Unlocking the Road Ahead: Your Ultimate Guide to Car Loans with Bad Credit and No Money Down

Unlocking the Road Ahead: Your Ultimate Guide to Car Loans with Bad Credit and No Money Down Carloan.Guidemechanic.com

The dream of owning a car is a universal one, representing freedom, convenience, and opportunity. Yet, for many, this dream can feel out of reach, especially when faced with the dual challenges of bad credit and the inability to provide a down payment. The phrase "car loans with bad credit and no money down" often conjures images of impossible hurdles and endless rejection.

But what if we told you it’s not always an impossible feat? While undeniably challenging, securing an auto loan under these circumstances is a journey many have successfully navigated. As an expert in automotive finance and an experienced content writer, I’m here to shed light on the realities, strategies, and essential considerations for those looking to buy a car without perfect credit or a hefty sum for a down payment. This comprehensive guide will equip you with the knowledge and confidence to approach the process strategically, turning a daunting task into an achievable goal.

Unlocking the Road Ahead: Your Ultimate Guide to Car Loans with Bad Credit and No Money Down

Understanding the Landscape: Why Bad Credit and No Money Down is a Tough Combo

Before diving into solutions, it’s crucial to understand why this specific financial scenario presents such a significant challenge to lenders. When you apply for a loan, lenders assess risk. They want to be confident that you will repay the money they lend you.

The Impact of Bad Credit

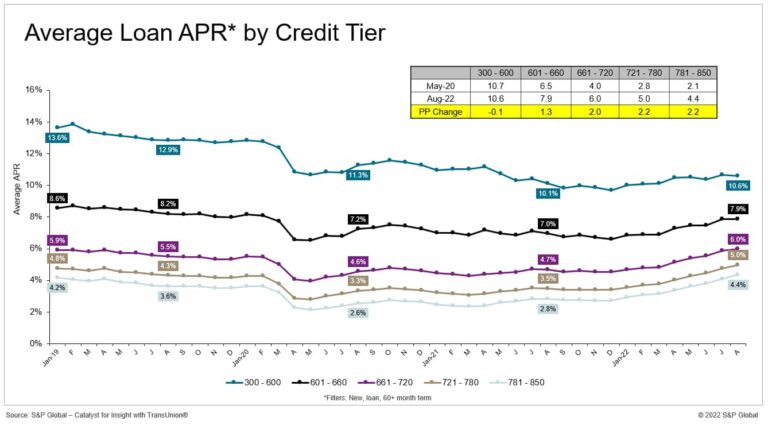

Your credit score is a numerical representation of your creditworthiness. It tells lenders how responsibly you’ve managed debt in the past. A "bad credit" score, typically below 620 on the FICO scale, signals a higher risk. This could be due to late payments, defaults, bankruptcies, or a high debt-to-income ratio.

From a lender’s perspective, a low score suggests a higher probability of future missed payments or even default. This increased risk often translates into higher interest rates, stricter terms, or outright loan denial, making bad credit car loans inherently more difficult to obtain.

The "No Money Down" Hurdle

A down payment serves multiple purposes for both the borrower and the lender. For the borrower, it reduces the total amount financed, lowering monthly payments and the overall interest paid. For the lender, it acts as a cushion.

If a borrower defaults, the down payment reduces the lender’s potential loss, as the car’s value typically depreciates rapidly after purchase. Without a down payment, the loan amount is 100% of the vehicle’s price, immediately placing the loan "upside down" (meaning you owe more than the car is worth). This makes no money down car financing significantly riskier for lenders, especially when combined with bad credit.

Is It Truly Possible? Setting Realistic Expectations

The short answer is yes, securing a car loan with bad credit and no money down can be possible. However, it’s vital to temper expectations. You won’t walk into just any dealership and get a prime loan rate with minimal effort. This path often comes with specific trade-offs and requires a strategic approach.

Dispelling the "Guaranteed Approval" Myth

Beware of any dealership or lender promising "guaranteed approval" for bad credit car loans. While some lenders specialize in subprime financing, no legitimate lender can guarantee approval without first reviewing your financial situation. These promises are often a tactic to get you in the door, where you might then face exorbitant interest rates or pressure to buy a car you can’t truly afford.

Based on my experience working with countless individuals, the key is to understand that approval is always contingent on some level of financial assessment, even for subprime loans.

The Trade-Offs: Higher Costs and Stricter Terms

When you secure a car loan with bad credit and no money down, you should anticipate less favorable terms. This typically includes:

- Higher Interest Rates (APR): Lenders compensate for the increased risk by charging significantly higher interest rates. This means you’ll pay much more over the life of the loan.

- Longer Loan Terms: To make monthly payments seem more affordable, lenders might extend the loan term (e.g., 72 or 84 months). While this lowers the immediate payment, it dramatically increases the total interest paid and means you’ll be paying for a car that depreciates quickly.

- Limited Vehicle Choices: You might be restricted to older, higher-mileage vehicles that fall within a price range deemed acceptable by the lender, rather than the brand-new model you might have hoped for.

Strategies for Securing a Car Loan with Bad Credit and No Money Down

Navigating this complex terrain requires a well-thought-out plan. Here are the most effective strategies to improve your chances of approval.

1. Target Specialized Lenders

Traditional banks and prime lenders are unlikely to approve loans for individuals with bad credit and no money down. Your best bet lies with lenders who specialize in subprime auto loans.

- Subprime Lenders/Second-Chance Auto Lenders: These financial institutions focus on borrowers with less-than-perfect credit histories. They understand the challenges and structure their loans to mitigate their risk, often with higher interest rates. They look beyond just your credit score, considering your current income stability, employment history, and debt-to-income ratio.

- Credit Unions: While not always as flexible as dedicated subprime lenders, credit unions are member-owned and often have more lenient lending criteria than big banks. If you’re already a member or qualify for membership, it’s worth exploring their options. They may offer slightly better rates than other subprime options.

- "Buy Here, Pay Here" Dealerships: These dealerships act as both the seller and the lender. This can be a viable option for those with very poor credit or complex financial situations.

- Pros: Often have very high approval rates, as they control the entire process. They may not even check your credit score extensively, focusing instead on your income.

- Cons: Typically come with the highest interest rates, and the vehicle selection might be limited to older, higher-mileage cars. The reporting of payments to credit bureaus can also be inconsistent, potentially limiting your credit-building opportunities. Always ensure they report to all three major credit bureaus.

2. Strengthen Your Application (Beyond Your Credit Score)

Since your credit score isn’t ideal, you need to highlight other areas of financial strength.

- Proof of Stable Income: This is paramount. Lenders want to see consistent income that clearly demonstrates your ability to make monthly payments. Gather recent pay stubs (at least 3-6 months), bank statements, and proof of employment history. The longer and more stable your employment, the better.

- Low Debt-to-Income (DTI) Ratio: While your credit score is low, try to show that your existing debt obligations (excluding the potential car payment) are manageable relative to your income. A DTI below 40% is generally favorable.

- Bring a Co-Signer: This is one of the most effective ways to secure a loan with bad credit and no money down. A co-signer, typically someone with good credit, agrees to be equally responsible for the loan if you default.

- Pro Tip from Us: Choose a co-signer wisely. This is a significant financial commitment for them. Ensure they understand the responsibility and that you are fully committed to making all payments on time. Their credit will be affected if you miss payments.

- Common Mistakes to Avoid: Don’t pressure someone into co-signing. Be transparent about your financial situation and the risks involved.

3. Consider Your Vehicle Choice Wisely

When dealing with bad credit and no money down, your dream car might need to take a backseat to practicality.

- Affordable, Reliable Used Cars: Lenders are more comfortable financing less expensive vehicles, as the risk is lower. Focus on reliable, used cars that hold their value reasonably well. A lower purchase price means a smaller loan amount, which is easier to get approved for and more manageable to repay.

- Research Vehicle Value: Use resources like Kelley Blue Book (KBB.com) or Edmunds to determine the fair market value of any car you consider. This helps prevent overpaying and ensures the loan amount aligns with the vehicle’s worth.

Navigating the Loan Process: What to Expect

Once you’ve identified potential lenders and strengthened your application, the next step is to navigate the actual loan process.

1. Get Pre-Approved (If Possible)

Pre-approval involves a lender reviewing your financial information and giving you an estimate of how much you can borrow, at what interest rate, and under what terms.

- Benefits: Pre-approval gives you leverage at the dealership. You know your budget before you start shopping, preventing you from falling in love with a car you can’t afford. It also shows the dealership you’re a serious buyer with financing already lined up.

- Soft vs. Hard Inquiries: Initial pre-approval checks are often "soft inquiries," which don’t affect your credit score. Once you formally apply for a loan, it becomes a "hard inquiry," which can slightly lower your score for a short period. Group all your loan applications within a 14-45 day window to minimize the impact of multiple hard inquiries.

2. Shop Around for the Best Offers

Don’t settle for the first loan offer you receive, especially with bad credit. Different lenders will assess risk differently and offer varying rates and terms.

- Compare APRs: Focus on the Annual Percentage Rate (APR), which includes the interest rate plus any fees, giving you the true cost of borrowing.

- Analyze Loan Terms: Compare the length of the loan and the total amount you’ll pay over time. A lower monthly payment might seem attractive, but a longer term often means significantly more interest paid.

- Read the Fine Print: Understand all fees, prepayment penalties (though less common with subprime loans), and any other clauses in the loan agreement.

3. Understand All Loan Terms and Total Cost

When you receive a loan offer, it’s easy to get fixated on the monthly payment. However, it’s crucial to look beyond that figure.

- Total Cost of the Loan: Calculate the total amount you will pay over the life of the loan, including principal and all interest. A $10,000 car might end up costing you $15,000 or more with a high interest rate over a long term.

- The "Upside Down" Risk: With no money down, you’re immediately "upside down" on your loan, meaning you owe more than the car is worth. This can make it difficult to sell or trade in the car in the future if your financial situation changes. Consider gap insurance to protect yourself in case the car is totaled before you catch up on its value.

Common Mistakes to Avoid Are:

Based on my experience, many borrowers make avoidable errors when seeking car loans with bad credit and no money down:

- Accepting the First Offer: Never feel pressured to take the first deal presented. Always compare.

- Not Checking Your Credit Report: Obtain a free copy of your credit report from AnnualCreditReport.com. Check for errors that could be negatively impacting your score and dispute them.

- Overextending Yourself: Don’t agree to a monthly payment that stretches your budget too thin. Factor in insurance, fuel, and maintenance costs. A car is an ongoing expense.

- Falling for "Guaranteed Approval" Scams: These often lead to predatory loans with outrageous terms.

- Focusing Only on Monthly Payments: Always ask for the total cost of the loan and the APR.

The Long-Term Game: Rebuilding Credit

Securing a car loan with bad credit and no money down isn’t just about getting a car; it’s also a powerful opportunity to rebuild your financial standing. This loan can serve as a stepping stone to a better financial future.

Making Timely Payments

The most crucial step in rebuilding your credit is making every payment on time, every single month. Payment history accounts for 35% of your FICO score. Consistent, on-time payments will gradually improve your credit score.

Consider setting up automatic payments to avoid missing due dates. Even a single late payment can severely damage the progress you’ve made.

Paying More Than the Minimum (If Possible)

If your budget allows, paying a little extra each month can significantly reduce the total interest paid over the loan term and help you pay off the loan faster. This demonstrates even greater financial responsibility to credit bureaus.

The Positive Impact on Your Credit Score

As you consistently make payments, the positive activity will be reported to the credit bureaus. Over time, this will lead to a higher credit score, opening doors to better interest rates on future loans (like mortgages or personal loans) and credit cards. This initial loan, though perhaps costly, can be an investment in your financial future.

Pro Tips from Us: Your Expert Guide

Having guided countless individuals through challenging financial situations, here are some final pieces of advice to maximize your success and minimize pitfalls:

- Focus on Affordability First: Before you even look at cars, create a realistic budget that includes the potential car payment, insurance, gas, and maintenance. Do not get a loan that puts you in financial jeopardy.

- Consider a Small Down Payment, Even If Not Required: If you can scrape together even a few hundred dollars, it can significantly improve your loan terms. A down payment shows the lender you have "skin in the game" and reduces their risk. It also lessens the amount you finance and the interest you pay.

- Negotiate Beyond the Monthly Payment: Dealerships often try to focus solely on the monthly payment to make a car seem affordable. Always negotiate the total price of the car and the APR separately.

- Don’t Be Afraid to Walk Away: If a deal doesn’t feel right, the terms are too high, or you feel pressured, be prepared to walk away. There will always be other cars and other lenders. Patience is your ally.

- Look for Reputable Dealers and Lenders: Read reviews, check their BBB rating, and ensure they have a history of treating customers fairly, especially those with challenging credit.

For more insights on managing your auto loan and understanding financial terms, consider exploring our article on Navigating Auto Loan Interest Rates: What You Need to Know and Understanding Your Credit Score: A Comprehensive Guide. Additionally, the Consumer Financial Protection Bureau offers excellent resources on auto loans and consumer rights, which you can find on their official website (e.g., consumerfinance.gov).

Conclusion: Your Journey to Car Ownership Begins Here

Securing car loans with bad credit and no money down is undeniably a challenging undertaking, but it is far from an impossible one. By understanding the intricacies of subprime lending, strategically preparing your application, setting realistic expectations, and diligently researching your options, you can significantly improve your chances of success.

Remember, this isn’t just about getting a car; it’s about making a smart financial decision that serves your current needs while also paving the way for a stronger financial future. With careful planning, persistence, and the right approach, you can unlock the road ahead and drive away in a vehicle that meets your needs. Start your journey today with confidence and informed choices.