Unlocking Your Car Loan: What’s An Average APR For A Car Loan (And How to Get the Best Rate)

Unlocking Your Car Loan: What’s An Average APR For A Car Loan (And How to Get the Best Rate) Carloan.Guidemechanic.com

Navigating the world of car loans can feel like deciphering a complex code, especially when terms like "APR" start flying around. You’re probably asking yourself, "What’s an average APR for a car loan?" and more importantly, "How can I ensure I’m getting a good deal?" Understanding your Annual Percentage Rate (APR) is absolutely crucial, as it’s the true cost of borrowing money for your new or used vehicle.

Based on my experience helping countless consumers understand their auto financing, many people mistakenly focus solely on the monthly payment. While the monthly payment is important for budgeting, the APR is the single most significant factor determining how much you’ll pay over the life of the loan. This comprehensive guide will demystify car loan APRs, explain what influences them, reveal current averages, and equip you with the knowledge to secure the most favorable terms possible.

Unlocking Your Car Loan: What’s An Average APR For A Car Loan (And How to Get the Best Rate)

What Exactly is APR? It’s More Than Just the Interest Rate

Before we dive into averages, let’s clarify what APR truly represents. The Annual Percentage Rate (APR) is the total cost of borrowing money, expressed as a yearly percentage. It includes not only the interest rate but also any additional fees charged by the lender, such as administrative fees, loan origination fees, or documentation fees.

Think of it this way: the interest rate is the pure cost of borrowing the principal amount. The APR, however, gives you a more complete picture of the loan’s overall expense. This comprehensive figure allows for an apples-to-apples comparison between different loan offers, helping you make an informed decision.

Understanding the difference is vital because a loan might advertise a low interest rate, but if it comes with high hidden fees, its APR could still be higher than another loan with a slightly higher interest rate but no additional charges. Always compare the APR, not just the interest rate, when shopping for a car loan. This is a fundamental principle of smart borrowing.

The Current Landscape: What’s an Average APR for a Car Loan?

Pinpointing a single "average" APR for a car loan is challenging because the rates are constantly fluctuating and depend on a multitude of factors. However, we can look at general ranges to give you a benchmark. Currently, average APRs for car loans can vary significantly based on whether you’re financing a new or used vehicle, and most importantly, your credit score.

For borrowers with excellent credit (typically FICO scores above 780), new car loan APRs can range from around 3% to 7%. Used car loans, due to higher perceived risk and depreciation, usually come with slightly higher rates, often starting around 4% and going up to 9% or more for those with top-tier credit. These numbers are just starting points, though, as many variables come into play.

As of late 2023 and early 2024, the Federal Reserve’s actions on interest rates have also played a significant role. When the Fed raises its benchmark rates, it generally translates to higher borrowing costs across the board, including for auto loans. Conversely, rate cuts can lead to lower APRs. For the most up-to-date national averages, trusted financial publications and data aggregators like Experian often publish quarterly reports. (For current national averages and trends, you can refer to reputable sources like Experian’s State of the Automotive Finance Market report).

Key Factors That Drive Your Car Loan APR

Your car loan APR isn’t some arbitrary number; it’s a carefully calculated figure based on several key elements. Lenders assess these factors to determine the risk involved in lending you money. The lower they perceive that risk, the lower your APR is likely to be.

Let’s break down the most influential factors in detail. Understanding these will empower you to take steps towards securing a better rate.

1. Your Credit Score: The Undisputed King of Factors

Without a doubt, your credit score is the most significant determinant of your car loan APR. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. A higher credit score indicates to lenders that you are a reliable borrower, thus reducing their risk.

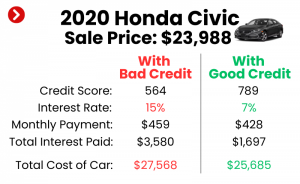

Borrowers with excellent credit scores (780+) are consistently offered the lowest APRs because they represent the lowest risk of default. Conversely, individuals with lower credit scores (sub-prime or deep sub-prime) are considered higher risk and will face significantly higher APRs, sometimes even double-digit rates. This is how lenders compensate for the increased likelihood of late payments or non-payment.

Based on my experience, many people underestimate the power of their credit score. Even a difference of 50-100 points can mean saving hundreds, if not thousands, of dollars over the life of a car loan. Taking the time to improve your credit before applying can have a massive financial payoff.

2. The Loan Term: How Long You’re Borrowing

The length of your loan, or the loan term, also plays a crucial role in determining your APR. Generally, shorter loan terms (e.g., 36 or 48 months) tend to come with lower APRs compared to longer terms (e.g., 60, 72, or even 84 months). Lenders prefer shorter terms because their money is at risk for a shorter period.

While a longer loan term might offer a lower monthly payment, making the car seem more affordable upfront, it almost always results in a higher APR and a greater total cost over the life of the loan. This is a common trap many consumers fall into, prioritizing a low monthly payment without considering the long-term financial implications. Always weigh the benefit of a lower monthly payment against the increased total interest paid.

3. New vs. Used Car: A Matter of Depreciation and Risk

The type of vehicle you’re financing—new or used—also influences your APR. New car loans typically have lower APRs than used car loans. This is primarily because new cars generally hold their value better in the initial years and are considered less of a risk for lenders. If a borrower defaults, a new car is easier for the lender to repossess and resell at a higher value than a comparable used car.

Used cars, on the other hand, have already undergone significant depreciation and carry more uncertainty regarding their mechanical condition. This higher perceived risk translates into higher APRs for used car financing. Lenders need to mitigate that increased risk, and a higher interest rate is one way they do it.

4. Your Down Payment: Showing Your Commitment

Making a substantial down payment can significantly impact your car loan APR. A larger down payment reduces the amount you need to borrow, which in turn reduces the lender’s risk. When you have more equity in the vehicle from the start, you’re less likely to default on the loan.

Lenders view a significant down payment as a sign of financial stability and commitment. It also means that if you were to default early in the loan term, the lender is less likely to lose money if they have to repossess and sell the vehicle. Aiming for at least 10-20% of the car’s value as a down payment is a smart strategy to potentially lower your APR.

5. Current Interest Rate Environment: The Macro Picture

Beyond your personal financial situation, broader economic factors also influence car loan APRs. The Federal Reserve’s monetary policy, specifically its target for the federal funds rate, has a ripple effect on all lending rates, including auto loans. When the Fed raises rates, borrowing becomes more expensive across the board.

Conversely, during periods of economic slowdown, the Fed might lower rates to stimulate borrowing and spending, which can lead to lower car loan APRs. While you can’t control the Fed’s actions, being aware of the prevailing economic climate can help you understand why rates might be higher or lower than in previous years.

6. Lender Type: Not All Lenders Are Created Equal

Where you get your loan can also affect your APR. Different types of lenders have different business models, risk appetites, and overheads.

- Banks: Often offer competitive rates, especially to customers with established banking relationships.

- Credit Unions: Known for member-focused services and often provide some of the lowest APRs, as they are non-profit organizations.

- Dealership Financing: Can be convenient, but dealers often mark up the interest rate they receive from their lending partners to make a profit. Sometimes, however, they offer promotional rates (e.g., 0% or very low APRs) on new vehicles, especially for highly qualified buyers.

- Online Lenders: Offer speed and convenience, often with competitive rates, particularly for borrowers with good credit.

Pro tips from us: Always get pre-approved from at least two or three different lenders (e.g., a credit union and an online lender) before you step into the dealership. This gives you leverage and a benchmark rate to compare against any offers the dealership might provide.

7. Debt-to-Income Ratio: Your Financial Balance

Lenders also look at your debt-to-income (DTI) ratio, which compares your total monthly debt payments to your gross monthly income. A high DTI ratio can signal that you might be overextended financially, increasing the risk of default.

While not as direct an impact as your credit score, a very high DTI can lead to a higher APR or even a loan denial. Lenders want to ensure you have sufficient disposable income to comfortably make your car payments without stretching your budget too thin.

Decoding Your Credit Score’s Impact on Car Loan APR

Let’s zoom in on the credit score, as its influence cannot be overstated. Your FICO score, which is widely used by lenders, typically ranges from 300 to 850. Here’s a general breakdown of how different credit score tiers can influence the average APR for a car loan:

- Exceptional (800-850): These borrowers are considered prime candidates for the absolute lowest rates, often securing APRs in the 3-5% range for new cars and 4-7% for used cars, depending on market conditions.

- Very Good (740-799): Still excellent, these borrowers also qualify for very competitive rates, perhaps a percentage point or so higher than the exceptional tier. Expect new car APRs around 4-6% and used car APRs around 5-8%.

- Good (670-739): The majority of consumers fall into this category. While still considered good, APRs will start to climb. New car loans might see APRs in the 6-9% range, with used car loans pushing 7-10% or more.

- Fair (580-669): Borrowers in this range are considered "subprime." Lenders perceive a higher risk, and APRs will reflect this, often jumping into double digits. New car APRs could be 9-14%, and used car APRs could easily be 12-18% or higher.

- Poor (300-579): These borrowers are considered high-risk. While getting a loan is still possible, it will come with significantly higher APRs, often 15-25% or even more, making the car much more expensive over the loan term.

It’s clear that improving your credit score is one of the most effective ways to lower your car loan APR. Pro tips from us: Regularly check your credit report for errors and work on reducing existing debt, paying bills on time, and avoiding new credit applications before seeking a car loan.

How to Secure a Lower Car Loan APR

Now that you understand what an average APR for a car loan looks like and what factors influence it, let’s discuss actionable strategies to help you secure the lowest possible rate. Getting a favorable APR can save you thousands of dollars over the life of your loan.

Here are some proven methods:

1. Improve Your Credit Score Before You Apply

This is often the most impactful step. A few months of diligent credit repair can make a huge difference. Start by ordering your free credit report from AnnualCreditReport.com and checking it for inaccuracies. Dispute any errors immediately. Focus on paying all your bills on time, especially credit card payments, and try to pay down existing debt to lower your credit utilization ratio.

Even small improvements can bump you into a better credit tier, unlocking lower rates. This proactive approach shows lenders you’re a responsible borrower.

2. Shop Around for Pre-Approvals

Do not rely solely on the dealership for financing. Dealerships often mark up interest rates to increase their profit. Instead, apply for pre-approval from multiple lenders, such as your bank, a local credit union, and online lenders. Each application within a short timeframe (usually 14-45 days, depending on the credit scoring model) will only count as one hard inquiry for scoring purposes.

Getting pre-approved gives you a concrete offer with an APR before you even step foot in a dealership. This transforms you into a cash buyer, giving you significant negotiation power and a benchmark against which to compare any offers from the dealer.

3. Make a Larger Down Payment

As discussed, a larger down payment reduces the amount you need to borrow and signals financial stability. Aim for at least 20% of the car’s purchase price, if possible. Not only can this potentially lower your APR, but it also reduces your monthly payments and lessens the risk of being "upside down" on your loan (owing more than the car is worth).

This strategy is particularly effective for used cars, where depreciation is more rapid. A significant down payment helps to counteract some of the inherent risks lenders associate with used vehicle financing.

4. Choose a Shorter Loan Term

While a longer loan term means lower monthly payments, it almost always results in a higher APR and significantly more interest paid over time. If your budget allows, opt for the shortest loan term you can comfortably afford.

A 36 or 48-month loan term will generally come with a much lower APR than a 72 or 84-month term. Weigh the immediate relief of a lower monthly payment against the long-term cost savings of a shorter loan.

5. Consider a Co-signer (If Necessary)

If your credit score is less than ideal, or you’re a first-time borrower with limited credit history, a co-signer with excellent credit can help you secure a lower APR. A co-signer essentially guarantees the loan, taking on the responsibility for repayment if you default.

This significantly reduces the lender’s risk. However, be aware that the loan will appear on your co-signer’s credit report, and any missed payments will negatively impact both of your scores. This should only be considered with someone you trust implicitly, like a close family member.

6. Negotiate the APR (Even After Pre-Approval)

Even if you have a pre-approval, you can still try to negotiate the APR with the dealer or your chosen lender. If the dealer can’t beat your pre-approved rate, you can confidently go with your pre-approval. If they offer a slightly better rate, you might consider it.

Remember, everything is negotiable in the car-buying process. Don’t be afraid to ask for a lower rate or better terms.

7. Look for Manufacturer Incentives

For new cars, manufacturers sometimes offer special financing deals, such as 0% APR for a limited term, especially for highly qualified buyers. These deals can be incredibly attractive, but they are often reserved for those with excellent credit and may be offered in lieu of other rebates or cash-back incentives.

Always do the math to see if the 0% APR or a cash rebate would save you more money overall. Sometimes a cash rebate combined with a slightly higher APR from an external lender can be a better deal.

Common Mistakes to Avoid When Getting a Car Loan

Based on my years of observing consumers navigate the car-buying process, certain pitfalls repeatedly trip people up, leading to higher APRs and unnecessary costs. Being aware of these common mistakes can help you steer clear of them.

- Focusing Only on Monthly Payments: This is perhaps the biggest mistake. A low monthly payment might seem appealing, but if it’s achieved through a very long loan term and a high APR, you’ll end up paying significantly more in total interest. Always ask for the total cost of the loan.

- Not Getting Pre-Approved: Walking into a dealership without a pre-approval is like going to a battle without armor. You lose your negotiating power and are at the mercy of the dealer’s finance department.

- Ignoring the Total Cost of the Loan: Beyond the APR, consider all fees, the total interest paid over the life of the loan, and any additional products (like extended warranties or GAP insurance) that might be rolled into your financing, inflating the total.

- Extending Loan Terms Too Long: While an 84-month loan might offer a tempting low monthly payment, you risk being "upside down" on your loan for a significant period, meaning you owe more than the car is worth. You also pay substantially more in interest.

- Not Checking Your Credit Report: Errors on your credit report can unjustly raise your APR. Always review your report well in advance of applying for a loan.

- Buying More Car Than You Can Afford: Even with a low APR, buying a car that pushes your budget limits can lead to financial strain down the road. Stick to a budget that comfortably accommodates the monthly payment, insurance, and maintenance costs. For more tips on budgeting and finding the right car for your needs, check out our article on Choosing the Right Car for Your Lifestyle.

The Hidden Costs: Beyond the APR

While the APR is the most comprehensive measure of your loan’s cost, be mindful of other potential charges that might not be directly reflected in the APR itself but still add to your overall expense. These can include:

- Loan Origination Fees: A fee charged by the lender for processing your loan application.

- Documentation Fees: Fees charged by the dealership for preparing the paperwork.

- Prepayment Penalties: Some lenders charge a fee if you pay off your loan early. Always check for this clause.

- Optional Add-ons: Things like extended warranties, GAP insurance, or anti-theft devices can be rolled into your loan, increasing the principal amount and, consequently, the total interest you pay. While some of these might be valuable, always scrutinize them and consider purchasing them separately if needed, rather than financing them at your car loan APR. Our guide on Understanding Car Loan Add-Ons provides more insights.

Conclusion: Empowering Your Car Loan Journey

Understanding what an average APR for a car loan looks like and, more importantly, the factors that influence your specific rate, is the cornerstone of smart car buying. It’s not just about finding a car you love; it’s about financing it intelligently to save money over the long term. By taking a proactive approach – improving your credit, shopping around for lenders, and understanding all the terms – you empower yourself to make a financially sound decision.

Don’t let the complexity of auto financing intimidate you. With the insights provided in this comprehensive guide, you’re now equipped to approach your next car loan with confidence, secure a favorable APR, and drive away knowing you’ve made a smart financial move. Start your research today, compare offers diligently, and always prioritize the total cost of the loan over just the monthly payment. Your wallet will thank you!