Unlocking the Truth About 0 Car Loans: Your Ultimate Guide to Driving Smarter

Unlocking the Truth About 0 Car Loans: Your Ultimate Guide to Driving Smarter Carloan.Guidemechanic.com

The allure of a "0 car loan" is powerful. Imagine driving off the lot in a brand-new vehicle, knowing you won’t pay a single cent in interest over the life of your loan. It sounds like a dream come true for any car buyer. In a world where every penny counts, the prospect of saving thousands on interest charges can be incredibly tempting.

However, as an expert in automotive financing and a seasoned blogger, I can tell you that while 0 APR (Annual Percentage Rate) car loans are indeed real, they come with a specific set of circumstances and conditions. They aren’t a universal solution for everyone, and understanding their intricacies is crucial for making a truly smart financial decision. This comprehensive guide will demystify 0 car loans, helping you navigate the fine print, assess your eligibility, and ultimately determine if this seemingly perfect deal is the right path for your next vehicle purchase.

Unlocking the Truth About 0 Car Loans: Your Ultimate Guide to Driving Smarter

What Exactly Are 0 Car Loans? The Allure and Reality

A 0 car loan, also known as a zero-interest car loan or 0 APR financing, is a special offer where the lender charges no interest on the money borrowed to purchase a vehicle. This means that over the term of the loan, you only pay back the principal amount—the sticker price of the car (minus any down payment or trade-in value). The appeal is obvious: it’s essentially like getting an interest-free installment plan for a major purchase.

From a consumer’s perspective, this can lead to substantial savings. For instance, on a $30,000 car financed over five years at a typical 5% interest rate, you could pay over $4,000 in interest alone. A 0 APR loan eliminates that entire cost, making your total expenditure significantly lower. This is why these offers are so heavily advertised and why they capture the imagination of potential buyers.

However, these offers don’t appear out of thin air. They are typically manufacturer-backed incentives, designed to boost sales of specific models, clear out older inventory, or stimulate demand during slow periods. Car manufacturers often subsidize these low-interest rates for their affiliated finance companies, absorbing the cost themselves as a marketing expense. This allows dealerships to advertise highly attractive rates without losing profit on the vehicle sale itself.

The "Catch": Understanding the Fine Print of Zero Interest

While 0 APR sounds incredibly straightforward, it’s essential to understand that there’s always a mechanism behind such generous offers. It’s not truly "free money" in the sense that there are no strings attached. These deals are strategically crafted financial products, and knowing the underlying conditions is key to leveraging them effectively.

One of the most significant "catches" often relates to the eligibility criteria. These loans are not universally available to all buyers. Lenders, even when backed by manufacturers, still need to mitigate their risk. Therefore, they reserve these premium offers for customers who represent the lowest possible risk of default. This means a very specific financial profile is required.

Another common trade-off involves the vehicle itself. Zero interest offers are frequently tied to particular models, often those that are less popular, older stock, or vehicles the manufacturer is trying to move quickly. This can limit your choices, potentially steering you away from your ideal car. Sometimes, these offers might also exclude specific trim levels or optional features, further narrowing your options.

Who Truly Qualifies for a 0 APR Car Loan?

Securing a 0 APR car loan is a testament to your financial responsibility and creditworthiness. Based on my experience in the automotive finance industry, the requirements are stringent and generally non-negotiable. Lenders are looking for a very specific type of borrower to qualify for these premium deals.

Excellent Credit Score is Paramount

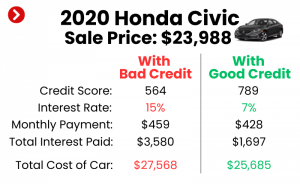

The single most critical factor is an excellent credit score. We’re talking about scores typically in the 750-800+ FICO range. Lenders use these scores to predict your likelihood of repaying debt. A score this high indicates a long history of on-time payments, responsible credit utilization, and a low risk of default. Without a stellar credit history, it’s highly unlikely you’ll be approved for a zero-interest offer. If your credit needs a boost, consider exploring resources like our guide on How to Improve Your Credit Score for a Car Loan to get ready.

Stable Income and Low Debt-to-Income Ratio

Beyond your credit score, lenders will scrutinize your income and existing debt. You’ll need to demonstrate a stable and verifiable income source that comfortably covers your proposed monthly car payment, along with all your other financial obligations. A low debt-to-income (DTI) ratio is also crucial. This ratio compares your total monthly debt payments to your gross monthly income. Lenders prefer a DTI ratio that indicates you have plenty of disposable income to manage new debt without strain.

Substantial Down Payment (Often Preferred)

While not always an absolute requirement, making a significant down payment can greatly improve your chances. A larger down payment reduces the amount you need to borrow, thereby lowering the lender’s risk. It also shows your commitment and financial stability. Some 0 APR offers might explicitly require a certain percentage down, such as 10% or 20%, to qualify for the special rate.

Specific Car Models and Loan Terms

As mentioned, 0 APR offers are rarely universal. They are usually tied to specific new car models that the manufacturer wants to sell. These might be last year’s models, vehicles with an upcoming redesign, or cars that aren’t selling as quickly as anticipated. Furthermore, the loan terms are often shorter, typically 36 or 48 months, though some might extend to 60 months. Longer terms mean higher total interest paid for standard loans, but for 0 APR, a shorter term can lead to higher monthly payments.

The Undeniable Pros of Securing a 0 APR Car Loan

If you meet the strict eligibility criteria, a 0 APR car loan offers several compelling advantages that can significantly benefit your financial situation. These benefits go beyond just the obvious savings and contribute to a healthier overall financial picture.

Significant Savings on Interest Costs

The most apparent benefit is the elimination of interest charges. On a typical car loan, interest can add thousands of dollars to the total cost of your vehicle. With 0 APR financing, every dollar you pay goes directly towards reducing your principal balance. This means you’re truly paying only for the car itself, which is a powerful financial advantage.

Lower Total Cost of Ownership

By cutting out interest, you reduce the overall cost of owning your vehicle. This can free up funds that you might otherwise spend on interest, allowing you to allocate that money towards other financial goals, such as savings, investments, or paying down other higher-interest debts. It makes the car purchase a more efficient use of your capital.

Faster Payoff and Debt-Free Living

Since all your payments attack the principal, you’ll pay off your car loan much faster than you would with an interest-bearing loan, assuming the same payment amount. Even with potentially higher monthly payments due to shorter terms, the speed at which you become debt-free is a significant advantage. This quick debt elimination can provide a great sense of financial freedom and peace of mind.

Psychological Benefit and Financial Empowerment

There’s a strong psychological benefit to knowing you’re not paying extra money just for the privilege of borrowing. It feels like a smart, savvy move. This sense of financial empowerment can motivate you to make other smart money choices, reinforcing good financial habits. It’s a win that goes beyond just the dollar amount.

Cons and Potential Pitfalls: What to Watch Out For

Despite the attractive headline, 0 APR car loans aren’t without their downsides and potential traps. It’s crucial to approach these deals with a critical eye, understanding that what looks too good to be true often has nuances that need careful consideration.

Stricter Eligibility Requirements

As previously discussed, the biggest hurdle is qualifying. If your credit score isn’t stellar, or your financial profile has any red flags, you simply won’t be approved. This can lead to disappointment and potentially push you into a less favorable standard loan if you’re not prepared. Don’t assume you’ll qualify; always check your credit score first.

Limited Vehicle Choice

Zero interest offers are rarely available across an entire dealership’s inventory. They are typically reserved for specific models, trims, or even individual vehicles that the dealer or manufacturer wants to sell quickly. This can severely limit your options, forcing you to choose a car that might not be your first preference, just to get the financing deal. You might compromise on features, color, or even the type of vehicle you truly need.

Shorter Loan Terms Often Mean Higher Monthly Payments

While a shorter loan term means you pay off the car faster, it also means your monthly payments will be significantly higher. For example, a $25,000 car financed over 36 months will have a much higher monthly payment than the same car financed over 60 or 72 months. If your budget can’t comfortably handle these elevated payments, even a 0 APR loan can become a financial strain. This is a common mistake: focusing only on the APR and neglecting the monthly budget.

Less Room for Negotiation on Car Price

Dealers often view 0 APR offers as their primary incentive to sell a vehicle. When you take advantage of such a deal, you might find that the dealership is less willing to negotiate on the car’s sticker price. They’ve already given up their potential profit on the financing, so they’ll want to maximize their profit on the vehicle itself. Sometimes, taking a small rebate or negotiating a lower price and a standard low-interest loan might actually save you more money overall than a 0 APR deal at full price.

"Payment Packing" and Additional Fees

Common mistakes to avoid are focusing solely on the monthly payment or the APR. Dealerships sometimes engage in practices like "payment packing," where they add unnecessary extras (like extended warranties, paint protection, or VIN etching) into your loan without clear explanation, inflating your total cost. Always scrutinize every line item on your contract. Make sure you understand exactly what you’re paying for beyond the car itself.

Navigating the Dealership: Pro Tips for Success

Armed with knowledge, you can approach the dealership confidently when considering a 0 APR car loan. Based on my experience, careful preparation and a strategic mindset are your best tools for securing the best possible deal.

Do Your Homework Before You Visit

Before even stepping foot on a car lot, research the specific 0 APR offers available from different manufacturers and dealerships. Understand which models are eligible, the typical loan terms, and any specific requirements. Knowing this information beforehand puts you in a strong negotiating position and helps you avoid being swayed by high-pressure sales tactics.

Get Pre-Approved for a Standard Loan First

Even if you’re aiming for 0 APR, it’s a pro tip from us to get pre-approved for a standard car loan from your bank or credit union beforehand. This serves two crucial purposes. First, it gives you a benchmark; you’ll know the best interest rate you can get elsewhere. Second, it provides leverage. If the dealership isn’t willing to budge on the car price with the 0 APR offer, you can always fall back on your pre-approved loan at a competitive rate, allowing you more room to negotiate the vehicle’s cost.

Negotiate the Car Price Separately from Financing

This is a critical strategy. Always negotiate the actual purchase price of the car first, as if you were paying cash. Once you’ve agreed on the lowest possible price for the vehicle, then introduce the discussion about financing options, including the 0 APR offer. This prevents the dealership from obscuring the true cost of the car by bundling it with the financing deal. It ensures you’re getting the best price on the car and the best financing.

Understand All Fees and Read the Contract Carefully

Never rush through the paperwork. Scrutinize every fee listed on the contract. Ask for clarification on anything you don’t understand, including documentation fees, registration fees, and any optional add-ons. Common mistakes to avoid include signing a contract before thoroughly reading it or feeling pressured to sign quickly. Ensure that the agreed-upon price, interest rate (0%!), and loan terms are accurately reflected. Don’t hesitate to take your time or even ask to review the contract away from the high-pressure environment of the finance office if permitted.

Common Mistakes to Avoid When Considering a 0 Car Loan

Even the most informed buyers can sometimes stumble when faced with the excitement of a new car and an enticing 0 APR offer. Being aware of these common pitfalls can help you stay grounded and make a truly wise decision.

Focusing Only on the APR, Ignoring Total Cost

The 0% interest rate is a huge draw, but it’s not the only number that matters. Common mistakes to avoid include overlooking the actual sale price of the vehicle. Sometimes, a dealership might offer a cash rebate or a lower sale price if you opt for standard financing instead of the 0 APR deal. It’s crucial to calculate the total cost of ownership under both scenarios – 0 APR at full price versus a lower price with a low-interest loan – to see which option truly saves you more money.

Not Understanding Your Eligibility

Many prospective buyers walk into a dealership assuming they’ll qualify for 0 APR, only to be disappointed. This can lead to frustration and feeling pressured into a less favorable deal. Always check your credit score and understand the typical eligibility requirements before you start shopping. Knowing your financial standing empowers you and prevents wasted time.

Rushing Into a Deal

Car buying can be an emotional process, especially when a great deal is on the table. However, rushing your decision is a common mistake. Take your time to compare offers, read reviews, and ensure the vehicle meets your needs. Don’t let the fear of missing out on a 0 APR deal push you into a purchase you’ll regret or a car that isn’t suitable for your lifestyle.

Ignoring the Value of Your Trade-In

Your trade-in vehicle is a separate asset, and its value should be negotiated independently. Don’t let a dealership bundle the trade-in discussion with the 0 APR offer. Dealers might offer less for your trade-in when you’re taking advantage of their financing incentives. Get an independent appraisal for your trade-in beforehand from sources like Kelley Blue Book or Edmunds, and negotiate its value separately.

Assuming All 0 APR Deals Are Equal

Not all zero-interest offers are identical. Some might be for shorter terms, others for specific trim levels, and some might require a larger down payment. Read the fine print of each individual offer carefully. Compare the specific conditions, eligible vehicles, and loan terms across different dealerships and manufacturers. A blanket assumption that all 0 APR deals are the same can lead to unexpected limitations or costs.

Alternatives to 0 APR Car Loans

What if you don’t qualify for a 0 APR loan, or the eligible vehicles don’t match your needs? Don’t despair! There are many excellent financing alternatives that can still help you secure a great deal on your next car.

Low-Interest Standard Auto Loans

For buyers with good (but not necessarily excellent) credit, a standard auto loan from a bank, credit union, or even the dealership’s finance department can still offer very competitive interest rates. Often, rates in the 2-4% range are available, which are still significantly lower than the national average. Shopping around and getting pre-approved from multiple lenders can help you find the best rate.

Used Car Loans

If buying new isn’t a priority, consider a quality used car. Used car loans often come with slightly higher interest rates than new car loans, but the initial purchase price of a used vehicle is typically much lower. This can lead to lower overall costs and more manageable monthly payments. Many certified pre-owned (CPO) programs offer attractive financing and extended warranties, providing peace of mind.

Cash Purchase (If Feasible)

The ultimate interest-free car purchase is, of course, paying with cash. If you have the savings and don’t need to finance, buying outright eliminates all interest and loan obligations. While this isn’t an option for everyone, it’s always worth considering if your financial situation allows. It gives you immediate ownership and freedom.

Leasing

Leasing is a different financial model where you essentially "rent" a new car for a set period (usually 2-4 years) and mileage limit. You make monthly payments, but you don’t own the car at the end of the term. Leasing often comes with lower monthly payments than buying, and you always get to drive a new car with the latest features. However, it doesn’t build equity, and you have mileage restrictions and potential end-of-lease fees. It’s a great option for those who like to frequently upgrade their vehicle and don’t mind not owning it.

Is a 0 APR Car Loan Right for You? A Decision Framework

Deciding whether a 0 APR car loan is the best choice involves more than just seeing the "0%" sign. It requires a thoughtful self-assessment and a careful weighing of your personal financial situation against the specific terms of the offer.

Self-Assessment Checklist:

- Credit Score: Is your FICO score consistently above 750?

- Budget: Can you comfortably afford the higher monthly payments that often come with shorter 0 APR loan terms?

- Vehicle Needs: Are you genuinely happy with the specific car models that are eligible for the 0 APR offer, or would you be compromising significantly?

- Down Payment: Are you able to make a substantial down payment, potentially 10-20% or more, if required?

- Financial Goals: Does taking on this specific car loan align with your broader financial goals (e.g., saving for a home, retirement, debt reduction)?

Weighing Pros and Cons for Your Individual Situation:

If you have excellent credit, can afford the monthly payments, and the eligible car is exactly what you want, a 0 APR loan can be an exceptional financial move. The savings on interest are undeniable and can significantly reduce your total cost of ownership. It’s a powerful tool for getting into a new vehicle without the burden of financing charges.

However, if your credit isn’t perfect, or if the 0 APR offer forces you into a car you don’t truly love or into monthly payments that stretch your budget, then it’s probably not the right choice. Don’t let the allure of "free money" overshadow practical financial considerations. In such cases, a low-interest standard loan on a car you genuinely prefer, or even a well-researched used car purchase, might be a much smarter financial decision in the long run. The best car loan is the one that fits your needs, not just the one with the lowest APR.

Driving Smarter: Your Path to a Great Deal

The appeal of a 0 car loan is undeniable, promising significant savings and the satisfaction of paying only for the vehicle itself. However, as we’ve explored, these premium offers are not a one-size-fits-all solution. They are strategic incentives designed for a specific segment of highly creditworthy buyers, often tied to particular vehicle models and stricter loan terms.

To truly drive smarter, you must approach 0 APR deals with diligence and a critical eye. Understand the stringent eligibility requirements, be aware of potential pitfalls like limited choices or less room for price negotiation, and always read every line of the contract. Remember the pro tip: negotiate the car’s price separately before discussing financing. By doing so, you ensure you’re getting the best deal on both the vehicle and the financing. For further reading on making informed car buying decisions, check out our article on Negotiating Car Prices: A Step-by-Step Guide.

Ultimately, the best car loan is one that aligns perfectly with your financial health and vehicle needs. Whether it’s a coveted 0 APR offer or a competitive standard loan, your goal should be financial empowerment. By educating yourself and shopping wisely, you can confidently navigate the complex world of automotive financing and make a decision that puts you in the driver’s seat of a great deal and a sound financial future. For more general consumer advice on car buying, you can also consult resources from trusted organizations like the Consumer Financial Protection Bureau.