Unlocking Your Car Loan: How Much Interest Will I Pay On My Car Loan? A Comprehensive Guide

Unlocking Your Car Loan: How Much Interest Will I Pay On My Car Loan? A Comprehensive Guide Carloan.Guidemechanic.com

Buying a new car is an exciting milestone, often accompanied by the exhilarating scent of fresh upholstery and the promise of new adventures. However, for most of us, this significant purchase isn’t made with cash in hand. Instead, we rely on car loans, which bring with them the often-overlooked cost of interest. Understanding "how much interest will I pay on my car loan" is not just about crunching numbers; it’s about making informed financial decisions that can save you thousands of dollars over the life of your loan.

This in-depth guide is designed to demystify car loan interest, transforming a complex financial concept into clear, actionable insights. We’ll explore the factors that dictate your interest rate, show you how to calculate your total interest, and equip you with strategies to significantly reduce your overall cost. By the end of this article, you’ll be empowered to navigate the world of auto financing with confidence, ensuring your dream car doesn’t come with an unexpectedly hefty price tag.

Unlocking Your Car Loan: How Much Interest Will I Pay On My Car Loan? A Comprehensive Guide

The Anatomy of Your Car Loan Interest: What Are You Really Paying For?

Before we dive into calculations and strategies, it’s crucial to understand the fundamental components that make up your car loan. Interest isn’t just a flat fee; it’s a dynamic element influenced by several key terms.

What Exactly Is Interest?

At its core, interest is the cost of borrowing money. When a lender provides you with a car loan, they are essentially taking a risk. To compensate for this risk and to make a profit, they charge you interest on the principal amount you borrow. Think of it as a rental fee for using someone else’s money.

This fee is typically expressed as a percentage of the loan amount and is paid over the loan’s duration. The higher the interest rate, the more expensive your loan becomes in the long run.

APR vs. Interest Rate: Knowing the True Cost

Many people confuse the interest rate with the Annual Percentage Rate (APR), but these two terms, while related, are distinct. Understanding the difference is vital for grasping the true cost of your car loan.

The interest rate is simply the percentage charged on the principal amount you borrow. It’s the base cost of the money itself.

The Annual Percentage Rate (APR), on the other hand, represents the total annual cost of borrowing, expressed as a percentage. It includes not only the nominal interest rate but also any additional fees or charges associated with the loan, such as origination fees or administrative costs. For example, some lenders might charge a lower nominal interest rate but then add significant processing fees, making the APR higher than expected.

Pro tip from us: Always focus on the APR when comparing loan offers. It gives you the most accurate picture of the total cost of borrowing, allowing for a genuine apples-to-apples comparison between different lenders. A lower APR always translates to less money out of your pocket over the life of the loan.

The Principal Amount: The Foundation of Your Loan

The principal amount is the initial sum of money you borrow to purchase your car. This is the core figure upon which all interest calculations are based. For instance, if you take out a $25,000 car loan, $25,000 is your principal.

As you make monthly payments, a portion of each payment goes towards reducing this principal, and another portion covers the accrued interest. The faster you reduce your principal, the less interest you will pay over time.

The Loan Term: Time is Money

The loan term, or repayment period, is the length of time you have to pay back the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). This factor has a profound impact on both your monthly payment and the total interest you will pay.

A longer loan term will result in lower monthly payments, which can seem attractive. However, it also means you’re paying interest for a longer period, significantly increasing the total amount of interest paid over the life of the loan. Conversely, a shorter loan term means higher monthly payments, but you’ll pay off the loan faster and incur substantially less interest.

Common mistake to avoid are: Focusing solely on the lowest possible monthly payment without considering the long-term cost. While a lower monthly payment might ease your immediate budget, it could end up costing you thousands more in interest.

Key Factors That Influence Your Car Loan Interest

The interest rate you qualify for isn’t arbitrary. Several critical factors come into play, each weighing heavily on how much interest you will ultimately pay on your car loan. Understanding these can help you strategize for a better deal.

Your Credit Score: The Ultimate Determinant

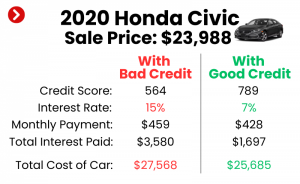

Without a doubt, your credit score is the single most influential factor in determining the interest rate you’ll receive on a car loan. Lenders use your credit score as a snapshot of your creditworthiness and your likelihood of repaying the loan.

- Excellent Credit (780-850): Borrowers with excellent credit are considered low-risk and typically qualify for the lowest interest rates available.

- Good Credit (670-739): Still considered low-risk, these borrowers usually secure very competitive rates.

- Fair Credit (580-669): Borrowers in this range might face slightly higher interest rates due to a perceived moderate risk.

- Poor Credit (300-579): High-risk borrowers with poor credit often receive the highest interest rates, making their car loans significantly more expensive.

Pro tip from us: Before you even start car shopping, check your credit score. Knowing where you stand allows you to either work on improving it or adjust your expectations for interest rates. You can get free credit reports annually from major credit bureaus.

The Loan Amount (Principal): More Borrowed, More Interest

It’s a straightforward concept: the more money you borrow, the more interest you will pay. This is because interest is calculated as a percentage of the principal. A larger principal amount, even with the same interest rate, will always generate a greater total interest charge over the loan term.

Consider borrowing $30,000 versus $20,000 at the same 5% interest rate over 60 months. The $30,000 loan will accrue significantly more interest simply because the base amount is larger.

The Loan Term: A Double-Edged Sword

As mentioned earlier, the loan term has a direct and substantial impact on your total interest paid. While a longer term lowers your monthly payments, it drastically increases the cumulative interest.

For example, a $25,000 loan at 5% interest over 36 months might have a higher monthly payment than the same loan over 72 months. However, the 72-month loan could result in thousands of dollars more in total interest paid because the principal balance remains higher for a longer period, continuously accruing interest. This extended period provides more opportunities for interest to accumulate.

Your Down Payment: Reducing Your Borrowing Needs

Making a larger down payment is one of the most effective ways to reduce the total interest you pay. A down payment directly reduces the principal amount you need to borrow. Less principal means less interest accrues over the life of the loan.

Furthermore, a substantial down payment can signal to lenders that you are a responsible borrower, potentially helping you qualify for a better interest rate. It also gives you immediate equity in the vehicle, which is a significant financial advantage.

Interest Rate Offered by Lender: The Importance of Shopping Around

Lenders are not all created equal. Banks, credit unions, and dealership financing arms each have their own lending criteria and profit margins, leading to varied interest rate offers.

Based on my experience, comparing offers from at least three different lenders can uncover significant savings. Don’t just accept the first offer you receive, especially from a dealership, without exploring other options. Credit unions, in particular, often offer very competitive rates to their members.

New vs. Used Car: A Subtle Difference in Rates

Generally, interest rates for used car loans tend to be slightly higher than those for new car loans. Lenders often perceive used cars as having a higher risk profile due to factors like depreciation, potential mechanical issues, and their shorter remaining lifespan compared to a new vehicle. This perceived risk translates into a higher interest rate for the borrower.

Market Interest Rates: The Broader Economic Picture

The prevailing economic environment also plays a role. When the Federal Reserve raises interest rates, it generally leads to higher borrowing costs across the board, including car loans. Conversely, in a low-interest-rate environment, car loan rates tend to be more favorable. These broader economic factors are largely beyond your control but can influence the rates you’ll encounter at any given time.

How to Calculate Your Car Loan Interest (The Math Made Easy)

Understanding the mechanics of interest calculation is empowering. While the exact calculations for an amortizing loan can be complex, we can break it down into manageable concepts and tools.

Understanding the Amortization Schedule

Car loans are typically "amortizing" loans. This means that each monthly payment you make consists of two parts: a portion that goes towards the principal balance and a portion that covers the accrued interest. Early in the loan term, a larger percentage of your payment goes towards interest. As the principal balance decreases over time, a larger percentage of your payment starts going towards the principal.

This gradual reduction of the principal balance, and consequently the interest charged, is detailed in an amortization schedule. While you won’t typically calculate this manually for a car loan, understanding the concept helps explain why early payments are so interest-heavy.

Basic Formula for Simple Interest (For Conceptual Understanding)

For a simplified understanding of how interest is calculated over a single period, you can use the simple interest formula:

Interest = Principal x Rate x Time (I = P x R x T)

- P: The principal amount (the amount borrowed or the remaining balance).

- R: The annual interest rate (expressed as a decimal, e.g., 5% = 0.05).

- T: The time period (in years or a fraction of a year for a monthly calculation).

For a monthly calculation, you would divide the annual rate by 12 and the time by 12 months. This formula is a simplification, as car loans use compounding interest, but it helps illustrate the basic relationship.

Using an Online Car Loan Calculator: Your Best Friend

The easiest and most accurate way to determine how much interest you will pay on your car loan is by using an online car loan calculator. These tools are readily available on most financial websites, bank websites, and even dealership sites.

You’ll typically input three key pieces of information:

- Loan Amount: The total principal you plan to borrow.

- Interest Rate: The APR you anticipate or have been offered.

- Loan Term: The number of months you plan to repay the loan.

The calculator will then instantly provide you with your estimated monthly payment and, crucially, the total amount of interest you will pay over the life of the loan, along with the total amount repaid (principal + interest).

Pro tip from us: Don’t rely on just one calculator. Use a few different reputable online calculators to cross-reference results and ensure accuracy. This also helps you experiment with different scenarios (e.g., lower interest rates, shorter terms) to see their impact on total interest.

Example Calculation: Putting it into Perspective

Let’s walk through a common scenario to illustrate the impact of these factors:

Scenario 1:

- Loan Amount (Principal): $30,000

- APR: 6% (or 0.06)

- Loan Term: 60 months (5 years)

Using an online calculator, you’d find:

- Estimated Monthly Payment: Approximately $579.98

- Total Amount Paid: Approximately $34,798.80

- Total Interest Paid: Approximately $4,798.80 ($34,798.80 – $30,000)

Scenario 2 (Shorter Term, Same Loan Amount & Rate):

-

Loan Amount (Principal): $30,000

-

APR: 6%

-

Loan Term: 36 months (3 years)

-

Estimated Monthly Payment: Approximately $912.78

-

Total Amount Paid: Approximately $32,859.90

-

Total Interest Paid: Approximately $2,859.90

Notice the significant difference: a shorter loan term (36 months vs. 60 months) reduces the total interest paid by nearly $2,000, even though the interest rate and principal are the same. This clearly demonstrates the power of the loan term on your overall cost.

Strategies to Reduce the Total Interest You Pay

Paying less interest means saving money, which you can then allocate to other financial goals. Here are some proven strategies to minimize the amount of interest you’ll pay on your car loan.

1. Improve Your Credit Score

Since your credit score is a major determinant of your interest rate, taking steps to improve it before applying for a loan can yield substantial savings.

- Pay all your bills on time, every time: Payment history is the most important factor in your credit score.

- Reduce your outstanding debt: Lowering your credit utilization ratio (how much credit you’re using versus how much you have available) can boost your score.

- Check your credit report for errors: Incorrect information can negatively impact your score. Dispute any inaccuracies promptly.

- Avoid opening new credit accounts right before applying for a car loan: This can temporarily lower your score.

2. Make a Larger Down Payment

This is one of the most direct ways to reduce interest. The less you borrow, the less interest accrues. A larger down payment also reduces your loan-to-value (LTV) ratio, which can make you a more attractive borrower to lenders, potentially leading to a lower interest rate offer. Aim for at least 10-20% of the car’s purchase price, if possible.

3. Choose a Shorter Loan Term

As demonstrated in our example, a shorter loan term drastically reduces the total interest paid. While your monthly payments will be higher, the long-term savings are often substantial. If your budget allows for the higher monthly payment, opting for a 36- or 48-month loan over a 60- or 72-month loan is a smart financial move.

4. Shop Around for the Best Rates

Never settle for the first loan offer you receive. This cannot be stressed enough.

Based on my experience, taking the time to get pre-approved from multiple lenders – including banks, credit unions, and online lenders – can reveal a significant difference in APRs. Even a difference of 0.5% or 1% can save you hundreds, if not thousands, over the life of the loan. Present your best offer to other lenders to see if they can beat it.

5. Refinance Your Car Loan

If you’ve already taken out a car loan but your financial situation has improved (e.g., your credit score has increased, or market rates have dropped), consider refinancing. Refinancing involves taking out a new loan to pay off your existing one, ideally at a lower interest rate or with more favorable terms.

This can be a powerful strategy to reduce your monthly payments and/or the total interest paid. for a deeper dive into this option.

6. Make Extra Payments

Paying more than your minimum monthly payment is an excellent way to reduce your principal balance faster, thereby reducing the amount of interest that accrues over time.

- Round up your payments: If your payment is $375, pay $400.

- Make an extra payment when you can: An extra payment per year can significantly shorten your loan term and save interest.

- Apply extra funds directly to principal: Pro tip: When making extra payments, always specify to your lender that the additional amount should be applied directly to the principal, not towards future payments. This ensures the money immediately starts working to reduce your interest burden.

7. Avoid Unnecessary Add-ons

Dealerships often push various add-ons like extended warranties, paint protection, or GAP insurance. While some might be worthwhile, many are overpriced or unnecessary. If you finance these add-ons, you’ll be paying interest on them for the entire loan term, further inflating your total cost. Carefully consider if you truly need them and if you can purchase them cheaper elsewhere.

Common Mistakes to Avoid When Taking Out a Car Loan

Even with the best intentions, borrowers can fall into common traps that end up costing them more in interest and overall. Being aware of these pitfalls can help you navigate the process more successfully.

1. Focusing Solely on Monthly Payments

This is perhaps the most common mistake. Dealerships often highlight low monthly payments to make a car seem more affordable. However, a low monthly payment usually comes with a longer loan term, which means significantly more interest paid over time. Always ask for the total cost of the loan, including interest.

2. Not Shopping Around for Rates

As discussed, failing to compare offers from multiple lenders can cost you hundreds or thousands of dollars. It takes a little extra effort, but the savings are well worth it. Don’t let the convenience of dealership financing prevent you from seeking better rates elsewhere.

3. Ignoring Your Credit Score

Many buyers go into the car buying process without knowing their credit score. This puts them at a disadvantage, as they don’t know what kind of rates they genuinely qualify for. Always check your score beforehand to be an informed negotiator.

4. Rolling Over Negative Equity from an Old Car

If you owe more on your current car than it’s worth (negative equity), some dealerships will offer to roll that balance into your new car loan. While this seems convenient, it means you’re starting your new loan already underwater, and you’ll be paying interest on money you no longer have (your old car’s debt). This is a financially risky move that should generally be avoided.

5. Not Reading the Fine Print

Loan agreements can be complex, but it’s crucial to understand every term and condition. Pay close attention to the APR, any prepayment penalties, late payment fees, and whether the interest rate is fixed or variable. Don’t sign anything you don’t fully comprehend.

Understanding the Long-Term Impact

The interest you pay on your car loan extends beyond just the immediate cost of your vehicle; it has a ripple effect on your broader financial health.

How Interest Affects Your Overall Financial Health

Every dollar spent on interest is a dollar that cannot be saved, invested, or used for other financial goals like a down payment on a home, retirement savings, or paying down higher-interest debt. High interest payments on a car loan can strain your budget, limiting your financial flexibility and slowing your progress towards wealth accumulation.

By strategically reducing the interest you pay, you free up cash flow that can be directed towards building your financial future. It’s about optimizing your resources for maximum benefit.

The Power of Compound Interest (Even in Reverse)

While compound interest is often celebrated for its ability to grow savings, it works in reverse for loans. The longer you owe money, the more that interest compounds on the remaining principal, increasing your overall debt burden. Understanding this dynamic underscores the importance of paying off loans as quickly and efficiently as possible.

Financial Freedom Implications

Minimizing car loan interest is a step towards greater financial freedom. A smaller debt burden means less financial stress and more control over your money. It allows you to accelerate other financial goals, build an emergency fund, or simply enjoy your income more fully without a significant portion being siphled off by interest payments.

Frequently Asked Questions (FAQs)

Here are some common questions people ask about car loan interest:

Is car loan interest tax-deductible?

Generally, no. Car loan interest is typically not tax-deductible for personal use vehicles. However, there are exceptions. If you use your car primarily for business purposes, you might be able to deduct a portion of the interest as a business expense. Always consult with a tax professional for personalized advice regarding your specific situation.

Does a higher down payment always mean less interest?

Yes, almost always. A higher down payment directly reduces the principal amount you need to borrow. Since interest is calculated on the principal, a smaller principal will naturally accrue less total interest over the life of the loan, assuming the same interest rate and loan term. It can also sometimes help you secure a lower interest rate, further reducing interest costs.

Can I pay off my car loan early without penalty?

Most car loans today do not have prepayment penalties, meaning you can pay off your loan early without incurring extra fees. This is a common and highly effective strategy to save on interest. However, it is absolutely crucial to always check your specific loan agreement for a prepayment penalty clause before making extra payments or planning an early payoff. Some older loans or specific lenders might still include them.

Conclusion: Drive Smarter, Not Harder

Understanding "how much interest will I pay on my car loan" is far more than a simple calculation; it’s a critical component of responsible car ownership and sound financial planning. By grasping the core concepts of interest, APR, principal, and loan term, and by actively applying the strategies outlined in this guide, you gain immense power over your car financing journey.

Remember, your credit score, down payment, and the diligence you exercise in shopping for rates are your most potent tools. Don’t just accept the first offer or focus solely on the lowest monthly payment. Be an informed consumer, ask questions, and leverage the knowledge you’ve gained here to secure the best possible deal.

By taking control of your car loan interest, you’re not just saving money; you’re building a stronger financial future, one smart decision at a time. Drive smarter, not harder, and let your car loan work for you, not against you. For more insights on managing your finances and making smart purchasing decisions, explore our other articles on . For further information on consumer lending regulations, you can also visit trusted sources like the Link to an external source, e.g., Consumer Financial Protection Bureau (CFPB) website.