Unlocking Your Auto Loan: The Ultimate Guide to Understanding Your Car Loan Schedule

Unlocking Your Auto Loan: The Ultimate Guide to Understanding Your Car Loan Schedule Carloan.Guidemechanic.com

Buying a car is an exciting milestone, a significant investment that often involves securing a car loan. While the thrill of driving off the lot in your new vehicle is undeniable, many drivers overlook one of the most crucial documents in their auto finance journey: the car loan schedule. This isn’t just a boring piece of paper; it’s the financial roadmap to owning your car outright.

Based on my experience working with countless car buyers and financial institutions, truly understanding your car loan schedule is the difference between simply making payments and strategically managing your debt. This comprehensive guide will demystify every aspect of your auto loan’s payment breakdown, empowering you to make smarter financial decisions and potentially save a substantial amount of money over the life of your loan. Let’s dive deep into the numbers that define your ride!

Unlocking Your Auto Loan: The Ultimate Guide to Understanding Your Car Loan Schedule

What Exactly Is a Car Loan Schedule? The Foundation of Your Auto Finance

At its core, a car loan schedule, often referred to as an amortization schedule, is a detailed table that breaks down each and every payment you’ll make on your auto loan. It’s more than just knowing your monthly payment; it shows you precisely how much of each payment goes towards the principal balance and how much covers the interest charged by the lender.

Think of it as a transparent ledger for your car debt. Each line item on this schedule typically lists the payment number, the date it’s due, the total payment amount, the portion of that payment allocated to interest, the portion allocated to principal, and your remaining loan balance after that payment is applied. It’s the ultimate tool for tracking your progress towards full ownership.

For many car owners, the monthly payment is the only figure they focus on. However, understanding the intricate details within your car loan schedule provides an unparalleled level of clarity and control. It reveals the true cost of borrowing and illuminates opportunities to accelerate your debt repayment, a strategy often overlooked by the average borrower.

Key Components That Shape Your Car Loan Schedule

To truly master your auto loan, you need to grasp the individual elements that construct its payment schedule. These components are interconnected, each playing a vital role in determining your monthly payment and the total cost of your loan.

1. The Principal Amount: Your Core Debt

The principal amount is the actual sum of money you borrow to purchase your car. This is the starting point of your debt journey, representing the vehicle’s price minus any down payment or trade-in value you’ve applied. It’s the "real" money you owe.

Every payment you make contributes to reducing this principal balance, albeit slowly at first. A larger principal means a larger initial debt to tackle, directly impacting your monthly payments and the total interest you’ll accrue over the loan term. Strategically, a higher down payment directly reduces this principal, immediately lowering your overall financial burden.

2. The Interest Rate (APR): The Cost of Borrowing

Your interest rate, often expressed as an Annual Percentage Rate (APR), is the fee your lender charges you for borrowing their money. It’s usually represented as a percentage and is applied to your outstanding principal balance. This is the "profit" for the lender.

The APR is a critical factor in your car loan schedule because it dictates how much extra you’ll pay beyond the car’s sticker price. A higher APR means a greater portion of your early payments will go towards interest, making it slower to chip away at the principal. Factors like your credit score, the loan term, and the current market rates significantly influence the APR you qualify for.

3. The Loan Term: How Long You’ll Pay

The loan term is the duration, typically expressed in months, over which you agree to repay your car loan. Common terms range from 36 months (3 years) to 72 months (6 years), or even longer. This choice profoundly impacts your monthly payment and the total interest paid.

A shorter loan term generally means higher monthly payments but significantly less interest paid over the life of the loan. Conversely, a longer loan term offers lower monthly payments, making the car more "affordable" on a month-to-month basis, but you’ll pay substantially more in interest overall. Based on my experience, finding the right balance between affordability and minimizing interest is key to smart auto financing.

4. The Monthly Payment: Your Regular Obligation

This is the fixed amount you pay to your lender each month until the loan is fully repaid. Your monthly payment is calculated based on the principal amount, the interest rate, and the loan term. It’s the most visible part of your car loan schedule.

While the total monthly payment remains constant, the allocation within that payment changes over time. Initially, a larger chunk goes towards interest, while later payments allocate more towards reducing your principal. Understanding this shifting dynamic is fundamental to leveraging your car loan schedule effectively.

5. Amortization: The Magic Behind the Numbers

Amortization is the process of paying off debt over time through regular, equal payments. For a car loan, it means that with each monthly payment, a portion goes to cover the interest accrued, and the remainder reduces the principal balance. This isn’t a static split.

The core principle of amortization for car loans is that more interest is paid at the beginning of the loan term, and more principal is paid towards the end. This is because interest is always calculated on the current outstanding principal balance. As your principal balance decreases with each payment, the interest portion of subsequent payments also decreases, allowing more of your payment to go towards the principal. Pro tips from us: This is why making extra principal payments early in the loan can have a dramatic impact on your total interest paid.

How to Read and Interpret Your Car Loan Schedule

Once you receive your car loan schedule, don’t just file it away. Take the time to understand what each column represents. It’s a powerful tool for financial planning.

Typically, your schedule will feature columns like:

- Payment Number: A sequential count of your payments.

- Payment Date: The specific date each payment is due.

- Beginning Balance: Your outstanding principal before the current payment.

- Monthly Payment: The fixed amount you’re paying.

- Interest Paid: The portion of your payment covering interest for that period.

- Principal Paid: The portion of your payment reducing your core debt.

- Ending Balance: Your outstanding principal after the current payment.

When you look at the initial payments, you’ll notice a significant portion going towards "Interest Paid" and a smaller amount to "Principal Paid." As you move down the schedule, you’ll see a gradual shift. The "Interest Paid" amount slowly decreases, while the "Principal Paid" amount steadily increases. This is the amortization process in action.

Common mistakes to avoid are just glancing at the total payment without understanding its components. Many people assume their payments are evenly split between principal and interest, which is rarely the case, especially early on. By observing this shift, you gain crucial insight into how your money is being allocated and how quickly you’re building equity in your vehicle.

The Power of Understanding Your Amortization Schedule

Grasping the intricacies of your car loan schedule goes far beyond simple tracking. It unlocks several strategic financial advantages.

1. Budgeting and Financial Planning with Precision

Knowing exactly how much of your payment goes to interest versus principal allows for more precise budgeting. You understand the true cost of your car each month, not just the sticker price. This clarity empowers you to allocate funds effectively, ensuring you’re not just making payments but actively managing your debt.

Furthermore, a detailed schedule helps you visualize your debt reduction progress, which can be a powerful motivator. It integrates seamlessly into your broader financial plan, helping you assess your liquidity and long-term financial goals.

2. Strategic Extra Payments: Saving on Interest

One of the most impactful benefits of understanding your car loan schedule is the ability to make strategic extra payments. Since interest is calculated on your outstanding principal balance, any additional money you pay directly to principal reduces that balance faster. This, in turn, reduces the amount of interest you’ll be charged on all subsequent payments.

Based on my experience, even small, consistent extra payments, when designated specifically for principal reduction, can shave months off your loan term and save hundreds, if not thousands, of dollars in interest. The car loan schedule clearly illustrates this potential savings by showing you the declining interest amounts.

3. Early Payoff Strategies: Is It Right for You?

The car loan schedule is your go-to document if you’re considering an early payoff. By looking at the "Ending Balance" column, you can quickly identify the exact amount needed to pay off your loan at any given point. This allows you to calculate the total interest saved by paying off early.

While an early payoff can be a smart move to save on interest and free up monthly cash flow, it’s important to weigh it against other financial priorities, such as high-interest credit card debt or investment opportunities. Your car loan schedule provides the data needed to make an informed decision. For more insights on this, you might find our article on helpful.

4. Refinancing Decisions: When and Why the Schedule Helps

If you’re considering refinancing your car loan, your current car loan schedule is indispensable. It shows you exactly how much principal you’ve paid down and what your current interest rate is. This information is crucial when comparing a new loan offer.

You can use the schedule to calculate how much interest you’ve already paid and project future interest costs under your current loan. Then, compare that with a potential new schedule from a refinanced loan with a lower interest rate or different term. This comparison helps you determine if refinancing will truly save you money or if you’re too far into your current loan for it to be worthwhile.

Creating Your Own Car Loan Schedule (Even Without the Lender’s Document)

What if your lender doesn’t provide a detailed car loan schedule, or you want to compare different loan scenarios before committing? You can easily create one yourself using online amortization calculators. These tools allow you to input the principal amount, interest rate, and loan term, and they instantly generate a full payment schedule.

While the exact formula can be complex (P * / ), online calculators handle the math for you. They are invaluable for understanding how different interest rates or loan terms will impact your monthly payments and total interest paid. This proactive approach helps you negotiate better deals and choose the best loan for your financial situation.

Factors That Influence Your Car Loan Schedule

Several variables contribute to the specific details of your car loan schedule. Being aware of these can help you secure more favorable terms.

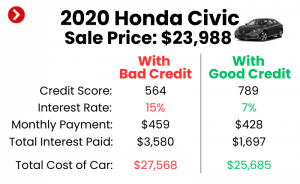

- Credit Score: A higher credit score signals lower risk to lenders, often resulting in a lower interest rate and thus a more favorable car loan schedule with less interest paid.

- Down Payment: A larger down payment directly reduces the principal amount borrowed, leading to lower monthly payments and significantly less interest over the loan’s life.

- Trade-in Value: Similar to a down payment, a valuable trade-in reduces the amount you need to finance, improving your car loan schedule.

- Loan Term: As discussed, the length of your loan directly impacts both your monthly payment amount and the total interest you’ll accrue.

- Interest Rate (APR): This is arguably the most critical factor, as it determines the cost of borrowing. Even a slight difference in APR can translate to hundreds or thousands of dollars over the loan term.

- Additional Fees/Taxes: While not part of the principal and interest calculation, fees like documentation fees, registration, and sales tax can increase the overall cost, sometimes even rolled into the financed amount, subtly affecting your schedule.

Pro Tips for Optimizing Your Car Loan Schedule

Now that you understand the mechanics, let’s look at actionable strategies to make your car loan schedule work for you, not against you.

- Negotiate the Best Interest Rate: Before signing any loan documents, shop around. Get quotes from multiple lenders, including banks, credit unions, and online lenders. A lower APR directly translates to less interest paid over the life of your loan. You can learn more about this by reading our article on .

- Consider a Larger Down Payment: If feasible, a substantial down payment reduces your principal, lowering both your monthly payment and total interest. It also creates a buffer against depreciation.

- Choose the Right Loan Term for Your Budget: While longer terms offer lower monthly payments, they come with a higher overall interest cost. Opt for the shortest loan term you can comfortably afford to minimize total interest paid.

- Make Extra Principal Payments Consistently: Even an extra $25 or $50 added to your principal each month can significantly shorten your loan term and save you money. Always specify that the extra amount should go towards principal.

- Regularly Review Your Financial Situation: Your financial health can change. If your credit improves or interest rates drop, refinancing might be a smart move to get a more favorable car loan schedule.

- Avoid Rolling Over Negative Equity: If you’re trading in a car that you owe more on than it’s worth (negative equity), avoid rolling that into your new car loan. This immediately puts you underwater and negatively impacts your new car loan schedule.

Common Misconceptions About Car Loan Schedules

Let’s clear up some widespread misunderstandings that can cost you money. Common mistakes to avoid are believing these myths:

- "All my payments go to principal first." This is almost never true for standard amortized loans. As we’ve seen, interest takes a larger share of early payments. Understanding this helps you make smarter decisions about extra payments.

- "Paying off early always saves a lot of money." While generally true, the actual savings depend on how far along you are in your loan. The most significant interest savings come from paying extra early in the loan term. If you’re nearing the end, the impact will be less dramatic.

- "My monthly payment is all I need to worry about." Focusing solely on the monthly payment can lead to choosing longer loan terms with lower payments but much higher overall interest costs. Always consider the total cost of the loan.

- "I don’t need to look at the schedule, the lender handles it." Relying solely on the lender means you miss opportunities to strategically manage your debt. Your car loan schedule is your personal financial tool.

When Things Change: Adjusting Your Car Loan Schedule

Life is unpredictable, and sometimes your financial situation or goals change. Your car loan schedule isn’t set in stone.

- Refinancing: If interest rates drop or your credit score improves, refinancing your car loan can provide a new, more favorable schedule. This could mean a lower monthly payment, a shorter loan term, or a reduced total interest cost.

- Selling the Car: If you decide to sell your car before the loan is paid off, your car loan schedule will show you the exact payoff amount needed to clear the debt. This is crucial for determining your selling price.

- Dealing with Financial Hardship: In difficult times, lenders may offer options like deferment or forbearance, temporarily altering your payment schedule. While these can provide relief, they often extend the loan term and increase total interest, so understand the full implications.

Conclusion: Take Control of Your Car Loan Schedule

The car loan schedule is far more than just a list of numbers; it’s a powerful financial blueprint for your auto ownership. By understanding its components – the principal, interest rate, loan term, and the magic of amortization – you transform from a passive payer into an active manager of your debt.

Armed with this knowledge, you can make informed decisions, optimize your payments, strategically save on interest, and ultimately achieve financial freedom faster. Don’t let your car loan schedule remain a mystery. Take the time to understand it, embrace its insights, and drive confidently towards owning your vehicle, free and clear. It’s your money, your car, and your financial future to control. For further details and general financial advice, the Consumer Financial Protection Bureau (CFPB) offers excellent resources on auto loans at .