Unlocking the Road Ahead: Your Definitive Guide to Navy Credit Union Car Loan Rates

Unlocking the Road Ahead: Your Definitive Guide to Navy Credit Union Car Loan Rates Carloan.Guidemechanic.com

Navigating the world of auto financing can often feel like a complex journey, filled with twists, turns, and sometimes, unexpected detours. But what if there was a path offering competitive rates, personalized service, and a deep understanding of your unique financial landscape? For service members, veterans, and their families, Navy Credit Unions present just such an opportunity. Specifically, understanding Navy Credit Union car loan rates can be a game-changer when you’re looking to finance your next vehicle.

This isn’t just another article scratching the surface; it’s a deep dive into everything you need to know to secure the best possible car loan from a Navy Credit Union. We’ll explore what makes these institutions stand out, how to qualify, what influences your rates, and crucial strategies to drive away with a deal that truly benefits you. Our ultimate goal is to empower you with the knowledge to make informed decisions and confidently approach your next car purchase.

Unlocking the Road Ahead: Your Definitive Guide to Navy Credit Union Car Loan Rates

Why Consider a Navy Credit Union for Your Car Loan? More Than Just Rates

When it comes to financing a car, most people automatically think of traditional banks or dealership financing. However, credit unions, especially those serving the military community like Navy Credit Unions (with Navy Federal Credit Union, or NFCU, being the most prominent), operate on a fundamentally different principle. Unlike banks that are for-profit entities, credit unions are not-for-profit financial cooperatives owned by their members. This core difference often translates into significant advantages for borrowers.

Based on my experience in the financial landscape, this member-centric approach means credit unions are frequently able to offer more favorable terms, including lower interest rates, fewer fees, and more flexible lending criteria, especially to their target demographics. They prioritize the financial well-being of their members over maximizing shareholder profits. For those with military ties, this ethos resonates deeply, offering a financial partner who truly understands their unique circumstances and needs.

Understanding Navy Credit Union Car Loan Rates: What Truly Influences Them?

While Navy Credit Unions generally offer competitive rates, it’s a misconception to think there’s a single "Navy Credit Union car loan rate" that applies to everyone. Your individual rate is a finely tuned reflection of several critical factors. Understanding these elements is the first step toward strategically positioning yourself for the best possible deal.

Let’s break down the key determinants:

1. Your Credit Score: The Cornerstone of Your Rate

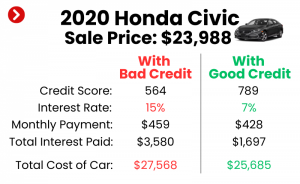

Your credit score is arguably the most significant factor influencing the interest rate you’ll be offered. It’s a three-digit number that summarizes your creditworthiness, telling lenders how reliably you’ve managed debt in the past. Higher scores indicate lower risk, leading to lower interest rates.

Lenders typically use FICO scores, which range from 300 to 850, with scores above 720 generally considered excellent. Even a slight improvement in your credit score can translate into substantial savings over the life of a car loan. If your score isn’t where you want it to be, taking steps to improve it before applying is a powerful strategy.

2. The Loan Term: Short vs. Long

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). While a longer loan term will result in lower monthly payments, it almost always means you’ll pay more in total interest over the life of the loan. This is because the money is borrowed for a longer period, and the interest rate itself might be slightly higher for extended terms due to increased risk for the lender.

Conversely, a shorter loan term means higher monthly payments but significantly less interest paid overall. It’s a delicate balance between affordability and total cost. Pro tips from us: Always calculate the total cost of the loan for different terms, not just the monthly payment, to make an informed decision.

3. The Loan Amount: How Much You Borrow

The total amount you wish to borrow for your car can also play a role in the interest rate. While not as direct as your credit score or loan term, extremely large loans might have slightly different rate considerations. Lenders assess their risk based on the total exposure.

It’s crucial to borrow only what you truly need and can comfortably afford. Over-borrowing can lead to financial strain down the line.

4. Vehicle Type and Age: New vs. Used, Private Party vs. Dealer

The car itself is a significant factor. New cars often qualify for lower interest rates than used cars. This is primarily because new cars typically hold their value better initially and present less risk to the lender in terms of unforeseen mechanical issues. Used cars, especially older models, are seen as higher risk.

Furthermore, how you purchase the car matters. Loans for vehicles bought from a licensed dealership might differ slightly from those for private party sales. Some credit unions may have specific policies or slightly different rates for each scenario.

5. Your Down Payment: The Power of Equity

A larger down payment immediately reduces the amount you need to borrow, which can lead to a lower monthly payment and less interest paid over time. More importantly, a substantial down payment signals to the lender that you are financially stable and committed to the purchase, reducing their risk.

This reduced risk can sometimes translate into a more favorable interest rate. Aiming for at least 10-20% of the vehicle’s purchase price as a down payment is often recommended to secure better terms and build immediate equity in your vehicle.

6. Membership Status and Relationship with the Credit Union

For Navy Credit Unions, your specific membership tier or the length of your relationship with them can sometimes influence the rates you receive. Long-standing members with a history of responsible financial behavior might be eligible for slightly better rates or special offers.

This is part of the "member-owner" benefit; the credit union rewards loyalty. It’s always worth asking if your membership history provides any additional advantages.

7. Market Conditions: The Broader Economic Picture

Beyond your personal financial profile, the general economic environment and prevailing interest rates set by the Federal Reserve also play a role. When the Fed raises or lowers its benchmark rates, it impacts borrowing costs across the board, including auto loans.

While you can’t control market conditions, being aware of them helps you understand why rates might fluctuate over time. Timing your loan application during periods of lower interest rates can be advantageous.

Eligibility for a Navy Credit Union Car Loan: Are You Covered?

Before diving into rates, it’s essential to confirm your eligibility for membership and, subsequently, a car loan. While specific criteria can vary slightly between different Navy Credit Unions, the overarching principle is serving the military community. Navy Federal Credit Union (NFCU) is the largest and most well-known, and its eligibility requirements are a good benchmark.

Generally, you are eligible for membership if you are:

- Active Duty, Reserve, or National Guard: All branches of the U.S. armed forces.

- Veterans: Those who have served and been honorably discharged.

- Department of Defense (DoD) Civilians: Employees of the DoD, contractors, or retirees.

- Family Members: Spouses, parents, grandparents, children, siblings, and even grandchildren of eligible service members or DoD civilians.

Once you establish membership, you then need to meet the credit union’s lending criteria, which includes demonstrating creditworthiness through a good credit score and stable income. Common mistakes to avoid are assuming your military affiliation automatically guarantees a loan, or failing to gather all necessary documentation for income verification.

The Application Process: A Step-by-Step Guide to Your Navy Credit Union Car Loan

Applying for a car loan, especially with a Navy Credit Union, can be a straightforward process if you’re prepared. Here’s a typical step-by-step guide, peppered with our pro tips for a smooth experience:

Step 1: Membership Confirmation

First, ensure you are an eligible member of the Navy Credit Union you wish to borrow from. If you aren’t, the first step is to apply for membership, which typically involves providing proof of your military affiliation or relationship to an eligible member. This usually takes just a few minutes online.

Step 2: Get Pre-Approved (Highly Recommended!)

This is perhaps the most crucial step in the entire car buying process. Pre-approval means the credit union has reviewed your financial information and approved you for a specific loan amount at a particular interest rate, before you even set foot in a dealership. This gives you immense power and confidence.

Pro tips from us: Pre-approval turns you into a cash buyer in the eyes of the dealership. You can focus on negotiating the car price, knowing your financing is already secured. This eliminates the pressure to accept high-interest dealership financing. It also provides a clear budget, preventing you from falling in love with a car outside your financial reach.

Step 3: Gather Your Documents

Whether applying for pre-approval or the final loan, you’ll need several documents. These typically include:

- Proof of Identity: Driver’s license, military ID.

- Proof of Income: Pay stubs, W-2s, tax returns, or direct deposit statements.

- Proof of Residence: Utility bill, lease agreement.

- Vehicle Information: If you’ve already found a car, details like VIN, make, model, and mileage.

Having these ready will significantly speed up the application process.

Step 4: Submit Your Application

Most Navy Credit Unions offer convenient online applications, which you can complete from the comfort of your home. You can also apply in person at a branch or over the phone. Be thorough and honest with all information provided.

Step 5: Await Decision and Funding

Once your application is submitted, the credit union will review it. This can take anywhere from a few minutes for instant approvals to a couple of business days, depending on the complexity of your situation. If approved, you’ll receive the final loan terms.

For funding, the credit union can typically disburse the funds directly to you or the dealership, often through a cashier’s check or electronic transfer. This makes the purchase seamless.

Unpacking Navy Federal Credit Union (NFCU) Car Loan Specifics

As the largest credit union in the U.S., Navy Federal Credit Union is often the first choice for many military members and their families seeking auto loans. Their offerings are generally very competitive, and they frequently provide additional benefits tailored to their member base.

While specific rates are dynamic and depend on market conditions and your individual profile, NFCU consistently aims to offer:

- Competitive APRs: Often lower than traditional banks, especially for members with excellent credit.

- Flexible Terms: A wide range of loan terms, from short 36-month options to extended 84-month terms for both new and used vehicles.

- Pre-approval Program: A robust pre-approval process that empowers buyers.

- Rate Match Program: In some cases, NFCU may match a better rate you’ve received from another lender, demonstrating their commitment to keeping your business.

- Special Programs: They occasionally offer specific promotions or discounts for certain vehicle types or during particular times of the year.

Common mistakes to avoid are solely relying on a rate you see advertised without understanding that it’s often the "best case" scenario for those with top-tier credit. Always get a personalized quote. Another mistake is not asking about all potential fees or charges that might be associated with the loan. Transparency is key.

Maximizing Your Chances for the Best Navy Credit Union Car Loan Rates

Getting a car loan is one thing; getting the best car loan is another. Here’s how to strategically position yourself for the most favorable Navy Credit Union car loan rates:

- Improve Your Credit Score: This is fundamental. Pay bills on time, reduce existing debt, and avoid opening new credit lines just before applying for a car loan. Even a 20-30 point increase can make a difference.

- Save for a Larger Down Payment: As discussed, a larger down payment reduces the loan amount and signals financial stability, potentially leading to a better rate.

- Choose a Shorter Loan Term (If Affordable): While higher monthly payments, shorter terms mean less interest and often slightly lower APRs.

- Shop Around, Even Within Credit Unions: Don’t assume NFCU is your only option. There are other excellent Navy-affiliated credit unions. Compare their rates, terms, and service. This will also give you leverage for NFCU’s rate match program.

- Negotiate the Car Price, Not Just the Loan: Remember, the loan rate applies to the car’s price. A lower car price means you borrow less, which is always a win, regardless of your interest rate. Negotiate the vehicle price first, then discuss financing.

- Consider a Co-Signer (Carefully): If your credit isn’t stellar, a co-signer with excellent credit can help you qualify for a better rate. However, understand that the co-signer is equally responsible for the loan, and their credit will be affected if payments are missed. Use this option judiciously.

Comparing Navy Credit Union Rates with Other Lenders

While Navy Credit Unions often provide excellent rates, it’s always wise to compare them with other lending sources to ensure you’re getting the best deal. This due diligence can save you hundreds, even thousands, over the life of your loan.

Consider these alternatives:

- Traditional Banks: Large banks like Chase, Wells Fargo, or Bank of America offer auto loans. Their rates can sometimes be competitive, especially if you’re an existing customer with a strong banking relationship.

- Other Credit Unions: Don’t limit yourself to just Navy-specific credit unions. Local or employer-based credit unions might also offer attractive rates, though their membership requirements will differ.

- Dealership Financing: While convenient, dealership financing often comes with higher interest rates as they may mark up the rate for profit. However, they sometimes offer special promotional rates (e.g., 0% APR) on new vehicles, which can be unbeatable if you qualify. Always read the fine print.

- Online Lenders: Companies like LightStream or Capital One Auto Navigator offer fully online application processes and can sometimes provide competitive rates, particularly for borrowers with excellent credit.

The importance of getting multiple quotes cannot be overstated. Apply for pre-approval with 2-3 different lenders, including a Navy Credit Union. This gives you concrete offers to compare and leverage. Multiple inquiries for the same type of loan within a short period (typically 14-45 days) are usually counted as a single inquiry on your credit report, minimizing impact.

Beyond the Loan: Post-Approval Considerations

Securing your Navy Credit Union car loan is a significant achievement, but your journey doesn’t end there. Understanding your loan agreement and managing your payments responsibly are crucial for maintaining good financial health.

- Understand Your Loan Agreement: Read every line of your loan contract. Know your interest rate, payment due date, any late fees, prepayment penalties (rare with credit unions, but always check), and how extra payments are applied.

- Payment Options: Most credit unions offer various convenient payment methods, including online payments, automatic deductions from your checking account, and in-person payments. Setting up automatic payments is a great way to ensure you never miss a due date.

- Refinancing Possibilities: If interest rates drop significantly after you’ve taken out your loan, or if your credit score improves substantially, you might be able to refinance your car loan for a lower rate. This can lead to considerable savings over the remaining term. Don’t hesitate to reach out to your credit union or explore other lenders for refinancing options.

- Maintaining Good Credit: Your car loan payments are reported to credit bureaus. Making timely payments consistently will strengthen your credit score, which benefits you for future loans and financial endeavors.

Your Journey to the Perfect Car Loan Starts Here

Securing a car loan doesn’t have to be a stressful ordeal. For those affiliated with the military, Navy Credit Union car loan rates often represent some of the best financing opportunities available. Their member-first philosophy, combined with competitive rates and personalized service, makes them an ideal choice for your next vehicle purchase.

By understanding the factors that influence your rate, strategically preparing your application, and diligently comparing offers, you can confidently navigate the auto loan landscape. Remember, the goal is not just to get a loan, but to get the right loan – one that fits your budget, aligns with your financial goals, and ultimately, puts you in the driver’s seat with peace of mind.

Ready to explore your options? Visit Navy Federal Credit Union’s official auto loan page to see their current offerings and start your pre-approval process today. For more insights on managing your finances, check out our article on Smart Budgeting Strategies for Military Families or learn about Understanding Your Credit Score: A Comprehensive Guide. Your ideal car loan is within reach!