Unlocking Your Dream Drive: The Ultimate Guide to Car Loans in Australia

Unlocking Your Dream Drive: The Ultimate Guide to Car Loans in Australia Carloan.Guidemechanic.com

Buying a car in Australia is an exciting milestone for many, offering newfound freedom, convenience, and adventure. However, for most of us, purchasing a vehicle outright isn’t always an option. This is where understanding car loans Australia becomes absolutely critical. It’s more than just finding a payment plan; it’s about making an informed financial decision that empowers your lifestyle without compromising your future.

Based on my extensive experience in consumer finance, navigating the world of vehicle loans can feel daunting. There are so many options, terms, and conditions to consider. This comprehensive guide is designed to demystify the process, providing you with all the knowledge you need to secure the best possible Australian car loan for your unique situation. We’ll dive deep into everything from loan types and application processes to finding the most competitive rates and avoiding common pitfalls.

Unlocking Your Dream Drive: The Ultimate Guide to Car Loans in Australia

Understanding Car Loans in Australia: The Essential Foundation

At its core, a car loan is a sum of money borrowed from a lender (like a bank, credit union, or specialist finance company) to purchase a vehicle. You then repay this amount, plus interest, over a predetermined period, typically ranging from one to seven years. This structured repayment allows you to acquire a car now and pay for it over time.

The decision to take out a car loan is significant, and it’s important to weigh the advantages and disadvantages. On the positive side, a car loan makes vehicle ownership accessible, allows you to preserve your savings for other investments, and can even help build your credit history if managed responsibly. Conversely, it adds a recurring expense to your budget, and interest charges mean you’ll pay more than the car’s sticker price over the loan term.

The Diverse Landscape of Australian Car Loans

The vehicle finance Australia market offers a range of products, each with its own characteristics. Understanding these distinctions is the first step towards making an educated choice.

1. Secured Car Loans:

This is by far the most common type of car loan in Australia. With a secured loan, the vehicle itself acts as collateral for the loan. This means if you default on your repayments, the lender has the right to repossess the car to recover their losses.

Because the lender has this security, secured car loans typically come with lower interest rates compared to unsecured options. They are generally easier to obtain and are available for both new and used vehicles, provided the car meets certain age and value criteria set by the lender.

2. Unsecured Car Loans:

An unsecured car loan does not require any collateral. The lender assesses your creditworthiness and ability to repay based solely on your financial history and income. These loans are less common for car purchases specifically but can be obtained as a personal loan and then used to buy a car.

Due to the higher risk for the lender, unsecured car loans usually carry significantly higher interest rates. They might be an option if you’re buying an older car that doesn’t meet secured loan criteria, or if you prefer not to use your vehicle as security, but be prepared for the increased cost.

3. Fixed vs. Variable Rate Loans:

When considering your car loan rates Australia, you’ll encounter both fixed and variable interest rate options. A fixed-rate loan means your interest rate remains the same for the entire loan term. This provides predictability, as your monthly repayments will not change, making budgeting much easier.

A variable-rate loan, however, means your interest rate can fluctuate according to market conditions or changes in the lender’s base rate. While this offers the potential for lower repayments if rates fall, it also carries the risk of increased repayments if rates rise. Based on my experience, most people prefer the certainty of a fixed rate for car loans, especially in times of economic uncertainty.

4. Loans with Balloon Payments:

Some Australian car loans come with a balloon payment option. This means a portion of the loan principal is deferred until the very end of the loan term. Your regular repayments will be lower throughout the loan period, as you’re not paying off the full amount.

At the end of the term, you’ll need to pay the lump sum balloon payment. Common mistakes to avoid here include not having a plan for this final payment. You might choose to pay it off, refinance it, or trade in your car to cover the cost. While it offers lower monthly payments, it can lead to a financial shock if you haven’t budgeted for the final sum.

5. Dealership Finance vs. Bank/Broker Finance:

You’ll often be offered finance directly at the car dealership. While convenient, it’s crucial to understand that dealership finance might not always offer the best car loan Australia for your situation. Dealerships often work with specific lenders and may add their own margins, potentially leading to higher interest rates or less flexible terms.

Pro tips from us: Always compare dealership offers with quotes from banks, credit unions, and independent finance brokers. Banks and credit unions are traditional lenders, while brokers act as intermediaries, comparing various lenders to find a suitable deal for you. Brokers can be particularly helpful if your situation is unique or if you’re looking for bad credit car loans Australia.

The Application Process: Your Roadmap to Approval

Securing a car loan doesn’t have to be a mystery. Understanding the steps and what lenders look for will significantly increase your chances of approval.

Eligibility Criteria for Car Loans in Australia

Before you even start looking at cars, it’s wise to understand the general criteria lenders use to assess your application. While specific requirements vary, these are the common benchmarks:

- Age: You must be at least 18 years old.

- Residency: You need to be an Australian citizen or permanent resident, or hold an eligible long-term visa.

- Income: Lenders want to see stable employment and a regular income stream. They assess whether your income is sufficient to comfortably cover the loan repayments, alongside your existing financial commitments.

- Credit Score: Your credit score is a numerical representation of your creditworthiness. A higher score indicates a lower risk to lenders, making approval easier and often leading to better interest rates. We’ll delve deeper into this shortly.

Documents You’ll Need

Gathering the necessary paperwork in advance can streamline your application process. While specific requests may vary, here’s a common list:

- Proof of Identity: Australian Driver’s Licence, Passport, or other government-issued ID.

- Proof of Income: Recent payslips (typically 2-3 months), employment contracts, tax returns (if self-employed), or bank statements showing income deposits.

- Proof of Expenses: Recent bank statements (typically 3-6 months) to show your living expenses and other financial commitments. This helps lenders assess your serviceability.

- Proof of Residency: Utility bills, rental agreements, or mortgage statements.

- Details of the Vehicle (if known): If you’ve already chosen a car, details like make, model, year, and VIN will be required for secured loans.

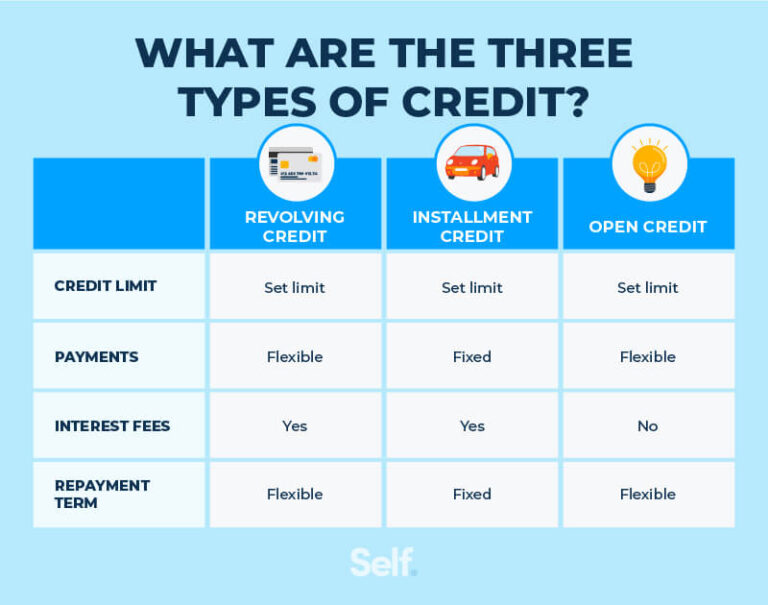

Your Credit Score: The Financial Fingerprint

Your credit score plays a pivotal role in your car loan application. It’s a three-digit number that summarises your financial history, including past loans, credit card usage, and repayment behaviour. A good credit score tells lenders that you are a reliable borrower, making them more confident in lending to you.

Pro tips from us: Before applying for any significant loan, it’s always a good idea to check your credit score. You can do this for free through services like Experian, Equifax, or Illion. If your score is lower than you’d like, focus on improving it by paying bills on time, reducing existing debts, and avoiding multiple loan applications in a short period. A strong credit score is your gateway to the best car loan Australia has to offer. For more detailed advice, you might find our guide on Improving Your Credit Score: A Comprehensive Guide particularly useful.

Navigating the Market: Finding the Best Car Loan Australia

With your documents ready and a clear understanding of your financial standing, the next step is to compare your options and find a loan that genuinely suits your needs.

Comparing Car Loan Rates and Fees

This is arguably the most critical step in securing an affordable car loan. Don’t just look at the headline interest rate; dig deeper.

- Interest Rates: This is the percentage charged by the lender for borrowing the money. A lower interest rate means less money you pay back over the loan term.

- Comparison Rates: This is a legally required rate in Australia designed to help you compare the true cost of a loan. The comparison rate includes the interest rate plus most fees and charges associated with the loan, expressed as a single percentage. Pro tips from us: Always focus on the comparison rate when comparing different loan products, as it gives you the most accurate picture of the total cost.

- Application Fees: A one-off fee charged by some lenders to process your application.

- Ongoing Fees: Some loans may have monthly or annual service fees.

- Early Repayment Fees: If you plan to pay off your loan sooner, check if there are penalties for doing so.

Using a Car Loan Calculator Australia

An online car loan calculator Australia is an invaluable tool in your research phase. By inputting the loan amount, interest rate, and desired loan term, these calculators can quickly estimate your monthly or fortnightly repayments.

This allows you to play with different scenarios – how a higher interest rate impacts repayments, or how extending the loan term reduces individual payments but increases total interest paid. It helps you budget effectively and understand the financial commitment before you apply.

The Role of a Car Loan Broker

A car loan broker acts as an intermediary between you and a network of lenders. They can save you significant time and effort by comparing various loan products from different financial institutions on your behalf.

Based on my experience, brokers are particularly useful if you have a complex financial situation, are short on time, or are looking for specific types of loans like bad credit car loans Australia. They often have access to exclusive deals and can negotiate on your behalf. However, ensure you understand how they are remunerated (e.g., commission from the lender) to ensure their recommendations align with your best interests.

Special Situations and Considerations

The world of car loans isn’t one-size-fits-all. Different circumstances call for different approaches.

Used Car Loans Australia vs. New Car Loans Australia

While the fundamental process is similar, there are key differences when financing a used car compared to a new one. Lenders generally perceive used cars as higher risk due to depreciation and potential maintenance issues.

This often means that used car loans Australia might come with slightly higher interest rates or stricter eligibility criteria than loans for brand-new vehicles. The maximum loan term might also be shorter for older cars. Always check the lender’s policies regarding the age of the vehicle they will finance.

Bad Credit Car Loans Australia

Having a less-than-perfect credit history doesn’t necessarily mean you can’t get a car loan. There are specialist lenders who cater to individuals with bad credit. However, it’s important to manage your expectations.

Bad credit car loans Australia typically come with higher interest rates to offset the increased risk for the lender. You might also be required to provide a larger deposit or have a guarantor. Common mistakes to avoid when applying with bad credit include not being transparent about your financial history or applying with too many lenders, which can further damage your credit score. Focus on one or two reputable specialist lenders and provide all requested information honestly.

Early Repayment: Good Idea or Not?

If you find yourself in a position to pay off your car loan earlier than planned, it can be a great way to save on interest. However, always check your loan agreement for any early repayment fees or penalties.

Some loans, particularly older fixed-rate loans, might charge a fee for early settlement. If there are no such penalties, paying off your loan sooner is generally a smart financial move. It frees up your cash flow and eliminates future interest charges.

Pro Tips for a Smooth Car Loan Journey (E-E-A-T)

Having guided countless individuals through the finance maze, here are some actionable tips to ensure your experience with car loans Australia is as smooth and beneficial as possible:

- Pro Tip 1: Research Thoroughly Before You Commit. Don’t jump at the first offer. Spend time comparing different lenders, loan types, and terms. A few hours of research can save you thousands of dollars over the life of the loan.

- Pro Tip 2: Understand the Total Cost of the Loan, Not Just the Monthly Payment. While a low monthly payment is appealing, a longer loan term or higher interest rate can mean you pay significantly more overall. Use a car loan calculator Australia to see the full picture.

- Pro Tip 3: Don’t Apply for Multiple Loans Simultaneously. Each loan application generates an inquiry on your credit report. Too many inquiries in a short period can negatively impact your credit score, making lenders hesitant. Shop around for quotes, but only submit a full application when you’re ready to commit.

- Pro Tip 4: Be Honest in Your Application. Providing inaccurate or misleading information can lead to your application being rejected, or worse, legal repercussions. Lenders will verify your details, so complete honesty is always the best policy.

- Pro Tip 5: Negotiate Where Possible. While interest rates are often set, you might be able to negotiate the car’s price, which directly impacts the loan amount needed. Even small reductions can lead to significant savings on interest over time.

Common Mistakes to Avoid:

- Not Budgeting for Additional Costs: Remember to factor in registration, compulsory third-party insurance (CTP), comprehensive car insurance, ongoing maintenance, and fuel costs into your overall budget. A car loan is just one part of car ownership.

- Taking the Longest Loan Term for the Lowest Payment: While a longer term reduces individual payments, it dramatically increases the total interest you’ll pay. Aim for the shortest term you can comfortably afford.

- Ignoring the Comparison Rate: As mentioned, the comparison rate is your best friend when comparing loans. Don’t be swayed by a low advertised interest rate if the comparison rate is much higher due to hidden fees.

- Signing Without Reading the Fine Print: Always read your loan contract thoroughly. Understand all terms, conditions, fees, and repayment schedules before you sign on the dotted line. If something is unclear, ask questions. For additional unbiased financial guidance, a trusted external source like the Australian Government’s MoneySmart website (www.moneysmart.gov.au) offers excellent resources.

Driving Forward with Confidence

Securing a car loan in Australia doesn’t have to be a stressful ordeal. By arming yourself with knowledge, understanding your options, and taking a strategic approach, you can navigate the process with confidence. From grasping the difference between secured and unsecured loans to diligently comparing comparison rates and leveraging the power of a car loan calculator Australia, every step you take brings you closer to your dream car.

Remember, the goal isn’t just to get a loan, but to secure the right Australian car loan that fits your financial capacity and helps you achieve your motoring aspirations without unnecessary financial burden. Start your research today, ask questions, and make an informed decision that puts you firmly in the driver’s seat of your financial future.