Unlocking Your Dream Car: The Ultimate Guide to Pre Approval Car Loan Soft Pulls (Without Hitting Your Credit!)

Unlocking Your Dream Car: The Ultimate Guide to Pre Approval Car Loan Soft Pulls (Without Hitting Your Credit!) Carloan.Guidemechanic.com

The journey to buying a new car is often a mix of excitement and apprehension. You dream of that perfect ride, but the reality of financing can quickly bring you back down to earth. Will you get approved? What interest rate will you qualify for? And perhaps the biggest question for many savvy consumers: how will this impact your precious credit score?

This is where the power of a "Pre Approval Car Loan Soft Pull" comes into play. It’s a game-changer for car buyers, offering a crucial advantage without the typical credit score anxiety. Far from a mere technicality, understanding soft pulls empowers you to navigate the car market with confidence, knowing your financial standing before you even step foot in a dealership.

Unlocking Your Dream Car: The Ultimate Guide to Pre Approval Car Loan Soft Pulls (Without Hitting Your Credit!)

In this comprehensive guide, we’ll dive deep into everything you need to know about pre-approval car loan soft pulls. We’ll explain what they are, why they matter, how they work, and how you can leverage them to secure the best possible financing for your next vehicle. Our goal is to equip you with the knowledge to make informed decisions, protect your credit, and ultimately, drive away happy.

What Exactly is a "Soft Pull" Credit Inquiry?

Let’s start with the basics. A "soft pull," also known as a soft inquiry or soft credit check, is a type of credit inquiry that does not negatively impact your credit score. It’s a way for lenders, or even yourself, to view a snapshot of your credit report without triggering the more severe consequences associated with a "hard pull."

Think of it like peeking through a window. A soft pull allows a lender to get a general idea of your creditworthiness – your payment history, outstanding debts, and overall credit profile – without leaving a visible mark that other lenders can see or that affects your credit score calculation. This preliminary look is incredibly valuable for initial assessments.

Soft pulls are commonly used in various scenarios. For instance, when you check your own credit score through a credit monitoring service, that’s a soft pull. Similarly, pre-screened credit card offers you receive in the mail often result from a soft pull performed by the issuer to determine if you meet basic eligibility criteria.

Why Pre-Approval with a Soft Pull is Your Smartest First Step

Embarking on the car buying journey without knowing your financing options is like going grocery shopping without a budget – you might end up with something, but it probably won’t be the best deal. A pre-approval based on a soft pull changes this dynamic entirely.

Clarity on Your Financial Standing

One of the most significant benefits is gaining clear insight into what you can truly afford. Before you fall in love with a car outside your budget, a soft pull pre-approval gives you a realistic maximum loan amount and an estimated interest rate. This financial clarity allows you to narrow down your vehicle search to cars that are genuinely within your reach.

It eliminates guesswork and potential disappointment. Knowing your financial boundaries upfront means you can focus on finding a car that fits your lifestyle and your wallet, making the entire process more efficient and less stressful.

Empowered Negotiations

Walking into a dealership with a pre-approval in hand instantly shifts the power dynamic. You are no longer just a buyer hoping for a good rate; you are a qualified buyer with an offer. This leverage is invaluable during negotiations.

Dealers know that you have alternative financing lined up, which can motivate them to offer competitive rates or even better deals to win your business. Based on my experience, having a pre-approval means you’re negotiating from a position of strength, not desperation.

Save Time and Reduce Stress

The traditional car buying process can be lengthy and exhausting, often involving multiple trips to different dealerships and hours spent waiting for financing approvals. A soft pull pre-approval significantly streamlines this.

By knowing your financing terms in advance, you can focus on the car itself – test driving, comparing features, and negotiating the vehicle price. It reduces the anxiety associated with financing decisions, making the overall experience much more enjoyable. Pro tips from us: Time is money, and stress is detrimental; a soft pull helps save both.

Protect Your Credit Score

This is arguably the cornerstone benefit of the soft pull pre-approval. Unlike a hard inquiry, which can temporarily ding your credit score by a few points, a soft pull leaves no trace on your credit report that affects your score.

This means you can shop around for the best pre-approval offers from multiple lenders without worrying about damaging your credit score. It allows you to compare different rates and terms from various financial institutions, ensuring you get the most favorable deal without any adverse impact.

Uncover Potential Issues Early

While a soft pull doesn’t give you a full credit report, it does provide enough information for lenders to make an initial offer. If there are any significant issues on your credit file that might hinder approval, a soft pull pre-approval process can bring them to light early.

This gives you an opportunity to address discrepancies or errors on your credit report before you commit to a hard inquiry. It’s a valuable heads-up that can save you frustration down the line.

The Pre-Approval Car Loan Soft Pull Process: What to Expect

Understanding the steps involved can help demystify the process and prepare you for what’s ahead. It’s generally straightforward and designed to be user-friendly.

Step 1: Research Lenders

Not all lenders offer soft pull pre-approvals, so your first step is to identify those that do. Major banks, credit unions, and a growing number of online lenders are increasingly adopting this customer-friendly approach. Look for phrases like "check your rate without affecting your credit" or "pre-qualify with no impact to your score."

Consider lenders you already have a relationship with, as they might offer preferential rates. However, don’t limit yourself; cast a wide net to ensure you compare diverse offers.

Step 2: Provide Basic Information

Once you’ve chosen a lender (or a few), you’ll typically fill out an online form. This form will ask for some basic personal and financial information. Expect to provide your name, address, date of birth, Social Security Number (SSN), employment status, income, and potentially your desired loan amount or vehicle type.

This information is crucial for the lender to perform the soft pull and make an initial assessment. Rest assured, your SSN is needed to correctly identify your credit file, but it still won’t trigger a hard inquiry at this stage.

Step 3: The Soft Pull Happens

Behind the scenes, the lender uses the information you provided to perform a soft inquiry on your credit report. This automated process quickly retrieves relevant data from one or more credit bureaus (Experian, Equifax, TransUnion) to evaluate your creditworthiness.

Crucially, this inquiry is only visible to you and, in some cases, the entity that made the inquiry. It’s not seen by other lenders and does not influence your credit score calculations in any way.

Step 4: Receive Your Pre-Approval Offer

Within minutes, or sometimes up to a day, you will receive a pre-approval offer. This offer will outline key details such as an estimated interest rate (APR), the maximum loan amount you qualify for, and the potential loan terms (e.g., 60 or 72 months).

Remember, this is an offer based on initial information. It’s not a final, binding loan agreement, but it’s a very strong indication of what you can expect.

Step 5: Review and Compare

If you’ve applied to multiple lenders, this is where you compare the offers side-by-side. Look beyond just the interest rate. Consider the loan term, any fees, and the overall flexibility of the offer.

Don’t rush this step. Take your time to understand each offer completely. Common mistakes to avoid are focusing solely on the monthly payment without considering the total cost of the loan over its full term.

Deciphering Your Pre-Approval Offer: Key Elements to Understand

Receiving your pre-approval offer is exciting, but it’s essential to understand what all the numbers and terms mean. This knowledge empowers you to make the best financial decision.

Interest Rate (APR)

The Annual Percentage Rate (APR) is perhaps the most critical number. It represents the total cost of borrowing money over a year, expressed as a percentage. It includes not just the interest rate but also any lender fees. A lower APR means lower borrowing costs.

Even a difference of half a percentage point can save you hundreds, or even thousands, of dollars over the life of a car loan. This is why comparing offers is so vital.

Loan Term (Months)

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 60 months, 72 months). A longer loan term usually results in lower monthly payments, but it also means you’ll pay more interest over the life of the loan.

Conversely, a shorter term means higher monthly payments but less total interest paid. Consider your budget and long-term financial goals when evaluating the loan term.

Maximum Loan Amount

This is the highest amount the lender is willing to finance for you. It’s crucial to stick within this limit when shopping for a car. Going above it would require a larger down payment or finding additional financing, which could complicate your purchase.

Your pre-approval letter will also often state if there are specific conditions, such as the age or mileage limits for the vehicle, or if a certain down payment is required. Always read the fine print.

Any Specific Conditions or Disclaimers

Pre-approval offers often come with disclaimers. These might include conditions like "subject to verification of income," "subject to final credit review," or "valid for X days." It’s important to acknowledge that the final loan approval is contingent on these conditions being met.

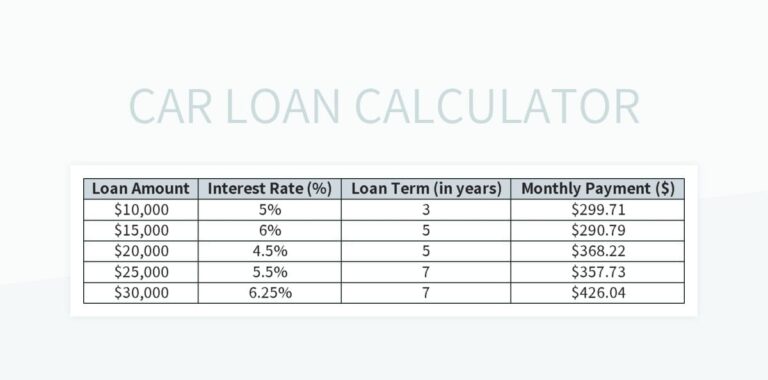

Pro Tip from us: Always focus on the total cost of the loan, not just the attractive monthly payment. A lower monthly payment over a longer term often means a significantly higher total repayment amount. Use an online loan calculator to compare the true cost of different offers.

Soft Pull vs. Hard Pull: A Crucial Distinction

Understanding the difference between a soft pull and a hard pull is fundamental for any responsible borrower. This distinction is at the heart of why pre-approval car loan soft pulls are so beneficial.

| Feature | Soft Pull (Soft Inquiry) | Hard Pull (Hard Inquiry) |

|---|---|---|

| Impact on Credit Score | None | Temporary negative impact (typically 3-5 points) |

| Visibility | Visible only to you and sometimes the inquiring entity | Visible to all future lenders who pull your credit report |

| Purpose | Pre-qualification, account review, identity verification | Application for new credit (loan, credit card, mortgage) |

| Permission | Often done without explicit permission (e.g., pre-screened offers) | Requires your explicit permission |

| Duration on Report | May or may not appear; if it does, it doesn’t affect score | Stays on your credit report for two years |

A soft pull is a benign inquiry. It occurs when a person or company checks your credit as part of a background check, to pre-approve you for an offer, or when you check your own credit. These inquiries do not affect your credit score and are not considered by other lenders when evaluating your creditworthiness.

A hard pull, on the other hand, is a formal request for your credit report that occurs when you apply for new credit, such as a car loan, mortgage, or credit card. Each hard inquiry can cause a small, temporary dip in your credit score, typically a few points. Multiple hard inquiries in a short period can signal to lenders that you are a higher credit risk, potentially leading to higher interest rates or even denial.

Common mistakes to avoid: Many people confuse the two and become overly anxious about any inquiry on their credit. Remember, a soft pull for a car loan pre-approval is designed to help you, not hurt you. The hard pull only happens after you’ve decided on a specific lender and are ready to finalize the loan agreement.

Who Offers Pre-Approval Car Loans with Soft Pulls?

The good news is that an increasing number of financial institutions recognize the value of offering soft pull pre-approvals to attract and empower customers. You have several avenues to explore.

Online Lenders: Many modern online lenders specialize in auto financing and have built their platforms around user-friendly, soft-pull pre-qualification processes. Companies like Capital One Auto Navigator, LightStream, and others often provide quick online tools that allow you to check your rates without affecting your credit score. These platforms are incredibly convenient and allow for easy comparison shopping.

Major Banks: Most large national and regional banks now offer online pre-approval processes that utilize soft pulls. Institutions like Chase, Bank of America, Wells Fargo, and US Bank often have dedicated auto loan sections on their websites where you can fill out an application and receive an initial offer.

Credit Unions: Credit unions are renowned for their competitive rates and personalized service. Many credit unions also provide soft pull pre-approvals as part of their commitment to member service. If you are a member of a credit union, or eligible to join one, it’s always a good idea to check their auto loan offerings first.

Based on my experience: Don’t limit yourself to just one type of lender. Applying to a mix of online lenders, traditional banks, and credit unions gives you the broadest spectrum of potential offers and increases your chances of finding the best deal. Each lender has different criteria and risk assessments, so what one offers might differ significantly from another.

Maximizing Your Chances of a Favorable Pre-Approval

While a soft pull pre-approval doesn’t affect your score, you still want the best possible offer. Taking a few proactive steps can significantly improve your chances.

Check Your Credit Report Beforehand

Before you even start applying for pre-approvals, pull your own credit reports from all three major bureaus (Experian, Equifax, and TransUnion). You can do this for free annually at AnnualCreditReport.com. Review them thoroughly for any errors, inaccuracies, or signs of identity theft.

Disputing and correcting errors can take time, so addressing them well in advance is crucial. A clean credit report presents a more favorable picture to lenders.

Improve Your Credit Score (If Time Allows)

If you have a few months before your planned car purchase, focus on improving your credit score. This could involve paying down existing debts, especially high-interest credit card balances, making all payments on time, and avoiding opening new lines of credit.

Even a small increase in your credit score can translate into a better interest rate on your car loan, saving you money over the long term. For more in-depth advice, you might find our article on "How to Boost Your Credit Score for Big Purchases" helpful. (Internal Link Placeholder)

Have Your Documents Ready

While the initial soft pull pre-approval requires minimal documentation, having your financial information organized can speed up the process if you decide to proceed with a hard inquiry. This includes proof of income (pay stubs, tax returns), proof of residence, and identification.

Being prepared shows lenders you are serious and organized, which can reflect positively on your application.

Be Realistic About Your Budget

Before seeking pre-approval, have a clear idea of what monthly payment you can comfortably afford, considering your other expenses. While a lender might pre-approve you for a high amount, it doesn’t mean you should spend that much.

Borrow only what you truly need and can manage without financial strain. Overextending yourself can lead to financial stress down the road.

Consider a Down Payment

A down payment demonstrates your commitment to the loan and reduces the amount you need to borrow. Lenders view borrowers with a down payment as less risky, which can result in a better interest rate.

Even a modest down payment can make a difference. It also reduces your loan-to-value (LTV) ratio, which is favorable for lenders.

Beyond the Soft Pull: What Happens Next?

The soft pull pre-approval is just the beginning. It sets the stage for the actual car purchase. Understanding the subsequent steps is key to a smooth transaction.

Using Your Pre-Approval at the Dealership

Once you have your pre-approval offer, you’re ready to shop for your car. When you find the right vehicle, present your pre-approval letter to the dealership’s finance manager. This offer acts as a benchmark. The dealership may try to beat your pre-approved rate, or they may match it.

It gives you a strong negotiating position, ensuring you don’t accept an inferior financing offer out of convenience. You are no longer solely dependent on the dealer’s financing options.

The Eventual Hard Pull When You Finalize the Loan

When you decide to move forward with a specific lender – whether it’s the one who gave you the soft pull pre-approval or the dealership’s finance department – they will perform a hard inquiry to finalize the loan. This is a necessary step before funds are disbursed.

At this point, the lender will verify all your provided information and conduct a thorough review of your full credit report. This hard pull will temporarily affect your credit score.

"Rate Shopping" and Its Impact on Hard Inquiries

Here’s a critical piece of information: when you are shopping for an auto loan, multiple hard inquiries within a specific timeframe are often treated as a single inquiry by credit scoring models like FICO. This is known as "rate shopping" or "credit shopping."

Typically, FICO models group all auto loan inquiries made within a 14-day, 30-day, or even 45-day window (depending on the specific model) as one. This means you can apply to several lenders for final approval within this window without suffering multiple hits to your credit score.

Pro Tip from us: To minimize the impact on your credit, aim to get all your hard pulls for car loans within a concentrated period, ideally within two to three weeks. This strategy allows you to compare final offers from different lenders and choose the best one, while protecting your credit score from excessive damage. For more on this, you can refer to trusted sources like Experian’s article on hard vs. soft inquiries. (External Link Placeholder: https://www.experian.com/blogs/ask-experian/whats-the-difference-between-hard-and-soft-inquiries/)

Common Misconceptions About Car Loan Pre-Approval Soft Pulls

Despite their numerous benefits, soft pull pre-approvals are still subject to some misunderstandings. Clearing these up can prevent unnecessary worry.

"It’s a Guaranteed Loan."

A pre-approval is an offer based on the initial information you provide and a snapshot of your credit. It is not a guaranteed loan. The final approval is contingent on several factors, including verification of your income, employment, and the specific vehicle you choose.

If your financial situation changes, or if there are discrepancies between the information you provided and the final verification, the lender can still deny the loan or adjust the terms.

"All Pre-Approvals Are Soft Pulls."

This is a critical misconception. While many reputable lenders offer soft-pull pre-approvals, some may conduct a hard inquiry even for an initial pre-approval or pre-qualification. Always clarify with the lender whether their pre-approval process involves a soft or hard inquiry.

Look for explicit language on their website or application that states "no impact to your credit score" or "soft pull only." If it’s not clear, don’t hesitate to ask before proceeding.

"It Means I Can Only Buy From That Lender."

A pre-approval from one lender does not obligate you to finance your car through them. It simply gives you an offer that you can use as a benchmark. You are free to take that offer to a dealership and see if their financing department can beat it, or you can use it to compare against other lenders’ offers.

The freedom to compare and choose is one of the greatest advantages of getting a pre-approval with a soft pull. It puts you, the buyer, in control.

Conclusion: Empowering Your Car Buying Journey

The pre-approval car loan soft pull is more than just a convenient tool; it’s a fundamental shift in how savvy consumers approach vehicle financing. By leveraging this option, you gain clarity, confidence, and crucial negotiating power, all while safeguarding your credit score.

You’re no longer walking into a dealership hoping for the best; you’re entering with a clear understanding of your financial capabilities and a strong offer in hand. This transforms the often-stressful car buying process into an empowered, efficient, and ultimately more satisfying experience.

So, as you embark on your quest for a new vehicle, remember this ultimate first step. Take advantage of the soft pull pre-approval process. Research lenders, compare offers, and arm yourself with the knowledge to make the best financial decisions. Your dream car, financed on your terms, is well within reach. Start your pre-approval journey today and drive away with confidence!