Unlocking the Road Ahead: Your Ultimate Guide to the Average APR for New Car Loans

Unlocking the Road Ahead: Your Ultimate Guide to the Average APR for New Car Loans Carloan.Guidemechanic.com

Navigating the world of car financing can feel like deciphering a complex code, especially when terms like "APR" start flying around. For many, the thrill of a new car quickly gives way to anxiety about interest rates and monthly payments. But what if you could approach the dealership—or your chosen lender—with confidence, armed with the knowledge to secure the best possible deal?

Understanding the Average APR for New Car Loans isn’t just about crunching numbers; it’s about empowering yourself. It’s the key to knowing if you’re getting a fair offer, saving thousands over the life of your loan, and ultimately, making a financially sound decision. This comprehensive guide will demystify APR, reveal the factors that shape your rate, and equip you with expert strategies to drive away with a fantastic deal.

Unlocking the Road Ahead: Your Ultimate Guide to the Average APR for New Car Loans

What Exactly is APR? Beyond Just the Interest Rate

Before we dive into averages, let’s clarify what APR truly means. APR stands for Annual Percentage Rate, and it’s far more important than just the stated interest rate. While the interest rate is the cost of borrowing the principal amount, the APR encompasses the total annual cost of your loan.

This crucial distinction means your APR includes not only the interest rate but also any additional fees or charges imposed by the lender. Think of origination fees, processing fees, or even certain insurance premiums bundled into the loan. By law, lenders must disclose the APR, giving you a transparent view of the complete cost of borrowing money for your new car.

Understanding APR is vital because it allows for an "apples-to-apples" comparison between different loan offers. A loan might advertise a low interest rate, but if its APR is significantly higher due to hidden fees, it could end up costing you more than a loan with a slightly higher interest rate but no extra charges. Always look at the APR when evaluating your options.

The Current Landscape: What’s the Average APR for New Car Loans Right Now?

So, what can you expect when you start looking for a new car loan today? The "average" APR is a moving target, influenced by a dynamic interplay of economic forces and individual borrower profiles. Generally, new car loan APRs typically range from 3% to 10% or even higher, depending heavily on a multitude of factors we’ll explore shortly.

Based on my experience, these averages are just starting points, not guarantees. The national average might be around 6-7% for a well-qualified buyer, but your specific rate could be significantly lower or higher. Economic conditions, such as the Federal Reserve’s interest rate policies, inflation, and overall market liquidity, play a significant role in dictating the baseline for lending rates across the board. When the Fed raises rates, the cost of borrowing for banks increases, which often translates to higher APRs for consumers.

For the most up-to-date national averages, reputable financial reporting sites and credit bureaus often publish quarterly reports. For instance, data from sources like Experian or Edmunds can provide real-time insights into prevailing market rates for different credit tiers. (External Link: Check current auto loan rates on Experian.com – Please note: This is a sample link. For actual deployment, verify the link’s validity and directness to current data.) Always remember that these averages reflect a broad spectrum of borrowers and situations, and your individual circumstances will be the ultimate determinant of your rate.

Key Factors That Influence Your New Car Loan APR

Your APR isn’t pulled out of thin air. It’s a carefully calculated risk assessment by lenders, based on several critical pieces of information about you and the loan itself. Understanding these factors is your first step towards securing a lower rate.

1. Your Credit Score: The Ultimate Financial Report Card

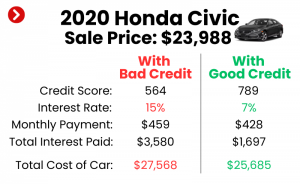

Without a doubt, your credit score is the single most influential factor in determining your car loan APR. This three-digit number, primarily FICO or VantageScore, tells lenders how reliably you’ve managed debt in the past. A higher score signals lower risk, which translates to a lower APR.

- Excellent Credit (780+): Borrowers in this tier typically qualify for the absolute best rates, often below the national average. Lenders see them as highly dependable.

- Good Credit (670-739): Most consumers fall into this category. You’ll still get competitive rates, though perhaps not the rock-bottom offers reserved for excellent credit.

- Fair Credit (580-669): Lenders consider this a moderate risk. APRs will be noticeably higher, reflecting the increased likelihood of late payments or default.

- Poor Credit (below 580): Securing a loan can be challenging, and if approved, the APR will be significantly higher, sometimes in the double digits.

Pro tips from us: Always check your credit score and report before you apply for a car loan. This allows you to identify any errors that could be dragging down your score and gives you time to address them. You can get free copies of your credit report annually from AnnualCreditReport.com.

2. Loan Term: The Length of Your Commitment

The loan term, or the duration over which you agree to repay the loan, also significantly impacts your APR. Generally, shorter loan terms come with lower APRs, while longer terms tend to have higher APRs.

Lenders view shorter terms (e.g., 36 or 48 months) as less risky because their money is tied up for a shorter period, reducing exposure to economic shifts or changes in your financial situation. While monthly payments will be higher with a shorter term, the total interest paid over the life of the loan will be substantially less. Conversely, longer terms (e.g., 72 or 84 months) offer lower monthly payments, which can be attractive for budget management. However, this convenience comes at a cost: a higher APR and significantly more total interest paid over time.

Common mistakes to avoid are automatically opting for the longest loan term to get the lowest monthly payment without considering the increased total cost and the extended period you’ll be making payments.

3. Down Payment Amount: Showing Your Commitment

The amount of money you put down upfront on your new car directly affects the principal loan amount, and consequently, your APR. A larger down payment reduces the amount you need to borrow, which lowers the lender’s risk.

When a lender’s risk is lower, they are often willing to offer a more attractive APR. Furthermore, a substantial down payment reduces your loan-to-value (LTV) ratio, meaning you owe less than the car is worth. This protects you from being "upside down" on your loan (owing more than the car is worth) and signals to the lender that you are a responsible borrower with a significant stake in the purchase. Aiming for at least a 10-20% down payment is generally recommended for new cars.

4. Debt-to-Income (DTI) Ratio: Your Financial Bandwidth

Your debt-to-income (DTI) ratio is a measure of your monthly debt payments compared to your gross monthly income. Lenders use this ratio to assess your ability to take on additional debt, like a new car loan. A lower DTI ratio indicates you have more disposable income available to comfortably make your car payments, making you a less risky borrower.

Typically, lenders prefer a DTI ratio of 36% or less, though some might go up to 43% or even higher depending on other factors. A high DTI suggests you might be overextended financially, which could lead to a higher APR or even loan denial. Before applying, calculate your DTI and consider paying down other debts if your ratio is on the higher side.

5. Vehicle Make, Model, and Age: The Asset’s Value

While this article focuses on new car loans, the specific vehicle you choose can subtly influence your APR. Certain makes and models hold their value better than others, which makes them less risky for lenders. If you default, the lender wants to be confident they can recoup their losses by selling the repossessed vehicle.

Luxury cars or vehicles with a history of rapid depreciation might sometimes see slightly higher APRs, as they represent a greater potential loss for the lender. Additionally, manufacturers often offer special low-APR financing incentives on specific new models to boost sales, which can significantly reduce your rate if you qualify.

6. Economic Conditions & Federal Reserve Rates: The Macro Picture

Beyond your personal financial profile, the broader economic climate plays a crucial role in shaping average APRs. When the Federal Reserve raises its benchmark interest rate, it becomes more expensive for banks to borrow money, a cost they then pass on to consumers through higher loan rates.

Conversely, during periods of economic slowdown, the Fed might lower rates to stimulate borrowing and spending, leading to more favorable APRs. Inflationary pressures can also influence rates, as lenders adjust to maintain their profit margins against the eroding value of money. While you can’t control these macro factors, being aware of them helps you understand why rates might fluctuate over time.

7. Lender Type: Where You Get Your Loan Matters

Not all lenders are created equal. The type of institution you choose for your car loan can also affect the APR you’re offered.

- Banks: Offer a wide range of loan products and often competitive rates, especially for prime borrowers.

- Credit Unions: Member-owned institutions that often provide some of the lowest APRs, as their mission is to serve their members rather than maximize profits. They are an excellent option to explore.

- Dealership Financing: Convenient, as you can arrange everything at the point of sale. However, dealerships sometimes mark up the interest rates offered by their partner lenders. They can also offer special manufacturer incentives that are very competitive.

- Online Lenders: Increasingly popular, these lenders often have streamlined application processes and can offer competitive rates, sometimes catering to a wider range of credit scores.

For a deeper dive into choosing the right lender and navigating the various options, check out our comprehensive article on .

Strategies to Secure the Best Possible New Car Loan APR

Knowing the factors is one thing; actively using that knowledge to your advantage is another. Here are proven strategies to help you lock in the lowest possible APR for your new car loan.

1. Know Your Credit Score (and Fix Any Errors)

This is non-negotiable. Before you even set foot in a dealership or apply online, pull your credit reports from all three major bureaus (Equifax, Experian, TransUnion) via AnnualCreditReport.com. Review them meticulously for any inaccuracies, such as accounts you didn’t open or payments you made that are incorrectly reported as late.

If you find errors, dispute them immediately. Correcting even minor mistakes can boost your score, potentially moving you into a better credit tier and qualifying you for a significantly lower APR. Based on my experience, many people skip this step, only to find out too late that a simple error cost them a better rate.

2. Get Pre-Approved by Multiple Lenders

This is perhaps the most powerful negotiation tool you have. Seek pre-approval from at least 2-3 different lenders—banks, credit unions, and online lenders—before you visit the dealership. Pre-approval gives you a concrete loan offer, including the APR and loan term, based on your creditworthiness.

Having pre-approval in hand transforms your position from a hopeful borrower to a cash buyer. You can walk into the dealership knowing exactly what APR you qualify for, which allows you to negotiate the car’s price separately and avoid getting played by inflated interest rates. If the dealership’s finance department can beat your pre-approved rate, great! If not, you have a solid backup.

3. Save for a Substantial Down Payment

As discussed, a larger down payment signals less risk to the lender and directly reduces the amount you need to borrow. Aim for at least 10% on a new car, but ideally 20% or more. This not only lowers your APR but also reduces your monthly payments and lessens the risk of being upside down on your loan.

Pro tips from us: Start saving early. Even an extra few hundred or thousand dollars can make a noticeable difference in your APR and overall loan cost. Consider setting up an automatic transfer to a dedicated "car down payment" savings account.

4. Choose the Right Loan Term for Your Budget

While a longer loan term means lower monthly payments, it almost always results in a higher APR and significantly more total interest paid. Carefully evaluate your budget to determine the shortest loan term you can comfortably afford.

For example, a 60-month loan often has a better APR than a 72-month loan. If the difference in monthly payment is manageable, opting for the shorter term will save you money in the long run. Common mistakes to avoid are extending the loan term purely to hit a specific low monthly payment without understanding the long-term financial implications.

5. Understand the Dealership’s Financing Office

When you’re at the dealership, they will inevitably offer to arrange financing for you. This can be convenient, but remember, the finance manager often earns a commission on the loans they arrange. They might try to "pack" the loan with high-profit add-ons like extended warranties, GAP insurance, or paint protection, which inflate your loan amount and total cost.

Be firm, review all documents carefully, and compare their financing offer (including the APR) directly against your pre-approvals. You are under no obligation to accept their financing. Negotiate each add-on separately, if you want them at all, and always check the price.

6. Consider a Co-signer (If Necessary and Strategic)

If your credit score is fair or poor, or if you’re a first-time buyer with a limited credit history, a co-signer with excellent credit can help you qualify for a much lower APR. A co-signer essentially guarantees the loan, reducing the lender’s risk.

However, this is a serious decision. The co-signer is equally responsible for the debt, and any missed payments will negatively impact their credit score as well. Only consider this option if both parties fully understand the risks and responsibilities involved.

7. Explore Refinancing Opportunities

Even if you don’t get the best APR on your initial loan, your financial journey doesn’t have to end there. If your credit score improves significantly after a year or two of on-time payments, or if market interest rates drop, you might be able to refinance your car loan for a lower APR.

Refinancing can save you a substantial amount of money over the remaining term of your loan. It’s always worth periodically checking current rates and comparing them to your existing loan. If you’re already in a car loan and looking to save, our guide on can provide you with all the details.

Calculating Your Potential Car Loan APR & Monthly Payments

While pre-approval gives you a precise rate, you can get a good estimate using online car loan calculators. These tools typically ask for the following information:

- Loan Amount: The price of the car minus your down payment.

- Loan Term: The number of months you plan to repay the loan.

- Estimated APR: Use the average rates for your credit tier as a starting point.

By inputting these figures, the calculator will provide an estimated monthly payment and the total interest you’ll pay over the life of the loan. This helps you budget effectively and understand the long-term cost implications of different APRs and loan terms. Experiment with different scenarios to see how a lower APR or a shorter term impacts your finances.

Common Pitfalls to Avoid When Financing a New Car

The car buying process is rife with potential financial traps. Being aware of these common mistakes can save you from costly regrets.

- Focusing Solely on Monthly Payments: Dealerships love to talk in terms of "how much per month." While important for budgeting, fixating only on the monthly payment can lead you to accept a longer loan term with a higher APR, resulting in significantly more interest paid overall. Always consider the total cost of the loan.

- Not Reading the Fine Print: Every document you sign has legal implications. Take your time, read all terms and conditions, and ask questions about anything you don’t understand before signing. Don’t let anyone rush you.

- Ignoring the Total Cost of the Loan: This includes the purchase price of the car, all interest paid over the loan term, and any fees. A lower APR means a lower total cost.

- Getting Lured by "0% APR" Deals Without Understanding Eligibility: While attractive, 0% APR offers are typically reserved for buyers with impeccable credit scores (usually 780+) and often on specific models or for shorter loan terms. Don’t assume you’ll qualify, and always compare it against other offers.

- Skipping Pre-approval: As emphasized, pre-approval is your strongest negotiation tool. Without it, you’re at the mercy of the dealership’s financing office, which may not always have your best financial interests at heart.

Conclusion: Drive Away with Confidence and a Great Rate

Understanding the Average APR for New Car Loans isn’t just a financial detail; it’s a fundamental aspect of smart car buying. By grasping what APR represents, knowing the factors that influence it, and proactively employing the strategies outlined in this guide, you can transform a potentially stressful experience into an empowering one.

Your credit score, the loan term, your down payment, and even the type of lender you choose all play pivotal roles in determining your ultimate APR. Take the time to prepare, compare offers, and negotiate wisely. Remember, the goal isn’t just to get a new car, but to do so on terms that make financial sense for you. Arm yourself with knowledge, and you’ll not only drive away in your dream car but also with the satisfaction of securing an excellent deal. Start your journey to a better car loan today!