Unlocking Your Dream Car: The Ultimate Guide to Prequalify Car Loan Capital One

Unlocking Your Dream Car: The Ultimate Guide to Prequalify Car Loan Capital One Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or used vehicle is an exciting prospect. However, for many, the financing aspect can feel daunting, shrouded in complex terms and uncertain outcomes. Imagine stepping into a dealership not with apprehension, but with confidence, knowing exactly what you can afford and the interest rate you’re likely to receive. This isn’t just a fantasy; it’s the reality that prequalifying for a car loan with Capital One can provide.

In this comprehensive guide, we’ll demystify the entire process of how to prequalify for a car loan with Capital One. We’ll dive deep into what prequalification means, why it’s a game-changer for car buyers, and walk you through every step to empower you with knowledge and clarity. Our goal is to equip you with the insights needed to navigate the auto financing landscape like a seasoned pro, making your car buying experience smooth, stress-free, and successful.

Unlocking Your Dream Car: The Ultimate Guide to Prequalify Car Loan Capital One

Understanding Car Loan Prequalification: Your First Step Towards Clarity

Before we delve into the specifics of Capital One, it’s crucial to grasp the fundamental concept of prequalification. Many people confuse prequalification with pre-approval or a full application, but there are distinct differences that empower you as a buyer.

What Exactly is Prequalification?

Prequalification is essentially a preliminary assessment of your creditworthiness by a lender. It gives you an estimate of how much you might be able to borrow for a car loan, along with a projected interest rate, based on the financial information you provide. This process is designed to be quick, easy, and, most importantly, have no impact on your credit score.

Think of it as dipping your toes in the water before jumping in. You get a feel for what’s available to you without committing or leaving a mark on your financial history. It’s an invaluable tool for setting realistic expectations and budgeting effectively for your next vehicle purchase.

Prequalification vs. Pre-approval vs. Full Application: Knowing the Difference

While often used interchangeably, these terms represent different stages in the loan process:

- Prequalification: This is the earliest stage. You provide basic financial information, and the lender performs a "soft inquiry" on your credit report. This soft inquiry doesn’t affect your credit score and results in an estimated loan amount and interest rate. It’s a conditional offer, not a guarantee.

- Pre-approval: This stage is more formal. You typically provide more detailed financial information, and the lender performs a "hard inquiry" on your credit report. A hard inquiry can slightly lower your credit score for a short period. If approved, you receive a conditional offer for a specific loan amount at a set interest rate, often with a letter you can take to a dealership. It’s a stronger indicator of approval than prequalification.

- Full Application: This is the final step once you’ve chosen a specific vehicle. The lender verifies all your information, often requiring documents like pay stubs or bank statements. This also involves a hard inquiry. If everything checks out, the loan is finalized, and funds are disbursed.

For the purpose of this article, our focus is entirely on the initial, risk-free step of prequalification, particularly with Capital One.

Why Prequalifying is a Game-Changer for Car Buyers

The benefits of taking the time to prequalify for a car loan with Capital One are substantial and can significantly enhance your car buying experience.

- Empowerment and Confidence: Knowing your estimated borrowing power transforms you from a speculative buyer into an informed consumer. You walk into a dealership with leverage, not uncertainty.

- Realistic Budgeting: Prequalification gives you a clear financial boundary. You’ll know what kind of monthly payment to expect, allowing you to focus on vehicles within your affordability range, avoiding disappointment or overstretching your budget.

- Faster Dealership Experience: With your financing framework already established, you can streamline the negotiation process at the dealership. You spend less time waiting for finance managers and more time focusing on the car itself.

- Better Negotiation Position: When you arrive at a dealership with an external offer, you have a benchmark. This allows you to compare the dealer’s financing options against your prequalified rate, potentially securing a better deal.

- No Impact on Your Credit Score: This is a huge advantage. You can explore your options without fear of negatively affecting your credit rating, allowing you to shop around for the best rates.

Based on my experience, many buyers regret not prequalifying because they end up feeling pressured or accepting less favorable terms at the dealership. Taking this simple step puts you in the driver’s seat of your financial decision.

Why Choose Capital One for Your Car Loan Prequalification?

Capital One has established itself as a significant player in the auto lending market, known for its innovative approach and commitment to a wide range of customers. Their dedication to making car buying easier shines through their tools and services.

Capital One’s Reputation in Auto Lending

Capital One is a well-regarded financial institution with a strong presence in various sectors, including auto financing. They are known for their accessibility and willingness to work with borrowers across a broad spectrum of credit profiles, from excellent to those with less-than-perfect credit. This inclusive approach makes them a popular choice for many car buyers.

The Power of Capital One’s Auto Navigator Tool

At the heart of Capital One’s prequalification process is their intuitive online tool, the Auto Navigator. This platform is designed to simplify the car buying journey by allowing you to get prequalified, find vehicles, and even see personalized financing terms for specific cars, all from the comfort of your home.

Pro tips from us: The Auto Navigator isn’t just for prequalification; it’s an end-to-end tool that connects your financing to actual vehicles available at partner dealerships. This integration is a huge time-saver.

The Capital One Prequalification Process: A Step-by-Step Guide

Getting prequalified for a car loan with Capital One is a straightforward and user-friendly process. Here’s a detailed walkthrough of what to expect:

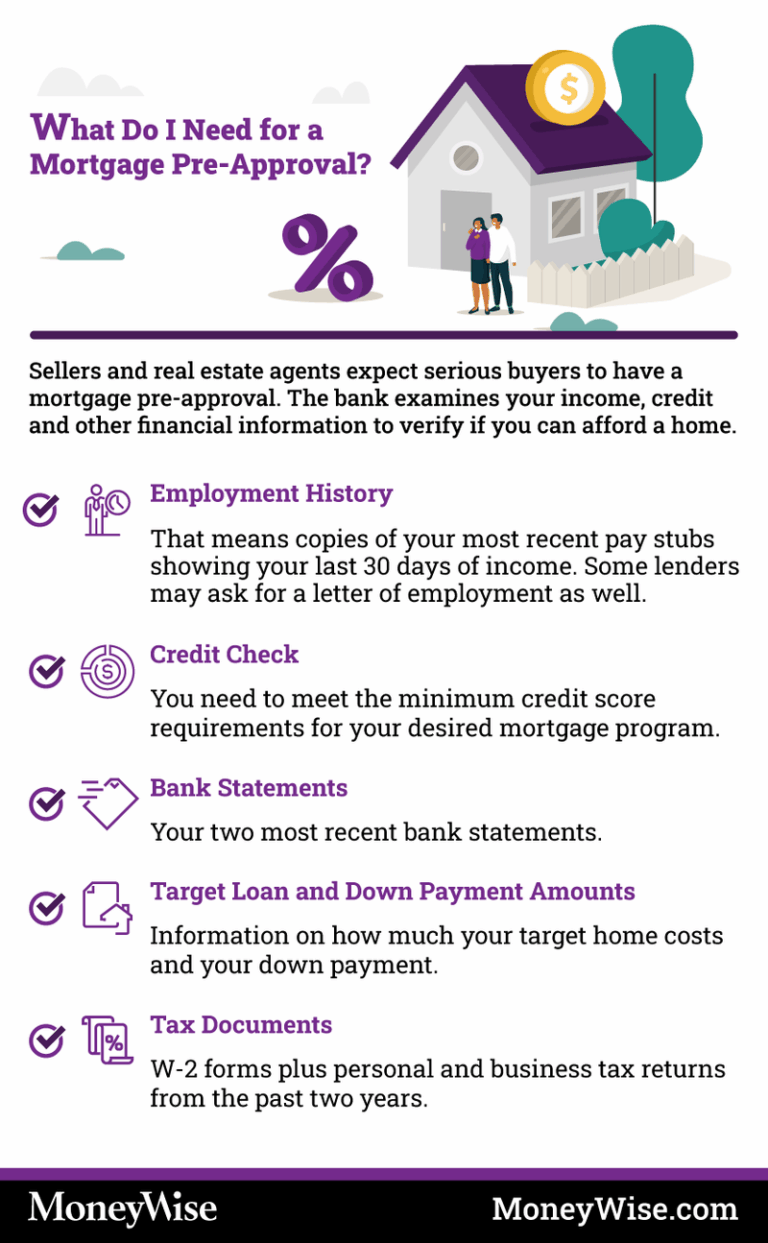

Step 1: Gather Your Essential Information

Before you begin, having key personal and financial details readily available will make the process much smoother. While prequalification doesn’t require extensive documentation, you’ll need to provide some basic information:

- Personal Information: Your full name, address, date of birth, and Social Security Number.

- Employment Details: Your employer’s name, occupation, and gross monthly income.

- Housing Information: Whether you rent or own, and your monthly housing payment.

Common mistakes to avoid are guessing your income or housing costs. Provide accurate figures to get the most precise prequalification offer.

Step 2: Accessing the Capital One Auto Navigator

The entire prequalification process for a car loan with Capital One is conducted online through their dedicated Auto Navigator platform.

- Simply open your web browser and search for "Capital One Auto Navigator" or visit their official website directly.

- Look for prominent buttons or links that say "Prequalify Now," "Get Pre-qualified," or "Start Shopping."

The platform is designed to be very intuitive, guiding you through each stage with clear prompts.

Step 3: Filling Out the Online Form

Once you’re on the Auto Navigator page, you’ll be prompted to enter the information you gathered in Step 1. The form is typically broken down into several sections:

- Personal Details: Enter your name, address, date of birth, and Social Security Number. Capital One uses your SSN to conduct the soft credit inquiry needed for prequalification.

- Income Information: Provide your gross monthly income and employment details. This helps Capital One assess your ability to repay a loan.

- Housing Costs: Input whether you rent or own, and your monthly housing payment. This contributes to calculating your debt-to-income ratio, another key factor for lenders.

The system is designed to be quick. You’ll likely spend only a few minutes completing these fields.

Step 4: Reviewing Your Personalized Offers

After submitting your information, Capital One’s system will quickly process it and present you with your personalized prequalification offers. This is where the magic happens!

- Estimated Loan Amount: You’ll see the maximum amount you might be able to borrow.

- Projected Interest Rate: This gives you a clear idea of the potential cost of borrowing.

- Estimated Monthly Payments: Based on various loan terms (e.g., 48 months, 60 months, 72 months), you’ll see what your monthly payments could look like.

Take your time to review these offers. Understand the different loan terms and how they impact both your monthly payment and the total interest paid over the life of the loan.

Step 5: No Impact on Your Credit Score (Soft Inquiry)

It’s worth reiterating: the Capital One prequalification process involves a soft credit inquiry. This means that when Capital One checks your credit report to generate your offers, it does not negatively affect your credit score. You can explore your options with peace of mind, knowing your credit remains untouched.

Pro tip: If you don’t get an offer immediately, don’t be discouraged. Capital One may suggest alternative paths or provide reasons why an offer wasn’t available at that moment. This feedback can be valuable for future attempts.

What Happens After Prequalification? Your Next Steps

Prequalifying for a car loan with Capital One is just the beginning. It’s the launchpad for a more informed and efficient car buying journey.

Understanding Your Prequalified Offer

Your prequalified offer from Capital One provides a solid framework for your car search. It tells you:

- Your Budget Ceiling: This is the maximum amount you’re likely to be approved for, guiding your vehicle selection.

- Estimated Cost of Borrowing: The interest rate gives you an idea of how much extra you’ll pay over the loan term.

- Payment Expectations: Knowing your estimated monthly payments helps you align your car choice with your overall financial picture.

Use this information wisely to focus your search on vehicles that truly fit your budget.

Finding Your Dream Car within the Capital One Network

One of the significant advantages of Capital One Auto Navigator is its integrated car shopping experience. After prequalifying, you can use the tool to:

- Browse Inventory: Search for new and used vehicles available at participating dealerships within Capital One’s network.

- See Personalized Terms: For many vehicles, you’ll be able to see personalized financing terms, including your estimated monthly payment and APR, directly applied to specific cars. This is incredibly powerful as it removes much of the guesswork.

This feature saves immense time and helps you understand the true cost of different vehicles upfront.

Visiting the Dealership with Confidence

When you’ve found a car you’re interested in, your Capital One prequalification becomes a powerful asset at the dealership.

- Communicate Your Prequalification: Inform the sales associate that you are already prequalified with Capital One.

- Streamlined Process: The dealership will work with Capital One to finalize your loan. Since much of the preliminary work is done, the process should be smoother and quicker.

- Negotiate from Strength: Even if the dealership tries to offer their own financing, you have your Capital One offer as a comparison point. This empowers you to negotiate for the best overall deal, whether it’s through Capital One or the dealership’s lender.

The Full Application: When a Hard Inquiry Occurs

Once you’ve selected a specific vehicle and are ready to move forward, the dealership will submit a full credit application to Capital One (or another lender). This is the point where a hard credit inquiry will occur.

This hard inquiry allows the lender to thoroughly review your complete credit history and verify all the information you provided. It’s a necessary step to finalize the loan and is standard practice for any significant credit extension. While it might cause a slight, temporary dip in your credit score, this is expected and part of the process when you’re serious about purchasing.

Common mistakes to avoid are not comparing your prequalified offer with any dealer-offered financing. Always ask for both options and do the math to see which saves you more in the long run. Also, avoid falling in love with a car outside your prequalified budget.

Factors Influencing Your Capital One Car Loan Prequalification

While prequalification is a soft pull, the estimated offers are based on crucial financial factors. Understanding these will help you maximize your chances of getting favorable terms when you prequalify for a car loan with Capital One.

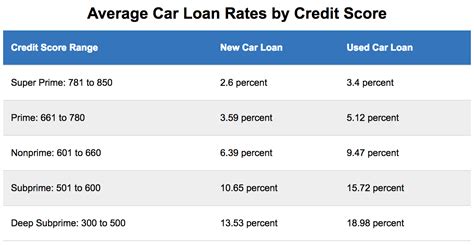

1. Your Credit Score

Your credit score is arguably the most significant factor. It’s a numerical representation of your creditworthiness, reflecting your payment history, debt levels, and credit age.

- Excellent Credit (780+): Generally qualifies for the best interest rates and loan terms.

- Good Credit (670-779): Still very strong, likely to receive competitive offers.

- Fair Credit (580-669): May receive offers, but interest rates could be higher.

- Poor Credit (Below 580): Prequalification is still possible with Capital One, but rates will be higher, and the loan amount might be limited.

Capital One is known for being relatively inclusive, so even if your credit isn’t perfect, it’s still worth exploring your options.

2. Income and Employment History

Lenders want to ensure you have a stable source of income to repay the loan.

- Steady Income: A consistent employment history and verifiable income are crucial.

- Income Level: Your income needs to be sufficient to comfortably cover the estimated monthly car payments, in addition to your other existing debts.

3. Debt-to-Income Ratio (DTI)

Your DTI ratio is the percentage of your gross monthly income that goes towards paying your monthly debt obligations. Lenders use this to assess your ability to take on new debt.

- Calculation: (Total Monthly Debt Payments / Gross Monthly Income) x 100

- Lender Preference: A lower DTI ratio (typically below 40-50%) is generally preferred, indicating you have more disposable income to manage new loan payments.

Based on my experience, a high DTI is one of the quickest ways to receive less favorable loan terms or even be denied, even with a decent credit score.

4. Down Payment

While not always mandatory, making a down payment significantly improves your loan prospects.

- Reduces Loan Amount: A larger down payment means you borrow less, which translates to lower monthly payments and less interest paid over time.

- Shows Commitment: It demonstrates your financial commitment to the purchase, making you a less risky borrower.

- Positive Equity: A substantial down payment can help you avoid being "upside down" on your loan (owing more than the car is worth) early on.

5. Loan Term and Vehicle Type

The length of the loan (term) and the type of vehicle you intend to purchase also play a role.

- Loan Term: Shorter loan terms typically come with lower interest rates but higher monthly payments. Longer terms have lower monthly payments but accumulate more interest over time.

- Vehicle Type: Lenders may view certain vehicles (e.g., very old, high mileage, or luxury cars) differently in terms of risk and collateral value.

These factors interrelate significantly. For instance, a strong credit score can offset a slightly higher DTI, while a large down payment can improve your terms even with a fair credit score.

Maximizing Your Chances of Approval and Getting the Best Rates

While Capital One is accommodating, there are proactive steps you can take to strengthen your financial position and improve your prequalification offer.

1. Improve Your Credit Score

Even small improvements can make a difference.

- Pay Bills on Time: Payment history is the biggest factor in your credit score.

- Reduce Credit Card Balances: Lowering your credit utilization ratio can boost your score.

- Check for Errors: Review your credit report for inaccuracies and dispute them.

For more tips on improving your credit score, check out our guide on (simulated internal link).

2. Save for a Down Payment

As discussed, a larger down payment is always beneficial. Aim for at least 10-20% of the vehicle’s purchase price, if possible. This not only reduces your loan amount but also signals financial responsibility to the lender.

3. Reduce Existing Debt

Lowering your overall debt, especially high-interest credit card debt, will improve your debt-to-income ratio, making you a more attractive borrower. Focus on paying down smaller debts or those with the highest interest rates first.

4. Know Your Budget and Be Realistic

Before you even start the prequalification process, have a clear idea of what you can comfortably afford each month. This includes not just the car payment but also insurance, fuel, and maintenance. Being realistic prevents overextending yourself.

5. Consider a Co-signer (If Necessary)

If your credit score or income isn’t ideal, a co-signer with strong credit can significantly improve your chances of approval and potentially secure a lower interest rate. However, ensure both parties understand the responsibilities, as the co-signer is equally liable for the loan.

Pro tips from us: Don’t just look at the monthly payment. Always consider the total cost of the loan, including interest, over the entire term. A lower monthly payment over a longer term often means paying much more in interest.

Frequently Asked Questions About Prequalifying for a Car Loan with Capital One

We’ve covered a lot of ground, but you might still have some lingering questions. Here are answers to some common inquiries:

How long is my Capital One prequalification valid?

Typically, your prequalification offer from Capital One is valid for a specific period, often around 30 days. This gives you ample time to shop for a car. Always check the specific validity period stated in your offer.

Can I prequalify for a used car with Capital One?

Absolutely! Capital One Auto Navigator allows you to prequalify for both new and used vehicles. Their network includes dealerships offering a wide range of inventory to suit various preferences and budgets.

What if my credit isn’t perfect? Can I still prequalify?

Yes, Capital One is known for working with a broad spectrum of credit profiles. While excellent credit will yield the best rates, they do offer options for those with fair or even less-than-perfect credit. Prequalifying is a no-risk way to see what terms you might receive.

Does prequalification guarantee final loan approval?

No, prequalification does not guarantee final loan approval. It’s an estimate based on the information you provide and a soft credit pull. Final approval is subject to a full credit application, verification of your information, and the selected vehicle meeting the lender’s criteria. However, it significantly increases your confidence in getting approved.

Can I change the car I want after prequalifying?

Yes, your prequalification is typically for a certain loan amount, not a specific vehicle. You can use your prequalified offer to shop for different cars within the approved amount and at Capital One’s partner dealerships. The Auto Navigator tool even allows you to see how your prequalification applies to various vehicles.

If you’re still weighing your options, our article on (simulated internal link) offers valuable insights into finding the best fit for your needs.

Conclusion: Drive Away with Confidence by Prequalifying with Capital One

Navigating the car buying process can be complex, but it doesn’t have to be stressful. By taking the proactive step to prequalify for a car loan with Capital One, you equip yourself with invaluable knowledge and confidence. This simple, risk-free process transforms you into an informed buyer, empowering you to make smart financial decisions, negotiate effectively, and ultimately, drive away in your dream car without any lingering doubts.

Capital One’s user-friendly Auto Navigator tool makes this process accessible and transparent, connecting you with potential financing options and a vast network of vehicles. So, before you step foot on a dealership lot, take a few minutes to get prequalified. It’s a small investment of your time that can yield significant returns in savings, peace of mind, and a truly empowering car buying experience. Start your journey today and experience the difference an informed approach makes. For the most up-to-date information directly from the source, always refer to the official Capital One Auto Navigator website. (Simulated external link: https://www.capitalone.com/auto-financing/auto-navigator/)