Unlocking Your "10 Apr Car Loan": A Comprehensive Guide to Smart Auto Financing by April 10th

Unlocking Your "10 Apr Car Loan": A Comprehensive Guide to Smart Auto Financing by April 10th Carloan.Guidemechanic.com

Securing a car loan can feel like navigating a complex maze, especially when you’re aiming for a specific timeframe. If you’re looking to secure your "10 Apr Car Loan" – meaning you want to finalize your vehicle financing around April 10th – you’re in a unique position. This period often brings a confluence of factors that savvy car buyers can leverage to their advantage. From strategic timing to meticulous preparation, understanding the nuances of auto financing can lead to better rates, more favorable terms, and a smoother overall experience.

This in-depth guide is designed to be your ultimate resource, transforming you from a hesitant applicant into an empowered car buyer. We’ll delve into every aspect of the car loan journey, ensuring you have all the knowledge needed to make the best decisions, specifically with your April 10th target in mind. Our goal is to provide real value, helping you secure an auto loan that fits your budget and lifestyle, with the highest chance of approval and excellent terms.

Unlocking Your "10 Apr Car Loan": A Comprehensive Guide to Smart Auto Financing by April 10th

Why "10 Apr Car Loan" is More Than Just a Date: Strategic Timing Matters

The specific timing of your car loan application, particularly around April 10th, isn’t just a random date. It can be a strategic window offering unique opportunities and considerations. Understanding these factors is the first step toward optimizing your "10 Apr Car Loan" experience.

Based on my experience in the auto finance industry, early April often presents a sweet spot for car purchases and loan applications. This period falls shortly after the end of the first fiscal quarter for many dealerships and lenders. This means there might be sales targets to meet, leading to more aggressive promotions and willingness to negotiate.

Furthermore, April is firmly within the tax refund season for many individuals. A significant tax refund can serve as a powerful down payment, drastically reducing the amount you need to borrow. This, in turn, can lower your monthly payments and the total interest paid over the life of the loan.

New model year vehicles also start to arrive on dealership lots around this time, or shortly thereafter. This often translates into dealerships offering attractive incentives and discounts on the outgoing model year inventory. Combining these vehicle discounts with favorable loan terms can lead to substantial savings.

The Foundations of a Strong "10 Apr Car Loan" Application: Pre-April 10th Prep

A successful car loan application, especially one targeted for April 10th, begins long before you step onto a dealership lot or apply online. Solid preparation is the cornerstone of securing favorable terms and ensuring a smooth process.

1. Deep Dive into Your Credit Score

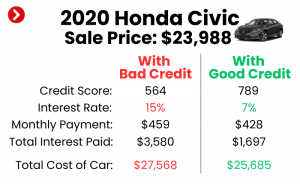

Your credit score is arguably the most critical factor influencing your car loan approval and the interest rate you’ll receive. Lenders use it to assess your creditworthiness and the risk associated with lending you money. A higher score signals less risk, leading to better offers.

Pro tips from us: Before even thinking about your "10 Apr Car Loan," pull your credit reports from all three major bureaus (Experian, Equifax, TransUnion). You can do this annually for free at AnnualCreditReport.com. Scrutinize these reports for any inaccuracies or errors. Disputing and correcting these can sometimes boost your score surprisingly quickly.

Beyond correcting errors, focus on improving your credit health. This involves consistently paying all your bills on time, every time. Reduce your credit utilization by paying down credit card balances. Avoid opening new lines of credit in the months leading up to your car loan application, as this can temporarily lower your score.

2. Budgeting for Your Car Loan: Beyond the Monthly Payment

Many prospective car buyers make the mistake of focusing solely on the monthly payment. While important, it’s only one piece of the financial puzzle. A truly smart "10 Apr Car Loan" decision requires a holistic view of affordability.

Start by calculating your total monthly vehicle budget. This includes not just the loan payment, but also insurance premiums, fuel costs, maintenance, and potential registration fees. These ancillary costs can significantly impact your overall financial health. Based on my experience, overlooking these often leads to buyer’s remorse down the line.

Consider the "20/4/10 rule" as a general guideline: aim for a 20% down payment, a loan term of no more than four years, and ensure your total monthly car expenses (loan, insurance, maintenance) don’t exceed 10% of your gross monthly income. While not always feasible for everyone, it’s a solid benchmark for financial prudence.

3. The Power of Your Down Payment

A substantial down payment is one of your most potent tools in securing an excellent "10 Apr Car Loan." It immediately reduces the principal amount you need to borrow, which directly translates to lower monthly payments and less interest paid over the loan term.

Lenders also view a larger down payment favorably. It signals your financial commitment and reduces their risk, often making them more willing to offer lower interest rates. If you’re receiving a tax refund around April, consider dedicating a good portion of it to your down payment. This can significantly strengthen your loan application.

Even a modest down payment can make a difference. Every dollar you put down upfront is a dollar you don’t pay interest on. It’s a direct investment in reducing your future financial burden.

Navigating the Car Loan Landscape: Types and Lenders for Your "10 Apr Car Loan"

Understanding the different types of car loans and the various lenders available is crucial for making an informed decision. Not all loans are created equal, and knowing your options can save you thousands over the life of your "10 Apr Car Loan."

1. Direct vs. Dealership Financing

When seeking your "10 Apr Car Loan," you essentially have two main avenues for financing:

- Direct Lending: This involves applying for a loan directly with banks, credit unions, or online lenders before you visit a dealership. The biggest advantage here is obtaining a pre-approval. This gives you a clear understanding of your budget and interest rate before you start shopping. It transforms you into a cash buyer in the eyes of the dealership, giving you significant leverage in price negotiations.

- Dealership Financing: Dealerships act as intermediaries, working with a network of lenders to find you a loan. While convenient, they often mark up the interest rate offered by the lender to make a profit. However, dealerships sometimes have access to special manufacturer incentives or promotional rates that direct lenders might not offer.

Pro tips from us: Always get a pre-approval from a direct lender first. Then, you can compare that offer with what the dealership can provide. This ensures you’re getting the best possible rate for your "10 Apr Car Loan."

2. New vs. Used Car Loans

The type of vehicle you choose impacts your loan terms. New car loans generally come with lower interest rates compared to used car loans. This is because new cars typically hold their value better initially and present less risk to the lender.

Used car loans, while often carrying higher rates, can still be a smart choice if you’re looking for a more affordable vehicle. The key is to ensure the used car is in good condition and priced appropriately for its age and mileage. Lenders may also impose age or mileage restrictions on used vehicles they will finance.

3. Refinancing Your "10 Apr Car Loan" (If Needed)

Perhaps you secured a "10 Apr Car Loan" under less-than-ideal circumstances, or your credit score has significantly improved since then. Refinancing can be a powerful tool to reduce your interest rate, lower your monthly payments, or even shorten your loan term.

Common mistakes to avoid are thinking your initial loan terms are set in stone. If market rates drop or your financial situation improves, revisit your loan. Many lenders offer refinancing options, and comparing them can lead to substantial long-term savings. This is particularly relevant if you rushed into your "10 Apr Car Loan" without proper preparation.

The Application Process: Step-by-Step Towards Your "10 Apr Car Loan"

Once you’ve done your homework, the application process itself becomes much smoother. Knowing what to expect and having your documents ready will expedite your "10 Apr Car Loan" approval.

1. Gathering Your Essential Documents

Lenders require specific documents to verify your identity, income, and financial stability. Having these ready will prevent delays.

Typically, you’ll need:

- Proof of identity (driver’s license, state ID).

- Proof of residence (utility bill, lease agreement).

- Proof of income (pay stubs, tax returns, bank statements).

- Social Security Number.

- Information about the vehicle you intend to purchase (if known).

Prepare a folder with both physical and digital copies of these documents. This readiness will streamline the process for your "10 Apr Car Loan."

2. The Power of Pre-Approval

As mentioned, pre-approval is a game-changer. It means a lender has reviewed your financial information and tentatively agreed to lend you a specific amount at a certain interest rate.

Based on my experience, many applicants overlook the power of pre-approval. It provides immense confidence and negotiation power. You know exactly what you can afford, and you walk into the dealership with your own financing ready, which often prompts them to try and beat your pre-approved rate.

It also protects you from getting emotionally invested in a car you can’t truly afford. With pre-approval, you shop for the vehicle, not for the loan.

3. Comparing Offers: Interest Rates, APR, and Terms

Never settle for the first loan offer you receive. Shop around! Apply to several direct lenders (banks, credit unions, online lenders) within a short window (typically 14-45 days). Multiple inquiries within this period are usually counted as a single hard inquiry on your credit report, minimizing the impact on your score.

When comparing offers for your "10 Apr Car Loan," look beyond just the interest rate. The Annual Percentage Rate (APR) includes the interest rate plus any fees, giving you a more accurate picture of the total cost of borrowing. Also, carefully consider the loan term. A longer term means lower monthly payments but significantly more interest paid over time. A shorter term means higher monthly payments but less overall interest.

4. Understanding the Fine Print

Before signing any document for your "10 Apr Car Loan," read everything. This includes the loan agreement, disclosure statements, and any additional warranties or add-ons.

Look out for:

- Prepayment Penalties: Some loans charge a fee if you pay off your loan early.

- Late Payment Fees: Understand the grace period and associated charges.

- Hidden Fees: Ensure there are no unexpected administrative or origination fees.

- Add-ons: Dealerships often try to sell extended warranties, GAP insurance, or other products. While some might be beneficial, ensure you understand their cost and whether they are truly necessary for your situation. You can often purchase these separately and often for less.

Don’t be afraid to ask questions. If something isn’t clear, demand clarification. It’s your right as a consumer to fully understand the terms of your "10 Apr Car Loan."

Beyond the Loan: Post-Approval & Ownership Considerations

Your "10 Apr Car Loan" journey doesn’t end when you sign the papers. There are ongoing responsibilities and considerations to ensure a smooth ownership experience.

1. Insurance Requirements

Before you can drive your new car off the lot, you’ll need to have adequate car insurance. Lenders typically require full coverage insurance (collision and comprehensive) to protect their investment.

Pro tips from us: Get insurance quotes before you finalize your purchase. Insurance costs can vary wildly based on the vehicle type, your driving history, and where you live. Factor this into your overall budget.

2. Registration and Titling

Once you’ve purchased the car and secured your "10 Apr Car Loan," the dealership usually handles the initial registration and titling process. However, it’s good to understand the steps involved. The title reflects ownership, and the registration allows you to legally operate the vehicle on public roads. Ensure all paperwork is correct and that you receive your official documents in due course.

3. Ongoing Loan Management

Making your payments on time is paramount. Set up automatic payments to avoid missing due dates and incurring late fees, which can also negatively impact your credit score.

Consider making extra payments whenever possible. Even small additional contributions can significantly reduce the total interest paid and shorten the loan term. For example, if your "10 Apr Car Loan" has a payment of $400, paying $450 each month can make a huge difference over five years.

Special Considerations for Your "10 Apr Car Loan"

The timing around April 10th offers specific advantages that can be capitalized upon.

1. Tax Refund Season Impact

As mentioned, early April is peak tax refund season. This presents a golden opportunity to strengthen your car loan application.

- Boost Your Down Payment: Use your refund to increase your down payment, reducing the loan amount and potentially securing a lower interest rate.

- Pay Down Other Debt: If you have high-interest debt, consider using your refund to pay it down. This improves your debt-to-income ratio, making you a more attractive borrower for your "10 Apr Car Loan."

- Create an Emergency Fund: A strong emergency fund provides financial stability, which can also indirectly support your loan application by demonstrating responsible financial management.

2. End-of-Quarter Deals for Dealerships

Many dealerships operate on quarterly sales targets. The end of March marks the close of the first quarter. This means by early April, dealerships might still be motivated to push sales to meet or exceed those targets, or to clear out lingering inventory from the previous quarter.

This can translate into more willingness to negotiate on vehicle prices, or even offer special financing incentives through their affiliated lenders. Being aware of this dynamic gives you an edge in negotiations for your "10 Apr Car Loan."

3. New Model Year Launches and Discounts

Automakers typically roll out new model years in the fall, but the effects ripple through the market well into spring. By April, dealerships are often looking to clear out remaining inventory of the previous year’s models.

This can mean significant discounts on cars that are technically "new" but are from the prior model year. If you’re flexible on having the absolute latest model, this can be a fantastic way to save money, making your "10 Apr Car Loan" go further.

Common Mistakes to Avoid When Securing Your "10 Apr Car Loan"

Even with all the preparation, it’s easy to fall into common pitfalls. Being aware of these can save you time, money, and stress.

- Not Checking Your Credit Score: This is fundamental. Without knowing your score, you’re going into negotiations blind. It’s like playing poker without knowing your hand.

- Ignoring the Total Cost of Ownership: As discussed, focusing only on the monthly payment is a recipe for financial strain. Factor in insurance, fuel, and maintenance.

- Only Getting One Loan Offer: This is perhaps the biggest mistake. Always shop around for the best rates. A difference of just one percentage point on a $30,000 loan can cost you hundreds, if not thousands, over the loan term.

- Rushing the Process: Don’t feel pressured to make a quick decision. Take your time, compare options, and read all documents thoroughly. A smart "10 Apr Car Loan" is a well-considered one.

- Not Understanding the Terms: If you don’t understand something in the loan agreement, ask. Don’t sign until you’re completely clear on all aspects of your financial commitment.

- Allowing Unnecessary Add-ons: Be firm about what you want and don’t want. Dealerships profit from selling extras. Only agree to what truly benefits you.

Frequently Asked Questions About Your "10 Apr Car Loan"

Q: Is April a good time to buy a car?

A: Yes, April can be a very good time to buy a car. It’s often during the tax refund season, which can boost your down payment. Additionally, it falls after the end of the first fiscal quarter for many dealerships, potentially leading to more aggressive sales goals and discounts on outgoing model year vehicles.

Q: How long does car loan approval take?

A: With good credit and all documents ready, pre-approval from an online lender can be as quick as a few minutes to a few hours. Traditional banks might take a day or two. At a dealership, approval can often happen on the spot if you have strong credit. However, always allow yourself ample time for shopping around and comparing offers, especially if aiming for a "10 Apr Car Loan."

Q: What credit score do I need for a car loan?

A: While you can get a car loan with various credit scores, generally, a score of 660 and above is considered "good" and will qualify you for more favorable rates. Excellent credit (780+) will get you the best rates. Scores below 600 might still get approved but often come with higher interest rates.

Q: Can I get a car loan with bad credit?

A: Yes, it’s possible to get a car loan with bad credit. However, you should expect higher interest rates and potentially stricter terms. To improve your chances, consider a larger down payment, a co-signer with good credit, or looking for specific lenders that specialize in bad credit auto loans. Always compare offers carefully.

Q: What is the difference between interest rate and APR?

A: The interest rate is the percentage charged on the principal amount of the loan. The Annual Percentage Rate (APR) is a broader measure of the cost of borrowing money, including the interest rate plus any additional fees or charges (like origination fees) associated with the loan. APR provides a more accurate picture of the total cost.

Conclusion: Driving Towards a Smart "10 Apr Car Loan"

Securing your "10 Apr Car Loan" doesn’t have to be a daunting task. By approaching the process with preparation, knowledge, and a strategic mindset, you can navigate the complexities of auto financing with confidence. From understanding the timing advantages of early April to meticulously preparing your finances and comparing loan offers, every step you take contributes to a more favorable outcome.

Remember, the goal isn’t just to get a car loan by April 10th, but to secure the best possible car loan for your unique situation. By following the insights and pro tips provided in this guide, you’re well-equipped to make informed decisions, avoid common pitfalls, and ultimately drive away with a vehicle and a loan that truly serves your needs. Start your preparation today and unlock the door to a smart "10 Apr Car Loan" experience!

Internal Link: – Learn more about boosting your creditworthiness.

Internal Link: – Explore different types of coverage and find the right policy for you.

External Link: – Get official guidance on auto loan best practices.