Unlocking Your Dream Ride: A Comprehensive Guide to Capital One Car Loan Requirements

Unlocking Your Dream Ride: A Comprehensive Guide to Capital One Car Loan Requirements Carloan.Guidemechanic.com

Navigating the world of auto financing can feel like a complex journey, especially when you’re aiming for a trusted lender like Capital One. As one of the largest and most recognized financial institutions, Capital One offers a broad spectrum of auto loan options designed to cater to a diverse range of financial situations. Whether you have pristine credit, are rebuilding your financial health, or fall somewhere in between, understanding their specific requirements is your first crucial step towards driving home your new or used vehicle.

This in-depth guide is crafted to be your ultimate resource, breaking down every facet of Capital One car loan requirements. We’ll delve into the essential criteria, share expert insights, highlight common pitfalls, and equip you with the knowledge to significantly boost your approval chances. Our goal is to demystify the process, turning what might seem daunting into an achievable goal, and helping you make informed decisions on your auto financing journey.

Unlocking Your Dream Ride: A Comprehensive Guide to Capital One Car Loan Requirements

Why Choose Capital One for Your Auto Loan?

Before we dive into the specifics, it’s worth understanding why Capital One stands out in the competitive auto loan landscape. They are renowned for their flexibility and their commitment to serving a wide range of credit profiles, not just those with perfect scores. This inclusive approach makes them a popular choice for many car buyers.

Capital One works with a vast network of dealerships, streamlining the process of finding a vehicle that fits your budget and loan approval. Their user-friendly online tools, like the pre-qualification process, empower consumers to shop with confidence, knowing their financing options upfront. This transparency and accessibility are key reasons why many individuals consider Capital One for their auto financing needs.

The Core Pillars of Capital One Car Loan Requirements

Securing a car loan, especially from a major lender like Capital One, hinges on several interconnected factors. Think of these as the fundamental pillars supporting your application. Each element plays a vital role in Capital One’s decision-making process, influencing not only your approval but also the interest rate and terms you’ll be offered.

Let’s break down each of these critical requirements in detail.

1. Your Credit Score: The Financial Foundation

Your credit score is arguably the most significant factor Capital One will consider. It acts as a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. A higher score generally indicates a lower risk to lenders, often leading to more favorable interest rates and terms.

Capital One’s Flexibility Across Credit Tiers:

One of Capital One’s strengths is its willingness to work with various credit profiles. While excellent credit will undoubtedly secure the best rates, they also offer solutions for individuals with average or even subprime credit. This broad approach means you shouldn’t be immediately discouraged if your score isn’t perfect.

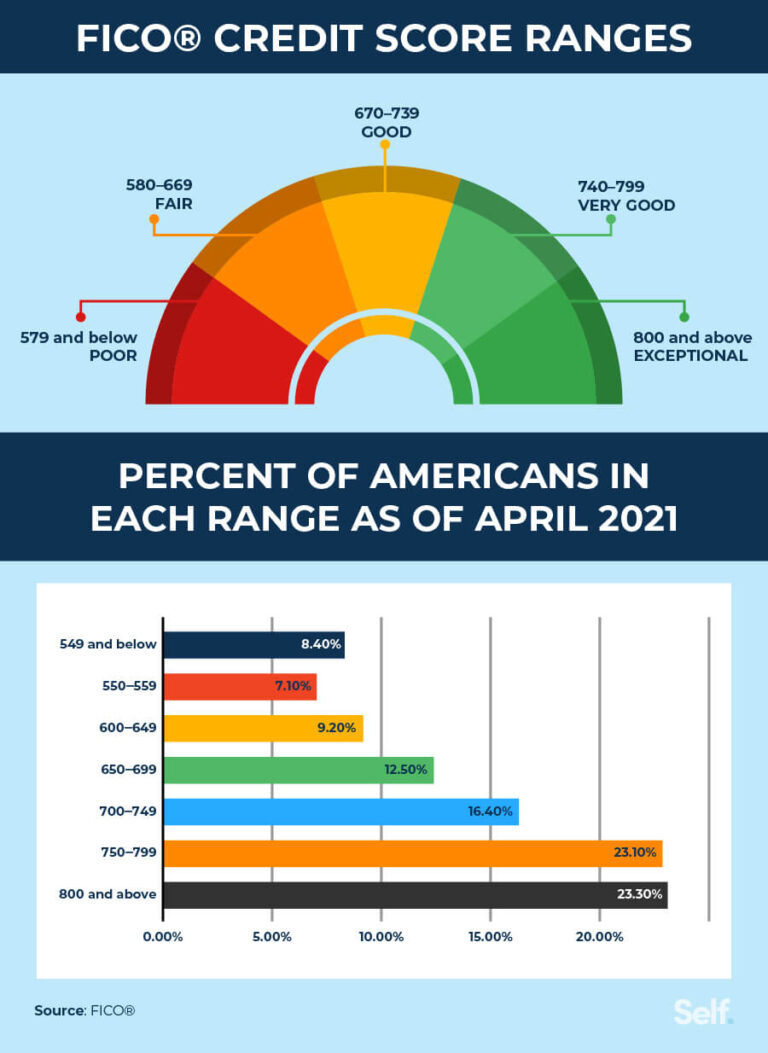

- Excellent Credit (720+ FICO): If your score falls into this range, you’re in an ideal position. You’ll likely qualify for Capital One’s most competitive interest rates and flexible terms. Lenders view you as a very low-risk borrower.

- Good Credit (660-719 FICO): This is a strong credit tier that generally qualifies for good rates, though perhaps not the absolute lowest. Capital One is very comfortable lending to individuals in this range, recognizing their solid payment history.

- Average/Fair Credit (600-659 FICO): Many applicants fall into this category. Capital One is known for working with borrowers here, offering viable loan options. You might see slightly higher interest rates compared to those with excellent credit, but approval is still very possible.

- Subprime/Poor Credit (Below 600 FICO): Even with a lower credit score, Capital One might still be an option. They have specialized programs designed for individuals rebuilding their credit. While rates will be higher to compensate for the increased risk, it’s a pathway to getting approved and improving your credit with timely payments.

Based on my experience helping countless individuals navigate auto loans, many applicants get anxious about their credit score, fearing it’s the sole determinant. While crucial, it’s part of a larger picture. Capital One looks at your entire financial profile, and a lower score can sometimes be offset by other strengths in your application, such as a substantial down payment or a stable income.

Pro Tips for Your Credit Score:

- Check Your Score Regularly: Before applying, obtain your credit reports from all three major bureaus (Experian, Equifax, TransUnion) via AnnualCreditReport.com. This allows you to identify and dispute any errors that could be dragging your score down.

- Understand Your Score: Know which factors are impacting your score – payment history, credit utilization, length of credit history, new credit, and credit mix.

- Improve Where Possible: If you have time before applying, focus on making all payments on time, reducing credit card balances, and avoiding new credit applications. Even small improvements can make a difference.

2. Income and Employment Stability: Proving Repayment Capacity

Beyond your credit history, Capital One needs assurance that you have the consistent financial capacity to make your monthly loan payments. This is where your income and employment stability come into play. Lenders want to see a reliable source of funds.

Minimum Income Expectations:

While Capital One doesn’t publicly state a universal minimum income requirement, they typically look for applicants to have a gross monthly income of at least $1,500. This threshold helps ensure that you can comfortably manage your loan payments alongside your other living expenses. However, this figure can vary based on your overall financial profile and the specific loan amount you’re seeking.

Proof of Employment:

Expect to provide documentation verifying your employment. This usually includes recent pay stubs (typically 1-2 months’ worth), W-2 forms, or for self-employed individuals, tax returns and bank statements. Capital One prefers to see a stable employment history, ideally with the same employer for at least six months to a year. Frequent job changes can sometimes raise a red flag about income consistency.

The Debt-to-Income (DTI) Ratio:

This is a critical metric Capital One uses to assess your ability to take on new debt. Your DTI ratio compares your total monthly debt payments (including the proposed car loan) to your gross monthly income. For example, if your total monthly debt payments are $1,000 and your gross monthly income is $3,000, your DTI is 33%.

Capital One generally prefers a DTI ratio below 50%, and ideally even lower. A high DTI suggests that too much of your income is already allocated to existing debts, potentially making it difficult to manage an additional car loan payment.

Common mistakes to avoid include misrepresenting your income or failing to disclose all your existing debts. Lenders have sophisticated ways of verifying this information, and any discrepancies can lead to immediate denial of your application. Ensure all financial details provided are accurate and up-to-date.

3. Down Payment: Reducing Risk and Saving Money

Making a down payment is not always strictly required by Capital One, especially for applicants with excellent credit. However, it is highly recommended and can significantly strengthen your application, regardless of your credit score. A down payment demonstrates your commitment to the purchase and reduces the lender’s risk.

Why a Down Payment Matters:

- Lower Loan Amount: A larger down payment means you borrow less money, which translates to lower monthly payments and less interest paid over the life of the loan.

- Improved Loan-to-Value (LTV) Ratio: The LTV ratio compares the amount you borrow to the car’s value. A lower LTV is more attractive to lenders because it means they have less financial exposure if the car depreciates or if you default on the loan.

- Offsetting Other Weaknesses: Pro tips from us: Even a modest down payment can significantly improve your loan terms or boost your approval chances if your credit score is average or your DTI ratio is slightly higher. It shows Capital One you have some skin in the game.

- Reduced Negative Equity Risk: Cars depreciate rapidly. A down payment helps prevent you from owing more on your car than it’s worth, a situation known as being "upside down" or having negative equity.

Typical Down Payment Percentages:

While there’s no fixed rule, a common recommendation is to put down at least 10% for a used car and 20% for a new car. However, any amount you can comfortably put down will be beneficial. Capital One will consider the down payment as a positive factor in your application.

4. Vehicle Requirements: What Kind of Car Qualifies?

It’s not just about your financial profile; the vehicle you intend to purchase also needs to meet certain criteria set by Capital One. These requirements are in place to manage their risk and ensure the collateral for the loan (the car itself) meets their standards.

Age and Mileage Limits:

Capital One typically finances new and used vehicles that are no more than 10 years old and have fewer than 120,000 miles on the odometer. These limits can sometimes be flexible depending on your credit profile and the specific loan product, but they serve as a general guideline. Older, high-mileage vehicles are considered higher risk due to potential mechanical issues and rapid depreciation.

Vehicle Value and Loan Amount:

The loan amount must be reasonable in relation to the vehicle’s market value. Capital One uses resources like Kelley Blue Book (KBB) or NADAguides to determine a fair market value. They won’t typically lend significantly more than the car is worth, as this increases their risk.

New vs. Used Cars:

Capital One finances both new and used vehicles. Generally, new cars often come with slightly better interest rates due to their higher value and lower depreciation risk. However, their used car programs are robust, making them a strong option for pre-owned vehicle purchases.

Approved Dealership Network:

Capital One works exclusively with a vast network of approved dealerships. You cannot use a Capital One auto loan to purchase a vehicle from a private seller. This network ensures that the dealerships meet certain quality and ethical standards, providing a smoother experience for both the borrower and the lender. You’ll need to use their Auto Navigator tool to find participating dealerships near you.

5. Residency and Age Requirements: The Basics

These are straightforward, non-negotiable requirements that ensure you are a legally eligible borrower.

- Legal Residency: You must be a legal resident of the United States. This typically means having a valid Social Security Number (SSN) and a verifiable U.S. address.

- Minimum Age: You must be at least 18 years old to enter into a loan agreement. In some states, the age of majority for contracts might be 19 or 21, so always check your local regulations.

6. Identification and Documentation: Proof You Are You

Once you’re ready to finalize your loan, Capital One will require specific documentation to verify your identity, residency, and financial information. Having these documents prepared in advance will significantly speed up the application process.

Commonly Required Documents Include:

- Valid Government-Issued Photo ID: Such as a driver’s license or state ID card.

- Proof of Residency: Utility bill, lease agreement, or mortgage statement showing your current address.

- Proof of Income: Recent pay stubs (1-2 months), W-2 forms, or tax returns for self-employed individuals. Bank statements might also be requested.

- Social Security Number (SSN): For identity verification and credit checks.

- Trade-in Information (if applicable): Vehicle title, registration, and payoff amount for any existing loan.

- Vehicle Information: Make, model, year, VIN, and mileage of the car you intend to purchase.

Ensuring all your documentation is accurate, current, and readily available is a crucial step. Any missing or outdated information can cause delays or even lead to a rejection.

Understanding Capital One’s Pre-Qualification Process

One of the most valuable tools Capital One offers is its Auto Navigator pre-qualification service. This step is highly recommended before you even set foot in a dealership. It provides a clear picture of what you can afford and what your potential loan terms might look like.

Soft vs. Hard Inquiry:

The beauty of Capital One’s pre-qualification is that it involves a "soft inquiry" on your credit report. This means it won’t negatively impact your credit score. It allows you to see if you’re likely to be approved and for how much, without any risk to your credit. A "hard inquiry," which does temporarily affect your score, only occurs when you submit a full application at the dealership and officially apply for the loan.

Benefits of Pre-Qualification:

- Shop with Confidence: You’ll know your approved loan amount and estimated monthly payments before you start car shopping, allowing you to focus on vehicles within your budget.

- No Obligation: Pre-qualification doesn’t commit you to a loan or a specific car.

- Time-Saving: It streamlines the process at the dealership, as much of the financial legwork is already done.

- Empowerment: Knowing your financing terms gives you leverage in negotiations at the dealership.

Based on my experience working with countless car buyers, the pre-qualification step is invaluable. It transforms the car buying experience from a stressful negotiation into a more confident and informed decision-making process.

Navigating the Application & Approval Journey

Once you’ve pre-qualified and found a car at a participating dealership, the next steps involve finalizing your loan.

- Select Your Vehicle: Choose a car that meets Capital One’s vehicle requirements and fits within your pre-qualified amount.

- Complete the Full Application: At the dealership, you’ll complete a full credit application. This is where the hard inquiry on your credit report will occur.

- Provide Documentation: Submit all the necessary documents we discussed earlier (ID, income proof, etc.).

- Review Loan Terms: Carefully review the final loan offer, including the interest rate, loan term, and monthly payments. Ensure they align with your expectations and budget.

- Sign and Drive: Once everything is in order, sign the loan agreement, and you’re ready to drive off in your new vehicle!

Strategies to Boost Your Chances of Approval

Even if you meet the basic Capital One car loan requirements, taking additional steps can significantly enhance your approval odds and potentially secure better loan terms.

- Improve Your Credit Score: If you have time before applying, focus on paying down high-interest debt, making all payments on time, and avoiding new credit applications. A few points increase can make a difference.

- Save for a Larger Down Payment: As discussed, a larger down payment reduces the amount you need to borrow and signals financial responsibility to the lender. Aim for 10-20% if possible.

- Consider a Co-signer: If your credit history is limited or your score is on the lower side, a co-signer with excellent credit can strengthen your application significantly. They assume equal responsibility for the loan, reducing Capital One’s risk.

- Choose an Affordable Car: Opting for a vehicle that is well within your budget, even below your pre-qualified amount, demonstrates financial prudence. This also helps keep your DTI ratio in check.

- Address Existing Debt: Reducing your existing debt, especially revolving credit card balances, will lower your DTI ratio and free up more of your income for car payments.

- Maintain Stable Employment: Lenders appreciate consistency. If you’ve been in your current job for a reasonable period, it works in your favor.

Common Misconceptions About Capital One Auto Loans

Let’s clear up a few common misunderstandings to help you approach your application with accurate information.

- "Capital One only lends to perfect credit." This is absolutely false. Capital One prides itself on serving a wide range of credit profiles, from excellent to subprime. Their flexible approach makes them accessible to many who might be turned down elsewhere.

- "Pre-qualification is a guaranteed approval." While pre-qualification gives you a strong indication of approval, it is not a final guarantee. The final approval depends on the full application, verification of all provided documents, and the specific vehicle chosen. Any significant changes in your financial situation between pre-qualification and final application could impact the outcome.

- "All dealerships accept Capital One financing." Capital One works with a specific network of approved dealerships. You must use their Auto Navigator tool to find participating dealers in your area. You cannot use their financing for a private party sale or at a non-partner dealership.

Beyond Approval: What to Consider Post-Loan

Securing your Capital One car loan is a significant achievement, but your financial journey doesn’t end there. Responsible management of your loan is crucial for your long-term financial health.

- Understand Your Loan Terms: Familiarize yourself with your interest rate, monthly payment amount, due date, and any fees. Mark your payment due date on your calendar.

- Make Timely Payments: This is paramount. Consistent, on-time payments are essential for building a positive credit history and avoiding late fees. Consider setting up automatic payments to ensure you never miss a due date.

- Monitor Your Credit: Regularly check your credit report to ensure your Capital One loan payments are being reported accurately. This helps you track your progress in building or rebuilding your credit.

- Refinancing Options: If your credit score significantly improves over time, or if interest rates drop, you might consider refinancing your car loan. This could lead to a lower interest rate and reduced monthly payments. Capital One itself offers refinancing options, or you might explore other lenders.

Conclusion: Your Roadmap to a Capital One Car Loan

Securing a car loan with Capital One is a highly achievable goal for many, thanks to their flexible lending practices and commitment to a wide range of credit profiles. By thoroughly understanding and addressing the Capital One car loan requirements – from your credit score and income stability to down payment considerations and vehicle criteria – you are empowering yourself to navigate the financing process with confidence.

Remember, preparation is key. Take the time to check your credit, gather your documents, and utilize Capital One’s pre-qualification tool. By presenting a strong, well-prepared application, you’ll significantly increase your chances of approval and be well on your way to driving the car you need and want.

Don’t let the financing process intimidate you. With this comprehensive guide, you now have the insights and strategies to approach your Capital One auto loan application effectively. Start your journey today and make your dream of a new vehicle a reality!

Further Reading:

- Want to dive deeper into managing your credit? Check out our article on How to Improve Your Credit Score for a Car Loan (Placeholder for an internal link).

- Considering a used car? Read our tips on What to Look for When Buying a Used Car (Placeholder for another internal link).

- For official information and to start your pre-qualification, visit the Capital One Auto Navigator (External link to a trusted source).