Unlocking the Road Ahead: Your Ultimate Guide to Affinity Plus Car Loan Rates

Unlocking the Road Ahead: Your Ultimate Guide to Affinity Plus Car Loan Rates Carloan.Guidemechanic.com

The dream of a new car, or even a reliable pre-owned vehicle, often comes with one significant question: how will I finance it? Navigating the world of car loans can feel daunting, with countless terms, rates, and lenders vying for your attention. But what if there was a financial partner focused on your well-being rather than just profits?

Enter Affinity Plus Federal Credit Union. As a member-owned, not-for-profit financial institution, Affinity Plus often stands out for its competitive Affinity Plus Car Loan Rates and a commitment to its members. This comprehensive guide will peel back the layers of auto financing with Affinity Plus, helping you understand everything from how rates are determined to securing the best possible deal. Our goal is to equip you with the knowledge to drive away with confidence, knowing you’ve made a smart financial decision.

Unlocking the Road Ahead: Your Ultimate Guide to Affinity Plus Car Loan Rates

Understanding Affinity Plus Federal Credit Union: More Than Just a Lender

Before we dive into the specifics of car loan rates, it’s crucial to understand who Affinity Plus is and what sets them apart. This isn’t just another bank; it’s a credit union.

What is a Credit Union?

Unlike traditional banks that are typically for-profit entities beholden to shareholders, credit unions are financial cooperatives owned by their members. This fundamental difference means their primary mission is to serve their members, not to maximize profits. Any earnings are usually reinvested into the credit union through lower loan rates, higher savings rates, and reduced fees.

Affinity Plus Federal Credit Union, specifically, is one of the largest credit unions in Minnesota. They have a long-standing history of providing personalized service and a wide array of financial products designed to benefit their member community. Their philosophy revolves around helping members achieve financial success, and this ethos extends directly to their loan offerings.

Becoming an Affinity Plus Member

To access the attractive Affinity Plus auto loans and their competitive rates, you first need to become a member. Membership eligibility typically includes living, working, worshipping, or attending school in certain counties in Minnesota, or being related to an existing member. The process is usually straightforward and involves opening a savings account with a small minimum deposit. This membership is your gateway to a world of member-centric financial services.

The Foundation of Car Loans: Key Terms You Need to Know

Before you even look at a car, understanding the basic language of auto financing is paramount. These terms directly impact your monthly payments and the total cost of your vehicle.

APR vs. Interest Rate: The Crucial Distinction

While often used interchangeably, the Annual Percentage Rate (APR) and the interest rate are distinct. The interest rate is simply the cost of borrowing money, expressed as a percentage of the principal. The APR, however, represents the total cost of borrowing, including not only the interest rate but also any additional fees or charges associated with the loan, such as origination fees.

Based on my experience, focusing solely on the interest rate can be misleading. Always compare APRs when evaluating loan offers, as it provides a more accurate picture of the true cost of the loan over its term. A lower interest rate might look appealing, but a higher APR due to hidden fees could make it a more expensive option overall.

Loan Term: How Long Will You Be Paying?

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). A longer loan term will result in lower monthly payments, which can be tempting for budget management. However, a longer term also means you’ll pay more in total interest over the life of the loan.

Conversely, a shorter loan term will lead to higher monthly payments but significantly reduce the total interest paid. Finding the right balance between affordability and minimizing overall cost is key. Pro tips from us: always calculate the total cost of the loan for different terms, not just the monthly payment.

The Power of a Down Payment

A down payment is the initial amount of money you pay upfront towards the purchase price of the vehicle. It directly reduces the amount you need to borrow, which can lead to lower monthly payments and less interest paid over the loan’s term. A larger down payment also signals less risk to lenders, potentially qualifying you for better Affinity Plus Car Loan Rates.

Common mistakes to avoid are neglecting to save for a down payment or putting down too little. Even a small down payment can make a significant difference. Aim for at least 10-20% of the vehicle’s price if possible, especially for new cars, to build equity faster and reduce your financial burden.

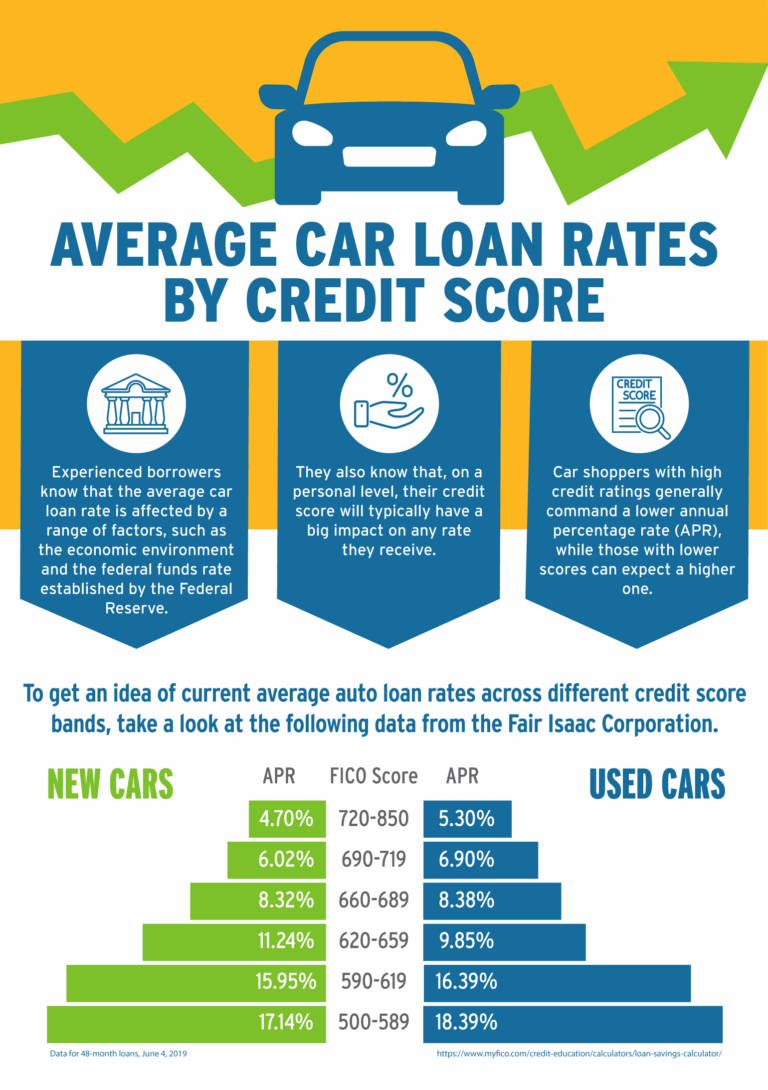

Your Credit Score: The Golden Ticket

Your credit score is arguably the single most important factor influencing the car loan rates you’ll be offered. It’s a three-digit number that reflects your creditworthiness based on your payment history, amounts owed, length of credit history, new credit, and credit mix. A higher credit score (generally above 700) indicates to lenders that you are a reliable borrower, leading to the most favorable interest rates.

Conversely, a lower credit score will result in higher interest rates, as lenders perceive a greater risk of default. Before applying for any car loan, it is always a smart move to check your credit score and report. For a deeper dive into improving your credit health, you might find our guide on incredibly helpful.

Diving Deep into Affinity Plus Car Loan Rates: What Influences Your Offer?

Now that we understand the basics, let’s focus specifically on how Affinity Plus determines the car loan rates they offer to their members. It’s a nuanced process, but being aware of the factors at play can help you position yourself for the best possible outcome.

Your Credit Score Tiers and Their Impact

As mentioned, your credit score is king. Affinity Plus, like most lenders, categorizes applicants into different credit tiers. Each tier corresponds to a specific range of credit scores, and each range has a corresponding set of rates.

- Excellent Credit (e.g., 750+): Members in this tier will typically qualify for the lowest advertised Affinity Plus Car Loan Rates. They are considered the least risky borrowers.

- Good Credit (e.g., 680-749): Still very favorable, but rates might be slightly higher than for excellent credit.

- Average Credit (e.g., 620-679): Rates will be notably higher, reflecting a moderate level of risk.

- Subprime Credit (e.g., below 620): While Affinity Plus strives to help all members, rates for subprime credit will be significantly higher due to the increased perceived risk.

Based on my experience, consistently making payments on time and keeping credit utilization low are the best ways to improve your credit score over time. This directly translates into savings on interest for major purchases like a car.

The Influence of Loan Term

We touched on loan term previously, but it bears repeating its direct impact on your rate with Affinity Plus. Generally, shorter loan terms (e.g., 36 or 48 months) come with lower interest rates. This is because the lender’s risk is reduced when the money is repaid quicker.

Longer terms (e.g., 72 or 84 months) will almost always carry a higher interest rate. While the monthly payment will be lower, the overall cost of the loan increases significantly. Affinity Plus provides a range of terms, allowing you to choose what fits your budget, but be mindful of the rate implications.

Vehicle Type and Age: New vs. Used

The type and age of the vehicle you’re financing also play a role. New cars generally qualify for slightly lower rates than used cars. This is primarily because new cars typically hold their value better in the initial years, offering more collateral security for the lender.

Used car loan rates from Affinity Plus can vary depending on the vehicle’s age, mileage, and condition. Older vehicles with high mileage might be seen as a higher risk due to potential mechanical issues, leading to slightly elevated rates. Always ensure the used car you’re considering is in good shape to secure a better rate and avoid future expenses.

Your Down Payment Size

As discussed, a larger down payment reduces the amount you need to borrow and lessens the lender’s risk. This can positively influence the Affinity Plus Car Loan Rates you receive. A substantial down payment demonstrates financial stability and commitment, making you a more attractive borrower.

Relationship with Affinity Plus: Member Benefits

One of the unique advantages of a credit union like Affinity Plus is that your existing relationship can sometimes unlock additional benefits. Members with multiple accounts (checking, savings, other loans) or those who set up automatic payments from an Affinity Plus account might qualify for slight rate discounts. These small percentage points can add up to significant savings over the life of the loan.

Types of Affinity Plus Car Loans

Affinity Plus offers a variety of auto loan options to suit different needs:

- New Car Loans: For brand-new vehicles straight from the dealership.

- Used Car Loans: For pre-owned vehicles, with rates often adjusted based on age and mileage.

- Refinance Car Loans: If you have an existing car loan with another lender and want to potentially lower your interest rate, reduce your monthly payment, or change your loan term, Affinity Plus offers refinancing options. Many members find significant savings by refinancing their high-interest auto loans through their credit union.

- Auto Loan Pre-approval: This is a crucial step for many. Getting pre-approved means Affinity Plus has already assessed your creditworthiness and committed to lending you a specific amount at a particular rate, subject to final vehicle verification. This empowers you to shop for a car with the confidence of a cash buyer, knowing exactly what you can afford and avoiding high-pressure sales tactics at dealerships.

Pro Tips for Securing the Best Affinity Plus Car Loan Rates

Getting a car loan is a significant financial decision. Here are some expert tips to help you secure the most favorable terms with Affinity Plus.

- Boost Your Credit Score: This is non-negotiable. Pay all your bills on time, reduce existing debt, and avoid opening new credit accounts before applying for a car loan. Even a few points can make a difference in your rate tier.

- Save for a Larger Down Payment: The more you put down, the less you borrow, and the better your chances of securing a lower interest rate. Aim for at least 10%, but 20% is ideal for new cars.

- Consider a Shorter Loan Term if Affordable: While it means higher monthly payments, a shorter term almost always results in a lower interest rate and significantly less total interest paid over the loan’s life. If your budget allows, this is a smart financial move.

- Leverage Your Membership: If you’re an existing Affinity Plus member, inquire about any loyalty discounts or benefits for setting up automatic payments. Don’t be afraid to ask!

- Get Pre-approved: Always get pre-approved before you step onto the dealership lot. This gives you a clear budget and negotiating power. You’ll know your maximum loan amount and interest rate from Affinity Plus, which you can then compare against any dealership financing offers.

The Application Process: Your Step-by-Step Guide

Applying for an Affinity Plus car loan is a straightforward process, but being prepared can make it even smoother.

Before You Apply:

- Check Your Credit Score and Report: Obtain a free copy of your credit report from AnnualCreditReport.com and review it for any errors. Dispute anything inaccurate. This is your chance to correct issues that could hurt your rate.

- Gather Necessary Documents: Have your identification (driver’s license), proof of income (pay stubs, tax returns), proof of residency (utility bill), and potentially information about the vehicle you intend to purchase (if you’ve already found one) readily available.

- Determine Your Budget: Don’t just think about the monthly car payment. Factor in insurance, fuel, maintenance, and potential registration fees. This holistic approach ensures you can comfortably afford the total cost of car ownership.

The Application Steps:

Affinity Plus offers several convenient ways to apply:

- Online: Their website typically has an intuitive online application portal. This is often the quickest way to start the process.

- In-Person: Visit one of their branch locations to speak with a loan officer. This can be beneficial if you have complex questions or prefer face-to-face interaction.

- By Phone: You can also apply over the phone with the assistance of a member service representative.

Once you submit your application, Affinity Plus will review your financial information and credit history. You’ll typically receive a decision relatively quickly, often within one business day for pre-approvals.

Common Mistakes to Avoid:

- Applying to Too Many Lenders: While it’s good to shop around, applying for multiple loans in a short period can temporarily ding your credit score. Focus on a few strong contenders like Affinity Plus.

- Not Checking Your Credit Report First: Errors on your report can unfairly impact your rate. Catching them early is crucial.

- Underestimating Hidden Costs: Remember to budget for insurance, registration, and potential extended warranties, which aren’t part of the loan itself but are critical to car ownership.

- Accepting the First Offer: Even with pre-approval, always compare the final offer against any dealership financing. Sometimes, a dealer might have special manufacturer incentives.

Beyond the Rate: Other Factors to Consider with Affinity Plus

While Affinity Plus Car Loan Rates are a primary concern, the overall loan experience and the features of the loan itself are equally important.

Fees and Charges

Credit unions are generally known for lower fees compared to traditional banks. However, it’s always wise to ask about any potential fees, such as application fees (rare for auto loans), late payment fees, or early payoff penalties. Pro tips from us: Affinity Plus, like most credit unions, typically does not charge prepayment penalties, meaning you can pay off your loan early without extra cost, saving you interest.

Exceptional Customer Service

As a member-owned institution, Affinity Plus prides itself on personalized customer service. This can be a huge advantage when you have questions about your loan, need to adjust payment methods, or encounter unexpected financial challenges. Their focus is on building long-term relationships, not just transactional business.

Flexibility and Payment Options

Affinity Plus usually offers flexible payment options, including setting up automatic payments, online payments, or payments by phone. Understanding these options can help you manage your loan efficiently and avoid late fees. Their commitment to members means they are often more willing to work with you during difficult times than a traditional bank might be.

Making an Informed Decision and Comparison

Even if you’re leaning towards Affinity Plus, it’s always a good practice to compare offers.

- Get Quotes from Multiple Lenders: Gather at least two to three loan offers from different financial institutions, including Affinity Plus, local banks, and perhaps online lenders. This will give you a benchmark for what constitutes a good rate for your specific credit profile.

- Compare APR, Terms, and Overall Costs: Don’t just look at the monthly payment. Calculate the total cost of each loan over its entire term, including interest and any fees. The lowest monthly payment isn’t always the cheapest option in the long run.

- Don’t Just Focus on the Monthly Payment: While crucial for budgeting, fixating solely on the lowest monthly payment can lead to longer loan terms and significantly more interest paid over time. Balance affordability with the total cost of borrowing.

For unbiased information and consumer protection tips on auto loans, the Consumer Financial Protection Bureau (CFPB) offers excellent resources . If you’re weighing your options between new and used vehicles, our article on offers valuable insights.

Driving Away with Confidence: Your Next Steps

Securing a car loan doesn’t have to be a source of stress. By understanding the factors that influence Affinity Plus Car Loan Rates and preparing yourself thoroughly, you can approach the process with confidence and clarity. Affinity Plus, with its member-first philosophy and competitive offerings, stands out as a strong contender for your auto financing needs.

Remember, preparation is key: know your credit score, understand your budget, and get pre-approved. By doing so, you’re not just getting a loan; you’re making an informed financial decision that puts you in the driver’s seat of your future. Start your journey today by exploring Affinity Plus’s auto loan options and experience the difference a credit union can make.