Unlocking Your Dream Car: The Ultimate Guide to a Free Car Loan Calculator With Tax

Unlocking Your Dream Car: The Ultimate Guide to a Free Car Loan Calculator With Tax Carloan.Guidemechanic.com

Buying a car is an exciting milestone, but the financial aspect can often feel like navigating a complex maze. Beyond the sticker price, a myriad of costs can quickly inflate your monthly payments and overall expenditure. Many aspiring car owners make the mistake of overlooking crucial elements like taxes and various fees, leading to budget surprises down the road. This is precisely why a Free Car Loan Calculator With Tax isn’t just a convenience; it’s an indispensable tool for smart car financing.

In this comprehensive guide, we’ll dive deep into understanding every facet of car loan calculation. We’ll explore why including taxes and fees is non-negotiable, how these calculators empower you, and most importantly, how to use them effectively to secure your dream car without financial strain. Get ready to transform from a bewildered buyer into a savvy car owner!

Unlocking Your Dream Car: The Ultimate Guide to a Free Car Loan Calculator With Tax

Understanding the True Cost of Your Car Loan: Beyond the Sticker Price

When you first eye that gleaming new vehicle, your mind often jumps straight to the advertised price. However, the sticker price is merely the tip of the iceberg. There are many layers of costs that contribute to the total amount you’ll finance and, subsequently, your monthly payments. Ignoring these additional charges is a common pitfall.

A simple car loan calculator, while helpful, often falls short by not factoring in these crucial elements. It might give you an estimate based purely on the vehicle’s price, your down payment, interest rate, and loan term. This creates an incomplete picture, potentially leading to a significant discrepancy between your initial budget and the actual amount you need to borrow. The true cost of your car extends far beyond the dealership’s asking price.

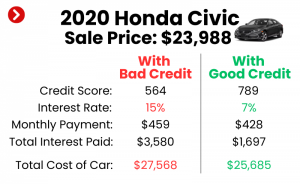

The crucial role of taxes and fees cannot be overstated. These are mandatory charges imposed by government entities and dealerships that directly impact your total loan amount. Without accounting for them, your monthly payment estimate will be inaccurate, making effective budgeting nearly impossible. This is why a specialized calculator that includes these factors is so vital.

Accurate budgeting is the cornerstone of responsible car ownership. Knowing the exact total loan amount, including all taxes and fees, allows you to set realistic financial goals. It prevents unpleasant surprises at the dealership, empowering you to negotiate with confidence and ensure your car purchase aligns perfectly with your financial health.

What is a Free Car Loan Calculator With Tax and Why Do You Need One?

At its core, a Free Car Loan Calculator With Tax is an online tool designed to provide a highly accurate estimate of your potential car loan payments. Unlike basic calculators, it incorporates the significant impact of sales tax, registration fees, and other mandatory charges into the overall loan amount. This comprehensive approach gives you a much clearer financial forecast.

The "tax" component in these calculators is incredibly important. It primarily refers to sales tax, which is levied by state and local governments on the purchase price of your vehicle. This tax can vary significantly from state to state, ranging from zero in some states to over 10% in others. For example, if you buy a $30,000 car in a state with 7% sales tax, that’s an additional $2,100 added to your purchase price that you’ll likely finance.

Beyond sales tax, other critical fees often included or estimated by these advanced calculators are registration fees, title fees, and license plate fees. These are administrative costs associated with legally owning and operating your vehicle. Documentation fees, sometimes called "doc fees," are also charged by dealerships for processing paperwork. While seemingly small individually, these fees can quickly accumulate to hundreds or even thousands of dollars, directly impacting your total loan amount.

Based on my experience, overlooking these "hidden" costs is one of the biggest mistakes new car buyers make. They often budget based solely on the car’s price and an estimated interest rate, only to find themselves scrambling to cover an unexpected additional 5-10% of the vehicle’s value in taxes and fees at the time of purchase. A calculator that includes these factors helps you avoid this common pitfall.

The benefits of using such a calculator are numerous. Firstly, it provides unparalleled accuracy in your budgeting, allowing you to truly understand your affordability. Secondly, it grants you significant negotiation power at the dealership. When you walk in knowing your exact financial limits, you can negotiate the car price and loan terms with greater confidence. Finally, and perhaps most importantly, it helps you avoid unpleasant financial surprises, ensuring your car buying experience is smooth and stress-free.

Key Components of Your Car Loan Calculation

To fully leverage a car loan calculator, it’s essential to understand each input. Every piece of information contributes to the final calculation of your monthly payment and total cost.

Vehicle Price (MSRP/Negotiated Price)

This is the starting point of your calculation. It refers to the Manufacturer’s Suggested Retail Price (MSRP) for new cars, or the agreed-upon selling price for any vehicle. It’s crucial to use the negotiated price here, not just the advertised price, as your ability to haggle can significantly reduce this initial figure. A lower vehicle price directly translates to a lower loan amount and, consequently, lower monthly payments.

Down Payment

Your down payment is the amount of cash you pay upfront towards the purchase of the vehicle. This reduces the total amount you need to borrow, which is always a smart financial move. A larger down payment can lead to lower monthly payments, a shorter loan term, and less interest paid over the life of the loan. It also signals financial stability to lenders, potentially securing you a better interest rate.

Trade-In Value (If Applicable)

If you’re trading in your current vehicle, its value can also act like a down payment. The agreed-upon trade-in value is subtracted from the vehicle’s purchase price before taxes and fees are applied. This further reduces your principal loan amount. Always research your car’s trade-in value using reputable sources like Kelley Blue Book or Edmunds before heading to the dealership to ensure you get a fair offer.

Interest Rate (APR)

The interest rate, often expressed as an Annual Percentage Rate (APR), is the cost of borrowing money. It’s a percentage of the loan principal that you pay to the lender for the privilege of using their funds. A lower interest rate means you’ll pay less over the life of the loan. Your credit score, the loan term, current market rates, and the lender you choose all significantly impact the interest rate you’ll be offered. Shopping around for the best APR is critical.

Loan Term (Duration)

The loan term refers to the length of time, typically measured in months, over which you will repay the loan. Common terms include 36, 48, 60, 72, and even 84 months. A longer loan term generally results in lower monthly payments, which can be appealing for budgeting. However, it also means you’ll pay more in total interest over the life of the loan. Conversely, a shorter term leads to higher monthly payments but significantly reduces the total interest paid.

Sales Tax

Sales tax is one of the most substantial additional costs. It’s a percentage charged by your state and sometimes local government on the purchase price of your car. The rules for sales tax can vary widely. Some states tax the full vehicle price, while others only tax the difference after a trade-in. It’s crucial to know your specific state’s sales tax rate and how it’s applied, as this directly impacts the total amount you finance.

Other Fees (Registration, Title, Documentation, License Plate)

These are the "hidden" costs that can quickly add up.

- Registration fees are annual charges to legally operate your vehicle.

- Title fees are paid to transfer ownership of the car into your name.

- Documentation fees (or "doc fees") are charged by the dealership for processing paperwork; these can vary greatly and are often negotiable.

- License plate fees are for your vehicle’s identification plates.

Always ask for a detailed breakdown of all fees from the dealership to ensure transparency.

How to Effectively Use a Free Car Loan Calculator With Tax

Using a sophisticated car loan calculator is straightforward once you gather the necessary information. Follow these steps to get the most accurate results:

- Gather Your Information: Before you start, collect all the relevant data points. This includes the car’s negotiated price, your planned down payment amount, any trade-in value, your estimated interest rate (pre-approval helps here), and your desired loan term. Don’t forget to know your state’s specific sales tax rate and estimate other common fees.

- Input the Data: Enter each piece of information into the corresponding fields on the calculator. Be precise with your numbers. Ensure you’re using a calculator that specifically allows for sales tax and other fees.

- Experiment with Scenarios: This is where the calculator truly shines. Play around with different variables:

- Down Payment: See how increasing your down payment affects your monthly payment and total interest.

- Loan Term: Compare a 60-month term versus a 72-month term. Notice the difference in monthly payment versus the total interest paid.

- Interest Rate: If you’ve received multiple loan offers, input each APR to see its impact.

- Interpret the Results: The calculator will provide you with an estimated monthly payment and often the total amount of interest you’ll pay over the loan’s life. Analyze these figures to ensure they align with your budget and financial goals. Pay attention to the total cost of the loan, not just the monthly payment.

Pro tips from us: Don’t just use the calculator once. Revisit it multiple times during your car buying process. Use it before negotiating to set your budget, and then again after receiving a firm offer to verify the numbers. This continuous verification ensures you remain in control of your finances throughout the process.

Common Mistakes to Avoid When Calculating Your Car Loan

Even with the best tools, it’s easy to make mistakes if you’re not careful. Common mistakes to avoid are:

- Ignoring Taxes and Fees: As emphasized, this is the most critical error. Failing to include sales tax, registration, and documentation fees will result in a significantly underestimated monthly payment and an inaccurate total loan cost.

- Focusing Only on the Monthly Payment: While an affordable monthly payment is important, it shouldn’t be your sole focus. A low monthly payment often comes with a longer loan term, which means paying significantly more in total interest. Always consider the overall cost of the loan.

- Not Shopping for Interest Rates: Many buyers simply accept the financing offered by the dealership. However, different lenders (banks, credit unions, online lenders) often offer varying interest rates. Securing pre-approval from multiple lenders can save you thousands of dollars in interest over the life of the loan.

- Miscalculating Trade-In Value: Don’t just accept the dealer’s first offer for your trade-in. Research your car’s value beforehand using independent sources. An accurate trade-in value ensures you’re getting a fair deal and correctly reducing your loan principal.

- Choosing an Overly Long Loan Term: While a 72 or 84-month loan might offer very low monthly payments, it prolongs your debt and increases the total interest paid. You also risk being "upside down" on your loan (owing more than the car is worth) for a longer period. Aim for the shortest term you can comfortably afford.

Beyond the Calculator: Smart Strategies for Car Financing

A calculator is a powerful tool, but it’s just one part of a comprehensive car financing strategy. Here are additional smart moves to ensure you get the best deal possible:

Improve Your Credit Score

Your credit score is a major factor in determining the interest rate you’ll be offered. A higher score signals less risk to lenders, leading to lower APRs. Before applying for a loan, check your credit report for errors and take steps to improve your score, such as paying down existing debts and making payments on time.

Save for a Larger Down Payment

The more you put down upfront, the less you need to borrow. This reduces your monthly payments, the total interest paid, and the risk of becoming upside down on your loan. Aim for at least 10-20% of the car’s value as a down payment if possible.

Shop Around for Lenders

Never settle for the first loan offer. Contact various banks, credit unions, and online lenders to compare interest rates and loan terms. Credit unions, in particular, often offer very competitive rates. This due diligence can save you a significant amount over the loan’s duration.

Understand Add-ons and Warranties

Dealerships often push extended warranties, GAP insurance, and other add-ons. While some might offer value, many are overpriced or unnecessary. Research each add-on carefully and only purchase what you genuinely need. Factor these into your budget after calculating the car loan itself. For more details on managing your budget, check out our guide on "Smart Budgeting Strategies for Car Owners." (This is a hypothetical internal link).

Pre-Approval

Getting pre-approved for a loan before visiting the dealership is a game-changer. It provides you with a firm interest rate and loan amount, turning you into a cash buyer. This puts you in a much stronger negotiating position, as you already have financing secured and can focus solely on negotiating the car’s price.

Real-World Scenarios: Putting the Calculator to the Test

Let’s illustrate how different factors impact your loan using hypothetical scenarios:

Scenario A: Savvy Buyer

- Vehicle Price: $30,000

- Down Payment: $6,000 (20%)

- Interest Rate: 4.5% APR

- Loan Term: 60 months

- Sales Tax: 7%

- Fees: $500

- Result: Lower monthly payment, less total interest paid, quicker path to ownership.

Scenario B: Budget-Conscious Buyer

- Vehicle Price: $30,000

- Down Payment: $3,000 (10%)

- Interest Rate: 6.0% APR (due to lower credit or less shopping around)

- Loan Term: 72 months

- Sales Tax: 7%

- Fees: $500

- Result: Higher monthly payment, significantly more total interest paid over a longer period, higher overall cost of the car.

These examples highlight how crucial each input is. Even small differences in interest rate or loan term can lead to substantial financial variations over time. The calculator allows you to visualize these differences instantly.

Choosing the Right Free Car Loan Calculator With Tax

With many calculators available online, how do you pick the best one? Look for a calculator that is:

- User-Friendly: It should have a clear, intuitive interface that’s easy to navigate.

- Comprehensive: Ensure it has fields for all the key components we discussed: vehicle price, down payment, trade-in, interest rate, loan term, and specific fields for sales tax and other fees. Some might even allow you to customize fee types.

- Reputable Source: Choose a calculator from a trusted financial institution, a well-known automotive website, or a reputable financial advice blog. This ensures the calculations are accurate and the tool is reliable. For general information on vehicle taxes and fees in your area, you can often consult your state’s Department of Motor Vehicles (DMV) website. (This is a hypothetical external link to a general resource).

Conclusion

Purchasing a car is one of the most significant financial decisions many people make. It’s a journey that should be approached with knowledge, confidence, and the right tools. A Free Car Loan Calculator With Tax is precisely that—a powerful ally in your quest for the perfect vehicle. By meticulously accounting for every financial detail, from the negotiated price to the often-overlooked sales taxes and fees, you empower yourself to make informed choices.

This comprehensive approach allows for accurate budgeting, strengthens your negotiating position, and ultimately prevents unwelcome financial surprises. Remember, the true cost of your car extends beyond its sticker price, and understanding every component is key to smart financing. Don’t let hidden costs derail your car-buying dreams. Start leveraging this essential tool today, and drive away with confidence, knowing you’ve made a sound financial decision. Happy calculating, and happy driving!