Unlocking Your Car Loan APR: The Ultimate Guide to Understanding and Securing the Best Rates

Unlocking Your Car Loan APR: The Ultimate Guide to Understanding and Securing the Best Rates Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or used vehicle is an exciting prospect. The gleaming paint, the new car smell, the promise of freedom on the open road – it’s easy to get swept up in the emotion. However, beneath the surface of vehicle choice and monthly payments lies a critical financial factor that can significantly impact the total cost of your car: the Annual Percentage Rate, or APR. Understanding "What APR will I get on a car loan?" isn’t just about a number; it’s about financial literacy, strategic planning, and ultimately, saving yourself a substantial amount of money.

As an expert blogger and professional SEO content writer, I’ve seen countless individuals navigate the complexities of car financing. My goal with this comprehensive guide is to demystify the car loan APR, provide you with actionable insights, and empower you to secure the most favorable rates possible. We’ll dive deep into every factor that influences your APR, from your personal credit history to the type of car you choose, ensuring you’re equipped to make a truly informed decision.

Unlocking Your Car Loan APR: The Ultimate Guide to Understanding and Securing the Best Rates

What Exactly Is APR, Beyond Just the Interest Rate?

Many people mistakenly use "interest rate" and "APR" interchangeably, but they are distinct financial terms with different implications for your car loan. While the interest rate is simply the cost of borrowing money, expressed as a percentage of the principal, the APR offers a more complete picture of your borrowing costs.

The Annual Percentage Rate (APR) represents the true annual cost of your loan, encompassing not only the interest rate but also any additional fees or charges associated with the loan. These might include origination fees, processing fees, or even certain insurance premiums bundled into the loan. By law, lenders must disclose the APR, giving you a standardized way to compare different loan offers.

Understanding this distinction is paramount. A loan with a slightly lower interest rate but higher fees could, in fact, have a higher APR than another loan with a marginally higher interest rate but no additional fees. Focusing solely on the interest rate can lead you to overlook hidden costs, potentially increasing your total repayment amount over the loan’s lifetime. Always scrutinize the APR as the ultimate benchmark for comparison.

Your Credit Score: The Undisputed King of APR Determination

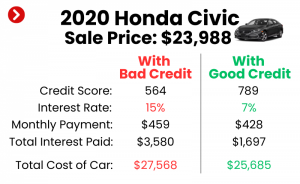

Without a doubt, your credit score is the single most influential factor in determining the APR you’ll be offered on a car loan. Lenders use your credit score as a quick and objective measure of your creditworthiness – essentially, how risky you are as a borrower. A higher credit score signals a lower risk, translating into more favorable loan terms and a lower APR.

Credit scores, like FICO or VantageScore, are complex algorithms that synthesize your financial history. They consider elements such as your payment history, the amount of debt you owe, the length of your credit history, the types of credit you use, and any new credit applications. Lenders rely heavily on these scores to predict the likelihood of you repaying your loan on time and in full.

Based on my experience in the financial industry, a strong credit score, typically above 700, can unlock the lowest APRs, often referred to as "prime" rates. If your score falls into the "good" (670-739) or "fair" (580-669) categories, you’ll likely still qualify for a loan, but your APR will be progressively higher to compensate the lender for the increased perceived risk. For those with "poor" credit (below 580), securing a car loan can be challenging, and the APRs offered will be significantly higher, sometimes even double-digit percentages.

Pro Tip from us: Always check your credit score and credit report before you even start car shopping. This allows you to identify any errors, understand your standing, and gives you time to make minor improvements if needed. You are entitled to a free credit report from each of the three major credit bureaus annually.

Debt-to-Income (DTI) Ratio: Your Financial Juggling Act

Beyond your credit score, lenders will also scrutinize your Debt-to-Income (DTI) ratio. This crucial metric indicates how much of your gross monthly income is consumed by debt payments. It’s a direct reflection of your ability to comfortably take on additional debt, such as a new car loan, without overextending your finances.

Your DTI is calculated by summing up all your monthly debt payments – including mortgage or rent, student loans, credit card minimums, and any existing car payments – and dividing that total by your gross monthly income. For example, if your monthly debt payments are $1,000 and your gross monthly income is $3,000, your DTI is 33%. Lenders prefer a lower DTI, as it suggests you have more disposable income to manage your new car loan payments.

Generally, a DTI ratio of 36% or less is considered excellent by most lenders, making you a highly attractive borrower for car loans. Some lenders might approve loans for DTIs up to 43% or even higher, especially if you have a very strong credit score. However, a higher DTI signals greater financial strain, which can lead to a higher APR or even a loan denial.

Common mistake to avoid: Many prospective car buyers focus solely on the car’s price and their credit score, completely overlooking their DTI. If your DTI is too high, even with excellent credit, a lender might view you as a higher risk, impacting your APR or your ability to get approved at all. It’s wise to calculate your DTI before applying to understand your financial capacity.

Loan Term: The Length of Your Commitment and Its APR Impact

The loan term, or the duration over which you agree to repay your car loan, is another significant factor influencing your APR. Car loans typically range from 24 to 84 months, with 60 or 72 months being common choices. While a longer loan term might seem appealing due to lower monthly payments, it often comes with a trade-off: a higher APR.

Lenders perceive longer loan terms as riskier. Over an extended period, there’s a greater chance of unforeseen circumstances impacting your ability to repay, such as job loss, economic downturns, or the car depreciating faster than the loan balance. To compensate for this increased risk, lenders typically charge a higher APR for longer terms. Additionally, you’ll end up paying more in total interest over the life of a longer loan, even if the APR difference seems small.

Conversely, shorter loan terms generally come with lower APRs. The reduced risk for the lender means they can offer more competitive rates. While your monthly payments will be higher with a shorter term, you’ll pay significantly less in total interest and own your car outright much sooner. It’s a balance between managing your monthly budget and minimizing the overall cost of the loan.

Pro tips from us: When considering the loan term, don’t just focus on the monthly payment. Calculate the total cost of the loan for different terms to see the true financial impact. A slightly higher monthly payment for a shorter term could save you thousands in interest over the life of the loan.

Your Down Payment: Showing Your Financial Commitment

The size of your down payment plays a crucial role in determining your car loan APR. A substantial down payment reduces the amount you need to borrow, which directly lowers the lender’s risk. When you put more money down upfront, you reduce the loan-to-value (LTV) ratio, making the loan more secure for the lender.

Lenders view a significant down payment as a sign of financial stability and commitment. It indicates that you have a vested interest in the vehicle and are less likely to default on the loan. This reduced risk translates into a willingness on the part of the lender to offer you a lower APR. Furthermore, a larger down payment means you’ll be financing a smaller amount, leading to lower monthly payments and less interest paid over the life of the loan.

Based on my years of observing car loan trends, a 20% down payment is often the sweet spot. While not always feasible for everyone, striving for at least 10-20% can significantly improve your chances of securing a favorable APR. This also helps you avoid being "upside down" on your loan, where you owe more than the car is worth, a common issue with minimal or no down payment.

Vehicle Type and Age: The Asset’s Role in Your APR

Believe it or not, the specific vehicle you choose can also influence the APR you receive. Lenders assess the risk associated with the collateral – in this case, the car itself. Factors like whether the car is new or used, its make and model, and its anticipated depreciation rate all play a part.

Generally, new cars tend to qualify for lower APRs than used cars. This is because new cars hold their value better initially, are less prone to mechanical issues, and are easier for lenders to appess. Used cars, on the other hand, have already undergone significant depreciation, and their future reliability can be less predictable. This higher perceived risk often translates into a slightly higher APR for used car loans.

Furthermore, certain types of vehicles or specific models might be viewed differently. A niche luxury car with high depreciation and potentially expensive repairs might carry a higher risk for a lender compared to a popular, reliable economy sedan. The older the used car, or the higher its mileage, the higher the risk often becomes, potentially pushing your APR upwards.

Common mistake to avoid: Focusing solely on the sticker price of a used car and overlooking how its age and condition might affect your financing terms. A "great deal" on an older car could be offset by a significantly higher APR, making the total cost of ownership much greater.

Market Conditions & The Broader Economic Environment

While many factors influencing your APR are personal, some are entirely external and beyond your direct control. Broader market conditions and the prevailing interest rate environment play a significant role in setting baseline loan rates across the board.

The Federal Reserve’s monetary policy, for instance, heavily influences the prime interest rate, which in turn affects the rates lenders offer for various loans, including car loans. When the Fed raises interest rates to combat inflation, car loan APRs tend to rise. Conversely, during periods of economic stimulus, rates may decrease. Economic stability, consumer confidence, and even global events can subtly shift the lending landscape.

Understanding these macro factors can help you gauge the general market. While you can’t change these conditions, being aware of them can help you decide if it’s a generally favorable time to borrow or if rates are unusually high. This awareness is part of being a savvy borrower.

Lender Type: Not All Financial Institutions Are Created Equal

Where you choose to apply for your car loan can have a considerable impact on the APR you receive. The lending landscape is diverse, encompassing traditional banks, local credit unions, dealership financing (including captive lenders and third-party partners), and online lenders. Each type has its own underwriting criteria, risk assessment models, and competitive advantages.

- Banks: Offer a wide range of loan products and often competitive rates, especially for borrowers with excellent credit.

- Credit Unions: Known for being non-profit organizations, credit unions often provide some of the most competitive APRs and more flexible terms to their members. They are an excellent option to explore.

- Dealership Financing: While convenient, rates can vary widely. Dealers often work with multiple lenders (third-party) or have their own "captive" finance companies (e.g., Toyota Financial Services). They might offer promotional rates, but it’s crucial to compare.

- Online Lenders: These modern lenders often have streamlined application processes and can sometimes offer competitive rates, especially for specific credit profiles.

Pro Tip from us: Always shop around and get pre-approved from at least 2-3 different lenders before you step foot on a dealership lot. This gives you concrete offers to compare and provides leverage during negotiations. Don’t settle for the first offer you receive.

Co-Signer or Co-Borrower: Leveraging Support for a Better APR

If your credit score isn’t ideal or your debt-to-income ratio is on the higher side, bringing in a co-signer or co-borrower can significantly improve your chances of approval and help you secure a lower APR. A co-signer is someone with good credit who agrees to be equally responsible for the loan repayment if you default.

Lenders view a co-signer as an added layer of security, as their strong credit history mitigates the risk associated with your application. This reduced risk often translates into a more favorable APR, which can save you a substantial amount of money over the life of the loan. It’s a common strategy for younger borrowers, those rebuilding credit, or individuals with limited credit history.

However, it’s crucial to understand the implications. The co-signer is legally bound to repay the loan if you cannot, and any missed payments will negatively impact their credit score as well. This should only be considered with a trusted individual who fully understands the commitment.

Negotiating Your APR: Yes, It’s Possible!

Many people believe that the APR offered on a car loan is a fixed, non-negotiable figure. Based on my professional experience, a well-informed borrower can often secure a better deal through negotiation, especially if they’ve done their homework beforehand. Lenders have some flexibility within their approved rate ranges, and they are more likely to offer their best rates to borrowers who demonstrate financial preparedness and present competitive offers from other institutions.

The key to negotiation lies in leveraging your pre-approvals. When you walk into a dealership with a pre-approved loan offer from your bank or credit union, you’ve established a baseline. The dealer’s finance department will then work to either match or beat that offer to keep your business in-house. This competition works in your favor.

Don’t be afraid to ask if there’s any wiggle room on the APR, particularly if you have an excellent credit score and a strong financial profile. Highlight your strengths as a borrower and politely inquire about the possibility of a lower rate. Remember, every fraction of a percentage point you can shave off your APR translates into real savings over the loan term.

Step-by-Step Guide: How to Get the Best Possible Car Loan APR

Securing the best possible APR requires a proactive and strategic approach. Follow these steps to maximize your chances:

- Check and Improve Your Credit Score: Obtain your credit reports from AnnualCreditReport.com. Review them for errors and dispute any inaccuracies. If your score needs a boost, focus on paying bills on time, reducing credit card balances, and avoiding new credit applications in the months leading up to your car loan application.

- Calculate Your Debt-to-Income (DTI) Ratio: Understand your current financial obligations. If your DTI is high, consider paying down other debts before applying for a car loan to present a more favorable financial picture.

- Determine Your Budget and Down Payment: Set a realistic budget for your car purchase, including the total loan amount and a comfortable monthly payment. Aim for at least a 10-20% down payment to reduce the loan amount and improve your APR.

- Shop for Pre-Approvals from Multiple Lenders: Contact various banks, credit unions, and online lenders to get pre-approved for a car loan. This process usually involves a soft credit pull, which won’t impact your score, and gives you concrete offers to compare.

- Compare Offers Meticulously: Don’t just look at the monthly payment. Compare the APR, total interest paid, loan term, and any associated fees from each offer. The lowest APR should be your primary focus.

- Negotiate with the Dealer/Lender: Use your pre-approved offers as leverage when discussing financing with the dealership. They may be able to match or beat your external offers. Be firm but polite in your negotiations.

- Read the Fine Print: Before signing any loan agreement, meticulously review all documents. Ensure the APR, loan term, and all other conditions match what you agreed upon. Don’t hesitate to ask questions about anything you don’t understand.

Common Mistakes to Avoid When Applying for a Car Loan

Based on years of helping people navigate car loans, these are the pitfalls I see most often that can lead to a higher APR or an unfavorable loan experience:

- Not Checking Your Credit Score: Going into the application process blind means you don’t know your leverage or potential weaknesses. This can lead to accepting a higher APR than you deserve.

- Only Getting One Loan Quote: Relying solely on the first offer you receive, especially from the dealership, is a common error. Always compare multiple offers to ensure you’re getting the most competitive rate.

- Focusing Solely on Monthly Payments: While monthly payments are important for budgeting, fixating on them alone can lead to agreeing to a longer loan term with a higher APR, ultimately costing you more in total interest.

- Falling for "Zero Down" Traps Without Understanding the APR: While no down payment might seem attractive, it typically means financing the full amount (or more, including taxes and fees) at a potentially higher APR, increasing your total cost and putting you at risk of being upside down on your loan.

- Signing Without Reading the Full Contract: The loan agreement is a legal document. Ensure you understand every clause, fee, and condition before putting your signature on the dotted line.

- Letting the Dealership Run Multiple Hard Credit Inquiries: While shopping around is good, multiple hard credit inquiries can slightly ding your score. Ensure inquiries are grouped within a short window (typically 14-45 days) so they count as one for scoring purposes.

Conclusion: Empowering Your Car Loan Journey

Understanding "What APR will I get on a car loan?" is more than just academic knowledge; it’s a powerful tool that puts you in control of your car buying experience. The Annual Percentage Rate is a reflection of your financial health, the lender’s risk assessment, and the prevailing market conditions. By taking the time to educate yourself on the various factors that influence your APR, you’re not just saving money; you’re making a smart, informed financial decision.

Remember, preparation is your greatest asset. By checking your credit, understanding your DTI, shopping around for the best rates, and being ready to negotiate, you significantly increase your chances of securing the lowest possible APR. Don’t let the excitement of a new vehicle overshadow the importance of sound financial planning. Armed with this knowledge, you are now well-equipped to navigate the car loan landscape with confidence and drive away with a deal that truly benefits your wallet. Start your journey to a better car loan today and take the driver’s seat of your financial future!

For more insights into managing your personal finances and building a stronger financial future, explore our comprehensive guide on . And if you’re venturing into the used car market, don’t miss our essential tips on to ensure you make a smart choice.

For official information regarding your credit rights and how credit scores are calculated, we recommend visiting the Consumer Financial Protection Bureau (CFPB) website at Consumer Financial Protection Bureau (CFPB).