Unlocking the Road Ahead: Your Comprehensive Guide to Managing Two Car Loans as One Person

Unlocking the Road Ahead: Your Comprehensive Guide to Managing Two Car Loans as One Person Carloan.Guidemechanic.com

The idea of managing two car loans as one person might sound daunting, or even unnecessary, to some. However, in today’s dynamic world, it’s a reality for a growing number of individuals. Whether it’s for evolving family needs, a specialized work vehicle, or simply a passion for driving, the question isn’t just "Can I get two car loans?" but more importantly, "Should I, and if so, how do I manage them effectively?"

This article serves as your ultimate guide, diving deep into the complexities, opportunities, and potential pitfalls of navigating the automotive financing landscape with multiple vehicles. We’ll explore everything from eligibility criteria to smart financial strategies, ensuring you’re well-equipped to make informed decisions. Our goal is to provide real value, offering insights that are both practical and easy to understand, transforming what might seem like a financial tightrope walk into a manageable journey.

Unlocking the Road Ahead: Your Comprehensive Guide to Managing Two Car Loans as One Person

Can One Person Really Have Two Car Loans? The Eligibility Deep Dive

Yes, absolutely. It’s entirely possible for one person to have two car loans. Lenders don’t inherently restrict the number of auto loans an individual can hold. However, the approval for a second loan hinges entirely on your financial health and ability to demonstrate responsible debt management. It’s a rigorous assessment where your financial history speaks volumes.

Based on my experience, lenders are primarily concerned with your capacity to repay both debts concurrently. They scrutinize several key factors to determine if you pose an acceptable risk. Understanding these elements is crucial before you even consider applying for a second vehicle.

Your Credit Score: The Ultimate Financial Report Card

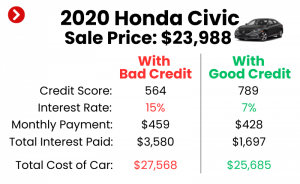

Your credit score is perhaps the single most influential factor in securing any loan, especially a second car loan. This three-digit number provides a snapshot of your creditworthiness, reflecting your payment history, outstanding debts, and length of credit history. A higher score signifies a lower risk to lenders.

When you already have an existing car loan, your credit score needs to be robust to absorb the impact of another significant debt. Lenders will look for a strong track record of on-time payments on your current loan and all other credit obligations. A score in the "good" to "excellent" range (typically 670 and above) significantly improves your chances of approval and securing favorable interest rates on the second loan.

Debt-to-Income (DTI) Ratio: Your Financial Balancing Act

The debt-to-income (DTI) ratio is arguably the most critical metric lenders use to assess your ability to take on additional debt. This ratio compares your total monthly debt payments to your gross monthly income. For instance, if your monthly income is $5,000 and your total monthly debt payments (including your first car loan, mortgage/rent, credit cards, student loans, and the proposed second car loan) add up to $2,000, your DTI would be 40% ($2,000 / $5,000).

Lenders generally prefer a DTI ratio of 36% or lower, though some might go up to 43-50% for well-qualified borrowers. Adding a second car loan will directly increase your debt portion, pushing your DTI higher. You must demonstrate that even with two car payments, your income comfortably supports all your financial obligations without overstretching your budget. This is where many aspiring two-car owners face their biggest hurdle. For more detailed information on debt-to-income ratios, you can refer to resources from the Consumer Financial Protection Bureau .

Income Stability and Employment History: A Steady Foundation

Lenders want to see a consistent and reliable source of income that can comfortably cover both loan payments, alongside your other living expenses. This means they will examine your employment history, looking for stability and longevity in your current role or industry. Typically, they prefer to see at least two years of consistent employment.

Having a steady job with a predictable income stream reassures lenders that you have the financial capacity to meet your obligations month after month. Self-employed individuals might face additional scrutiny, requiring more extensive documentation of their income over several years to prove stability.

Payment History: Your Track Record Matters

Your payment history across all your existing debts—not just your current car loan—is a critical indicator of your financial responsibility. Lenders will pull your credit report to see if you have a history of making payments on time, every time. Any late payments, defaults, or collections can significantly damage your chances of approval.

A flawless payment history on your first car loan demonstrates to lenders that you are a reliable borrower who honors their financial commitments. This track record builds trust and confidence, making them more inclined to extend another line of credit.

Down Payment: Reducing the Risk

While not always mandatory, making a substantial down payment on your second vehicle can significantly improve your chances of approval. A larger down payment reduces the amount you need to borrow, thereby lowering your monthly payments and decreasing the lender’s risk. It also shows a commitment to the purchase and a healthy financial position.

Pro tips from us: Even a 10-20% down payment can make a noticeable difference in both your approval odds and the overall cost of the loan due to potentially lower interest rates. It also helps in avoiding negative equity, where you owe more than the car is worth.

Loan-to-Value (LTV) Ratio: The Car’s Worth

The loan-to-value (LTV) ratio compares the amount of the loan to the market value of the car you’re purchasing. Lenders prefer a lower LTV, as it means less risk for them. For instance, if you’re buying a car worth $20,000 and taking out a $18,000 loan, your LTV is 90%.

A significant down payment directly impacts the LTV, bringing it down and making the loan more attractive to lenders. This is especially relevant for a second car, as lenders might be more conservative with their LTV requirements.

Why Would Someone Need Two Car Loans? Common Scenarios Unpacked

The notion of a single individual managing two car loans might seem unusual at first glance, but there are numerous legitimate and practical reasons why someone might find themselves in this situation. It’s often driven by evolving life circumstances or specific personal and professional needs that a single vehicle simply cannot fulfill.

Understanding these common scenarios can help you assess if taking on a second car loan aligns with your genuine requirements. It’s rarely about luxury and more often about necessity or strategic planning.

Evolving Family Needs and Separate Commutes

One of the most frequent reasons for needing a second vehicle is a change in family dynamics or commuting requirements. A growing family might necessitate a larger, more practical vehicle like an SUV or minivan, while the individual still needs a smaller, fuel-efficient car for their daily commute. For instance, one parent might need a reliable family hauler for school runs and errands, while the other requires a different car for a long, solo commute to work.

This scenario often arises when spouses have different work schedules or locations, making a single car impractical for coordinating pickups and drop-offs. Having two cars allows for greater independence and reduces logistical stress, especially if public transport isn’t a viable alternative.

Business Use: Personal Car Plus Work Vehicle

For entrepreneurs, contractors, or professionals whose work requires a specific type of vehicle, a second car loan can be a business necessity. Imagine a carpenter who needs a sturdy pickup truck for tools and materials but also desires a comfortable sedan for personal use and client meetings. Or a real estate agent who drives clients around in a professional, reliable vehicle, but wants a smaller, more economical car for their personal errands.

In these cases, the second vehicle isn’t just a convenience; it’s an essential tool for their livelihood. Keeping business and personal mileage separate can also offer tax advantages, making the two-car arrangement a smart financial decision in the long run.

Specialized Vehicles: Workhorse and Weekend Toy

Sometimes, the need for a second car stems from a desire for a specialized vehicle that complements a daily driver. This could involve a dedicated off-road vehicle for adventure enthusiasts, a classic car for weekend cruises, or a performance car for track days. These vehicles often serve a specific purpose that a standard commuter car cannot fulfill.

While these might seem like "wants" rather than "needs," for many, these specialized vehicles contribute significantly to their quality of life or hobbies. The key is ensuring that the financial commitment for such a vehicle doesn’t jeopardize the stability provided by the primary car loan.

Unexpected Circumstances: A Sudden Need

Life is unpredictable, and sometimes a second car loan becomes necessary due to unforeseen events. Perhaps your primary vehicle was totaled in an accident, and you need a replacement quickly but haven’t finished paying off the first loan, which is now tied up with insurance claims. Or a new job opportunity arises in a location not served by public transport, creating an immediate need for a second reliable vehicle.

In these situations, securing a second loan might be the most practical solution to maintain mobility and avoid significant disruptions to daily life. It highlights the importance of financial preparedness, even when facing unexpected challenges.

Lifestyle Choices: Convenience and Freedom

Beyond necessity, some individuals opt for two cars for the sheer convenience and freedom they offer. This might involve having a primary vehicle for everyday use and a smaller, more nimble car for city driving and easy parking, or vice-versa. It caters to a lifestyle where different types of vehicles are preferred for different situations.

This choice is often a reflection of personal preferences and a desire for maximum flexibility. While it incurs higher costs, for some, the benefits of tailored mobility outweigh the financial burden.

The "Should I?" – Pros and Cons of Managing Multiple Auto Loans

Deciding whether to take on a second car loan is a significant financial decision that requires careful consideration. It’s not just about qualifying; it’s about understanding the long-term impact on your financial health and lifestyle. Let’s weigh the advantages against the potential drawbacks.

The Advantages: More Than Just Convenience

Having two car loans can offer several compelling benefits, primarily centered around increased flexibility and meeting diverse needs.

1. Flexibility and Convenience: Double the Options

The most apparent advantage is the unparalleled flexibility. Two vehicles mean you’re not reliant on a single mode of transport. This is invaluable for households with multiple drivers, differing schedules, or those living in areas with limited public transportation. It offers freedom to pursue separate activities without logistical headaches.

For example, if one car breaks down, you still have a backup for essential travel. This peace of mind, knowing you won’t be stranded, is a significant plus for many individuals and families.

2. Meeting Diverse Needs: Tailored Transportation

As discussed earlier, different situations call for different vehicles. A robust truck for hauling equipment and a fuel-efficient sedan for commuting, or a family-friendly SUV and a sporty convertible for personal enjoyment. Two loans allow you to tailor your transportation to perfectly fit your varied lifestyle requirements.

This can lead to greater efficiency (using the right car for the right job) and enhanced satisfaction, as you’re not compromising on vehicle utility or personal preference.

3. Potential for Credit Building (If Managed Well)

Successfully managing two car loans can positively impact your credit score. By making consistent, on-time payments for both vehicles, you demonstrate to credit bureaus your ability to handle multiple lines of credit responsibly. This can strengthen your credit profile, potentially opening doors to better rates on future loans, like a mortgage.

However, this is a double-edged sword. Any missed payments can have a magnified negative effect, underscoring the importance of meticulous financial management.

The Disadvantages: A Heavier Financial Burden

While there are clear benefits, the downsides of taking on a second car loan are primarily financial and can be substantial. These are common mistakes to avoid: overstretching your budget and underestimating the total cost of ownership.

1. Significant Financial Strain: Double the Payments and Expenses

The most obvious drawback is the increased financial burden. You’re not just doubling your monthly car payments; you’re also doubling related expenses. This includes higher insurance premiums, increased maintenance costs (two cars, two sets of tires, two oil changes), and potentially higher fuel costs. This can quickly deplete your disposable income.

Based on my experience, many people underestimate the cumulative effect of these "small" expenses. They can add up to a significant portion of your budget, leaving less room for savings or other financial goals.

2. Increased Debt Burden: Impact on Future Borrowing

Taking on a second car loan significantly increases your overall debt-to-income ratio. A higher DTI can make it much harder to qualify for other substantial loans in the future, such as a mortgage or personal loans, or could result in less favorable terms. Lenders will view you as a higher risk due to your existing debt load.

This increased debt also reduces your financial flexibility. If an unexpected expense arises, your ability to borrow further or draw on existing credit lines might be limited.

3. Credit Score Risk: The Double-Edged Sword

While responsible management can build credit, the risk of damage is equally high. Missing payments on even one of the loans can severely impact your credit score. Missing payments on both simultaneously would be catastrophic. Each late payment on your credit report signals to lenders that you are a high-risk borrower.

This risk is amplified when managing two loans, as there’s a greater chance of oversight or financial strain leading to missed payments. It demands impeccable organization and strict budgeting.

4. Reduced Financial Flexibility and Savings

With two substantial monthly payments, plus all the associated costs, you’ll likely have less discretionary income. This can impact your ability to save for retirement, a down payment on a house, or an emergency fund. Your financial flexibility to handle unforeseen expenses or take advantage of investment opportunities will be significantly reduced.

Pro tips from us: Always prioritize building an emergency fund before taking on significant additional debt like a second car loan. This acts as a crucial safety net.

5. Higher Insurance Costs

Insuring two vehicles is considerably more expensive than insuring one. Even if you bundle policies, you’re looking at two sets of premiums, potentially with different coverage levels depending on the vehicle. This ongoing cost is often overlooked in initial budget calculations but can be a substantial monthly outflow.

6. Depreciation of Assets

Cars are depreciating assets. The moment you drive a new car off the lot, its value begins to drop. With two vehicles, you’re essentially doubling your exposure to this depreciation. This means a larger portion of your wealth is tied up in assets that are continually losing value, rather than appreciating.

Financial Implications and Strategies for Success

Successfully managing two car loans requires meticulous financial planning and a disciplined approach. It’s not just about making the payments; it’s about optimizing your financial health while doing so. Here are some key strategies to consider.

Budgeting: Your Financial Blueprint

The cornerstone of managing multiple loans is an ironclad budget. You need to have a clear, realistic understanding of your income versus your expenses. This budget must meticulously account for both car payments, insurance, fuel, maintenance, and all other fixed and variable costs. Use budgeting apps or spreadsheets to track every dollar.

Pro tips from us: Create a "two-car budget" before you even apply for the second loan. Live by this hypothetical budget for a few months, putting aside the "extra" car payment into savings. This will not only test your readiness but also build a down payment or emergency fund.

Refinancing Options: Smart Moves for Better Terms

If you have an existing car loan with a high interest rate, or if your credit score has significantly improved since you took out your first loan, consider refinancing. Refinancing can lower your monthly payments, reduce the total interest paid over the loan term, or even shorten the loan duration. This frees up cash flow, making it easier to manage a second car loan.

You can also explore refinancing both loans simultaneously if your financial standing allows, potentially consolidating them or securing better terms on both. Always compare offers from multiple lenders to find the best deal.

Down Payments: Leverage Your Capital

As mentioned earlier, a substantial down payment on the second vehicle is highly recommended. It reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay. Furthermore, it helps avoid negative equity, especially with a depreciating asset.

Even a small down payment can make a difference. It signals financial responsibility to lenders and can unlock better interest rates, ultimately saving you money over the life of the loan.

Understanding Interest Rates: Every Percentage Point Counts

Interest rates can significantly impact the total cost of your loans. Even a seemingly small difference in percentage points can translate into thousands of dollars over the loan term. Always strive for the lowest possible interest rate by maintaining a strong credit score and shopping around.

If you have a higher-interest loan, prioritize paying it down faster or explore refinancing options. The less you pay in interest, the more financial flexibility you retain for other expenses or savings.

Loan Terms: Short vs. Long

The length of your loan term directly affects your monthly payment and the total interest paid. Shorter loan terms mean higher monthly payments but less interest paid overall. Longer loan terms offer lower monthly payments but accumulate more interest over time.

For a second car loan, carefully evaluate what you can comfortably afford without straining your budget. While a longer term might seem appealing due to lower monthly payments, it can lead to paying significantly more in the long run. Balance affordability with the total cost.

Emergency Fund: Your Financial Safety Net

An emergency fund is non-negotiable when managing two car loans. Unexpected expenses, such as a job loss, medical emergency, or major car repair, can quickly derail your ability to make payments. A robust emergency fund (typically 3-6 months of living expenses) provides a crucial buffer.

Based on my experience, neglecting an emergency fund is one of the biggest mistakes people make when taking on significant debt. It can be the difference between weathering a financial storm and defaulting on your loans.

Alternatives to Taking on a Second Car Loan

Before committing to the significant financial burden of two car loans, it’s wise to explore viable alternatives. Sometimes, a different approach can meet your transportation needs without the added debt.

Public Transportation: An Eco-Friendly Option

Depending on your location, robust public transportation systems (buses, trains, subways) can be an excellent alternative for one or both commutes. This not only saves on car payments, insurance, and fuel but also reduces your environmental footprint. Investigate routes and schedules to see if this is a practical option for your specific needs.

Ridesharing and Car-sharing Services: On-Demand Mobility

Services like Uber, Lyft, Zipcar, or Turo offer on-demand transportation without the commitment of ownership. Ridesharing is great for occasional trips, while car-sharing provides access to vehicles for longer periods, even by the hour or day, without the overheads of insurance, maintenance, and parking. This can be a cost-effective solution for those who only need a second car intermittently.

One-Car Household with Carpooling: Maximizing Efficiency

If you live with a partner or housemate, a single-car household with strategic carpooling can be highly effective. Coordinating schedules and sharing rides can significantly reduce the need for a second vehicle. This requires good communication and planning but can lead to substantial savings.

Purchasing a Used Car Outright (or with a Smaller Loan): Reduce Debt

Instead of taking on another large loan for a brand-new vehicle, consider purchasing a reliable used car. If you have savings, buying a used car outright eliminates a monthly payment entirely. If not, a smaller loan for a less expensive used car will be a much lighter financial burden than a second new car loan.

Motorcycle/Scooter: An Economical Commuter

For solo commutes, especially in urban areas, a motorcycle or scooter can be an incredibly fuel-efficient and agile alternative. The upfront cost and ongoing expenses (insurance, fuel) are typically much lower than a second car, making it an attractive option for certain individuals.

Leasing a Second Vehicle: Short-Term Flexibility

While still a financial commitment, leasing a second vehicle can offer more flexibility than buying, especially if your need is temporary or you prefer always driving a newer model. Lease payments are often lower than loan payments, but you won’t own the vehicle at the end of the term. This can be a good option if you only need a second car for a few years.

Making the Decision: A Step-by-Step Guide

The decision to take on a second car loan is a personal one, deeply rooted in your financial situation and lifestyle needs. Here’s a structured approach to help you make the best choice.

1. Assess Your Current Financial Health

Before anything else, conduct a thorough audit of your finances.

- Calculate your current DTI ratio: Include all existing debts (mortgage, first car loan, credit cards, student loans).

- Review your credit report: Check for accuracy and understand your credit score.

- Analyze your cash flow: How much disposable income do you truly have after all essential expenses?

This honest assessment will reveal if you even have the capacity to consider a second loan.

2. Determine Your Actual Need

Distinguish between a "want" and a genuine "need."

- Why do you need a second car? Is it for work, family logistics, or a lifestyle choice?

- Is this need permanent or temporary? A temporary need might be better served by leasing or car-sharing.

- Can any of the alternatives suffice? Seriously explore the options discussed above.

3. Research Loan Options

Don’t jump at the first offer.

- Shop around: Get pre-approvals from multiple lenders (banks, credit unions, online lenders) to compare interest rates and terms.

- Understand all fees: Look beyond the interest rate to application fees, origination fees, and prepayment penalties.

- Consider the type of vehicle: New vs. used will impact loan terms and insurance costs.

4. Calculate Total Costs

It’s not just the monthly payment.

- Factor in insurance: Get quotes for adding a second vehicle to your policy.

- Estimate fuel and maintenance: Account for increased running costs.

- Consider registration and taxes: These will be double for two vehicles.

- Run scenarios: What if interest rates rise? What if fuel prices spike?

5. Consider the Long-Term Impact

Think beyond the immediate future.

- Future financial goals: How will two car loans affect your ability to save for a house, retirement, or children’s education?

- Risk assessment: Are you comfortable with the increased debt burden and the potential for financial strain?

- Lifestyle changes: Will this decision force you to cut back on other activities or luxuries?

6. Seek Professional Advice

If you’re unsure, consult a financial advisor.

- A professional can provide an unbiased assessment of your financial situation.

- They can help you create a comprehensive budget and long-term financial plan.

- They can also offer strategies for debt management and wealth building.

Conclusion: Driving Forward with Confidence

Navigating the landscape of "2 car loans one person" is undoubtedly a journey with its share of twists and turns. While it’s entirely feasible to manage multiple auto loans, it’s a decision that demands meticulous planning, financial discipline, and a deep understanding of your personal circumstances. The ultimate goal isn’t just to qualify for a second loan, but to ensure that this financial commitment enhances your life without compromising your long-term financial stability.

We’ve delved into the critical factors that determine eligibility, explored the common reasons why individuals opt for multiple vehicles, and weighed the significant pros and cons. We’ve also armed you with practical financial strategies and presented valuable alternatives to consider. Remember, responsible financial planning is your most powerful tool. By assessing your needs honestly, budgeting diligently, and exploring all your options, you can drive forward with confidence, making choices that truly align with your financial well-being and lifestyle aspirations.

What are your thoughts or experiences with managing multiple car loans? Share your insights in the comments below – your perspective could help others on their journey!

for more tips on strengthening your financial foundation.

to master your finances before taking on new debt.