Unlocking Value: A Deep Dive into Farm Bureau Car Loan Rates for Smart Car Buyers

Unlocking Value: A Deep Dive into Farm Bureau Car Loan Rates for Smart Car Buyers Carloan.Guidemechanic.com

Buying a car is a significant financial decision, and securing the right financing can make all the difference in your budget and overall ownership experience. Among the myriad of lending institutions, Farm Bureau often emerges as a compelling option, especially for its members. But what exactly are Farm Bureau car loan rates, and how do they stack up against other lenders?

As an expert blogger and someone deeply familiar with the intricacies of vehicle financing, I understand the questions swirling in your mind. This comprehensive guide is designed to peel back the layers, offering you an in-depth look at Farm Bureau car loan rates, the factors that influence them, and how you can leverage your membership for the best possible deal. Our goal is to equip you with the knowledge to make an informed, confident decision.

Unlocking Value: A Deep Dive into Farm Bureau Car Loan Rates for Smart Car Buyers

Understanding Farm Bureau: More Than Just Farming

Before we delve into the specifics of car loans, it’s crucial to grasp the essence of Farm Bureau itself. Often perceived solely as an agricultural organization, the American Farm Bureau Federation and its state-level counterparts are, in fact, much broader. They are a national organization advocating for farmers, ranchers, and rural communities, but their reach extends far beyond that.

Across the United States, Farm Bureau operates as a grassroots organization, providing a wide array of services and benefits to its members. Membership is typically open to anyone, regardless of whether they are directly involved in agriculture. This inclusivity is a key point, as it means many people can access their benefits without needing to be a farmer.

These benefits often include insurance services – covering everything from auto and home to life and health – and various financial products, including loans. The core mission revolves around community support, advocacy, and providing value to its members through collective strength. This unique structure often translates into competitive offerings for members.

Why Consider Farm Bureau for Your Car Loan?

When you’re shopping for a car loan, you’re faced with a dizzying array of choices: banks, credit unions, dealership financing, and online lenders. Farm Bureau car loans carve out a distinct niche, offering several compelling advantages that warrant a closer look.

Exclusive Member Benefits

One of the most significant draws of Farm Bureau is its member-centric approach. Unlike traditional banks that offer generalized services, Farm Bureau leverages its membership model to provide exclusive perks. These can range from discounts on vehicles themselves to preferential rates on loans and insurance.

These benefits are designed to add tangible value, making membership a worthwhile investment even if your primary interest is just a car loan. It’s a testament to their commitment to their community.

Potentially Competitive Rates

The phrase "Farm Bureau car loan rates" often conjures images of favorable terms, and for good reason. Due to their non-profit or member-owned structure in many instances, and their focus on providing value, Farm Bureau often boasts competitive interest rates. They might not always be the absolute lowest, but they are consistently strong contenders, especially when considering the holistic value package.

Based on my experience in the lending landscape, these rates are often comparable to, or even better than, those offered by many credit unions. This is particularly true for members with strong credit profiles.

Personalized Service and Local Agent Advantage

Another distinct advantage is the personalized service you often receive. Many Farm Bureau operations are rooted in local communities, allowing for direct interaction with agents. This isn’t just about processing paperwork; it’s about building relationships.

Having a local agent means you can sit down, discuss your financial situation, and get tailored advice. This level of personal touch is a stark contrast to the often impersonal experience of large online lenders or national banks. They understand local market conditions and can guide you through the process with a familiar face.

Community Focus and Trustworthiness

Farm Bureau has a long-standing history and a strong reputation built on trust and community support. For many, this translates into peace of mind when securing a loan. Knowing you’re working with an organization that prioritizes its members and local communities can be a significant factor.

This inherent trust can simplify the decision-making process, especially for those who prefer to keep their financial dealings within organizations they know and respect. It’s about more than just numbers; it’s about reliability.

Demystifying Farm Bureau Car Loan Rates

Understanding how Farm Bureau car loan rates are determined is crucial for anyone seeking financing. It’s not a one-size-fits-all scenario; several factors converge to shape the interest rate you’re offered. Let’s break down these critical components.

What Affects Your Car Loan Rate?

Your interest rate is a reflection of the lender’s perceived risk in lending you money. The lower the risk, the lower your rate. Here’s what lenders, including Farm Bureau, typically evaluate:

- Credit Score: This is arguably the most significant factor. Your credit score is a numerical representation of your creditworthiness, based on your payment history, amounts owed, length of credit history, new credit, and credit mix. A higher score (generally 700+) indicates a lower risk and typically qualifies you for the best Farm Bureau car loan rates. Conversely, a lower score will result in a higher rate.

- Loan Term: This refers to the duration over which you will repay the loan. Common terms range from 36 to 84 months. Shorter terms usually come with lower interest rates because the lender’s money is tied up for less time, reducing their risk. However, shorter terms mean higher monthly payments. Longer terms offer lower monthly payments but typically carry higher interest rates and mean you pay more in total interest over the life of the loan.

- Loan Amount: The total amount you borrow can also subtly influence the rate. While not as direct as credit score, very large or very small loan amounts might be subject to slightly different risk assessments. Lenders often have minimum and maximum loan amounts they are comfortable with.

- Down Payment: Making a substantial down payment reduces the loan amount you need to borrow and signals financial stability to the lender. It reduces their risk exposure, as you have more equity in the vehicle from day one. A larger down payment can often lead to a more favorable interest rate.

- Vehicle Type (New vs. Used): New cars often qualify for lower interest rates compared to used cars. This is because new cars typically have a clear value, a warranty, and are less prone to immediate mechanical issues. Used cars, with their varying conditions and depreciation, are seen as slightly riskier collateral.

- Market Conditions: Broader economic factors play a role too. The prevailing interest rate environment, set by central banks, influences the cost of borrowing for all lenders. When these rates are low, car loan rates across the board tend to be lower, and vice-versa.

How Farm Bureau Determines Rates

Farm Bureau, while factoring in the points above, also incorporates its unique membership model into its rate determination.

- Membership Status: Being a member is the gateway to their specific rates and benefits. Some Farm Bureau state organizations might even offer tiered rates based on the length or type of your membership.

- Underwriting Process: Like any lender, Farm Bureau has an underwriting process to assess your financial health and ability to repay the loan. This involves reviewing your credit report, income, debt-to-income ratio, and employment history.

- Relationship Banking: If you have other financial products with Farm Bureau, such as auto insurance, there might be opportunities for additional discounts or preferential rates. Building a comprehensive financial relationship can sometimes unlock better terms.

The Farm Bureau Car Loan Application Process: A Step-by-Step Guide

Applying for a Farm Bureau car loan is a straightforward process, but understanding each step can help you navigate it smoothly and efficiently.

Becoming a Member

The first and most fundamental step is to become a Farm Bureau member. As mentioned, membership is typically open to everyone and usually involves an annual fee, which is often quite affordable. You can usually join online through your state’s Farm Bureau website or by visiting a local office. This membership is your key to accessing their car loan rates and other benefits.

Gathering Your Documents

Before you even start the application, having all your necessary documents in order will save you time and potential frustration. You’ll typically need:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Pay stubs, tax returns, or bank statements to verify your ability to repay.

- Proof of Residence: Utility bills or a lease agreement.

- Social Security Number: For credit checks.

- Vehicle Information (if applicable): If you’ve already found a car, details like VIN, make, model, and year will be required.

Applying for the Loan

Once you’re a member and have your documents ready, you can submit your application. This can often be done in several ways:

- Online: Many state Farm Bureau organizations offer online application portals for convenience.

- In-Person: Visiting a local Farm Bureau office allows you to speak directly with an agent, which can be beneficial for personalized guidance.

- By Phone: Some may offer phone applications.

During the application, you’ll provide your personal and financial details. Be thorough and accurate to avoid delays.

Understanding the Offer

If your application is approved, Farm Bureau will present you with a loan offer. This will include the approved loan amount, the interest rate (APR), the loan term, and your estimated monthly payments. It’s crucial to review these terms carefully.

Remember, the Annual Percentage Rate (APR) includes not only the interest rate but also any additional fees associated with the loan, giving you a truer picture of the total cost. Don’t hesitate to ask your agent to explain anything you don’t understand.

Closing the Deal

Once you accept the loan offer, you’ll proceed to the closing. This involves signing the loan documents, which legally bind you to the terms. Ensure you read every document before signing.

The funds will then be disbursed, either directly to you (for a private sale) or to the dealership. You’ll then be ready to drive off in your new vehicle!

Pro Tip from Us: Always try to get pre-approved for a car loan before you step onto a dealership lot. A pre-approval gives you a clear understanding of what you can afford and provides significant negotiating power. It transforms you from a casual shopper into a serious buyer with financing already secured.

Comparing Farm Bureau Rates: How Do They Stack Up?

Evaluating Farm Bureau car loan rates in isolation isn’t enough. To truly understand their value, you need to compare them against other common lending sources.

Bank vs. Credit Union vs. Dealership vs. Farm Bureau

- Banks: Large national banks often have a wide range of loan products and competitive rates, especially for prime borrowers. However, they can sometimes lack the personalized touch of smaller institutions.

- Credit Unions: Known for their member-centric approach and often lower interest rates, credit unions are strong competitors. They are similar to Farm Bureau in their community focus but might have stricter membership requirements.

- Dealership Financing: While convenient, dealership financing often involves an intermediary mark-up. They might offer promotional 0% APR deals, but these are typically reserved for those with impeccable credit on specific new models. For most buyers, dealership rates can be higher than what you could get independently.

- Farm Bureau: Farm Bureau often sits comfortably alongside credit unions, offering competitive rates, personalized service, and the added benefit of their broader membership perks. Their rates are typically more favorable than average bank rates and almost always better than standard dealership rates.

What to Look For Beyond the Rate

While the interest rate is paramount, a truly smart car buyer looks beyond just the APR.

- Fees: Are there any origination fees, application fees, or prepayment penalties? Some lenders charge these, which can add to your overall cost. Farm Bureau, like many member-focused organizations, often has transparent and minimal fees.

- Flexibility: How flexible are the loan terms? Can you choose a term that suits your budget? Does the lender offer options for payment deferral in case of financial hardship?

- Customer Service: How easy is it to communicate with your lender? Is there a dedicated point of contact? Good customer service can make a significant difference if you encounter issues during the life of your loan.

- Insurance Discounts: With Farm Bureau, check if securing a car loan also opens doors to better rates on your auto insurance, creating a synergistic financial benefit.

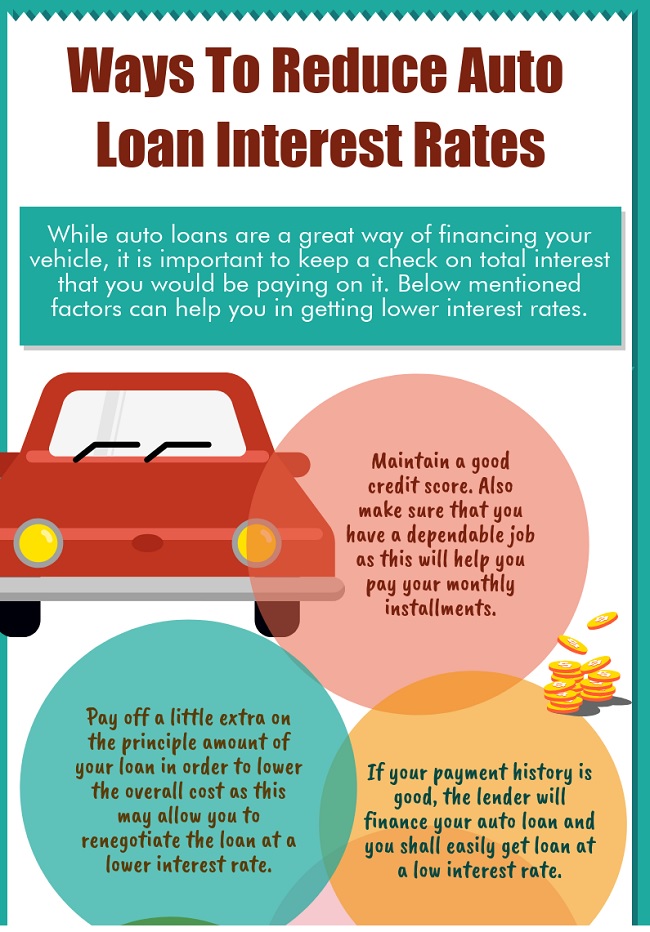

Maximizing Your Chances for the Best Farm Bureau Car Loan Rate

Securing the most favorable Farm Bureau car loan rate requires proactive steps and strategic planning. Here’s how you can optimize your application.

Improve Your Credit Score

This is foundational. If your credit score isn’t in the "excellent" range, take steps to improve it before applying. Pay off existing debts, especially credit card balances, and ensure all your payments are made on time. You can also dispute any errors on your credit report. Even a small increase in your score can translate into significant savings over the life of the loan.

Internal Link: For a deeper dive into improving your credit, check out our article on . (Placeholder for internal link)

Save for a Larger Down Payment

The more you put down upfront, the less you need to borrow, and the lower the risk for the lender. Aim for at least 10-20% of the car’s purchase price. A larger down payment can not only secure a better interest rate but also reduce your monthly payments and protect you from negative equity (owing more than the car is worth).

Choose a Shorter Loan Term

While a longer term offers lower monthly payments, it almost always means a higher overall cost due to increased interest. If your budget allows, opt for the shortest loan term you can comfortably afford. This will reduce the total interest paid and help you become debt-free faster.

Negotiate the Car Price

Remember that your car loan is based on the final price of the vehicle. A lower purchase price means you’re borrowing less, which indirectly makes your loan more affordable. Don’t be afraid to negotiate aggressively with the dealership on the car’s price before you even discuss financing.

Internal Link: Learn powerful negotiation tactics in our guide to . (Placeholder for internal link)

Leverage Your Membership

Don’t just assume Farm Bureau knows all your needs. Proactively ask about all available discounts and benefits for members. Sometimes, simply asking if there are additional ways to save can uncover opportunities you weren’t aware of. Inquire about multi-product discounts if you’re also considering their insurance.

Common Mistakes to Avoid Are: Not comparing offers. While Farm Bureau offers excellent value, it’s always wise to get at least three to four loan offers from different lenders (e.g., another credit union, a bank) to ensure you’re getting the absolute best deal for your unique financial situation. Don’t feel pressured to take the first offer.

Real-World Scenarios and Expert Insights

To illustrate how Farm Bureau car loan rates can vary, let’s consider a few hypothetical scenarios. These examples, based on my extensive knowledge of the lending landscape, highlight the impact of different financial profiles.

-

Scenario A: The Prime Borrower (Excellent Credit, Large Down Payment)

- Profile: Credit score 780+, 25% down payment on a new car, stable income.

- Farm Bureau Outcome: This borrower would likely qualify for the most competitive Farm Bureau car loan rates, potentially matching or even beating top credit union offers. The low risk makes them a highly attractive client. They might also receive additional perks due to their strong financial standing.

- Expert Insight: For borrowers in this category, Farm Bureau provides not just competitive rates but often a superior customer service experience compared to larger, more impersonal lenders.

-

Scenario B: The Good Borrower (Good Credit, Average Down Payment)

- Profile: Credit score 680-720, 10-15% down payment on a used car, steady income.

- Farm Bureau Outcome: This borrower would still receive a very good rate, likely better than most traditional banks. While not the absolute lowest, the overall value proposition, including the potential for insurance bundling, would be highly attractive.

- Expert Insight: For individuals in this bracket, Farm Bureau’s commitment to members often shines, providing access to better rates than they might get elsewhere with a similar credit profile.

-

Scenario C: The Subprime Borrower (Fair Credit, Small Down Payment)

- Profile: Credit score 600-640, 5% down payment, some recent credit challenges.

- Farm Bureau Outcome: While the rate would be higher than for prime borrowers, Farm Bureau might still offer a more reasonable rate than a specialized subprime lender or a dealership with limited options. They may also be more willing to work with a member to improve terms over time.

- Expert Insight: Even with fair credit, Farm Bureau’s member-focused approach can sometimes offer a lifeline, providing a path to vehicle ownership that might be more expensive or inaccessible through other channels. It’s always worth exploring their options first.

Based on my experience, Farm Bureau often strikes a valuable balance between competitive rates and human-centered service. They are not just looking at your credit score; they are looking at you as a member of their community. This can make a significant difference, especially when you need a little more flexibility or understanding.

Final Thoughts: Is Farm Bureau the Right Choice for Your Car Loan?

Deciding on the best car loan involves weighing various factors, but for many, Farm Bureau car loan rates present a compelling argument. Their unique blend of competitive interest rates, exclusive member benefits, personalized local service, and a foundation of trust makes them a strong contender in the auto financing landscape.

If you’re already a Farm Bureau member, or if you’re considering joining, exploring their auto loan options is a highly recommended step. The potential for savings, combined with the convenience of managing multiple financial products under one trusted roof, can offer significant value. Remember to always compare offers, understand all the terms, and leverage your membership to secure the best possible deal for your next vehicle.

Conclusion

Navigating the world of car loans can feel overwhelming, but with the right information, you can make a choice that truly benefits your financial well-being. Farm Bureau car loan rates stand out as a valuable option for many, offering a blend of affordability and member-focused service that is often hard to beat. By understanding the factors that influence your rate, preparing thoroughly for the application process, and strategically comparing your options, you’ll be well-equipped to secure the best possible financing for your next car. Drive smart, save more, and enjoy the journey!

External Link: For general information on understanding car loan basics, you can consult reputable financial resources like Investopedia’s guide to auto loans. (Placeholder for external link)