid driver’s license.

- References: Sometimes personal or professional references are requested.

- Down Payment: Be ready to show proof of funds for your down payment.

Showing up prepared with all necessary documentation demonstrates your seriousness and responsibility, which can positively influence a lender’s decision.

Common Mistakes to Avoid When Seeking a Bad Credit Car Loan

Based on my experience, many individuals make critical errors that can jeopardize their chances or lead to unfavorable loan terms. Avoiding these pitfalls is crucial.

1. Applying Everywhere Indiscriminately

Each time you apply for credit, it typically results in a "hard inquiry" on your credit report, which can temporarily lower your score. Spreading out applications over a long period can damage your credit further.

Pro tips from us: Group your applications within a short timeframe (e.g., 14-45 days, depending on the scoring model). Credit scoring models often count multiple auto loan inquiries within this window as a single inquiry, recognizing that you’re rate shopping.

2. Not Reading the Fine Print

This is a common mistake for any financial product, but it’s especially critical with bad credit car loans. High interest rates, hidden fees, and restrictive terms can lurk within the contract.

Always take your time to read the entire loan agreement. If you don’t understand something, ask for clarification. Don’t be pressured into signing anything you’re uncomfortable with.

3. Ignoring the Annual Percentage Rate (APR)

Focusing solely on the monthly payment can be misleading. A low monthly payment might mean a longer loan term and significantly more interest paid over time. The APR reflects the true annual cost of borrowing, including interest and some fees.

Always compare APRs across different loan offers. A lower APR, even with a slightly higher monthly payment, usually means a better deal in the long run.

4. Falling for "Guaranteed Approval" or "No Credit Check" Scams

Be extremely wary of any lender promising "guaranteed approval" regardless of your credit score, or "no credit check" car loans, unless it’s a legitimate Buy Here, Pay Here dealer (which, as discussed, has its own caveats). These often come with exorbitant interest rates, hidden fees, or predatory terms designed to trap you.

If an offer sounds too good to be true, it almost certainly is. Legitimate lenders will always assess your ability to repay, even if they specialize in bad credit loans.

The Road Ahead: Improving Your Credit for the Future

Getting a car loan with bad credit isn’t just about securing the vehicle; it’s also an opportunity to rebuild your financial health. Your new auto loan can be a powerful tool for improving your credit score, opening doors to better financial opportunities in the future.

Making Timely Payments

This is the most critical step. Consistently making your car loan payments on time, every time, will gradually build a positive payment history, which is the largest factor in your credit score. Each on-time payment demonstrates reliability to credit bureaus.

Reducing Other Debts

While focusing on your car loan, also work on reducing other outstanding debts, especially high-interest credit card balances. A lower debt-to-income ratio and improved credit utilization can further boost your score. For more tips on improving your credit score, check out our guide on .

Monitor Your Credit Regularly

Continue to check your credit reports periodically. This helps you track your progress, identify any new errors, and understand the impact of your responsible financial behavior. Free credit monitoring services are widely available through various financial institutions.

Pro Tips from an Expert: Beyond the Basics

As someone who has seen countless individuals navigate this process, I have a few additional insights that can make a significant difference.

Negotiation is Still Key

Even with bad credit, don’t be afraid to negotiate. This applies to the car’s price, the trade-in value (if applicable), and even the loan terms. While your negotiation leverage on the interest rate might be limited, you can still haggle on the overall vehicle price. Every dollar saved on the purchase price is a dollar less you need to borrow and pay interest on.

Understand the Total Cost of Ownership

Beyond the monthly payment, factor in the total cost of owning the car. This includes insurance, fuel, maintenance, and potential repairs. A cheaper car might have higher maintenance costs, negating any initial savings. A reliable, slightly older model might be a smarter financial decision than a brand-new car you can barely afford.

The Long-Term View

Think of this car loan as a stepping stone. Your primary goal is to get reliable transportation, but your secondary goal should be to use this opportunity to build excellent credit. Once you’ve established a consistent payment history, you may be able to refinance your loan at a lower interest rate down the line, saving you thousands of dollars. We have another article that delves into for more details.

Conclusion: Your Journey to a Car Loan with Bad Credit Starts Now

Securing a car loan with bad credit is not just a pipe dream; it’s a realistic goal achievable through diligent preparation, smart decision-making, and a clear understanding of the lending landscape. By knowing your credit, saving for a down payment, exploring diverse lenders, and avoiding common mistakes, you significantly increase your chances of driving away with a deal that works for you.

Remember, this process is about more than just getting a car; it’s about taking control of your financial future. Use this opportunity to not only gain reliable transportation but also to rebuild your credit and pave the way for a more stable financial tomorrow. The road ahead may have a few bumps, but with the right approach, you can navigate them successfully and reach your destination. For more unbiased information on managing debt and improving your financial health, consider visiting a trusted resource like the Consumer Financial Protection Bureau (CFPB) website.