Unlocking Your Dream Car: A Comprehensive Guide to Car Loans with a 746 Credit Score

Unlocking Your Dream Car: A Comprehensive Guide to Car Loans with a 746 Credit Score Carloan.Guidemechanic.com

Securing a car loan is a significant financial step, and your credit score plays a pivotal role in determining the terms you’ll receive. If you’re reading this, chances are you have a 746 credit score – and that’s fantastic news! This score places you firmly in the "very good" to "excellent" credit range, opening doors to some of the most favorable car loan options available.

But what exactly does a 746 credit score mean for your car buying journey? How can you leverage this excellent standing to get the best possible deal? This comprehensive guide will walk you through everything you need to know, from understanding your score’s power to navigating the application process and securing your dream car with confidence.

Unlocking Your Dream Car: A Comprehensive Guide to Car Loans with a 746 Credit Score

Understanding Your 746 Credit Score: A Foundation of Trust

A 746 credit score is a strong indicator of financial responsibility. It tells lenders that you have a proven track record of managing debt wisely, making payments on time, and generally being a low-risk borrower. This isn’t just a number; it’s a testament to your financial discipline.

What Does a 746 Score Really Mean?

In the most common FICO and VantageScore models, a 746 score typically falls into the "Very Good" category, sometimes even bordering on "Excellent." While specific ranges can vary slightly between models, this score consistently signals to lenders that you are a highly desirable applicant. You’ve demonstrated a strong ability to handle credit, which translates directly into better loan terms.

Lenders view borrowers with scores in this range as reliable. They are confident you will repay your loan as agreed, significantly reducing their risk. This confidence is precisely why they are willing to offer you more attractive interest rates and more flexible repayment options.

The Benefits of This Score for Car Loans

Having a 746 credit score gives you a distinct advantage when applying for an auto loan. The most significant benefit is access to lower interest rates. Even a fraction of a percentage point can save you hundreds, if not thousands, of dollars over the life of a car loan.

Beyond interest rates, this score often means you’ll encounter less stringent requirements for down payments. You might also be approved for higher loan amounts, giving you more flexibility in your car choice. Furthermore, the application process itself can be smoother and quicker, as lenders are eager to approve well-qualified borrowers.

How Credit Scores Are Calculated (Briefly)

Your credit score is a dynamic number influenced by several key factors. While you don’t need to be an expert in credit scoring algorithms, understanding the basics can help you maintain your excellent score. Payment history, which accounts for about 35% of your score, is paramount – consistent on-time payments are crucial.

Credit utilization, or the amount of credit you’re using compared to your available credit, makes up around 30%. Keeping this low (ideally under 30%) is beneficial. The length of your credit history (15%), new credit (10%), and credit mix (10%) also play significant roles. Your 746 score suggests you’re managing these factors effectively.

The Power of a 746 Score in Auto Financing

Your 746 credit score is a powerful tool in the car loan market. It provides you with leverage that many other borrowers simply don’t have. Let’s explore how this score translates into tangible benefits for your auto financing.

Expected Interest Rates: What You Can Anticipate

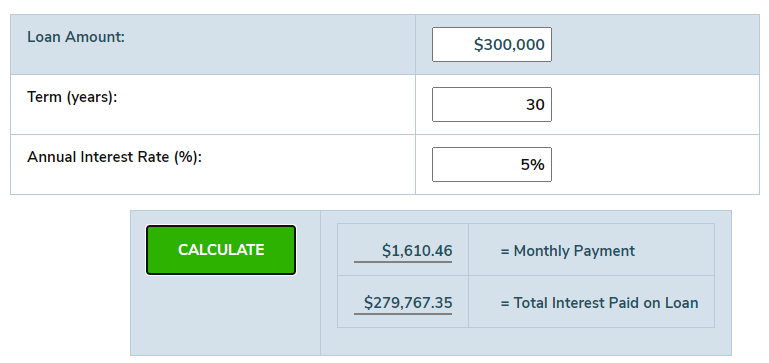

With a 746 credit score, you’re positioned to receive some of the most competitive interest rates available. While rates fluctuate based on market conditions, the specific lender, and the loan term, you should generally expect offers in the low single digits. For example, it’s not uncommon for borrowers with this score to qualify for rates between 3% and 6% APR, and sometimes even lower, depending on current economic factors and promotions.

Based on my experience, consistently shopping around is key, even with an excellent score. Don’t just accept the first offer. Different lenders have varying risk assessments and promotional rates, so comparing multiple offers ensures you truly get the best deal for your financial profile.

Loan Terms and Flexibility

A strong credit score also grants you greater flexibility with loan terms. Lenders might be more willing to offer longer repayment periods (e.g., 60, 72, or even 84 months) with lower monthly payments, or shorter terms with higher payments if you prefer to pay off the loan quicker and save on total interest. However, a pro tip from us is to be cautious with very long terms. While they reduce monthly payments, they significantly increase the total interest paid over the life of the loan and can lead to negative equity sooner.

You’ll also find that lenders are more amenable to approving loans for a wider range of vehicles, including newer or more expensive models, without requiring an excessive down payment. Your 746 score provides that layer of trust.

Down Payment Considerations

While your excellent credit score might reduce the necessity of a large down payment, making one is still a smart financial move. A substantial down payment reduces the amount you need to borrow, which directly translates to lower monthly payments and less interest paid over time. It also helps you avoid being "upside down" on your loan, where you owe more than the car is worth, especially in the early years of ownership.

Even with a 746 score, consider putting down at least 10-20% of the car’s purchase price if your budget allows. This strategy not only saves you money but also provides a buffer against depreciation.

Negotiating Power

Your high credit score is a significant negotiating asset. When a dealership knows you’re pre-approved for an excellent rate from an external lender, they’re often more motivated to match or even beat that offer to keep your business in-house. This competition works entirely in your favor.

Don’t be afraid to use your pre-approval as leverage. It demonstrates that you’re a serious buyer with solid financing options already secured. This puts you in a strong position to negotiate both the vehicle’s price and the financing terms simultaneously.

Preparing for Your Car Loan Application

Even with a stellar 746 credit score, preparation is crucial. A well-prepared applicant is a confident applicant, and confidence often leads to better outcomes. Taking a few proactive steps before you even set foot in a dealership can streamline the entire process.

Checking Your Credit Report

Before applying for any significant loan, always pull your full credit report from all three major bureaus: Experian, TransUnion, and Equifax. You can do this for free once a year through AnnualCreditReport.com. While your score is excellent, it’s essential to ensure there are no errors or fraudulent activities that could unexpectedly impact your application.

Identify any discrepancies, even minor ones. If you find an error, dispute it immediately. Clearing up inaccuracies ensures that lenders see the most accurate representation of your financial health. This step is a cornerstone of responsible financial planning.

Gathering Necessary Documents

Having all your paperwork in order beforehand will make the application process much smoother. Lenders will typically require:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2 forms, or tax returns if self-employed.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Insurance Information: You’ll need proof of auto insurance before driving off the lot.

Having these documents readily available will prevent delays and show lenders you are organized and serious.

Determining Your Budget

Knowing how much car you can truly afford is paramount. Don’t just focus on the maximum loan amount you’re approved for. Consider your overall financial picture, including all your monthly expenses, savings goals, and other debt obligations.

Calculate your debt-to-income (DTI) ratio. This is your total monthly debt payments divided by your gross monthly income. Lenders often prefer a DTI below 36%, though with a 746 score, you might have more leeway. A good rule of thumb is to keep your total car expenses (payment, insurance, fuel, maintenance) to no more than 10-15% of your take-home pay.

Pre-Approval vs. Applying at the Dealership

This is one of the most critical decisions you’ll make. Getting pre-approved for a loan before you visit a dealership is highly recommended. Pre-approval means a lender has reviewed your financial information and provisionally agreed to lend you a specific amount at a particular interest rate.

Having a pre-approval gives you immense power. It establishes a benchmark for the interest rate you’re willing to accept, allowing you to negotiate the car’s price separately from the financing. If you apply at the dealership first, you risk getting caught up in a "four-square" negotiation where they bundle the car price, trade-in, down payment, and monthly payment all together, making it difficult to discern the true cost of each component.

Finding the Right Lender

Your 746 credit score makes you an attractive client for a wide range of lenders. Exploring different types of institutions will help you uncover the most competitive rates and terms.

Banks (National and Local)

Traditional banks are a common source for auto loans. Large national banks often have established auto loan divisions and competitive rates, especially for prime borrowers like yourself. Local banks might offer more personalized service and sometimes have unique promotions for their account holders.

It’s always a good idea to check with your current bank, as they might offer loyalty discounts or streamlined application processes.

Credit Unions (Often Competitive Rates)

Credit unions are member-owned financial cooperatives, and they are frequently lauded for offering some of the most competitive auto loan rates. Because they are non-profit organizations, their primary goal is to serve their members, often translating into lower interest rates and fees compared to traditional banks.

Even if you’re not currently a member, many credit unions have easy eligibility requirements, such as living in a specific geographic area or working for a particular employer. It’s definitely worth exploring credit unions in your area.

Online Lenders (Convenience and Speed)

The digital age has brought forth a plethora of online lenders specializing in auto financing. These lenders often boast quick application processes, instant decisions, and highly competitive rates due to their lower overhead costs. Websites like LightStream, Capital One Auto Finance, and others are popular choices.

Online lenders offer unparalleled convenience, allowing you to shop for rates from the comfort of your home. This can be a great way to secure multiple pre-approvals without visiting various physical locations.

Dealership Financing (Convenience, But Compare Rates)

Dealerships often offer financing through their network of partner lenders. This can be convenient, as it’s a one-stop shop for buying and financing your car. However, it’s crucial to approach dealership financing with caution. While they might sometimes offer attractive promotional rates, they also have an incentive to maximize their profit on the financing.

Common mistakes to avoid include letting the dealership run your credit with multiple lenders without your explicit permission, which can lead to unnecessary hard inquiries. Always arrive at the dealership with a pre-approval in hand to use as a baseline for comparison.

The Application Process: What to Expect

Once you’ve chosen your car and decided on a lender, the application process itself is usually straightforward for someone with a 746 credit score. Knowing what to expect can ease any anxieties.

Filling Out the Application

Whether online or in person, the loan application will request personal information (name, address, Social Security Number), employment details, income, and existing debt obligations. Be prepared to provide all the documents you gathered in your preparation phase. Accuracy is key here; double-check all information before submitting.

Lenders will perform a "hard inquiry" on your credit report when you formally apply for a loan. This inquiry can cause a slight, temporary dip in your credit score. However, credit scoring models are designed to recognize rate shopping for auto loans, so multiple inquiries for the same type of loan within a short period (typically 14-45 days, depending on the model) are often treated as a single inquiry.

Understanding Loan Offers

Once approved, you’ll receive a loan offer detailing the Annual Percentage Rate (APR), the loan term (number of months), and your estimated monthly payment. The APR is crucial as it represents the true cost of borrowing, including interest and any fees. Don’t just look at the monthly payment; compare the total cost of the loan over its entire term.

A pro tip from us is to create a spreadsheet comparing offers from different lenders. Look at the APR, total interest paid, and any origination fees. This holistic view will help you make the most financially sound decision.

Reading the Fine Print

Never sign any loan documents without thoroughly reading and understanding them. Pay close attention to:

- Prepayment Penalties: Some loans charge a fee if you pay off the loan early. With your credit score, you should be able to avoid these.

- Late Payment Fees: Understand the grace period and associated charges.

- Default Clauses: What constitutes a default and the consequences.

- Any additional fees: Ensure there are no hidden costs.

If anything is unclear, ask for clarification. A reputable lender will be happy to explain all terms and conditions.

Maximizing Your Approval & Loan Terms

Even with a strong 746 credit score, there are strategies you can employ to further enhance your loan approval chances and secure the most favorable terms possible.

A Healthy Down Payment

As discussed, a substantial down payment signals to lenders that you’re serious about your commitment. It reduces their risk and can sometimes lead to an even lower interest rate, even if your score is already excellent. Aim for at least 10-20% if feasible.

This also gives you a buffer against depreciation, helping to prevent you from being "upside down" on your loan.

Trade-In Value

If you have a car to trade in, its value can act like an additional down payment. Research your car’s trade-in value using resources like Kelley Blue Book (KBB) or Edmunds before you go to the dealership. Knowing its worth puts you in a stronger negotiating position.

Be prepared to negotiate the trade-in value separately from the new car’s price and financing.

Having a Co-signer (Usually Not Needed, But an Option)

With a 746 credit score, a co-signer is almost certainly unnecessary. However, if for some reason you’re looking for an even lower rate or a significantly larger loan amount than you’re pre-approved for, a co-signer with an equally strong or stronger credit profile could potentially help. This is a rare scenario for someone with your excellent score.

Only consider a co-signer if there’s a specific, compelling reason, as it ties their credit to your loan.

Negotiating the Car Price Separately from the Loan

Based on my experience, this is perhaps the single most important piece of advice for car buyers. Always negotiate the car’s purchase price first, as if you were paying cash. Once you’ve agreed on a price, then discuss financing.

This strategy prevents the "payment packing" tactic where dealerships manipulate various figures to make a higher car price or less favorable loan terms seem acceptable by focusing solely on a palatable monthly payment. Your pre-approval acts as your shield here.

Common Pitfalls and How to Avoid Them

Even smart borrowers with excellent credit can fall victim to common traps if they’re not vigilant. Knowing what to watch out for will protect your wallet and your peace of mind.

Getting Lured by Extended Warranties or Add-ons

Dealerships often push extended warranties, GAP insurance, paint protection, or other add-ons. While some of these might offer value, many are overpriced or unnecessary. Do not feel pressured to purchase them on the spot. Research their true cost and benefit before committing.

You can often buy extended warranties directly from manufacturers or third-party providers at a lower cost. GAP insurance, while valuable, can sometimes be purchased more affordably from your auto insurer.

Focusing Only on the Monthly Payment

This is the most common mistake buyers make. A low monthly payment might seem appealing, but it can hide a longer loan term, a higher interest rate, or a higher overall car price. Always look at the total cost of the loan, including all interest and fees, over its entire duration.

A lower monthly payment is only a good deal if it also means a lower total cost or fits genuinely within your budget for a reasonable term.

Ignoring the Total Cost of the Loan

As mentioned, the total cost of the loan (principal + interest + fees) is your ultimate financial responsibility. A $25,000 car financed at 5% over 60 months will cost significantly less in total than the same car financed at 7% over 72 months, even if the latter has a slightly lower monthly payment. Use online loan calculators to run different scenarios.

This comprehensive view helps you make an informed decision that aligns with your long-term financial goals.

Multiple Hard Inquiries in a Short Period

While credit models are forgiving for rate shopping within a specific window, unnecessary hard inquiries can still impact your score. Avoid letting multiple dealerships or lenders run your credit without a clear purpose. Stick to getting a few pre-approvals from different types of lenders (banks, credit unions, online) and then using those to compare.

Common mistake to avoid: Don’t let every dealership you visit "check your rate" unless you intend to finance through them and have agreed on a specific vehicle and price.

After Approval: What Next?

Congratulations, you’ve secured your car loan! But the journey doesn’t end there. A few final steps ensure a smooth transition and help you maintain your excellent financial standing.

Understanding Your Loan Documents

Before you drive off the lot, ensure you have copies of all signed loan documents. Review them one last time to confirm that the agreed-upon terms (APR, loan amount, term, monthly payment) are accurately reflected. If you spot any discrepancies, address them immediately.

These documents are your legal agreement with the lender, so keep them safe and accessible.

Setting Up Payments

Most lenders offer various payment options:

- Automatic Payments: Often the easiest way to ensure on-time payments, sometimes with a small interest rate discount.

- Online Portal: Manage your account and make payments digitally.

- Mail or Phone: Traditional methods are usually available.

Choose the method that works best for you, but prioritize consistency to protect your credit score.

Maintaining Your Excellent Credit Score

Your 746 credit score is an asset; continue to nurture it. Make all your car loan payments on time, every time. This consistent positive payment history will reinforce your strong credit profile. Keep your credit utilization low on other credit lines and continue to monitor your credit report periodically for any changes.

for more in-depth tips on credit maintenance.

Consider Refinancing in the Future (Though Less Likely)

With a 746 score, you’re likely getting a very competitive rate upfront, so refinancing might not be necessary. However, if interest rates drop significantly, or if your credit score improves even further (e.g., into the 800s), you could potentially refinance to an even lower rate. This is less common for prime borrowers but always an option to keep in mind.

It’s also an option if your financial situation changes, and you need to adjust your monthly payments.

Conclusion: Your 746 Score – A Gateway to Opportunity

Your 746 credit score is a powerful financial asset, particularly when it comes to securing a car loan. It positions you as a low-risk, highly desirable borrower, granting you access to lower interest rates, flexible terms, and increased negotiating power. By understanding your score, thoroughly preparing for the application process, and wisely navigating the lending landscape, you can ensure a smooth, cost-effective car buying experience.

Remember to leverage your pre-approval, compare offers diligently, and always focus on the total cost of the loan, not just the monthly payment. Armed with this knowledge and your excellent credit, you’re not just buying a car; you’re making a smart financial decision that will serve you well for years to come.

Ready to take the wheel? Start comparing loan offers today and drive away with confidence! For more tips on making smart car-buying decisions, check out our article on . And for general credit score information, a great external resource is the Consumer Financial Protection Bureau (CFPB) website, which offers unbiased advice on managing your finances. .