Unlocking Your Dream Car: A Deep Dive into the 744 Credit Score Car Loan Advantage

Unlocking Your Dream Car: A Deep Dive into the 744 Credit Score Car Loan Advantage Carloan.Guidemechanic.com

Securing a car loan is a significant financial step for many, and your credit score plays a pivotal role in the entire process. If you’re reading this, chances are you’re sitting on a powerful asset: a 744 credit score. This isn’t just a number; it’s a golden ticket to some of the most favorable car loan terms available. In this comprehensive guide, we’ll explore exactly what a 744 credit score means for your car buying journey, how to leverage it, and what steps to take to ensure you drive away with the best possible deal.

Understanding the landscape of a 744 credit score car loan is about more than just getting approved. It’s about optimizing interest rates, negotiating power, and overall financial savvy. We’ll delve into the nuances of lender expectations, the power of pre-approval, and critical strategies to maximize your excellent credit. Prepare to become an expert in using your 744 credit score to your ultimate advantage in the car market.

Unlocking Your Dream Car: A Deep Dive into the 744 Credit Score Car Loan Advantage

What Does a 744 Credit Score Really Mean for Car Loans?

A 744 credit score places you firmly in the "Very Good" to "Excellent" category, depending on the specific credit scoring model used. This is a fantastic position to be in when seeking a car loan. Lenders view scores in this range as indicative of a highly responsible borrower with a strong history of managing debt effectively.

From years of helping individuals navigate the complexities of auto financing, what we’ve seen consistently is that a score like 744 signals reliability. It tells potential lenders that you pose a very low risk of default. This perception of low risk directly translates into tangible benefits for you, the borrower.

Essentially, your 744 credit score opens doors that remain closed for those with lower scores. It’s not just about approval; it’s about accessing the most competitive interest rates and flexible terms available in the market.

The Golden Ticket: Unlocking Prime Interest Rates with a 744 Score

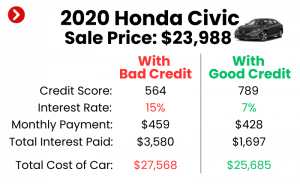

One of the most significant advantages of a 744 credit score for a car loan is access to the absolute best interest rates. Lenders reserve their lowest Annual Percentage Rates (APRs) for borrowers with excellent credit profiles. Your 744 score positions you perfectly to receive these prime rates.

Even a small difference in your interest rate can save you hundreds, if not thousands, of dollars over the life of your loan. For instance, reducing your APR by just one or two percentage points on a $30,000, 60-month loan can lead to substantial savings. This is where your strong credit score truly shines.

Pro tips from us: Don’t just settle for the first offer you receive, even if it seems good. With a 744 credit score, you have the leverage to shop around aggressively for the absolute lowest rate. Your goal should be to secure an interest rate that reflects your impeccable credit standing.

Preparing for Your Car Loan Journey: Beyond the Score

While a 744 credit score is a tremendous asset, it’s just one piece of the puzzle. Thorough preparation is key to a smooth and successful car loan experience. Taking these steps before you even set foot in a dealership will empower you significantly.

1. Know Your Budget Inside and Out

Before you start eyeing that shiny new vehicle, understand your financial boundaries. Your budget should encompass more than just the monthly car payment. Consider insurance costs, fuel, maintenance, and potential registration fees.

Based on my experience, many people focus solely on the monthly payment, overlooking the total cost of ownership. A comprehensive budget prevents you from being "house poor" with your car. Factor in your current debt obligations and ensure the new car payment fits comfortably without straining your finances.

2. Check Your Credit Report for Accuracy

Even with an excellent score like 744, errors on your credit report can occur. These inaccuracies, though rare for high scorers, could potentially affect your loan terms or even your eligibility. It’s always wise to review your report thoroughly.

You can obtain a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once every 12 months. Visit AnnualCreditReport.com to access yours. Scrutinize every entry for any discrepancies, outdated information, or signs of identity theft. If you find errors, dispute them immediately to ensure your credit profile is flawless.

3. Gather Essential Documentation

Lenders will require certain documents to process your loan application. Having these ready in advance can significantly speed up the approval process. This proactive approach demonstrates your readiness and seriousness as a borrower.

Typically, you’ll need:

- Proof of identity (driver’s license, state ID)

- Proof of residence (utility bill, lease agreement)

- Proof of income (pay stubs, tax returns if self-employed)

- Social Security number

- Information about your current employment

Having these documents organized and accessible shows lenders you are prepared, which can contribute to a smoother application experience.

4. Strategize Your Down Payment

Even with a strong 744 credit score, a down payment is a powerful tool. It reduces the total amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the loan term. A significant down payment also reduces the loan-to-value (LTV) ratio, making your loan more attractive to lenders.

While not always strictly necessary with excellent credit, a down payment can offer additional benefits. It provides you with immediate equity in the vehicle, and in some cases, can even unlock slightly better interest rates. Consider how much you can comfortably put down without depleting your emergency savings.

The Pre-Approval Advantage with Your 744 Credit Score

One of the smartest moves you can make with a 744 credit score is to get pre-approved for a car loan. Pre-approval means a lender has reviewed your financial information and tentatively agreed to lend you a specific amount at a particular interest rate, before you even choose a car. This process is incredibly empowering.

Why is pre-approval so crucial for buyers with excellent credit? It transforms you into a cash buyer at the dealership. You walk in knowing exactly how much you can spend and what your interest rate will be. This removes the uncertainty and allows you to focus solely on negotiating the vehicle’s price, rather than getting entangled in financing discussions with the salesperson.

Common mistakes to avoid are going to the dealership without pre-approval and letting them dictate the financing terms. Pre-approval shifts the power dynamic firmly into your favor. Remember, multiple pre-approval inquiries within a short period (typically 14-45 days, depending on the scoring model) are usually treated as a single hard inquiry, minimizing the impact on your score.

Choosing the Right Lender: Options for Excellent Credit

With a 744 credit score, you have a wide array of lending options, each with its own set of advantages. Shopping around is paramount to securing the best deal. Don’t limit yourself to just one type of lender.

- Dealership Financing: While convenient, dealership financing often includes a markup on the interest rate. They act as intermediaries, connecting you with various lenders. With your 744 score, you can often negotiate these rates down, especially if you have a pre-approval in hand.

- Banks and Credit Unions: These institutions are often a fantastic source for competitive auto loan rates. Credit unions, in particular, are member-owned and frequently offer some of the lowest rates. If you’re a member of a credit union, start there.

- Online Lenders: The digital landscape has brought forth many reputable online lenders specializing in auto loans. They offer convenience, quick approvals, and often highly competitive rates due to lower overheads. Exploring these options can be very beneficial.

Our experts often advise applying to 3-5 different lenders (including a mix of banks, credit unions, and online providers) to compare offers side-by-side. This competitive process is your best strategy for securing the lowest possible interest rate on your 744 credit score car loan.

Key Factors Lenders Consider (Even with a 744 Score)

While your 744 credit score is a significant factor, lenders look at a holistic view of your financial health. Understanding these additional considerations will help you present the strongest possible application.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. Lenders prefer a lower DTI, typically below 43%, as it indicates you have sufficient income to manage new debt. Even with excellent credit, a high DTI can make lenders hesitant.

- Loan-to-Value (LTV) Ratio: This ratio compares the amount you want to borrow to the car’s actual value. A lower LTV (meaning you’re borrowing less relative to the car’s worth, often due to a down payment) reduces the lender’s risk. A low LTV can sometimes lead to slightly better rates.

- Loan Term: The length of your loan (e.g., 36, 60, 72 months) impacts your monthly payment and the total interest paid. Shorter terms mean higher monthly payments but less interest. Longer terms reduce monthly payments but accrue more interest over time. Lenders consider the term when assessing risk.

- Vehicle Type and Age: The specific car you choose also plays a role. Newer, more reliable vehicles are generally seen as less risky collateral than older, high-mileage cars. This is because the resale value and likelihood of costly repairs are different.

Navigating the Car Buying Process with Confidence

Armed with your 744 credit score and pre-approval, you’re ready to tackle the dealership. This is where your preparation truly pays off, allowing you to negotiate from a position of strength.

1. Negotiating the Car Price Separately

Never discuss financing until you have firmly agreed on the car’s purchase price. This is a common tactic dealerships use to confuse buyers. With pre-approval, you can tell the salesperson you’re a cash buyer and focus solely on getting the best price for the vehicle itself. This separation prevents them from "packing" the deal with hidden fees or higher interest rates.

For more insights on negotiating car prices, check out our guide on ‘Smart Car Buying Strategies’.

2. Understanding Loan Offers: APR vs. Interest Rate

When reviewing loan offers, always focus on the Annual Percentage Rate (APR), not just the stated interest rate. The APR includes the interest rate plus any additional fees charged by the lender, giving you the true cost of borrowing. It’s the most accurate metric for comparing different loan offers.

Make sure you fully understand all the terms and conditions. Read the fine print carefully before signing anything. This diligence ensures there are no surprises down the road.

3. The Power of Walking Away

Your ultimate leverage in any negotiation, especially with a strong 744 credit score, is your willingness to walk away. If a dealership isn’t meeting your expectations on price or trying to push unfavorable financing, simply leave. There are plenty of other dealerships and cars available. This power sends a clear message and often leads to better offers.

Making Your 744 Score Even Stronger (Future Proofing)

While a 744 is an excellent score, there’s always room to maintain it or even push it higher. Consistent good financial habits will ensure your credit remains stellar for future endeavors.

- Maintain a Perfect Payment History: Always pay all your bills on time, every time. Payment history is the single most important factor in your credit score.

- Keep Credit Utilization Low: Aim to use less than 30% of your available credit on credit cards. Lower is always better.

- Avoid Unnecessary New Debt: While a car loan is a good debt, avoid opening multiple new credit lines simultaneously, as this can temporarily dip your score.

- Monitor Your Credit Regularly: Keep an eye on your credit reports and scores to catch any changes or potential issues quickly.

If you’re interested in boosting your credit further, read our article on ‘Advanced Credit Score Improvement Techniques’. Maintaining a high credit score is a continuous effort that yields significant financial rewards.

Common Pitfalls to Avoid with Your 744 Credit Score

Even with excellent credit, certain mistakes can undermine your advantage. Be vigilant and avoid these common pitfalls:

- Not Shopping Around for Loans: This is perhaps the biggest mistake. Assuming the first offer is the best because you have good credit can cost you money. Always compare multiple pre-approvals.

- Focusing Only on Monthly Payments: Dealerships might try to stretch your loan term to lower the monthly payment, but this significantly increases the total interest paid. Always consider the total cost of the loan.

- Ignoring the Fine Print: Never sign a document you haven’t thoroughly read and understood. Look for hidden fees, prepayment penalties, or unfavorable clauses.

- Letting the Dealer Run Multiple Hard Inquiries: While rate shopping inquiries are often grouped, unnecessary multiple hard inquiries can slightly ding your score. Stick to your pre-approvals and only allow a hard pull for the lender you choose.

- Impulse Buying: Even with great credit, buying a car you haven’t researched or can’t truly afford long-term is a recipe for regret. Take your time and make an informed decision.

Conclusion: Drive Away Confidently with Your 744 Credit Score Car Loan

A 744 credit score is a powerful asset that places you in an enviable position when seeking a car loan. It signifies financial responsibility and opens the door to the most competitive interest rates and favorable terms available. By understanding its implications, preparing thoroughly, and adopting savvy negotiation tactics, you can maximize your excellent credit to secure an outstanding deal.

Remember, your 744 credit score car loan journey isn’t just about approval; it’s about empowerment. Leverage pre-approval, shop multiple lenders, separate your car price negotiation from financing, and always understand the true cost of your loan. With this comprehensive knowledge, you’re not just buying a car; you’re making a smart financial decision that will serve you well for years to come. Drive away with confidence, knowing you’ve secured the best possible financing for your dream vehicle.