Unlocking the Road Ahead: Your Ultimate Guide to a Car Loan with a 760 Credit Score

Unlocking the Road Ahead: Your Ultimate Guide to a Car Loan with a 760 Credit Score Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is an exciting prospect, and when you’re armed with an impressive 760 credit score, that journey becomes significantly smoother and more rewarding. A 760 credit score isn’t just good; it’s excellent. It places you firmly in the top tier of borrowers, signaling to lenders that you are a highly reliable and low-risk individual. This outstanding credit profile opens doors to the most favorable financing options available, transforming the often-stressful car buying process into a confident and strategic negotiation.

This comprehensive guide is designed to empower you, the savvy borrower with a 760 credit score, to maximize your advantage when securing a car loan. We’ll delve deep into understanding the true power of your credit, navigating the best strategies for loan approval, and avoiding common pitfalls. Our ultimate goal is to ensure you drive away not just with the car of your dreams, but with the best possible terms that save you thousands over the life of your loan. Get ready to leverage your excellent credit and secure an unbeatable 760 credit score car loan.

Unlocking the Road Ahead: Your Ultimate Guide to a Car Loan with a 760 Credit Score

Understanding Your 760 Credit Score and Its Unrivaled Power

A credit score of 760 places you squarely in the "Very Good" to "Excellent" category, depending on the scoring model used. For most lenders, this is a golden ticket. It indicates a history of responsible financial management, including timely payments, low credit utilization, and a healthy mix of credit accounts.

Lenders view a 760 score as a strong indicator of your ability and willingness to repay debt. They see you as a safe bet, and this perception directly translates into tangible benefits for your car loan. This isn’t just a number; it’s a powerful financial asset that commands respect and offers significant leverage.

What Constitutes an Excellent Score?

An excellent credit score, like your 760, is typically built on a foundation of several key factors. These include a long history of on-time payments, which is the most influential component. Maintaining low balances on your credit cards, indicating responsible credit utilization, also plays a crucial role.

Furthermore, a diverse credit mix, such as a combination of credit cards and installment loans, demonstrates your ability to manage different types of debt effectively. The age of your credit accounts also contributes, as older accounts generally show more stability. Your 760 score is a testament to diligently managing these elements over time.

Why a 760 is a Golden Ticket for Car Loans

For car loans specifically, a 760 credit score puts you in an elite group of borrowers who qualify for the absolute best interest rates and terms. Lenders compete for your business because the risk of default is exceptionally low. This competitive environment works entirely in your favor.

Based on my experience in the lending and automotive industries, a 760 score transforms you from a mere applicant into a preferred customer. You’re not just asking for a loan; you’re dictating the terms to a certain extent. This power dynamic is crucial to remember throughout your car buying process.

The Unbeatable Advantages of a 760 Credit Score for Your Car Loan

Possessing a 760 credit score isn’t just about getting approved; it’s about unlocking a suite of advantages that can save you a substantial amount of money and provide unparalleled flexibility. These benefits are the direct result of your strong financial standing.

Let’s explore the specific ways your excellent credit score empowers your car loan journey. Each of these advantages contributes to a more affordable and less stressful car buying experience.

Significantly Reduced Interest Rates

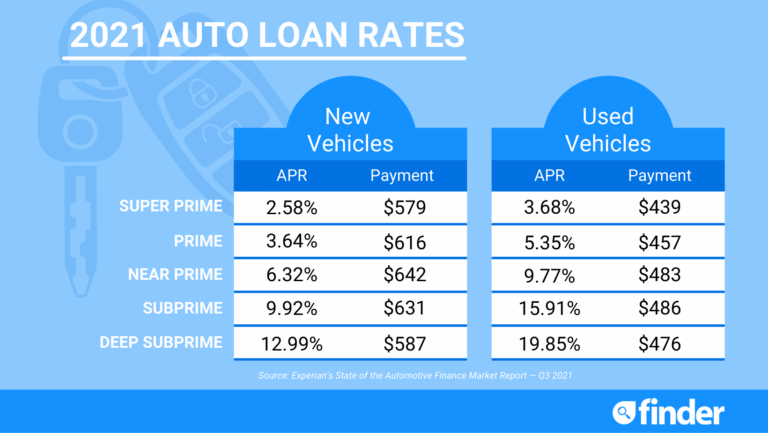

This is perhaps the most significant advantage of an excellent credit score. With a 760, you’ll qualify for the lowest interest rates offered by lenders. Even a seemingly small difference in APR (Annual Percentage Rate) can save you thousands of dollars over a 5- or 6-year loan term.

Consider this: on a $30,000 car loan over 60 months, the difference between a 7% APR (for good credit) and a 3% APR (for excellent credit) can amount to over $3,500 in total interest paid. Your 760 credit score directly puts that money back in your pocket. This substantial saving is a testament to your diligent financial habits.

Flexible Loan Terms

Lenders are more willing to offer flexible loan terms to borrowers with excellent credit. This means you might have the option for a shorter loan term, which saves you interest, or a longer term, which lowers your monthly payments, without incurring a significant rate penalty. The choice is yours, tailored to your personal financial strategy.

This flexibility allows you to structure the loan in a way that best suits your budget and long-term financial goals. You’re not boxed into standard offerings; instead, you have the power to customize. This freedom is a direct benefit of your outstanding creditworthiness.

Wider Lender Choices

A 760 credit score opens the doors to virtually every lender in the market. You’re not limited to subprime lenders or those specializing in higher-risk borrowers. Instead, you can approach traditional banks, credit unions, online lenders, and even manufacturer financing programs with confidence.

This broad selection allows you to shop around and compare offers extensively, ensuring you find the absolute best deal. The more options you have, the greater your chances of securing the most favorable terms for your 760 credit score car loan.

Enhanced Negotiating Power

Your excellent credit score gives you significant leverage at the dealership. When you arrive with a pre-approved loan offer at a low interest rate, the dealer knows they need to match or beat it to earn your business. This dramatically shifts the power dynamic in your favor.

You’re not just negotiating the car’s price; you’re also negotiating the financing. Dealers often make profits on financing, but your pre-approval limits their ability to inflate rates. This positions you as a formidable negotiator, ready to secure the best overall deal.

Lower Down Payment or No Down Payment Options

While a down payment is always a smart financial move to reduce the total amount financed and lower monthly payments, an excellent credit score can give you more flexibility. Lenders might be willing to approve you for a loan with a very low or even zero down payment.

This option can be beneficial if you prefer to keep your cash reserves for other investments or emergencies. However, we generally recommend putting down as much as you comfortably can to reduce your loan amount and the total interest paid.

Preparing for Your Car Loan Journey with a 760 Credit Score

Even with an excellent 760 credit score, preparation is key to a smooth and successful car loan experience. Don’t assume your score alone will guarantee the best outcome. Strategic planning will ensure you fully capitalize on your credit advantage.

By taking these preparatory steps, you’ll approach the car buying process with confidence and clarity. This groundwork will solidify your position as a well-informed and powerful buyer.

Knowing Your Exact Score and Report

Before you even think about stepping into a dealership or applying for a loan, check your credit report and score. While you know it’s around 760, it’s crucial to see the exact number and review your report for any inaccuracies. Even a minor error could slightly impact an offer.

You can obtain your credit report for free once a year from each of the three major credit bureaus (Experian, Equifax, TransUnion) at AnnualCreditReport.com. For official credit reporting information, you can visit the Consumer Financial Protection Bureau’s website. Reviewing your report allows you to dispute any errors and ensure everything is accurate before a lender pulls your credit.

Budgeting Wisely: Beyond the Monthly Payment

While a low monthly payment is attractive, a smart budget considers the total cost of car ownership. Factor in insurance, fuel, maintenance, registration fees, and potential depreciation. Your 760 credit score car loan will likely have a great interest rate, but the overall cost needs to fit your financial picture.

Pro tips from us: Create a realistic monthly budget that accounts for all these expenses, not just the loan payment. This holistic view prevents unexpected financial strain down the road and ensures your new car is a joy, not a burden.

Researching Vehicles and Their Value

Before you commit to a loan, commit to a car. Research different makes and models that fit your needs and budget. Understand their market value, common issues, and depreciation rates. This knowledge helps you negotiate the purchase price effectively, which directly impacts your loan amount.

Whether you’re looking at new or used vehicles, sites like Kelley Blue Book (KBB) or Edmunds can provide valuable pricing information. This research empowers you to make an informed decision and ensures you’re getting a fair price for the vehicle itself.

Gathering Essential Documents

Lenders will require certain documents to process your loan application. Having these ready in advance will streamline the approval process. This usually includes proof of identity (driver’s license), proof of income (pay stubs, tax returns), proof of residence (utility bill), and potentially proof of insurance.

Organizing these documents beforehand demonstrates your preparedness and professionalism. It helps the lender process your 760 credit score car loan application quickly and efficiently, moving you closer to driving your new vehicle.

The Strategic Path to Securing Your 760 Credit Score Car Loan

With your excellent credit and thorough preparation, it’s time to strategically approach securing your car loan. This process involves more than just filling out an application; it’s about leveraging your position to get the best possible terms.

Following these steps will ensure you not only get approved but also walk away with an unbeatable deal. Your 760 credit score is your most powerful tool in this journey.

Step 1: Get Pre-Approved (Crucial!)

This is the single most important step for anyone, especially those with excellent credit. Pre-approval means a lender has conditionally agreed to lend you a specific amount at a specific interest rate before you even set foot in a dealership. It gives you concrete numbers to work with.

Pro tip from us: Always get pre-approved from at least one, preferably two or three, direct lenders (banks, credit unions, online lenders). This gives you a solid benchmark interest rate and empowers you to negotiate the car’s price separately from the financing. This way, you can focus on getting the best deal on the vehicle itself.

Step 2: Compare Loan Offers

Do not settle for the first loan offer you receive, even if it seems good. With a 760 credit score, multiple lenders will want your business. Compare interest rates (APR), loan terms, and any associated fees across different institutions.

Look at local credit unions, which often offer highly competitive rates, as well as national banks and reputable online lenders. Comparing these offers ensures you’re truly getting the most competitive rate available for your excellent credit. This is where your pre-approvals become invaluable.

Step 3: Understand the Loan Terms Beyond APR

While APR is critical, delve into the fine print of each loan offer. Understand the total amount you’ll pay over the life of the loan, including all interest and fees. Clarify if there are any prepayment penalties should you decide to pay off the loan early.

Common mistakes to avoid are focusing solely on the monthly payment without understanding the total cost or the loan term. A lower monthly payment over a longer term might mean paying significantly more interest overall. Ensure the terms align with your financial comfort and goals.

Step 4: Negotiate with Confidence

Armed with your pre-approval and comparative loan offers, you are in a powerful negotiating position at the dealership. Approach the car buying process as two separate negotiations: the price of the car and the financing terms.

First, negotiate the vehicle’s purchase price as if you were paying cash. Once you’ve agreed on a price, then present your pre-approved financing. The dealer may try to beat your rate, and that’s fine – but you have a strong benchmark. Never let them combine the car price and financing negotiations into one confusing bundle.

Common Mistakes to Avoid with a 760 Credit Score Car Loan

Even with an excellent credit score, certain missteps can diminish your advantage. Being aware of these common pitfalls will help you maintain control and secure the best possible deal. Your 760 score is a powerful asset, but it needs to be wielded wisely.

Avoiding these mistakes ensures you fully leverage your creditworthiness. Don’t let excitement or a lack of attention to detail undermine your excellent financial standing.

Not Getting Pre-Approved

As emphasized, skipping pre-approval is a significant error. Without it, you walk into the dealership blind, without a clear idea of the best interest rate you qualify for. This leaves you vulnerable to potentially higher rates offered by dealer financing.

A pre-approval acts as your financial shield and sword, providing clarity and negotiation power. It’s the cornerstone of a smart car loan strategy for excellent credit holders.

Focusing Only on Monthly Payment

While a manageable monthly payment is important, fixating solely on it can lead to longer loan terms and significantly more interest paid over time. Dealers often use this tactic to make more expensive vehicles seem affordable.

Always prioritize the total cost of the loan and the interest rate. A slightly higher monthly payment for a shorter term can save you thousands in the long run.

Skipping the Fine Print

Loan agreements can be lengthy and filled with jargon, but it’s crucial to read every line. Look for hidden fees, prepayment penalties, or unfavorable clauses. If something is unclear, ask for clarification before signing.

Your 760 credit score earned you the best rates, so ensure no obscure terms negate that advantage. Don’t let excitement override your due diligence.

Letting the Dealer Run Multiple Hard Inquiries

When a dealer "shops around" your credit for you, they might submit your application to multiple lenders. Each of these can result in a hard inquiry on your credit report. While multiple inquiries for the same type of loan within a short period (typically 14-45 days) are often grouped as one for scoring purposes, excessive inquiries can still have a minor, temporary impact.

It’s better to control who pulls your credit by securing your own pre-approvals. Use your pre-approvals, then let the dealer try to beat that specific offer if you choose to consider their financing.

Impulse Buying

Even with a 760 credit score, an impulse purchase can lead to buyer’s remorse. Take your time, do your research, and stick to your budget. Don’t let high-pressure sales tactics rush you into a decision you haven’t thoroughly considered.

Your excellent credit gives you the luxury of time and choice. Use it wisely to make a well-informed decision that you’ll be happy with for years to come.

Dealer vs. Direct Lender: Which is Best for Your 760 Credit Score?

When it comes to financing your car, you essentially have two main avenues: securing a loan directly from a bank, credit union, or online lender (direct lender), or using the financing options provided by the dealership. With a 760 credit score, you’re in an excellent position to leverage both.

Understanding the pros and cons of each will help you make the most strategic choice for your specific situation. Your goal is to find the best possible rate, regardless of the source.

Direct Lenders (Banks, Credit Unions, Online Lenders)

Pros:

- Transparency: Direct lenders often offer very straightforward rates and terms, making comparisons easier.

- Pre-approval Power: Getting pre-approved through a direct lender gives you immense leverage at the dealership, allowing you to separate the car price negotiation from the financing.

- Focus on Rates: Their primary business is lending, so they are often highly competitive on interest rates. Credit unions, in particular, are known for excellent rates.

Cons:

- Less Convenient: Requires you to do the legwork of applying to multiple institutions.

- Limited Flexibility: Once approved, your terms are usually fixed, though some offer slight adjustments.

Dealership Financing

Pros:

- Convenience: You can often handle everything – car purchase and financing – in one place.

- Special Programs: Dealers may have access to manufacturer-backed incentives, low APR offers, or special lease deals that direct lenders don’t.

- Potential to Beat Rates: If you arrive with a strong pre-approval, the dealer’s finance department might work to beat your rate to keep the financing business in-house.

Cons:

- Less Transparent: Dealer financing can sometimes be less transparent, with a focus on monthly payments rather than the total cost or APR.

- Potential for Markups: Dealers can mark up the interest rate they receive from their lending partners, keeping the difference as profit.

- Multiple Inquiries: As mentioned, they might submit your application to many lenders, leading to multiple hard inquiries if not managed carefully.

Leveraging Both with Your 760 Score

The smartest strategy for someone with a 760 credit score is to pursue pre-approval from at least one or two direct lenders first. This establishes your baseline best rate. Then, when you’re at the dealership, negotiate the car price. Once that’s settled, you can present your pre-approval and see if the dealership can beat it.

This approach puts you in the driver’s seat, allowing you to capitalize on the best aspects of both financing avenues. You get the transparency and competitive rates of direct lenders, combined with the potential for dealer-specific incentives.

What to Do After Your 760 Credit Score Car Loan is Approved

Congratulations! You’ve successfully navigated the car loan process with your excellent 760 credit score and secured fantastic terms. However, the journey doesn’t end when you drive off the lot. Responsible management of your new loan is crucial for maintaining your excellent credit and ensuring long-term financial health.

These post-approval steps are simple but vital. They solidify your financial discipline and ensure your excellent credit continues to work for you.

Make Payments On Time, Every Time

This might seem obvious, but it’s the bedrock of good credit. Set up automatic payments or calendar reminders to ensure your car loan payments are made punctually each month. Late payments, even one, can negatively impact your credit score and incur fees.

Maintaining a perfect payment history on your new car loan will further strengthen your already impressive 760 credit score. It’s a simple habit that yields significant financial rewards.

Consider Paying More Than the Minimum (If Possible)

If your budget allows, paying a little extra each month towards your principal can significantly reduce the total interest you pay and shorten your loan term. Even an extra $25-$50 per month can make a substantial difference over the life of the loan.

With your low interest rate from your 760 credit score car loan, this strategy becomes even more impactful. It’s an excellent way to accelerate your path to debt freedom.

Monitor Your Credit Report

Periodically check your credit report to ensure your loan is being reported correctly. Look for accurate payment history and outstanding balance. Catching and correcting any errors early can prevent future headaches.

This vigilance ensures your credit file accurately reflects your responsible borrowing habits. It’s a proactive measure to protect your hard-earned 760 credit score.

Maintain Good Insurance Coverage

Always ensure your vehicle has adequate insurance coverage, as required by your lender and state law. Lenders typically require full coverage (collision and comprehensive) until the loan is paid off. Maintaining proper insurance protects your investment and fulfills your loan obligations.

This is a non-negotiable aspect of car ownership, especially when you have an outstanding loan. It safeguards both your asset and your financial stability.

Conclusion: Drive Away Confidently with Your 760 Credit Score Car Loan

Securing a car loan with a 760 credit score is not just about getting approved; it’s about leveraging your financial excellence to achieve the most advantageous terms possible. Your excellent credit is a powerful tool that opens doors to lower interest rates, flexible terms, and superior negotiating power, ultimately saving you thousands of dollars over the life of your loan.

By understanding the true value of your score, meticulously preparing, strategically comparing offers, and avoiding common pitfalls, you can transform the car buying experience from daunting to incredibly rewarding. Remember to get pre-approved, compare offers from various lenders, and read all the fine print.

You’ve worked hard to build your exceptional credit, and now it’s time to let it work hard for you. Drive away with confidence, knowing you’ve secured an unbeatable 760 credit score car loan that perfectly aligns with your financial goals. Your journey to a new vehicle, backed by smart financing, starts now.