Unlocking the Road Ahead: Your Guide to a Prime Credit Score for the Best Car Loan

Unlocking the Road Ahead: Your Guide to a Prime Credit Score for the Best Car Loan Carloan.Guidemechanic.com

Imagine cruising down the highway in your dream car, knowing you secured an incredible deal. For many, this dream feels out of reach, often overshadowed by the daunting process of car financing. The secret to unlocking those coveted low interest rates and favorable loan terms often lies in one powerful three-digit number: your credit score.

Specifically, achieving a prime credit score for a car loan isn’t just a goal; it’s your golden ticket to significant savings and a smoother buying experience. In this comprehensive guide, we’ll dive deep into what a prime credit score means, why it’s so critical for auto financing, and how you can achieve or maintain it to secure the best possible deal on your next vehicle. Get ready to transform your car buying journey!

Unlocking the Road Ahead: Your Guide to a Prime Credit Score for the Best Car Loan

What Exactly is a "Prime Credit Score" for a Car Loan?

When lenders talk about credit scores, they often categorize them into different tiers. A "prime credit score" sits comfortably in the upper echelon, signaling to lenders that you are a reliable borrower with a strong history of managing debt responsibly.

While the exact cut-offs can vary slightly between lenders and credit bureaus, generally, a prime credit score typically falls within the range of 660 to 719. However, to truly qualify for the best auto loan rates and be considered a "super prime" borrower, you’re usually looking at scores of 720 and above. This top tier grants you access to the most competitive interest rates and the most flexible terms available in the market.

Why does this distinction matter so much for car loans? Lenders assess risk. A higher credit score indicates lower risk. Borrowers with prime or super prime scores are seen as highly likely to repay their loans on time, making them incredibly attractive to lenders who are eager to offer them the most favorable financing options.

The Unbeatable Benefits of a Prime Credit Score for Your Car Loan

Possessing a prime credit score isn’t just about feeling good; it translates directly into tangible financial advantages. These benefits can save you thousands of dollars over the life of your car loan, making your vehicle ownership experience much more affordable and less stressful.

Lower Interest Rates: The Ultimate Savings Generator

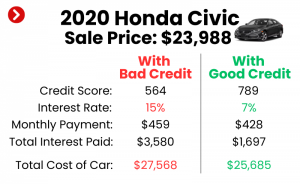

This is arguably the most significant advantage. With a prime credit score, you qualify for significantly lower Annual Percentage Rates (APRs). Even a difference of just a few percentage points can lead to substantial savings over a 5-year or 6-year loan term.

Based on my experience, I’ve seen car buyers with excellent credit pay half the interest rate of someone with average credit, sometimes even less. For instance, on a $30,000 car loan, a 3% APR versus a 7% APR could mean saving over $4,000 in interest alone! This is real money that stays in your pocket, not the lender’s.

Reduced Monthly Payments: Easing Your Budget

Lower interest rates directly translate to lower monthly payments. This can make a substantial difference in your monthly budget, freeing up funds for other necessities or savings. A lower payment can also allow you to afford a slightly more expensive vehicle or keep your overall debt-to-income ratio healthier.

It provides greater financial flexibility. You won’t feel as strained each month trying to meet a high car payment, which contributes to overall financial well-being.

More Favorable Loan Terms: Flexibility and Freedom

Lenders are more willing to offer flexible and beneficial terms to prime borrowers. This could include longer loan repayment periods without a punitive increase in interest rates, smaller down payment requirements, or even less stringent requirements for co-signers.

You might also find more options for early repayment without penalties. This flexibility allows you to tailor the loan to your specific financial situation, rather than being stuck with rigid, less attractive options.

Wider Range of Lenders & Vehicle Choices: More Options, Better Deals

With a prime credit score, virtually every lender, from large banks to local credit unions and even online lenders, will be eager to compete for your business. This competition works in your favor, as you can shop around for the absolute best offer.

Furthermore, lenders are typically more comfortable financing a wider range of vehicles for prime borrowers. This means you have more freedom to choose the car you truly want, rather than being limited by financing restrictions based on your credit tier.

Faster Approval Process: Time is Money

Lenders view prime borrowers as low risk, which often streamlines the approval process. Applications are processed more quickly, and you might receive instant approvals, saving you valuable time and hassle. This efficiency can be particularly beneficial when you’re eager to drive off the lot in your new car.

Pro tips from us: Getting pre-approved with a prime score often means you can walk into a dealership with confidence, knowing exactly what you can afford and what rates you qualify for. This dramatically simplifies negotiations.

Stronger Negotiating Power: Your Credit as Leverage

Your prime credit score is a powerful negotiating tool. When you have a solid pre-approval in hand at a low interest rate, the dealership knows they have to work harder to match or beat it. This gives you leverage not just on the financing terms, but potentially on the vehicle price itself.

They understand that you are an attractive customer who can easily take their business elsewhere. Use this to your advantage to secure the best overall deal, combining a great vehicle price with excellent financing.

How Lenders Evaluate Your Credit for a Car Loan (Beyond Just the Score)

While your credit score is a critical starting point, lenders look at a broader picture to assess your creditworthiness. They want to understand your complete financial health and your capacity to repay the loan.

Your Comprehensive Credit History

Lenders delve deep into your credit report. They examine:

- Payment History: Have you paid your bills on time, every time? This is the most crucial factor, demonstrating your reliability.

- Length of Credit History: How long have you been managing credit? A longer history, especially with positive accounts, is favorable.

- Types of Credit Used: A mix of credit (e.g., credit cards, student loans, mortgage) shows you can handle various debt types.

- Amounts Owed (Credit Utilization): How much of your available credit are you currently using? Lower utilization is better.

- New Credit: How many new accounts have you recently opened? Too many can signal higher risk.

Debt-to-Income (DTI) Ratio

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders prefer a lower DTI, as it indicates you have sufficient income left after paying your existing debts to comfortably handle a new car payment. A common acceptable DTI for many lenders is usually below 43%, though for auto loans, they might look for something lower for prime borrowers.

Common mistakes to avoid are ignoring your DTI. Even with a great credit score, a very high DTI can make lenders hesitant, as it suggests you might be overextended.

Payment-to-Income (PTI) Ratio

Similar to DTI, your PTI ratio specifically looks at how your new car payment will compare to your gross monthly income. Lenders want to see that the car payment won’t consume too large a portion of your income, ensuring it’s affordable. Typically, a car payment that is no more than 10-15% of your gross monthly income is considered healthy.

Employment History

A stable employment history demonstrates a consistent income stream, which reassures lenders about your ability to make payments. They often look for at least two years of consistent employment with the same employer or in the same field. Frequent job changes might be viewed as a potential instability.

Down Payment Amount

While not directly tied to your credit score, a substantial down payment significantly reduces the lender’s risk. It means you’re borrowing less, and you have more equity in the vehicle from day one. For prime borrowers, a large down payment might not be strictly necessary, but it can further sweeten the deal and potentially secure an even lower rate.

Vehicle Choice

The type of vehicle you choose can also subtly influence the loan. Lenders consider the vehicle’s value and how well it holds that value. A new car typically has a higher value and better resale potential than an older, high-mileage used car, which can be seen as less risky collateral.

Steps to Achieve or Maintain a Prime Credit Score for Your Next Car Loan

If you’re aiming for a prime credit score, or if you already have one and want to keep it pristine, these strategies are essential. Building and maintaining excellent credit is a long-term commitment that pays off handsomely.

Check Your Credit Report Regularly

This is your financial report card. You’re entitled to a free copy of your credit report from each of the three major bureaus (Experian, Equifax, and TransUnion) once every 12 months via AnnualCreditReport.com. Review it meticulously for errors, which can unfairly drag down your score.

Pro tips from us: Don’t just check your score; scrutinize the actual report. Look for accounts you don’t recognize, incorrect payment statuses, or outdated information. Promptly dispute any inaccuracies. (For more details, you might want to check out our article on Understanding Your Credit Report and How to Dispute Errors).

Pay Bills On Time, Every Time

Your payment history accounts for the largest portion of your credit score (around 35%). Missing even one payment can significantly damage your score and stay on your report for up to seven years. Set up automatic payments or calendar reminders to ensure you never miss a due date.

Consistency is key here. A long history of on-time payments is the bedrock of a strong credit profile.

Reduce Existing Debt, Especially Revolving Credit

High balances on credit cards can negatively impact your score. Focus on paying down high-interest debt. This not only improves your credit utilization ratio but also frees up more of your income, improving your debt-to-income ratio.

Prioritize paying off credit cards before seeking a major loan. It demonstrates financial prudence to lenders.

Keep Credit Utilization Low

Credit utilization refers to how much of your available credit you’re using. Financial experts recommend keeping your utilization below 30% across all your credit cards. For example, if you have a credit limit of $10,000, try to keep your balance below $3,000.

Lowering this ratio shows that you can manage credit responsibly and aren’t overly reliant on borrowed money. The lower, the better for your score.

Avoid Opening New Credit Accounts Unnecessarily

Each time you apply for new credit, a "hard inquiry" is placed on your credit report. A few hard inquiries within a short period can temporarily ding your score. While applying for a car loan will involve a hard inquiry, try to avoid opening new credit cards or other lines of credit in the months leading up to your car purchase.

This keeps your credit profile stable and signals to lenders that you aren’t desperate for credit.

Dispute Errors on Your Credit Report

As mentioned, errors happen. If you find one, gather documentation and contact the credit bureau and the creditor involved to dispute it. Be persistent. Correcting errors can sometimes boost your score significantly in a relatively short period.

The Federal Trade Commission (FTC) provides excellent guidance on disputing credit report errors on their website, a trusted external source for consumer information.

Be Patient

Building a prime credit score takes time and consistent good financial habits. There are no quick fixes. Focus on these strategies consistently, and your score will gradually improve.

If you’re starting with limited credit history, consider a secured credit card or a credit-builder loan to establish positive payment history. These tools are designed to help you build credit responsibly.

Navigating the Car Loan Process with a Prime Credit Score

Armed with a prime credit score, you’re in an excellent position to tackle the car loan process. Your goal now is to leverage your strong credit to get the absolute best deal.

Get Pre-Approved

Before you even step foot on a dealership lot, get pre-approved for a car loan. Contact your bank, credit union, or online lenders. A pre-approval tells you exactly how much you can borrow, at what interest rate, and for what terms.

Based on my experience, having a pre-approval in hand transforms you from a vulnerable buyer to a powerful negotiator. It gives you a baseline for comparison and shifts the focus from "Can I get approved?" to "What’s the best deal I can get?" (You might find our article on The Ultimate Guide to Car Loan Pre-Approval very helpful here.)

Shop Around for Rates

Do not settle for the first loan offer you receive, especially from the dealership. Compare offers from multiple lenders – banks, credit unions, and reputable online auto loan providers. Rates can vary significantly, even for prime borrowers.

Remember that multiple auto loan inquiries within a short period (typically 14-45 days, depending on the scoring model) are usually treated as a single inquiry, so it won’t harm your score to shop around.

Understand the Loan Terms

Beyond the interest rate, pay close attention to the entire loan agreement. Understand the Annual Percentage Rate (APR), which includes the interest rate plus certain fees. Look at the loan term (e.g., 36, 60, 72 months), any prepayment penalties, and late payment fees.

Ensure you’re comfortable with the monthly payment and the total cost of the loan over its duration. Don’t be pressured into longer terms just to achieve a lower monthly payment if it means paying significantly more interest overall.

Negotiate Like a Pro

Your prime credit score is your biggest asset. When the dealer asks about financing, you can confidently state you’re pre-approved at a low rate. This immediately puts you in a strong position. Use your pre-approval as leverage to see if the dealership can beat it.

Negotiate the price of the car first, then discuss financing. Don’t let them combine the two into one confusing negotiation.

Read the Fine Print

Before signing any documents, read everything carefully. Ensure all the agreed-upon terms, rates, and fees are accurately reflected in the contract. Don’t hesitate to ask questions if something is unclear.

Common mistakes to avoid are rushing through the paperwork or assuming everything is as discussed. Take your time to review every line item.

What If Your Credit Score Isn’t "Prime" Yet? (Alternative Strategies)

If your credit score isn’t quite in the prime category, don’t despair. You still have options, though they might involve slightly higher costs or a bit more effort. The key is to be realistic and strategic.

Consider a Co-signer

A co-signer with excellent credit can significantly improve your chances of approval and help you secure a better interest rate. A co-signer essentially guarantees the loan, taking on equal responsibility for repayment.

Pro tips from us: Ensure your co-signer understands the full implications of their commitment. If you miss payments, it will negatively affect both your credit and theirs. This should only be considered with someone you trust implicitly.

Make a Larger Down Payment

A substantial down payment reduces the amount you need to borrow, which lowers the lender’s risk. This can sometimes compensate for a less-than-prime credit score, making you a more attractive borrower and potentially qualifying you for a better rate.

A larger down payment also reduces your monthly payments and the total interest paid over the life of the loan.

Consider a Less Expensive Vehicle

If your credit isn’t prime, you might need to adjust your expectations regarding the vehicle you can afford. Opting for a more affordable car reduces the loan amount, making it easier to get approved and manage payments.

This also gives you time to improve your credit while still having reliable transportation. You can always upgrade later once your credit score is stronger.

Work on Improving Your Credit First

Sometimes, the best strategy is to delay the purchase and focus intensely on credit repair. If you can wait six months to a year, implement the strategies outlined in Section VI. A significant improvement in your credit score can save you thousands in interest, making the wait well worth it.

Pro tips from us: Focus on consistent, small improvements rather than looking for quick fixes. Address any missed payments, reduce credit card balances, and review your credit report for errors. This foundational work pays dividends for all future financial endeavors.

Debunking Common Myths About Credit Scores and Car Loans

Misinformation can lead to poor financial decisions. Let’s clarify some common misconceptions about credit scores and car loans.

Myth: "Checking my credit hurts my score too much."

Reality: There are two types of credit inquiries: "soft" and "hard." Checking your own credit report (a soft inquiry) has no impact on your score. Hard inquiries, which occur when you apply for new credit, do have a small, temporary effect. However, multiple inquiries for the same type of loan within a short period (typically 14-45 days) are often grouped by credit scoring models and treated as a single inquiry, minimizing their impact. So, shop around for car loans without excessive worry.

Myth: "I need perfect credit to get a car loan."

Reality: While a perfect score (850) is fantastic, it’s not a prerequisite for a car loan. A prime credit score (generally 660-719) or super prime (720+) is more than enough to qualify for excellent rates and terms. Lenders understand that few people have perfect credit.

Myth: "All lenders offer the same rates."

Reality: Absolutely not! This is why shopping around is so crucial. Banks, credit unions, online lenders, and even dealership financing departments all have different criteria and offer varying rates. Your job is to find the one that offers you the best deal.

Myth: "My credit score doesn’t matter if I have a big down payment."

Reality: While a large down payment certainly helps, your credit score still matters significantly. It impacts the interest rate you’ll receive on the remaining loan amount. A strong credit score combined with a substantial down payment is the ideal scenario for securing the absolute lowest rates.

Conclusion: Your Prime Credit Score – The Key to Smart Car Buying

Navigating the world of car loans can feel overwhelming, but understanding the pivotal role of your credit score empowers you to take control. A prime credit score for a car loan isn’t just a number; it’s a testament to your financial responsibility and your most valuable asset when seeking vehicle financing.

By focusing on diligent credit management – paying bills on time, keeping debt low, and regularly monitoring your credit report – you position yourself to unlock lower interest rates, more flexible terms, and substantial savings. Whether you’re aiming to achieve a prime score or maintain your excellent standing, the strategies outlined here are your roadmap to a smarter, more affordable car buying experience. Drive confidently, knowing you’ve secured the best possible deal.