Unlocking Your Car Loan: The Ultimate Guide to Interest Calculators and Amortization (Your Roadmap to Financial Freedom)

Unlocking Your Car Loan: The Ultimate Guide to Interest Calculators and Amortization (Your Roadmap to Financial Freedom) Carloan.Guidemechanic.com

Buying a car is an exciting milestone, offering freedom and convenience. Yet, for many, the joy of a new vehicle can quickly be overshadowed by the complexities of a car loan. Understanding how your car loan works, especially the interest and its amortization, is not just smart—it’s essential for your financial well-being. Without this knowledge, you could end up paying significantly more than necessary.

This comprehensive guide is designed to transform you from a passive borrower into an empowered car owner. We’ll demystify the "Car Loan Interest Calculator Amortization" concept, breaking down complex financial terms into easy-to-understand insights. By the end of this article, you’ll possess the knowledge to confidently navigate your car loan, make informed decisions, and potentially save thousands of dollars over its lifetime.

Unlocking Your Car Loan: The Ultimate Guide to Interest Calculators and Amortization (Your Roadmap to Financial Freedom)

Demystifying Car Loan Amortization: What It Is and Why It Matters

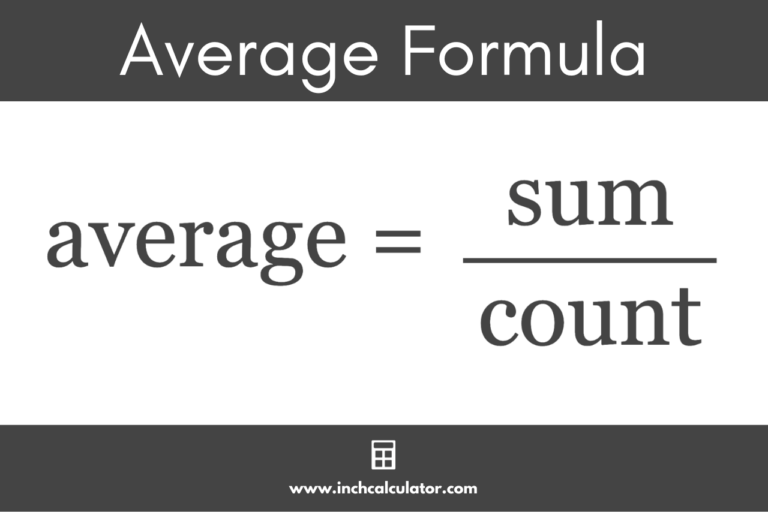

When you take out a car loan, you’re not just borrowing the price of the car; you’re also agreeing to pay interest on that borrowed money. Amortization is the process of gradually paying off a debt over time through a series of regular payments. Each payment consists of both principal (the original amount borrowed) and interest.

Think of it as a meticulously planned repayment schedule. Every time you make a monthly payment, a portion goes towards reducing your loan’s principal balance, and another portion covers the interest accrued since your last payment. Understanding this structure is foundational to managing your car loan effectively. It’s the blueprint of your financial commitment.

Why does this matter so much? Because the way interest is calculated and applied can significantly impact your total cost. A car loan interest calculator, combined with an amortization schedule, provides unparalleled transparency. It reveals precisely where your money is going with each payment, empowering you to strategize for earlier debt freedom and substantial savings.

The Core Components of Your Car Loan: Decoding the Numbers

Before you can effectively use a car loan interest calculator, it’s crucial to understand the key variables that define your loan. These elements work in concert to determine your monthly payment and the total cost of your loan. Based on my experience, many borrowers overlook the interplay of these factors, focusing solely on the monthly payment figure.

-

Principal Amount: This is the actual amount of money you borrowed to purchase the car. It’s the sticker price minus any down payment or trade-in value. A lower principal means less money to accrue interest on.

-

Interest Rate (APR): The Annual Percentage Rate (APR) is the cost of borrowing money, expressed as a yearly percentage. It includes not only the basic interest rate but also certain fees associated with the loan. A lower APR directly translates to less interest paid over the life of the loan, making it a critical factor to negotiate.

-

Loan Term (Duration): This refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). While a longer term can mean lower monthly payments, it almost always results in paying significantly more interest overall. It’s a trade-off between immediate affordability and long-term cost.

-

Monthly Payment: This is the fixed amount you agree to pay each month until the loan is fully repaid. This figure is a direct result of the principal, interest rate, and loan term. Understanding how these components influence your monthly payment is vital for budgeting and financial planning.

How a Car Loan Interest Calculator Works: The Magic Behind the Numbers

At its heart, a car loan interest calculator is a powerful simulation tool. It takes the core components of your loan—the principal amount, your interest rate (APR), and the loan term—and instantly computes your estimated monthly payment. But its utility goes far beyond just that single figure.

You simply input these three key pieces of information into the calculator. Within seconds, it will display not only your projected monthly payment but often also the total interest you’ll pay over the loan’s life and the overall cost of the car including interest. This immediate feedback allows you to see the real financial implications of different loan scenarios.

The calculator utilizes a standard loan amortization formula, a complex mathematical equation that determines how each payment is split between principal and interest. While you don’t need to understand the intricate math, knowing that a robust formula underpins the calculation provides confidence in its accuracy. Pro tips from us include always trying different interest rates and loan terms. This will reveal how seemingly small changes can lead to substantial savings or increased costs over time.

Diving Deep into the Amortization Schedule: Your Loan’s Blueprint

An amortization schedule is the true hero in understanding your car loan. It’s a detailed table that breaks down every single payment you’ll make over the entire loan term. Each row typically shows the payment number, the date, the total payment amount, how much of that payment goes towards interest, how much goes towards principal, and your remaining loan balance.

Early in the loan term, you’ll notice that a larger portion of your monthly payment goes towards interest. This is a standard practice in loan amortization, often referred to as "interest-front-loading." As you progress through the loan, the amount allocated to interest gradually decreases, and the portion applied to the principal steadily increases. By the end of the loan, almost your entire payment will be reducing the principal balance.

Reading this schedule provides incredible insight. It allows you to track your progress, see exactly how much interest you’ve paid to date, and visualize how much principal you still owe. This transparency is invaluable for financial planning. It also highlights the significant impact of making extra payments, as they directly reduce the principal balance, thereby cutting down future interest accrual.

Beyond the Basics: Advanced Strategies & Considerations

Once you grasp the fundamentals, you can leverage your understanding of car loan amortization to implement advanced strategies. These techniques are designed to save you money, reduce your loan term, and accelerate your path to car ownership. From years of observing loan structures, we know these methods can make a significant difference.

- Prepayment Strategies: One of the most effective ways to save on interest is by paying more than your minimum monthly payment. Even a small extra amount can drastically reduce the total interest paid and shorten your loan term. You can achieve this by making one extra principal-only payment per year, rounding up your monthly payment, or even making bi-weekly payments (which results in 13 full payments per year instead of 12).

- Common mistakes to avoid are blindly prepaying without first checking if your loan has any prepayment penalties. While rare for car loans, it’s always wise to confirm this with your lender.

- The Impact of a Down Payment: A larger down payment immediately reduces the principal amount you need to borrow. This has a cascading effect: less principal means less interest accrues over the loan term, leading to lower monthly payments or a shorter loan term with the same payment. It’s a powerful tool for reducing your overall cost.

- Loan Term vs. Interest Paid: This is a crucial balancing act. While a longer loan term (e.g., 72 or 84 months) offers lower monthly payments, it significantly increases the total interest you’ll pay over the life of the loan. Conversely, a shorter term (e.g., 36 or 48 months) means higher monthly payments but substantially less interest paid. Use the calculator to compare these scenarios and find the sweet spot for your budget and long-term financial goals.

- The Power of a Lower Interest Rate: Even a small difference in APR can lead to thousands of dollars in savings. Always shop around for the best interest rate before you go to the dealership. Get pre-approved by your bank or credit union. This gives you leverage and a benchmark to compare against the dealership’s financing offers. Negotiating a lower rate is one of the most impactful actions you can take.

Choosing the Right Car Loan Calculator: What to Look For

Not all car loan calculators are created equal. To get the most accurate and useful information, you need to select one that offers specific features. A good calculator becomes your personal financial advisor, helping you model various scenarios before committing to a loan.

- Accuracy and Reliability: Ensure the calculator uses standard financial formulas and provides consistent results. Look for tools from reputable financial institutions or well-known financial education websites.

- User-Friendliness: The interface should be intuitive and easy to navigate. You should be able to quickly input your numbers and understand the output without confusion.

- Ability to Customize: The best calculators allow you to adjust variables like down payment, trade-in value, and even model extra payments. This flexibility is crucial for exploring different financial strategies.

- Amortization Schedule Output: A truly comprehensive calculator will generate a full amortization schedule. This feature is invaluable for understanding the principal-interest breakdown of each payment. For a deeper dive into choosing the best financial tools, check out our guide on .

Real-World Scenarios and Practical Applications

Let’s put theory into practice. Using a car loan interest calculator, you can simulate real-world situations to make the best decision for your finances. Always run these numbers before signing any papers.

- Scenario 1: Comparing Two Loan Offers: Imagine you have two offers for a $30,000 car:

- Offer A: 5% APR over 60 months.

- Offer B: 6% APR over 48 months.

By plugging these into a calculator, you can see which offers a lower monthly payment, but more importantly, which results in less total interest paid. You might find that Offer B, despite a higher APR, costs less overall due to the shorter term.

- Scenario 2: The Impact of an Extra Payment: Suppose your monthly payment is $400. What if you consistently pay an extra $50 each month? The calculator can show you how many months you’ll shave off your loan term and the substantial amount of interest you’ll save. This visualization is incredibly motivating.

- Scenario 3: Deciding on Loan Term: You’re considering a $25,000 loan. Should you take a 60-month term at 4.5% APR or a 72-month term at 4.75% APR? The calculator will quickly illustrate that while the 72-month term has a lower monthly payment, the total interest paid could be thousands more. This helps you weigh immediate budget relief against long-term cost.

Common Mistakes to Avoid When Taking Out a Car Loan

Even with the best tools, it’s easy to fall into common traps. Being aware of these pitfalls can save you from costly errors.

- Focusing Only on Monthly Payments: This is perhaps the most common mistake. Dealerships often highlight low monthly payments to make a car seem affordable, but this often comes at the expense of a longer loan term and much higher total interest paid. Always look at the total cost of the loan.

- Ignoring the Total Interest Paid: The difference between a good loan and a bad loan often lies in the total interest. Use your calculator to clearly see this figure. A low interest rate over a very long term can still result in more interest than a slightly higher rate over a short term.

- Not Checking Your Credit Score: Your credit score is a major determinant of the interest rate you’ll be offered. A higher score typically unlocks lower rates. Check your score well in advance and address any inaccuracies. Understanding your creditworthiness is your first step. For more details on how your credit score impacts loans, consult trusted resources like the Consumer Financial Protection Bureau (CFPB) at https://www.consumerfinance.gov/.

- Skipping the Amortization Schedule: As discussed, this schedule is your loan’s roadmap. Failing to review it means you’re driving blind. Demand to see it from your lender or generate one yourself using an online calculator.

- Not Shopping Around for Rates: Never accept the first financing offer you receive. Get quotes from multiple banks, credit unions, and online lenders. Competition among lenders works in your favor and can lead to significant savings.

Your Journey to Car Loan Mastery Begins Now

Understanding your car loan interest calculator and its amortization schedule is more than just financial literacy; it’s a critical skill for responsible car ownership. This knowledge empowers you to make informed decisions, negotiate effectively, and ultimately save a substantial amount of money over the life of your loan. You now have the tools and the insights to see beyond the monthly payment and understand the true cost of your vehicle.

Don’t let the complexities of car financing intimidate you. Embrace the power of the car loan interest calculator and its detailed amortization schedule. Use it to compare offers, strategize extra payments, and confidently navigate your financial journey. By taking control of your car loan, you’re not just buying a car; you’re investing in your financial future. To continue building your financial literacy, explore our article on for even more insights. Take the driver’s seat of your finances today!