Unlocking Wells Fargo Car Loan Rates: Your Ultimate Guide to Driving Away with the Best Deal

Unlocking Wells Fargo Car Loan Rates: Your Ultimate Guide to Driving Away with the Best Deal Carloan.Guidemechanic.com

The thrill of a new car – whether it’s the latest model or a reliable pre-owned vehicle – often comes with the practical step of securing financing. For many, a car loan is an essential bridge between desire and reality. Navigating the world of auto loans can feel complex, with various lenders, terms, and, most importantly, interest rates to consider.

Among the prominent players in the financial landscape, Wells Fargo stands out as a major provider of auto loans. If you’re considering financing your next vehicle through them, understanding Wells Fargo car loan rates is paramount. This comprehensive guide will demystify the process, explain what influences your rate, and equip you with the knowledge to secure the best possible deal. Let’s dive deep into making your car ownership dreams a smooth reality.

Unlocking Wells Fargo Car Loan Rates: Your Ultimate Guide to Driving Away with the Best Deal

Understanding Wells Fargo Car Loans: An Overview

Wells Fargo, a long-standing financial institution, offers a range of auto loan options designed to meet diverse borrower needs. They cater to individuals looking to finance new or used vehicles, as well as those interested in refinancing an existing car loan. Their extensive network and reputation make them a go-to choice for many prospective car buyers.

Choosing a lender like Wells Fargo often comes with the advantage of a well-established infrastructure. This includes accessible customer service, online application portals, and the potential for a streamlined process if you’re an existing bank customer. However, like any major lender, securing the best rate requires preparation and understanding.

Based on my experience, many borrowers appreciate Wells Fargo’s broad network and the convenience of managing multiple financial products under one roof. They offer both direct-to-consumer loans and indirect financing through dealerships, providing flexibility in how you apply. This dual approach means you can apply directly with Wells Fargo or inquire about their financing options when you’re at a dealership.

Demystifying Wells Fargo Car Loan Rates

At the heart of any car loan is the interest rate, which directly impacts the total cost of your vehicle. A "car loan rate" refers to the Annual Percentage Rate (APR) you’ll pay on the money borrowed. It’s not just the interest; the APR includes the interest rate plus any additional fees associated with the loan, providing a more accurate representation of the total borrowing cost.

Why do these rates fluctuate so much? Several dynamic factors are at play. General market conditions, influenced by the Federal Reserve’s monetary policy, play a significant role. When the Fed raises its benchmark interest rate, lenders typically follow suit, leading to higher auto loan rates across the board.

Pro tips from us: It’s crucial to understand that advertised rates are often starting points, typically reserved for borrowers with excellent credit scores. Your individual rate will be customized based on a personalized assessment of your financial profile and the specifics of the loan. Common mistakes people make are only looking at the advertised rate and assuming they will qualify for it without understanding the underlying criteria.

Factors That Influence Your Wells Fargo Car Loan Rate

Wells Fargo, like other lenders, evaluates several key factors to determine the car loan rate they offer you. Understanding these elements is your first step toward securing a favorable deal. Each component plays a vital role in assessing the risk associated with lending you money.

1. Your Credit Score

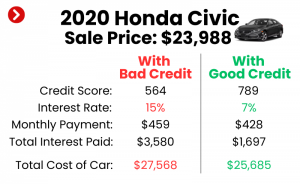

Your credit score is arguably the most critical factor influencing your car loan rate. It’s a numerical representation of your creditworthiness, reflecting your history of managing debt. Lenders use it to predict the likelihood of you repaying your loan on time.

Generally, FICO scores range from 300 to 850. Scores in the excellent (780-850) and very good (740-779) ranges typically qualify for the lowest interest rates. Good (670-739) and fair (580-669) scores will still get approved, but often with incrementally higher rates. If your score falls into the poor (below 580) category, you might face significantly higher rates or even require a co-signer.

Based on countless applications I’ve seen, a higher credit score is the single biggest determinant of securing a competitive interest rate. Lenders view borrowers with strong credit histories as lower risk, and they reward that reliability with better terms.

2. Your Debt-to-Income (DTI) Ratio

Your debt-to-income (DTI) ratio is another crucial metric Wells Fargo will assess. It compares your total monthly debt payments to your gross monthly income. This ratio indicates your ability to comfortably take on additional debt.

For instance, if your monthly gross income is $5,000 and your total monthly debt payments (including mortgage/rent, credit cards, student loans, etc.) are $1,500, your DTI would be 30% ($1,500 / $5,000). Lenders generally prefer a DTI ratio below 36-40%, though this can vary. A lower DTI suggests you have more disposable income to cover your car payments, making you a less risky borrower.

3. The Loan Term

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). This choice significantly impacts both your monthly payment and the total interest you’ll pay over the life of the loan.

While a longer term means lower monthly payments, it almost always translates to higher total interest over the loan’s life. This is because you’re paying interest for a longer period, and lenders often charge a slightly higher interest rate for extended terms due to increased risk. Conversely, shorter terms typically come with higher monthly payments but lower overall interest costs.

4. Vehicle Type (New vs. Used)

The type of vehicle you intend to finance also influences your interest rate. New cars often come with lower interest rates compared to used cars. Lenders perceive new vehicles as less risky because they haven’t depreciated as much, and their condition is guaranteed.

Used cars, on the other hand, typically carry slightly higher rates. This is due to factors like age, mileage, and potential for mechanical issues, which increase the lender’s risk. The older the used car, the higher the perceived risk, and potentially the higher the interest rate.

5. Your Down Payment

Making a substantial down payment can significantly impact your Wells Fargo car loan rate. A larger down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk. This reduced risk often translates into a more favorable interest rate.

Beyond the rate, a larger down payment also helps prevent you from being "upside down" on your loan, where you owe more than the car is worth. Many financial experts recommend a down payment of at least 20% for new cars and 10% for used cars, if possible.

6. Co-signer

If your credit score or DTI ratio isn’t ideal, adding a co-signer with strong credit can help you secure a better rate. A co-signer essentially guarantees the loan, taking on equal responsibility for repayment. This reduces the lender’s risk and can open doors to lower interest rates.

However, it’s crucial to understand the implications for the co-signer. If you fail to make payments, their credit will also be negatively impacted, and they will be legally obligated to cover the debt. This decision should always be made with full transparency and careful consideration for all parties involved.

7. Relationship with Wells Fargo

Sometimes, your existing relationship with Wells Fargo can play a subtle role. If you’re a long-time customer with other accounts like checking, savings, or a mortgage, the bank might be more inclined to offer you preferential rates or a smoother application process. This is because they have a broader view of your financial stability and loyalty.

While not a guarantee, maintaining a good banking relationship can sometimes provide a slight edge. It demonstrates a history of responsible financial management within their ecosystem.

The Wells Fargo Car Loan Application Process: A Step-by-Step Guide

Applying for a car loan, especially with a major lender like Wells Fargo, can be a straightforward process if you’re prepared. Knowing what to expect at each stage can alleviate stress and ensure you move efficiently toward securing your financing.

1. Pre-qualification or Pre-approval

From my professional vantage point, getting pre-approved is non-negotiable for smart car shopping. Pre-qualification gives you an estimate of what you might be approved for, often with a "soft" credit inquiry that doesn’t affect your score. Pre-approval is a more definitive offer, stating the maximum loan amount and estimated interest rate you qualify for, typically involving a "hard" credit inquiry.

Benefits of pre-approval include knowing your budget before stepping onto a dealership lot, which gives you significant negotiation power. You can focus on the car’s price, knowing your financing is already in place. It essentially turns you into a cash buyer in the eyes of the dealer.

2. Gathering Required Documents

Once you’re ready to apply, either for pre-approval or the final loan, you’ll need to gather several documents. This typically includes proof of income (pay stubs, tax returns), identification (driver’s license, Social Security number), proof of residency (utility bill), and details about the vehicle you intend to purchase (VIN, mileage, make, model). Having these ready streamlines the entire process.

3. Submitting Your Application

You can typically apply for a Wells Fargo car loan online, over the phone, or in person at a branch. The application will ask for personal information, employment details, income, and financial history. Be thorough and accurate to avoid delays.

After submitting, Wells Fargo will review your application, pulling your credit report and assessing all the factors discussed earlier. You might receive a decision quickly, sometimes within minutes for online applications, or it could take a few business days.

4. Reviewing the Loan Offer

If approved, Wells Fargo will present you with a loan offer detailing the loan amount, interest rate (APR), loan term, and monthly payment. This is a critical step where you need to carefully read and understand all the terms and conditions.

Common mistake: Many applicants rush this step, overlooking hidden fees or unfavorable terms. Pay close attention to the APR, as it includes all costs, not just the base interest rate. Also, confirm there are no prepayment penalties if you plan to pay off the loan early.

5. Finalizing the Loan

Once you’ve reviewed and are satisfied with the loan offer, you’ll sign the necessary paperwork. This legally binds you to the loan terms. Wells Fargo will then disburse the funds, either directly to you (for direct loans) or to the dealership (for indirect loans), allowing you to complete your vehicle purchase.

Strategies to Secure the Best Wells Fargo Car Loan Rate

Getting a car loan is more than just applying; it’s about strategizing to ensure you get the most favorable terms. By taking proactive steps, you can significantly improve your chances of securing a lower interest rate from Wells Fargo.

1. Improve Your Credit Score: This is fundamental. Before even applying, check your credit report for errors and work on improving your score. Pay bills on time, reduce existing debt, and avoid opening new credit accounts unnecessarily. For more detailed advice on boosting your credit score, check out our guide on .

2. Reduce Your Debt-to-Income (DTI) Ratio: If your DTI is high, consider paying down other debts before applying for a car loan. Even a small reduction in credit card balances can make a difference, signaling greater financial capacity to lenders.

3. Save for a Larger Down Payment: The more you can put down upfront, the less you need to borrow, and the lower your risk profile becomes. Aim for at least 10-20% of the vehicle’s price to see a noticeable impact on your rate.

4. Consider a Shorter Loan Term: If your budget allows, opting for a shorter loan term (e.g., 48 or 60 months instead of 72 or 84) often results in a lower interest rate. While monthly payments will be higher, you’ll pay significantly less in total interest over the life of the loan.

5. Shop Around and Compare Offers: Don’t just settle for the first offer you receive. Get quotes from Wells Fargo, other banks, credit unions, and even dealership financing departments. Comparing multiple offers within a short period (typically 14-45 days) will count as a single hard inquiry on your credit report, allowing you to find the best rate without further credit impact.

6. Negotiate: Armed with a pre-approval from Wells Fargo, you have a strong negotiating position. If a dealership offers financing, you can use your Wells Fargo pre-approval as leverage to get them to beat or match the rate.

Wells Fargo Car Loan Refinancing: Is It Right For You?

Sometimes, you might find yourself in a car loan with terms that no longer serve your best interests. Perhaps your credit score has significantly improved since you first bought the car, or interest rates have dropped across the market. In such cases, Wells Fargo car loan refinancing could be a smart move.

Refinancing involves taking out a new loan to pay off your existing car loan, ideally with more favorable terms. This can be particularly beneficial if you can secure a lower interest rate, which will reduce your monthly payments and the total amount of interest paid over the life of the loan.

Other reasons to consider refinancing include shortening your loan term to pay off the car faster, or extending it to lower your monthly payments if you’re experiencing financial strain. Wells Fargo offers refinancing options for eligible borrowers, and it’s worth exploring if your current loan no longer meets your needs. To learn more about auto loan refinancing in general, the Consumer Financial Protection Bureau offers excellent resources on their website. External Link: https://www.consumerfinance.gov/consumer-tools/auto-loans/

Common Mistakes to Avoid When Getting a Car Loan

Based on my years of observing borrowers, certain pitfalls consistently trip people up. Avoiding these common mistakes can save you money and stress.

- Not getting pre-approved: This leaves you at the mercy of dealership financing and removes your negotiation power.

- Focusing only on the monthly payment: While important, an artificially low monthly payment might hide a much longer term and significantly higher total interest. Always look at the total cost of the loan.

- Ignoring the total cost of the loan: Factor in interest, fees, and any additional charges. The lowest monthly payment isn’t always the cheapest option overall.

- Not reading the fine print: Loan documents can be complex, but understanding every clause, especially regarding fees, penalties, and terms, is crucial.

- Accepting the dealer’s first offer without comparison: Always compare any dealer financing offer with your pre-approval from Wells Fargo or other lenders.

Conclusion

Securing a car loan through Wells Fargo, or any lender, doesn’t have to be a daunting task. By understanding the intricate factors that influence your interest rate, preparing your finances, and approaching the application process strategically, you empower yourself to drive away with the best possible deal. Your credit score, debt-to-income ratio, loan term, and down payment are all key levers you can influence.

Wells Fargo, with its comprehensive offerings and established presence, can be a strong partner in your car buying journey. Remember, preparation is your most powerful tool. Get pre-approved, gather your documents, and compare offers diligently. This proactive approach ensures you not only get the car you want but also the most financially advantageous terms.

Take control of your car financing destiny. Research, prepare, and negotiate, and you’ll be well on your way to a smooth and affordable ride. If you’re still weighing your options between different lenders, our article on might provide further clarity as you make your final decision.