Unlocking Your Car Loan APR: The Definitive Guide to Understanding Your Borrowing Costs

Unlocking Your Car Loan APR: The Definitive Guide to Understanding Your Borrowing Costs Carloan.Guidemechanic.com

Navigating the world of car financing can feel like deciphering a complex code, with terms like "APR," "interest rate," and "loan term" often causing confusion. Yet, understanding these concepts is crucial for making a smart financial decision when purchasing a vehicle. Among them, your car loan’s Annual Percentage Rate (APR) stands out as arguably the most vital figure, as it truly represents the total cost of borrowing.

As an expert blogger and SEO content writer with years of experience in personal finance, I’ve seen firsthand how a lack of understanding about APR can lead consumers to pay thousands more than necessary over the life of their car loan. This comprehensive guide is designed to demystify "What Would My APR Be On A Car Loan," breaking down every factor that influences it, how to estimate it, and most importantly, how to secure the best possible rate. Our ultimate goal is to empower you with the knowledge to approach your next car purchase with confidence and financial savvy.

Unlocking Your Car Loan APR: The Definitive Guide to Understanding Your Borrowing Costs

What Exactly Is APR on a Car Loan? Beyond Just the Interest Rate

When you’re asking, "What would my APR be on a car loan?", it’s essential to understand that APR is far more than just the interest rate. While the interest rate is a core component, the Annual Percentage Rate provides a holistic view of the annual cost of borrowing money. It encompasses not only the interest charged by the lender but also various other fees associated with the loan.

Think of the interest rate as the base price for borrowing money, expressed as a percentage of the principal loan amount. This is the direct cost the lender charges for the use of their funds. However, there are often administrative costs and other charges involved in setting up and managing a loan.

The APR wraps all these additional costs into a single, annualized percentage. These might include origination fees, documentation fees, processing fees, or even certain insurance premiums required by the lender. By consolidating these charges, the APR gives you a standardized metric to compare different loan offers, allowing for a more accurate assessment of the true expense of your financing.

This distinction is incredibly important because two lenders might offer seemingly similar interest rates, but their APRs could differ significantly due to varying fees. Always look at the APR when comparing loan options, as it offers the most transparent picture of your total borrowing expense. Ignoring this could lead you to choose a loan that appears cheaper upfront but costs more in the long run.

The Key Factors That Dictate Your Car Loan APR

Your car loan APR is not a one-size-fits-all number. It’s a highly personalized figure influenced by a confluence of variables. Understanding these factors is the first step in knowing "what would my APR be on a car loan" and, more importantly, how you can work towards securing a more favorable rate.

Your Credit Score: The Undisputed King of Influence

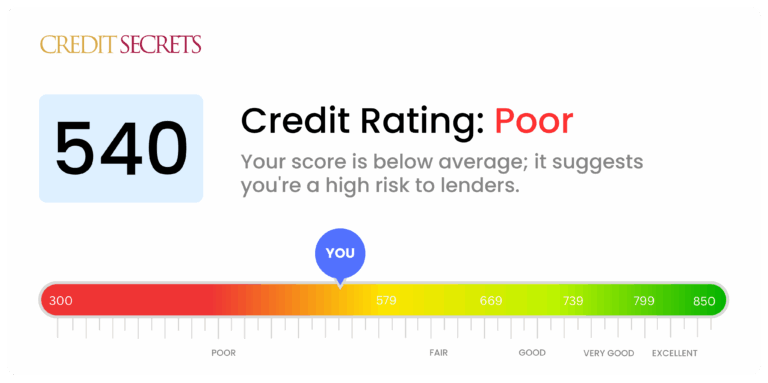

Without a doubt, your credit score is the single most significant determinant of your car loan APR. Lenders use your credit score as a primary indicator of your creditworthiness – essentially, how likely you are to repay the loan on time. A higher credit score signals lower risk to lenders, making them more willing to offer you a lower interest rate and, consequently, a lower APR.

Credit scores, like FICO and VantageScore, typically range from 300 to 850. Generally, scores above 780 are considered excellent, 670-739 are good, 580-669 are fair, and below 580 are poor. Based on my experience, someone with an excellent credit score could see APRs as low as 3-5%, while someone with a fair or poor score might face APRs in the double digits, sometimes exceeding 15% or even 20%, depending on the market and lender.

It’s not just about having a high score; lenders also look at the components that make up your score, such as your payment history, the amount of debt you owe, the length of your credit history, and your credit mix. A history of consistent, on-time payments across various credit accounts demonstrates reliability, which lenders highly value when assessing your loan application.

Your Debt-to-Income (DTI) Ratio: A Measure of Your Financial Capacity

Another critical factor lenders consider is your Debt-to-Income (DTI) ratio. This ratio compares your total monthly debt payments to your gross monthly income. For instance, if your total monthly debt payments (including rent/mortgage, credit card minimums, student loans, and existing car payments) are $1,500 and your gross monthly income is $4,000, your DTI ratio would be 37.5% ($1,500 / $4,000).

Lenders use your DTI to assess your ability to take on additional debt, like a new car loan, without becoming overextended. A lower DTI ratio indicates that you have more disposable income available to cover your new loan payments, which reduces the perceived risk for the lender. Pro tips from us: Aim for a DTI ratio below 36%, with some lenders preferring it even lower, especially for the best rates. A high DTI can signal financial strain, potentially leading to a higher APR or even a loan denial, even if your credit score is decent.

Loan Term (Length of the Loan): The Trade-off Between Monthly Payment and Total Cost

The length of your car loan, often expressed in months (e.g., 36, 48, 60, 72, or even 84 months), significantly impacts your APR. Generally, shorter loan terms come with lower APRs. This is because a shorter term means the lender gets their money back sooner, reducing their risk exposure to potential market changes or your financial circumstances deteriorating over time.

While a longer loan term will result in lower monthly payments, which can be very appealing, it almost always comes with a higher APR. This means you’ll pay more in total interest over the life of the loan. Common mistakes to avoid are focusing solely on the monthly payment without considering the overall cost and the higher APR associated with extended terms. A 72-month loan might seem more affordable each month than a 48-month loan, but the cumulative interest paid, driven by a higher APR, could be substantially greater.

Down Payment Amount: Reducing Risk and Your Loan Principal

The size of your down payment plays a crucial role in determining your APR. A larger down payment reduces the amount you need to borrow, which in turn reduces the lender’s risk. If you put down a substantial amount, you’re less likely to be "upside down" on your loan (owing more than the car is worth) early in the loan term, especially given vehicle depreciation.

Lenders view a significant down payment as a sign of financial stability and commitment. Consequently, they are often willing to offer a lower APR to borrowers who make a larger upfront investment. Pro tips from us: Aim for at least 10-20% of the vehicle’s purchase price as a down payment. This not only can lower your APR but also reduces your monthly payments and the total amount of interest you’ll pay over the life of the loan.

Vehicle Type and Age: Depreciation and Resale Value

The type and age of the vehicle you intend to purchase can also influence your APR. Newer cars, especially those with strong resale values, generally pose less risk to lenders. If you default, the lender can repossess and sell the vehicle to recoup their losses. A newer, more desirable car will likely fetch a better price at auction.

Conversely, older used cars, particularly those with high mileage or a history of reliability issues, might come with higher APRs. This is because they depreciate more rapidly and can be harder to resell if repossessed, increasing the lender’s risk. Luxury vehicles, while often expensive, might also be subject to different lending criteria and potentially higher APRs due to their specialized market and higher repair costs.

Current Market Interest Rates: The Economic Climate

Your car loan APR is also subject to the broader economic environment, specifically the prevailing market interest rates. These rates are heavily influenced by the Federal Reserve’s monetary policy. When the Fed raises its benchmark interest rate, it typically leads to higher borrowing costs across the board, including car loans.

Conversely, during periods of economic slowdown, the Fed might lower rates to stimulate borrowing and spending, which can translate into lower APRs for consumers. While this factor is largely out of your control, being aware of the current economic climate can help you anticipate "what would my APR be on a car loan" and when might be a good time to buy.

Lender Type: Banks, Credit Unions, Dealerships, and Online Lenders

Different types of lenders offer varying APRs and loan terms. Traditional banks, credit unions, dealership financing (captive lenders like Ford Credit or Toyota Financial Services), and online lenders all have their own criteria and risk assessments.

- Credit Unions are often known for offering some of the most competitive APRs because they are non-profit organizations focused on their members.

- Banks offer a wide range of rates, often depending on your relationship with them.

- Dealership financing can be convenient but may not always offer the best rates unless there are special manufacturer incentives.

- Online lenders have become increasingly popular, often providing quick approvals and competitive rates, especially for those with good credit.

Shopping around with multiple lender types is a pro tip that can uncover significant savings on your APR.

Co-signer: Sharing the Risk, Sharing the Benefits

If your credit score or DTI ratio isn’t strong enough to secure a favorable APR on your own, a co-signer might be an option. A co-signer, typically someone with excellent credit, agrees to be equally responsible for the loan. Their good credit history and financial stability can help you qualify for a lower APR.

However, using a co-signer comes with significant risks for both parties. If you miss payments, it negatively impacts both your credit scores, and the co-signer is legally obligated to make those payments. It’s a serious commitment that should only be undertaken with clear communication and a solid repayment plan.

How to Estimate Your Car Loan APR (and Get the Best Rate)

Understanding the factors that influence your APR is one thing, but actively working to secure the best rate is another. Here’s a step-by-step guide on how to estimate "what would my APR be on a car loan" and position yourself for the most favorable terms.

1. Check Your Credit Score First

Before you even step foot in a dealership or apply for a loan, know where you stand. Access your credit report and score from one of the three major credit bureaus (Experian, Equifax, TransUnion) or through services like Credit Karma. This gives you a realistic expectation of the APRs you might qualify for. If your score is lower than you’d like, you might consider delaying your purchase to improve it. For more detailed guidance, see our article: .

Knowing your score allows you to identify any errors on your report that could be unfairly dragging it down. Disputing and correcting these errors can quickly boost your score. It also helps you understand the general APR range you can expect, preventing you from being surprised or taken advantage of by lenders.

2. Get Pre-Approved from Multiple Lenders

This is perhaps the most powerful tool in your arsenal. Pre-approval involves applying for a loan with various lenders (banks, credit unions, online lenders) before you even choose a car. Each lender will provide you with a conditional loan offer, including an estimated APR, based on your financial profile.

Getting pre-approved has several benefits. First, it gives you a concrete idea of "what would my APR be on a car loan" with different institutions, allowing you to compare offers side-by-side. Second, it provides you with negotiating power at the dealership. You walk in knowing the best rate you’ve already secured, so the dealership has to beat or match it. Importantly, multiple loan applications within a short window (typically 14-45 days) are usually counted as a single inquiry on your credit report, minimizing the impact.

3. Shop Around – Don’t Settle for the First Offer

Based on my experience, one of the common mistakes consumers make is accepting the financing offered by the dealership without exploring other options. While dealership financing can sometimes be competitive, especially with manufacturer incentives, it’s rarely the only or best option.

Always compare the pre-approved offers you’ve received with any financing presented by the dealership. This comparison ensures you’re getting the most competitive APR. Remember, even a percentage point difference in APR can save you hundreds, if not thousands, of dollars over the life of the loan.

4. Calculate Your Debt-to-Income Ratio

While lenders will calculate your DTI, doing it yourself beforehand provides valuable insight. If your DTI is high, you might consider paying down other debts before applying for a car loan. Reducing your DTI can significantly improve your chances of securing a lower APR, as it demonstrates to lenders that you have sufficient capacity to handle new debt obligations.

Understanding your DTI empowers you to make informed decisions about how much car you can truly afford without overextending your finances. It’s a proactive step that can lead to better loan terms.

5. Consider a Larger Down Payment

As discussed, a larger down payment reduces the principal loan amount and signals financial stability to lenders. If you have savings, deploying a more substantial down payment is one of the most effective ways to lower your APR and your overall borrowing costs.

Even an extra few hundred or thousand dollars can make a noticeable difference in the APR offered and the total interest you’ll pay. It also helps you build equity in your car faster and reduces the risk of being upside down on your loan.

6. Opt for a Shorter Loan Term (If Affordable)

While lower monthly payments can be tempting, resist the urge to automatically choose the longest loan term available. If your budget allows, opting for a shorter loan term (e.g., 48 or 60 months instead of 72 or 84) will almost always result in a lower APR and significantly less total interest paid.

Balance your monthly budget with the long-term cost. A slightly higher monthly payment for a shorter duration could save you a substantial amount of money in interest over the life of the loan, especially if it leads to a lower APR.

Understanding the Fine Print: Beyond the APR

While the APR is the most comprehensive measure of your borrowing cost, it’s crucial to understand that not every cost associated with your loan is included in the APR calculation. Common mistakes to avoid are assuming the APR covers every single potential expense.

For instance, late payment fees, returned check fees, or even prepayment penalties (though less common in car loans today) are typically not factored into the initial APR. These are contingent fees that only apply if you fail to meet your loan obligations or make specific financial choices. Always read the entire loan agreement to understand all potential charges.

Additionally, lenders might require specific types of insurance, such as gap insurance, which protects you if your car is totaled and you owe more than its market value. While this isn’t part of the APR, it’s an additional cost of ownership tied to your financing. For a deeper dive into understanding loan disclosures, the Consumer Financial Protection Bureau (CFPB) offers excellent resources:

Common Mistakes to Avoid When Applying for a Car Loan

Based on my experience, many consumers make avoidable errors that cost them significantly when financing a car. Steering clear of these pitfalls can help you secure a better APR and a more favorable loan.

- Not Checking Your Credit Score: Going into a loan application blind is a major disadvantage. Know your score, dispute errors, and understand your standing.

- Only Shopping at the Dealership: Relying solely on dealership financing limits your options and negotiating power. Always get pre-approved elsewhere first.

- Focusing Solely on Monthly Payments: This is a trap! A low monthly payment often comes with a longer loan term and a higher APR, leading to much more interest paid overall.

- Ignoring the Total Cost of the Loan: Look beyond the monthly payment and even the APR to calculate the total amount you’ll pay back (principal + interest + fees).

- Applying for Too Many Loans at Once (Outside the Shopping Window): While multiple inquiries for the same type of loan within a short period are often grouped, excessive, scattered applications can negatively impact your credit score.

Pro Tips for Securing a Lower Car Loan APR

Now that you understand "what would my APR be on a car loan" and the factors at play, here are some actionable strategies to help you get the best possible rate.

- Actively Improve Your Credit Score: This is a long-term strategy but incredibly effective. Pay bills on time, reduce credit card balances, and avoid opening new lines of credit unnecessarily before applying for a car loan. A higher score directly translates to a lower APR.

- Save for a Larger Down Payment: The more you put down upfront, the less you borrow, and the less risk the lender takes on. This often results in a more attractive APR.

- Consider a Co-signer Strategically: If your credit isn’t ideal, a co-signer with excellent credit can help you qualify for a much lower APR. However, ensure both parties understand the shared responsibility and potential risks.

- Negotiate, Negotiate, Negotiate! Armed with pre-approval offers, you have leverage. Don’t be afraid to negotiate the APR with the dealership’s finance department. They might be able to beat your outside offer to earn your business.

- Refinance Later: If you secure a car loan with a higher APR due to circumstances (e.g., lower credit score at the time), you can often refinance the loan later. If your credit score improves or market interest rates drop, you might qualify for a significantly lower APR and reduce your monthly payments or total interest.

Conclusion: Empowering Your Car Buying Journey

Understanding "what would my APR be on a car loan" is not just about crunching numbers; it’s about making informed financial decisions that can save you thousands of dollars over the lifespan of your vehicle. The Annual Percentage Rate is your clearest indicator of the true cost of borrowing, encompassing both the interest rate and associated fees.

By diligently checking your credit, getting pre-approved from multiple lenders, making a substantial down payment, and being strategic about your loan term, you empower yourself to secure the most favorable APR. Don’t fall into common traps like focusing solely on monthly payments or accepting the first offer presented. With the insights provided in this comprehensive guide, you are now equipped to navigate the car financing landscape with confidence and financial wisdom. Start your journey to an informed car purchase today and drive away with a deal that truly benefits your bottom line.