Unlocking Your $7500 Car Loan: A Comprehensive Guide to Approval and Smart Borrowing

Unlocking Your $7500 Car Loan: A Comprehensive Guide to Approval and Smart Borrowing Carloan.Guidemechanic.com

The open road beckons, and for many, a reliable vehicle is more than just transportation—it’s freedom, independence, and a vital part of daily life. Perhaps you’re eyeing a dependable used car, need a second family vehicle, or require a specific model for your commute. Whatever your reason, a $7500 car loan can be the perfect financial bridge to get you behind the wheel.

Navigating the world of car financing can feel daunting, especially when you’re looking for a specific loan amount like $7500. This comprehensive guide is designed to demystify the process, provide you with expert insights, and equip you with the knowledge to secure your $7500 car loan with confidence. We’ll explore everything from lender expectations to application strategies, ensuring you make informed decisions every step of the way.

Unlocking Your $7500 Car Loan: A Comprehensive Guide to Approval and Smart Borrowing

The $7500 Car Loan Landscape: What Does It Cover?

A $7500 car loan sits in a sweet spot for many budget-conscious buyers. It’s often the ideal amount for purchasing a quality used car, covering the gap for a substantial down payment on a newer model, or even financing a classic project car. This specific loan amount offers significant flexibility without the burden of a massive debt.

Typically, a loan of this size is perfect for reliable sedans, smaller SUVs, or compact cars that are a few years old. These vehicles often come with lower insurance costs and maintenance expenses, making them excellent choices for those seeking an affordable car loan. Understanding what $7500 can realistically get you is the first step toward a successful purchase.

Key Factors Lenders Consider for Your $7500 Car Loan

When you apply for a $7500 car loan, lenders aren’t just looking at the number. They’re assessing your overall financial health and your ability to repay the loan responsibly. Based on my experience in the lending sector, understanding these core factors is crucial for increasing your approval chances and securing favorable terms.

Your Credit Score: The Foundation of Trust

Your credit score is arguably the most critical piece of information lenders evaluate. It’s a three-digit number that summarizes your financial reliability. A higher score indicates a lower risk to lenders, often translating into better interest rates and easier approval for your $7500 car loan.

- What Lenders Look For: Generally, a credit score above 670 is considered "good," while scores above 740 are "very good" or "excellent." Even with a lower score, approval for a $7500 loan is possible, but you might face higher interest rates or require additional conditions.

- Pro Tips From Us: Before you even think about applying, get a free copy of your credit report from AnnualCreditReport.com. Review it for any errors and understand where you stand. This empowers you to address issues or set realistic expectations.

Income and Employment Stability: Can You Afford It?

Lenders need assurance that you have a consistent income stream to make your monthly payments. They’re not just looking at how much you earn, but also the stability of that income. A steady job history with the same employer for several years is a significant plus.

- Debt-to-Income Ratio (DTI): This crucial metric compares your total monthly debt payments to your gross monthly income. Lenders prefer a DTI ratio below 36%, though some might approve loans with a DTI up to 43%. A lower DTI means you have more disposable income to cover your new car payment.

- Common Mistakes to Avoid Are: Not accurately calculating your DTI before applying. Overstating your income or understating your existing debts can lead to application delays or outright rejection. Be honest and transparent to build trust.

Your Down Payment: Showing Your Commitment

While a $7500 loan might not always require a substantial down payment, making one can significantly strengthen your application. A down payment reduces the loan amount, thereby lowering the lender’s risk and potentially decreasing your monthly payments and total interest paid.

- Benefits of a Down Payment: Even a modest down payment of $500 to $1,000 shows financial discipline and commitment. It signals to the lender that you are invested in the purchase and less likely to default on the loan. For a $7500 car loan, a down payment makes the amount even more manageable for lenders.

Types of $7500 Car Loans Available

Understanding your options for a $7500 car loan is key to finding the best fit for your financial situation. While most car loans are secured, there are various sources and structures to consider.

Secured vs. Unsecured Loans

A car loan is almost always a secured loan, meaning the vehicle itself serves as collateral. If you fail to make payments, the lender has the right to repossess the car. This reduces the risk for the lender, which in turn can lead to more favorable interest rates for you. Unsecured loans, like personal loans, don’t require collateral but typically come with higher interest rates due to the increased risk for the lender.

Where to Find Your $7500 Car Loan

- Banks and Credit Unions:

- Pros: Often offer competitive interest rates, especially to existing customers. Credit unions are known for their customer-centric approach and can be more flexible.

- Cons: Application processes can sometimes be slower, and they might have stricter credit requirements compared to other lenders.

- Dealership Financing:

- Pros: Convenient "one-stop shop" experience. Dealers often work with multiple lenders, allowing them to shop around for you. They may also offer special promotions or incentives.

- Cons: Interest rates might not always be the most competitive, and there can be less transparency in the overall loan terms if you don’t do your homework.

- Online Lenders:

- Pros: Quick application and approval processes, often within minutes. Many specialize in various credit profiles, from excellent to fair, and can offer competitive rates.

- Cons: Less personal interaction. It’s crucial to research their reputation and read reviews before committing.

Choosing the right lender is as important as choosing the right car. For a deeper dive into this topic, you might find our article on "Choosing the Right Lender for Your Car Loan" helpful. (Note: Replace with a real internal link if available).

The Application Process for Your $7500 Car Loan: A Step-by-Step Guide

Securing your $7500 car loan doesn’t have to be complicated. Following a structured approach can make the process smooth and stress-free. Based on my experience, preparation is the ultimate key to success.

Step 1: Check Your Credit Report and Score

As mentioned earlier, this is your starting point. Request your free credit reports from all three major bureaus (Experian, Equifax, TransUnion) via AnnualCreditReport.com. Look for inaccuracies and understand your score. If you find errors, dispute them immediately as they can negatively impact your loan application.

Step 2: Determine Your Realistic Budget

A $7500 car loan is just one piece of the puzzle. Your budget needs to account for the total cost of car ownership. This includes:

-

Monthly Loan Payments: The principal and interest.

-

Car Insurance: Get quotes before buying.

-

Registration and Taxes: Varies by state.

-

Maintenance and Repairs: Set aside a fund for this.

-

Fuel Costs: Estimate based on your driving habits.

-

Pro Tips From Us: Don’t just focus on the monthly loan payment. A slightly higher payment might be worth it if it means a shorter loan term and less interest paid overall.

Step 3: Gather Necessary Documents

Being prepared with all required paperwork will expedite the application process. While specific documents may vary slightly by lender, you’ll generally need:

- Government-issued identification (Driver’s License, State ID)

- Proof of income (Pay stubs, W-2s, tax returns for self-employed)

- Proof of residence (Utility bill, lease agreement)

- Bank statements

- Social Security Number

Step 4: Get Pre-Approved for Your Loan

Pre-approval is a powerful tool. It means a lender has conditionally agreed to lend you a certain amount (in your case, up to $7500) at a specific interest rate, based on a preliminary review of your finances.

- Benefits of Pre-Approval:

- Know Your Budget: You’ll know exactly how much you can spend on a car.

- Negotiating Power: You walk into the dealership as a cash buyer, which gives you leverage.

- Rate Shopping: You can compare pre-approved offers from multiple lenders without multiple hard inquiries impacting your credit score.

- Common Mistakes to Avoid Are: Going to the dealership without any pre-approval. This puts you at a disadvantage and can lead to impulse decisions or less favorable loan terms.

Step 5: Shop for Your Car

With your pre-approval in hand and a clear budget, you can confidently shop for your vehicle. Focus on cars that fit your needs and fall within your approved loan amount. Test drive thoroughly and get a vehicle history report (like CarFax) for any used car you consider.

Step 6: Finalize the Loan and Purchase

Once you’ve found the perfect car, you’ll finalize the loan. Review all documents carefully, paying close attention to the interest rate (APR), loan term, and any additional fees. Ask questions until you understand every detail. Sign only when you are completely comfortable with the terms.

- Pro Tips From Us: Don’t feel pressured to sign immediately. Take a copy of the loan agreement home to review if possible, or have a trusted advisor look it over.

Boosting Your Chances of $7500 Car Loan Approval

Even if your credit isn’t perfect, there are proactive steps you can take to significantly improve your odds of securing a $7500 car loan. Based on my experience, these strategies often make the difference between approval and rejection.

Improve Your Credit Score

Even small improvements can have a big impact.

- Pay Bills On Time: This is the single most important factor. Set up reminders or automatic payments.

- Reduce Existing Debt: Pay down credit card balances to lower your credit utilization ratio.

- Avoid New Credit Applications: Don’t open new credit accounts in the months leading up to your car loan application, as this can temporarily lower your score.

Increase Your Down Payment

As discussed, a larger down payment reduces the amount you need to borrow and signals financial stability. Even an extra few hundred dollars can make your application more attractive to lenders for a $7500 loan.

Find a Co-Signer

If your credit score or income isn’t strong enough on its own, a co-signer with excellent credit and stable income can significantly boost your application. The co-signer essentially guarantees the loan, promising to make payments if you default.

- Important Note: A co-signer takes on equal responsibility for the loan. Both your and their credit will be affected by the loan’s payment history. Ensure both parties fully understand this commitment.

Choose the Right Vehicle

Lenders are more comfortable financing vehicles that retain their value and are easily resold if repossession becomes necessary. A reliable, well-maintained used car within a reasonable price range is generally less risky for a lender than a niche or excessively old vehicle.

Demonstrate Income Stability

Lenders appreciate consistency. If you’ve been at your job for a while, that’s a plus. If you’ve recently changed jobs, be prepared to explain the circumstances and show proof of consistent income over time. Based on my experience, a stable job history is gold for lenders. They want to see a reliable source of income that will continue throughout the loan term.

Smart Strategies for Managing Your $7500 Car Loan

Securing your $7500 car loan is a big step, but managing it wisely is equally important. Responsible loan management protects your credit and saves you money in the long run.

Understanding Your Loan Terms

Beyond the monthly payment, familiarize yourself with:

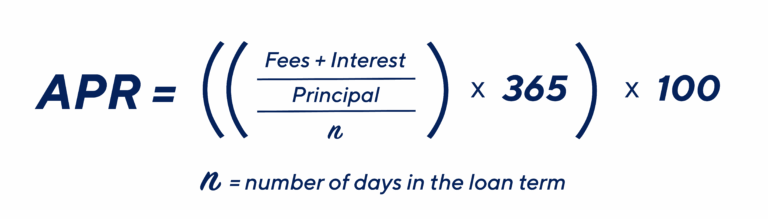

- Annual Percentage Rate (APR): This is the true cost of borrowing, including interest and some fees, expressed as an annual percentage. A lower APR means less total cost.

- Loan Term: The length of time you have to repay the loan (e.g., 36, 48, 60 months). Shorter terms usually mean higher monthly payments but less interest paid overall.

- Total Cost of Loan: Calculate the sum of all monthly payments plus any upfront fees to understand the total financial commitment.

Making Payments On Time

This cannot be stressed enough. On-time payments are crucial for:

- Building Positive Credit History: This improves your credit score, making future borrowing easier and cheaper.

- Avoiding Late Fees: These fees can quickly add up and increase your loan’s cost.

- Preventing Default: Missing payments can lead to vehicle repossession and severe damage to your credit.

Consider Early Payoff

If your budget allows, making extra payments or paying off your $7500 car loan early can save you a significant amount in interest, especially if your loan has a higher APR. Always check your loan agreement for any prepayment penalties, though these are rare for car loans.

Refinancing Options

If your credit score has improved since you first took out your loan, or if interest rates have dropped, you might be able to refinance your $7500 car loan. Refinancing can lead to a lower interest rate, a reduced monthly payment, or a shorter loan term. It’s always worth exploring if your financial situation has improved. For more detailed information on managing various types of debt, you can refer to trusted financial resources like the Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov.

Common Pitfalls and How to Avoid Them

Even with the best intentions, borrowers can sometimes fall into traps. Being aware of these common mistakes will help you navigate your $7500 car loan journey successfully.

- Ignoring Your Credit Score: Not knowing your credit standing before applying can lead to rejections or surprisingly high interest rates. Always check your score first.

- Not Budgeting for Total Ownership Costs: Focusing solely on the monthly payment without considering insurance, maintenance, and fuel is a common pitfall. This can lead to financial strain down the road.

- Settling for the First Offer: Always shop around for your loan. Getting quotes from multiple lenders ensures you’re getting the most competitive rate and terms available to you.

- Misunderstanding Loan Terms: Rushing through the loan agreement and not asking questions about the APR, loan term, or any hidden fees can be costly. Read every line carefully.

- Common Mistakes to Avoid Are: Falling for "buy here, pay here" dealerships without understanding their typically higher interest rates and less flexible terms, especially if you have other options.

Your Journey to a $7500 Car Loan: The Road Ahead

Securing a $7500 car loan is a significant financial step that can open up new possibilities. By taking the time to understand the lending landscape, preparing your finances, and approaching the application process strategically, you significantly increase your chances of approval and secure favorable terms.

Remember, knowledge is power. Armed with the insights from this comprehensive guide, you are well-equipped to make informed decisions, avoid common pitfalls, and confidently navigate your way to owning the vehicle you need. Start your car loan journey today with confidence, knowing you have a clear roadmap to success.