Unlocking Your Credit Potential: The Definitive Guide on How to Add a Car Loan to Your Credit Report

Unlocking Your Credit Potential: The Definitive Guide on How to Add a Car Loan to Your Credit Report Carloan.Guidemechanic.com

As an expert in personal finance and a seasoned professional in SEO content, I’ve seen countless individuals navigate the complexities of credit building. One common question that often arises, particularly for those looking to establish or improve their financial standing, is how their car loan impacts their credit report. A car loan, when handled correctly, can be a powerful tool for building a robust credit history. But what happens when it doesn’t appear as it should?

This comprehensive guide will walk you through everything you need to know about car loans and your credit report. We’ll explore why your loan might not be showing up, how to ensure it gets reported, and the profound impact it can have on your credit score. Our ultimate goal is to empower you with the knowledge to proactively manage your financial reputation, ensuring your hard-earned payments contribute positively to your credit profile. Get ready to transform your understanding of auto loans and credit reporting!

Unlocking Your Credit Potential: The Definitive Guide on How to Add a Car Loan to Your Credit Report

The Foundation: How Car Loans Typically Interact with Your Credit Report

Before diving into solutions, it’s crucial to understand the standard operating procedure. When you secure a car loan from a legitimate financial institution, a process is set in motion that should naturally lead to it appearing on your credit report. This isn’t a passive event; it’s a deliberate system designed to track your borrowing behavior.

The Role of Lenders and Credit Bureaus

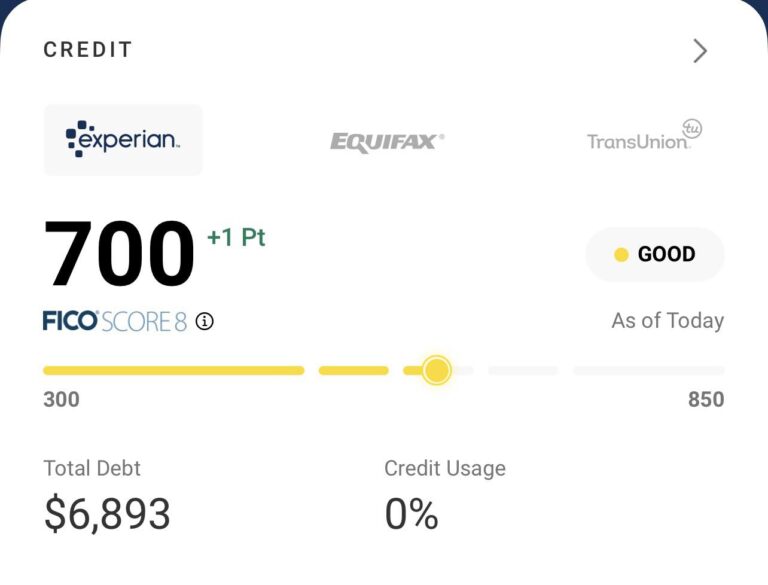

Most traditional lenders – banks, credit unions, and major auto finance companies – routinely report your loan activity to the three major credit bureaus: Experian, Equifax, and TransUnion. These bureaus are the central repositories of your credit history, collecting data from various creditors. This data includes details like the loan amount, the date it was opened, your payment history, and the loan’s current status.

Why This Reporting is Crucial

The information reported by your car loan lender directly influences your credit score. A history of timely payments on an installment loan like an auto loan demonstrates financial responsibility. It shows future lenders that you are a reliable borrower, capable of managing debt over time. Conversely, late payments or defaults can severely damage your credit standing, making it harder to obtain credit in the future.

Based on my experience, consistently making on-time payments on an auto loan is one of the most effective ways to build a positive credit history, especially for those new to borrowing or looking to diversify their credit mix. It acts as a verifiable testament to your reliability.

When Good Loans Go Missing: Why Your Car Loan Might Not Be on Your Credit Report

It can be incredibly frustrating to discover that a significant financial commitment, like your car loan, isn’t reflecting on your credit report. You’re making payments diligently, yet your efforts aren’t being acknowledged by the credit bureaus. There are several reasons why this might occur, and understanding them is the first step toward resolution.

1. It’s Too New to Appear

Credit reporting isn’t instantaneous. When you first take out a car loan, it can take anywhere from 30 to 90 days for the lender to process the initial information and report it to the credit bureaus. This delay is standard practice as they gather all necessary details and integrate your account into their reporting cycle. If your loan is very recent, patience might be the only requirement.

2. Your Lender Doesn’t Report to All Bureaus (or Any)

Not all lenders report to all three major credit bureaus, and some smaller lenders, or "buy here, pay here" dealerships, might not report to any at all. While most reputable financial institutions understand the importance of comprehensive reporting, it’s not a universal mandate. If your lender only reports to one or two bureaus, your loan might be missing from the others.

Common mistakes to avoid are assuming all lenders operate identically. Always clarify their reporting practices upfront, especially with non-traditional lenders.

3. Reporting Errors or Omissions

Human error or technical glitches can happen. Sometimes, a lender might simply make a mistake and fail to report your loan, or they might report incorrect information. This could be anything from a typo in your name or account number to an oversight that prevents the loan from being transmitted to the bureaus. Such errors are surprisingly common and require proactive intervention.

4. "Buy Here, Pay Here" Dealerships

Loans obtained from "buy here, pay here" dealerships often operate outside the traditional credit reporting system. These dealerships typically offer financing directly to consumers, often those with poor or no credit. While they provide an essential service for some, they frequently do not report payment activity to the major credit bureaus. This means your consistent on-time payments, while beneficial to the dealership, won’t help you build credit history with the broader financial world.

From my years of helping individuals navigate their finances, I’ve observed that while "buy here, pay here" loans can get you on the road, they rarely contribute to improving your credit score, which is a significant drawback for credit-building goals.

The Action Plan: How to Actively Ensure Your Car Loan is on Your Credit Report

If you’ve identified that your car loan is missing or inaccurately reported, it’s time to take action. This isn’t a passive waiting game; it requires you to be a proactive advocate for your financial data. Follow these steps meticulously to ensure your car loan contributes positively to your credit profile.

Step 1: Verify Your Credit Reports from All Three Bureaus

Your first and most crucial step is to obtain a copy of your credit report from each of the three major bureaus: Experian, Equifax, and TransUnion. This allows you to see exactly what information each bureau has on file for you.

- How to Get Them: The official, government-mandated website for free annual credit reports is AnnualCreditReport.com. You are entitled to one free report from each bureau every 12 months. Be wary of look-alike sites that try to charge you.

- What to Look For: Once you have your reports, carefully review each one. Look for a section dedicated to "Installment Accounts" or "Auto Loans." Check if your car loan is listed, and verify all the details: the lender’s name, account number, original loan amount, current balance, and payment history.

- Compare Reports: It’s essential to compare all three reports. It’s not uncommon for a loan to appear on one bureau’s report but be missing from another. This comparison will pinpoint exactly where the discrepancy lies.

Step 2: Contact Your Lender Directly

If your car loan is missing from one or all of your credit reports, your lender is your primary point of contact. They are the source of the information, and they have the power to correct any omissions or errors.

- Gather Information: Before you call, have all your loan details ready: your full name, account number, loan origination date, and the specific credit bureaus where the loan is missing.

- Initiate Contact: Call your lender’s customer service department. Clearly explain that your car loan is not appearing on your credit reports (or specific reports) and that you need them to investigate and report it accurately.

- Ask Key Questions:

- Do you report to Experian, Equifax, and TransUnion?

- When did you last report my account information?

- Can you confirm the account number and my personal details you are reporting?

- What is the process for ensuring my loan is reported?

- How long will it take for the correction to appear on my credit reports?

- Document Everything: Keep a detailed record of your communication: the date and time of your call, the name of the representative you spoke with, a summary of your conversation, and any reference numbers provided. This documentation is vital if further action is required.

Pro tips from us: Be persistent but polite. Sometimes, you may need to escalate your request to a supervisor if the initial representative is unable to assist.

Step 3: Understand Lender Reporting Policies and Cycles

During your conversation with the lender, try to gain clarity on their specific reporting policies. Some lenders report monthly, while others might do so less frequently, such as quarterly. Understanding this cycle will help you manage your expectations regarding when the loan might appear after a correction.

- Reporting Frequency: Inquire about their typical reporting schedule. Knowing this helps you anticipate when to check your credit reports again for updates.

- Which Bureaus: Reconfirm which credit bureaus they consistently report to. This information is crucial for future monitoring.

Step 4: If Your Lender Confirms Non-Reporting or You Encounter Resistance

What if your lender explicitly states they don’t report to certain bureaus, or you face resistance in getting an error corrected? This is where a more direct approach with the credit bureaus comes into play.

Option A: Dispute Inaccuracies Directly with the Credit Bureaus

If your lender is uncooperative, or if they claim they are reporting but the loan still isn’t showing up after a reasonable waiting period (e.g., 60-90 days), you can dispute the omission directly with the credit bureaus. This is your right under the Fair Credit Reporting Act (FCRA).

- Identify the Bureau(s): Pinpoint which specific credit report(s) are missing the car loan information.

- Gather Documentation: You’ll need evidence to support your claim. This includes:

- Copies of your credit reports showing the missing loan.

- Your car loan agreement.

- Proof of payments (bank statements, cancelled checks, payment confirmations).

- Any communication records with your lender (as documented in Step 2).

- Initiate the Dispute: Each credit bureau has its own dispute process, which can usually be done online, by mail, or by phone.

- Experian: experian.com/disputes/main.html

- Equifax: equifax.com/personal/credit-report-services/credit-dispute/

- TransUnion: transunion.com/credit-dispute/disputes

- Clearly State the Issue: In your dispute letter or online form, clearly state that your car loan is missing from your credit report and provide all supporting documentation. Request that the bureau investigate and add the account.

- Bureau Investigation: The credit bureau will then investigate your dispute, typically contacting your lender to verify the information. They usually have 30-45 days to complete their investigation and respond to you.

- Review Results: Once the investigation is complete, the bureau will send you the results. If they find an error, they will update your report. If they find no error, they will explain why.

For a more in-depth understanding of this process, you might find our article on "How to Dispute Errors on Your Credit Report" (simulated internal link) helpful.

The Profound Impact of a Car Loan on Your Credit Score

Once your car loan is accurately reported, its presence on your credit report can significantly influence your credit score. This influence can be either positive or negative, depending entirely on your payment behavior. Understanding this impact is key to leveraging your auto loan as a credit-building asset.

Positive Impacts:

- Payment History (35% of FICO Score): This is the most crucial factor. Consistently making on-time payments demonstrates reliability. Each on-time payment recorded on your credit report strengthens your payment history, which accounts for the largest portion of your FICO score.

- Credit Mix (10% of FICO Score): A car loan is an installment loan, meaning you borrow a fixed amount and repay it over a set period. Having a mix of different types of credit – like installment loans (car loans, mortgages) and revolving credit (credit cards) – can positively impact your score. It shows you can manage various forms of debt responsibly.

- Length of Credit History (15% of FICO Score): The older your accounts, the better. A car loan that remains open and in good standing for several years contributes positively to the average age of your credit accounts, which is a factor in your score.

Negative Impacts:

- Late Payments: Even a single late payment (typically 30 days or more past due) can severely damage your credit score. Lenders report these delinquencies to the credit bureaus, creating a negative mark that can stay on your report for up to seven years.

- Default and Repossession: If you fail to make payments and default on your loan, the car can be repossessed. Both the default and the repossession will be reported to the credit bureaus, causing significant and long-lasting damage to your credit score.

- High Debt-to-Income Ratio: While not directly a credit score factor, taking on too much car loan debt can impact your ability to get other loans. Lenders look at your debt-to-income (DTI) ratio to assess your capacity to take on more debt. A high DTI can signal financial strain.

Pro tips from us: Your car loan, when managed responsibly, is an excellent opportunity to build a strong credit foundation. However, vigilance is key, as missed payments can quickly undo months of positive progress.

Maintaining a Healthy Credit Profile with Your Car Loan

Getting your car loan on your credit report is just the first step. The real work—and the real credit-building benefit—comes from consistent, responsible management of that loan. Here’s how to maintain a healthy credit profile with your auto loan:

- Always Pay On Time: This cannot be stressed enough. Set up automatic payments from your checking account or calendar reminders to ensure you never miss a due date. Even a payment a few days late can affect your standing, though it’s typically reported as late if it’s 30 days or more past due.

- Pay More Than the Minimum (If Possible): While not directly impacting your credit score, paying extra on your principal balance can help you pay off the loan faster, reducing the total interest paid and freeing up your budget sooner.

- Monitor Your Credit Reports Regularly: Don’t just check once. Make it a habit to review your credit reports annually (or more frequently with free credit monitoring services). This allows you to catch any new errors, ensure your payments are being reported correctly, and track your progress.

- Avoid Taking on Excessive Debt: While a car loan is a good credit builder, don’t overextend yourself. Ensure your car payment is affordable within your budget. Stretching your finances too thin can lead to difficulties making payments, which ultimately harms your credit.

From my years of helping individuals navigate their finances, I’ve seen that proactive monitoring is the hallmark of a financially responsible individual. It’s your financial health check-up!

Common Myths and Misconceptions About Car Loans and Credit

The world of credit is rife with myths. Let’s debunk a few common misconceptions surrounding car loans and their impact on your credit report.

- Myth 1: Paying off a car loan early always gives a huge credit score boost.

- Reality: While paying off debt is generally good, paying an installment loan off significantly early might not always provide a dramatic score boost. The benefit often comes from the consistent, on-time payments over the entire loan term. Closing an account prematurely might slightly reduce the average age of your accounts, which could have a minor, temporary negative effect, though the overall benefit of being debt-free usually outweighs this.

- Myth 2: A car loan is "bad debt" and should be avoided at all costs.

- Reality: Debt isn’t inherently good or bad; it’s about how it’s managed. A car loan, like a mortgage, is an installment loan that can be "good debt" if used responsibly. It allows you to acquire an asset (a vehicle) that may be necessary for work or life, while simultaneously building a positive credit history through timely payments.

- Myth 3: Only major banks report car loans to credit bureaus.

- Reality: While major banks and captive finance companies (like Toyota Financial Services or Ford Credit) certainly report, many credit unions, smaller regional banks, and even some reputable online lenders also report to the credit bureaus. The key is to verify their reporting practices before you sign on the dotted line.

Advanced Strategies & Considerations

Beyond the basics, there are a few advanced scenarios and considerations related to car loans and your credit report.

"Buy Here, Pay Here" Dealerships Revisited

As mentioned, many "buy here, pay here" lots do not report to credit bureaus. If you have a loan with one of these dealerships and are committed to building credit, you might consider:

- Inquiring Directly: Ask if they can or will report your payments to any bureau. Some may, especially if you have an excellent payment history with them.

- Refinancing: After a period of consistent payments, you might qualify for a traditional auto loan from a bank or credit union. Refinancing your "buy here, pay here" loan into a traditional loan could then allow your payments to be reported and start building your credit.

The Role of Co-Signers

If you co-signed a car loan for someone else, that loan will appear on your credit report as well. This means their payment history directly impacts your credit score. If they make late payments or default, your credit will suffer. Always be fully aware of the risks before co-signing any loan.

Refinancing Your Car Loan

Refinancing an existing car loan can have several credit implications:

- New Hard Inquiry: The application for a new loan will result in a hard inquiry on your credit report, which can temporarily dip your score by a few points.

- Account Closure: Your old loan account will be closed, which might slightly reduce the average age of your credit accounts.

- New Account Opened: A new loan account will be opened, which starts a new payment history. If you get a better interest rate or lower monthly payments, it can make managing the debt easier, indirectly benefiting your credit by reducing the likelihood of missed payments.

For further insights into managing your overall debt load, consider reading our post on "Understanding Your Debt-to-Income Ratio" (simulated internal link).

To understand more about your rights regarding credit reporting and disputes, a trusted external source is the Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov. Their website offers a wealth of unbiased information.

Conclusion: Your Proactive Stance is Your Greatest Asset

Ensuring your car loan is accurately reflected on your credit report is not just about a technicality; it’s about claiming the credit you deserve for your financial responsibility. A car loan, when handled correctly, is a powerful credit-building tool, capable of significantly boosting your credit score and opening doors to better financial opportunities.

Remember, your credit report is a living document, and you are its primary guardian. By proactively monitoring your reports, understanding your lender’s policies, and taking swift action to correct any discrepancies, you empower yourself to build a robust and reliable credit profile. Don’t let your diligent payments go unnoticed; take charge of your credit today and drive towards a stronger financial future.