Unlocking the True Cost: How Much Is A Car Loan, Really? Your Expert Guide to Smart Auto Financing

Unlocking the True Cost: How Much Is A Car Loan, Really? Your Expert Guide to Smart Auto Financing Carloan.Guidemechanic.com

Buying a car is an exciting milestone, offering freedom and convenience. Yet, for many, the joy quickly turns to anxiety when faced with the complexities of car loans. It’s not just about the sticker price; understanding "how much is a car loan" truly entails delving into a labyrinth of factors that shape your monthly payments and, more importantly, the total amount you’ll pay over time.

As an expert blogger and professional SEO content writer, my mission is to demystify this process for you. This comprehensive guide will break down every component of a car loan, providing you with the knowledge to make informed decisions. We’ll go beyond the surface, exploring hidden costs, strategic tips, and common pitfalls, ensuring you become a savvy auto finance consumer.

Unlocking the True Cost: How Much Is A Car Loan, Really? Your Expert Guide to Smart Auto Financing

The Foundation: Deconstructing Your Car Loan Cost

At its core, a car loan is a simple concept: you borrow money to buy a car, and you pay it back with interest over a set period. However, several key elements combine to determine your actual financial outlay. Let’s unpack these crucial components.

1. The Principal Amount: What You Actually Borrow

The principal amount is the actual sum of money you borrow from a lender to purchase your vehicle. This isn’t necessarily the car’s sticker price. It’s the negotiated price of the car minus any down payment or trade-in value you contribute.

For example, if you negotiate a car price of $30,000 and put down a $5,000 down payment, your principal loan amount would be $25,000. This figure forms the base upon which all other costs, primarily interest, are calculated. Understanding this distinction is the first step toward grasping your true loan cost.

2. The Interest Rate: The Cost of Borrowing Money

The interest rate is arguably the most significant factor influencing how much a car loan will cost you over its lifetime. It’s essentially the fee a lender charges for letting you borrow their money, expressed as a percentage of the principal loan amount. A higher interest rate means you’ll pay more for the privilege of borrowing.

Several variables influence the interest rate you’re offered. Your credit score is paramount, but the loan term, the type of car, and even the current economic climate also play a role. Based on my experience, even a slight difference in interest rates can translate into hundreds or thousands of dollars over the life of the loan. Shopping around for the best rate is not just good advice; it’s financially imperative.

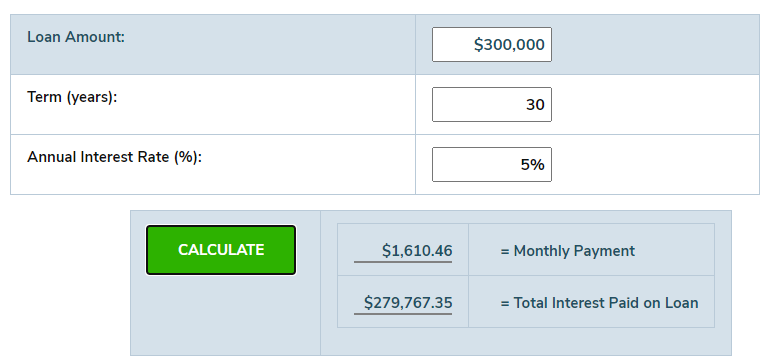

3. The Loan Term: How Long You’ll Be Paying

The loan term, or repayment period, is the length of time you have to pay back the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). This factor has a dual impact on your finances. A longer loan term generally results in lower monthly payments, which can seem appealing.

However, a longer term also means you’ll be paying interest for a more extended period. This inevitably leads to a higher total cost for the car. Conversely, a shorter loan term means higher monthly payments but significantly less interest paid over the life of the loan. It’s a delicate balance between affordability and overall cost efficiency.

Pro Tip from us: Don’t be swayed solely by the lowest monthly payment. Always ask for the total cost of the loan over its entire term. A low monthly payment on an 84-month loan might cost you far more in the long run than a slightly higher payment on a 60-month loan.

Initial Payments and Upfront Costs: Beyond the Monthly Bill

Before you even make your first monthly payment, there are other financial commitments that contribute to "how much is a car loan." These upfront costs can sometimes be overlooked, leading to budget surprises.

1. The Down Payment: Your Initial Investment

A down payment is the amount of money you pay upfront toward the purchase of the car, reducing the principal loan amount. While not always mandatory, making a substantial down payment offers several significant advantages. It lowers the amount you need to borrow, which in turn reduces your monthly payments and the total interest you’ll pay.

Furthermore, a larger down payment can make you a more attractive borrower to lenders, potentially qualifying you for a lower interest rate. It also helps you build equity in your vehicle faster and reduces the risk of being "upside down" on your loan (owing more than the car is worth).

2. Trade-in Value: Leveraging Your Old Ride

If you have an existing vehicle, its trade-in value can act similarly to a down payment. When you trade in your old car at the dealership, its appraised value is deducted from the purchase price of your new vehicle, directly reducing the principal amount you need to finance. This is a convenient way to lower your loan amount without tapping into your savings.

To maximize your trade-in value, ensure your vehicle is clean, well-maintained, and that you research its market value beforehand using resources like Kelley Blue Book or Edmunds. This preparation helps you negotiate effectively.

3. Fees and Taxes: The Often-Forgotten Expenses

Car loans come with a range of associated fees and taxes that can add a surprising amount to your overall cost. These vary by state and dealership but commonly include:

- Sales Tax: A percentage of the car’s purchase price, usually paid upfront or rolled into the loan.

- Registration Fees: Charges to register your vehicle with the state’s Department of Motor Vehicles (DMV).

- Documentation Fees (Doc Fees): Administrative fees charged by the dealership for processing paperwork.

- Title Fees: Costs associated with transferring the car’s title into your name.

- License Plate Fees: Charges for your vehicle’s license plates.

Common mistakes to avoid are: Forgetting to factor in these additional costs when calculating your budget. Always ask for a detailed breakdown of all fees and taxes before signing any paperwork. Dealers are legally obligated to disclose these, and being prepared will prevent any last-minute shocks.

Influential Factors: What Determines Your Specific Loan Offer?

Beyond the basic mechanics, several personal and market-driven factors heavily influence the interest rate you’re offered and, consequently, how much a car loan will ultimately cost you.

1. Your Credit Score: The Ultimate Game Changer

Your credit score is arguably the single most important factor in determining your car loan interest rate. Lenders use your credit score as a quick snapshot of your creditworthiness – your history of borrowing and repaying debt. A higher credit score (typically 700+) indicates a lower risk to lenders, often resulting in significantly lower interest rates. Conversely, a lower credit score can lead to higher rates or even loan denial.

Based on my experience, improving your credit score even by a few points before applying for a car loan can save you hundreds, if not thousands, of dollars. Pay bills on time, reduce existing debt, and check your credit report for errors well in advance.

2. Your Debt-to-Income Ratio (DTI): A Measure of Affordability

Lenders also assess your debt-to-income ratio (DTI), which compares your total monthly debt payments to your gross monthly income. A lower DTI indicates that you have more disposable income available to comfortably make your car loan payments, making you a less risky borrower.

A high DTI might signal to lenders that you’re already stretched thin financially, potentially leading to a higher interest rate or a requirement for a larger down payment. Understanding and, if necessary, improving your DTI before applying can significantly impact your loan terms.

3. Vehicle Choice: New vs. Used, Luxury vs. Economy

The type of vehicle you choose also plays a role. New cars often qualify for lower interest rates due to manufacturer incentives and their higher resale value. Used cars, while generally more affordable in purchase price, might come with slightly higher interest rates depending on their age, mileage, and condition, as they represent a greater risk to the lender.

Luxury vehicles, which typically have higher price tags, will naturally result in a larger principal loan amount, meaning higher monthly payments and total interest paid, even at a comparable interest rate. Choosing a car that aligns with your budget and needs is crucial for managing loan costs.

4. Lender Type: Where You Get Your Loan Matters

Not all lenders are created equal. You have several options when seeking a car loan, each with potential advantages:

- Banks: Offer competitive rates, especially if you have an existing relationship.

- Credit Unions: Often known for offering lower interest rates due to their non-profit structure.

- Dealership Financing: Convenient, but rates can vary widely. Dealers often work with multiple lenders and may mark up rates.

- Online Lenders: Provide quick approvals and often competitive rates, allowing for easy comparison shopping.

Based on my experience: Always get pre-approved for a loan from a bank or credit union before stepping into a dealership. This gives you a benchmark interest rate and empowers you to negotiate the best deal, treating dealership financing as another option to compare, not your only one.

Beyond Monthly Payments: Understanding Total Loan Cost

It’s easy to get fixated on the monthly payment, but focusing solely on this figure can be a costly mistake. The true measure of "how much is a car loan" is the total amount you will pay over the entire loan term.

The Amortization Effect: Interest First

Most car loans are amortized, meaning that in the early stages of your loan, a larger portion of your monthly payment goes toward interest, and a smaller portion goes toward reducing the principal. As the loan progresses, this ratio gradually shifts, with more of your payment attacking the principal balance.

This amortization schedule highlights why a longer loan term, even with a seemingly attractive low monthly payment, can lead to paying significantly more interest overall. You’re effectively paying the "cost of borrowing" for a longer period.

The Illusion of Lower Monthly Payments

While a lower monthly payment might seem like a financial relief, it often comes at the expense of paying more in total interest. Extending your loan term from, say, 60 months to 72 or 84 months will certainly reduce your monthly outlay. However, it also means you’re accruing interest for an additional year or two.

This is a common tactic used by dealerships to make expensive cars seem more affordable. Always look beyond the monthly payment and ask for the total cost of the loan, including all interest and fees. This transparency is key to smart financial planning.

(Internal Link Placeholder 1)

Beyond the Loan: The Full Spectrum of Car Ownership Costs

Even after you’ve secured your car loan, the financial journey of car ownership doesn’t end there. Understanding "how much is a car loan" requires acknowledging the broader financial implications of owning a vehicle. These ongoing costs are critical for a realistic budget.

1. Car Insurance: A Non-Negotiable Expense

Car insurance is a legal requirement in most places and a financial necessity everywhere. The cost of your insurance premiums will depend on numerous factors, including the type of car you drive, your driving history, your age, location, and the coverage limits you choose.

It’s crucial to get insurance quotes before finalizing your car purchase. A car that is expensive to insure can significantly increase your total monthly expenses, even if its loan payment seems affordable.

2. Maintenance and Repairs: The Unexpected Outlays

Every car, new or used, will require routine maintenance (oil changes, tire rotations, brake checks) and, eventually, repairs. These costs can be substantial, especially for older or luxury vehicles. Factor in an emergency fund for unexpected repairs.

Common mistakes to avoid are: Neglecting to budget for maintenance. Regular upkeep not only keeps your car running smoothly but also helps preserve its value, which can be beneficial if you plan to trade it in later.

3. Fuel Costs: A Constant Expenditure

With fluctuating gas prices, fuel can be a significant and ongoing expense. Consider the car’s fuel efficiency (miles per gallon or MPG) when making your purchase decision, especially if you have a long daily commute. An SUV or truck will typically cost more to fuel than a compact sedan.

4. Depreciation: The Silent Cost

While not a direct loan cost, depreciation is the loss in a vehicle’s value over time. It’s a significant financial aspect of car ownership. New cars typically lose a substantial portion of their value in the first few years. While you don’t write a check for depreciation, it impacts your equity and what you might get when you sell or trade in the vehicle.

Smart Strategies to Reduce Your Car Loan Costs

Now that you understand all the components, let’s talk about proactive steps you can take to minimize how much a car loan will cost you.

1. Improve Your Credit Score

As discussed, your credit score is king. Before applying for a loan, take steps to boost it: pay all bills on time, reduce credit card balances, and avoid opening new lines of credit. Even a few months of diligent effort can make a difference.

2. Save for a Larger Down Payment

The more you put down upfront, the less you borrow, and thus the less interest you pay. Aim for at least 20% for new cars to avoid negative equity, and consider even more for used cars. This also gives you more financial breathing room.

3. Shop Around for Rates (and Get Pre-Approved)

Don’t settle for the first loan offer. Contact multiple lenders—banks, credit unions, and online providers—to compare interest rates and terms. Getting pre-approved from at least two sources gives you negotiating power at the dealership.

4. Negotiate the Car Price

Remember, the car’s sticker price is just a starting point. Negotiate the purchase price of the vehicle before discussing financing. A lower purchase price directly translates to a smaller principal loan amount, reducing your overall costs.

5. Consider a Shorter Loan Term (If Affordable)

While monthly payments will be higher, a shorter loan term will dramatically reduce the total interest paid over the life of the loan. If your budget allows, opting for a 48 or 60-month loan instead of 72 or 84 months can save you thousands.

6. Explore Refinancing Options

If you already have a car loan and your credit score has improved, or interest rates have dropped, consider refinancing. You might qualify for a lower interest rate or a more favorable loan term, which can reduce your monthly payments or the total amount you pay over time.

(External Link Placeholder)

Budgeting for Your Car Loan: A Realistic Approach

Integrating your car loan into your overall financial picture is crucial. Don’t let the excitement of a new car overshadow sound financial planning.

The 20/4/10 Rule: A Good Starting Point

A popular guideline for car affordability is the 20/4/10 rule:

- 20% Down Payment: Aim to put down at least 20% of the car’s purchase price.

- 4-Year Loan Term: Keep your loan term to a maximum of four years (48 months) to minimize interest and avoid negative equity.

- 10% of Gross Income: Your total monthly car expenses (loan payment, insurance, fuel, maintenance) should not exceed 10% of your gross monthly income.

While a guideline, this rule provides a solid framework for determining a truly affordable car loan. Adjust it based on your personal financial situation and comfort level.

Creating a Realistic Budget

Before you even start looking at cars, create a detailed budget. Account for your income, existing debts, living expenses, and savings goals. Then, determine how much you can realistically afford for a car payment, insurance, and ongoing maintenance without stretching yourself too thin.

Based on my experience: Many people make the mistake of buying "too much car" and end up struggling with payments or neglecting other important financial goals. A car should enhance your life, not burden it. Be honest with yourself about what you can comfortably afford.

(Internal Link Placeholder 2)

Conclusion: Empowering Your Car Loan Journey

Understanding "how much is a car loan" is far more nuanced than simply looking at a monthly payment. It encompasses the principal, interest, loan term, down payment, fees, your creditworthiness, and even the type of car you choose. By delving into each of these components, you gain the power to negotiate effectively, secure the best possible terms, and avoid costly mistakes.

Remember, a car loan is a significant financial commitment. Approaching it with comprehensive knowledge and a strategic mindset will not only save you money but also provide peace of mind. Use this guide as your roadmap to navigate the auto financing landscape with confidence, ensuring your next car purchase is a smart financial move that genuinely adds value to your life. Drive safely and wisely!