Unlocking Your Dream Ride: A Comprehensive Guide to Car Loan Programs

Unlocking Your Dream Ride: A Comprehensive Guide to Car Loan Programs Carloan.Guidemechanic.com

The thrill of a new car, the freedom of the open road, or simply the necessity of reliable transportation – these are powerful motivators. For most people, turning that dream into a reality involves navigating the world of car loan programs. Far from a simple transaction, auto financing is a multi-faceted process that can significantly impact your financial well-being.

Based on my experience in the financial and automotive sectors, understanding car loan programs is not just about getting approved; it’s about securing the best terms, avoiding pitfalls, and making an informed decision that benefits you in the long run. This comprehensive guide is designed to empower you with the knowledge and strategies needed to confidently finance your next vehicle, ensuring a smooth and advantageous journey from browsing to driving.

Unlocking Your Dream Ride: A Comprehensive Guide to Car Loan Programs

Understanding the Basics of Car Loan Programs

Before you even step foot into a dealership or contact a lender, it’s crucial to grasp the fundamental concepts of car loan programs. This foundational knowledge will serve as your compass, guiding you through the complexities and helping you make smarter financial choices. Don’t rush this initial learning phase; it’s where many common mistakes originate.

What is a Car Loan?

At its core, a car loan is a sum of money borrowed from a financial institution or lender specifically for the purpose of purchasing a vehicle. You, the borrower, agree to repay this amount, known as the principal, over a predetermined period, typically ranging from 24 to 84 months. This repayment includes an additional charge called interest, which is the cost of borrowing the money.

The loan acts as a secured debt, meaning the car itself serves as collateral. If you fail to make your payments as agreed, the lender has the legal right to repossess the vehicle to recover their losses. This structure protects the lender and is why interest rates for car loans are often lower than unsecured loans like personal loans.

Why Do You Need a Car Loan?

Few people have enough cash readily available to purchase a new or used car outright, especially given today’s vehicle prices. Car loan programs bridge this gap, making vehicle ownership accessible to a much broader population. They allow you to spread the substantial cost of a car over several years, breaking it down into manageable monthly payments.

Beyond accessibility, using a car loan can also be a strategic financial move. It can help you preserve your cash reserves for emergencies or other investments. Additionally, consistently making on-time car loan payments can be an excellent way to build or improve your credit history, opening doors to better financial products in the future.

Key Terminology Explained

Navigating car loan programs requires familiarity with specific financial terms. Understanding these definitions is not merely academic; it directly impacts your ability to compare offers and make sound decisions. Let’s break down the most important ones.

-

Annual Percentage Rate (APR): This is perhaps the most critical number to understand. APR represents the true annual cost of your loan, encompassing not only the interest rate but also any additional fees or charges imposed by the lender. A lower APR means a less expensive loan overall.

When comparing car loan offers, always focus on the APR rather than just the interest rate. It provides a more accurate picture of the total borrowing cost. Different lenders might quote similar interest rates but have varying fees, which the APR will consolidate.

-

Loan Term: This refers to the length of time you have to repay the loan, typically expressed in months (e.g., 60 months, 72 months). A shorter loan term usually means higher monthly payments but less interest paid over the life of the loan. Conversely, a longer term offers lower monthly payments but results in more interest accumulating over time.

Based on my experience, choosing the right loan term involves balancing your monthly budget with the total cost of the loan. While lower monthly payments might seem attractive, an excessively long term can lead to paying significantly more for the car than its actual value, especially as depreciation kicks in.

-

Principal: The principal is the original amount of money you borrow to purchase the vehicle, after any down payment or trade-in value has been deducted. This is the base amount upon which interest is calculated. As you make payments, a portion goes towards reducing the principal, and another portion covers the interest.

Understanding the principal helps you track how much you still owe on the car. It’s important to remember that early payments primarily cover interest, and later payments contribute more significantly to reducing the principal balance.

-

Interest: This is the fee charged by the lender for the use of their money. It’s usually expressed as a percentage of the principal balance. Interest rates can be fixed (staying the same throughout the loan term) or variable (fluctuating with market conditions).

The interest rate directly affects your monthly payment and the total amount you pay back. Even a small difference in the interest rate can translate into hundreds or thousands of dollars saved or spent over the life of the loan.

-

Down Payment: A down payment is the initial amount of money you pay upfront towards the purchase price of the car. It reduces the total amount you need to borrow, thereby lowering your monthly payments and the overall interest you’ll pay. Lenders often view a substantial down payment as a sign of financial stability and commitment.

Pro tips from us: Aim for a down payment of at least 10-20% of the car’s purchase price, if possible. This not only makes your loan more affordable but can also help you secure better interest rates and protect you from being "upside down" on your loan (owing more than the car is worth).

-

Trade-in Value: If you own an existing car, you might be able to use its value as part of your down payment when purchasing a new vehicle. This is known as a trade-in. The dealership appraises your old car and deducts that amount from the price of the new one, reducing the amount you need to finance.

Always research your car’s trade-in value beforehand using independent sources like Kelley Blue Book or Edmunds. This prevents you from being low-balled by a dealership and helps you negotiate more effectively.

-

Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. Lenders use DTI to assess your ability to take on additional debt and make timely loan payments. A lower DTI ratio generally indicates less financial risk to lenders.

Most lenders prefer a DTI ratio of 36% or lower, though some may approve loans with higher ratios depending on other factors like your credit score. Calculating your DTI before applying for a car loan gives you a realistic picture of your borrowing capacity.

Types of Car Loan Programs: Finding Your Perfect Match

Not all car loan programs are created equal. Different types cater to various financial situations, vehicle choices, and preferences. Understanding these distinctions is crucial for selecting the financing option that best aligns with your needs.

New Car Loans vs. Used Car Loans

The primary difference between new and used car loans often lies in their interest rates and available terms. New car loans typically come with lower interest rates due to the vehicle’s higher value, longer lifespan, and lower risk of mechanical issues. Lenders see new cars as more secure collateral.

Used car loans, conversely, often carry slightly higher interest rates. This is because used vehicles are seen as having a higher risk of mechanical failure and faster depreciation. The loan terms for used cars may also be shorter, as lenders want to ensure the loan is paid off before the car’s value significantly diminishes.

Direct Loans vs. Dealership Financing

When financing a car, you essentially have two main avenues: getting a direct loan from a bank, credit union, or online lender, or securing financing directly through the car dealership. Each has its own set of advantages and disadvantages.

Direct loans allow you to get pre-approved for a specific loan amount before you even step into a dealership. This gives you significant leverage, as you walk in with your own financing in hand, effectively making you a cash buyer. You can then focus solely on negotiating the car’s price without the pressure of financing discussions.

Dealership financing, on the other hand, involves the dealership acting as an intermediary, working with various lenders to find a loan for you. They might offer promotional rates or special incentives, sometimes even beating direct loan offers. However, the convenience often comes with less transparency, and there’s a risk of markups on interest rates. Pro tips from us: Always get pre-approved for a direct loan first, even if you plan to use dealership financing. This benchmark allows you to compare and negotiate for the best possible deal.

Refinancing Car Loans

Refinancing a car loan means taking out a new loan to pay off your existing one, often with more favorable terms. This can be a smart move if interest rates have dropped since you originally financed your car, if your credit score has significantly improved, or if you simply want to lower your monthly payments by extending the loan term.

Common mistakes to avoid are not researching current market rates or assuming your current lender offers the best deal. Always shop around for refinancing offers from multiple lenders to ensure you’re getting the most competitive rate.

Specialty Loans: Bad Credit and First-Time Buyer Programs

For individuals with less-than-perfect credit or those with no credit history, obtaining a traditional car loan can be challenging. However, several specialty car loan programs are designed to assist these borrowers. Bad credit car loans often come with higher interest rates due to the increased risk for lenders, but they provide an opportunity to secure transportation and rebuild credit.

First-time buyer programs are specifically tailored for individuals with limited or no credit history. These programs may have more flexible eligibility criteria but often require a stable income, a reasonable down payment, and sometimes a co-signer. Both options offer a pathway to vehicle ownership and, more importantly, a chance to establish a positive credit footprint.

Factors Influencing Your Car Loan Approval and Terms

The terms of your car loan – specifically whether you’re approved and at what interest rate – are determined by a combination of factors. Lenders meticulously assess these elements to gauge your creditworthiness and the risk involved in lending to you. Understanding these factors allows you to prepare and potentially improve your chances of securing a favorable loan.

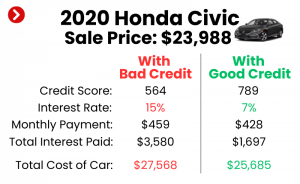

Your Credit Score: The Ultimate Game Changer

Your credit score is arguably the single most important factor in determining your car loan terms. It’s a numerical representation of your creditworthiness, based on your payment history, outstanding debt, length of credit history, and other factors. A higher credit score (typically 700+) indicates a lower risk to lenders, translating into lower interest rates and more flexible loan terms.

Conversely, a lower credit score signals higher risk, leading to higher interest rates or even loan denial. Lenders use various scoring models, like FICO and VantageScore, but the principle remains the same. To dive deeper into improving your financial standing, read our guide on .

Income and Debt-to-Income Ratio

Lenders need assurance that you can comfortably afford your monthly loan payments. They assess this through your income and your debt-to-income (DTI) ratio. Your stable employment history and sufficient income demonstrate your ability to meet financial obligations.

The DTI ratio provides a clearer picture by comparing your total monthly debt payments (including the proposed car loan) to your gross monthly income. A low DTI ratio (typically under 36%) suggests you have ample disposable income to handle new debt, making you a more attractive borrower.

Down Payment: The Power of Upfront Cash

Making a significant down payment sends a strong signal to lenders about your commitment and financial stability. It directly reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the life of the loan.

A substantial down payment also reduces the lender’s risk, as there’s less money outstanding against the collateral (the car). This can often lead to better interest rates and more favorable loan terms. Furthermore, it helps prevent you from owing more than the car is worth, especially in the early years of ownership when depreciation is highest.

Loan Term Length: Balancing Monthly Payments and Total Cost

The length of your loan term directly impacts your monthly payments and the total interest you’ll pay. Shorter terms (e.g., 36 or 48 months) mean higher monthly payments but significantly less interest paid overall. Longer terms (e.g., 72 or 84 months) offer lower monthly payments, making the car seem more affordable, but you’ll end up paying substantially more in interest over the life of the loan.

Based on my experience, while a longer term might alleviate immediate budget pressure, it often results in you paying far more for the car than its actual value. It’s a delicate balance: aim for the shortest term you can comfortably afford without straining your budget.

Vehicle Age and Type

The vehicle you choose also plays a role in your loan approval and terms. Lenders consider the car’s age, mileage, and type when assessing risk. Newer vehicles with lower mileage are generally seen as less risky because they are less likely to break down and have a higher resale value, making them better collateral.

Older, higher-mileage vehicles may face higher interest rates or shorter loan terms due to increased mechanical risk and faster depreciation. Exotic or highly customized vehicles might also be viewed differently than standard models, potentially affecting loan availability or terms.

Interest Rates: What Drives the Cost of Borrowing

Interest rates are the cost of borrowing money, and they are influenced by a combination of market conditions, the lender’s policies, and your individual creditworthiness. They can be fixed, meaning the rate remains constant throughout the loan term, or variable, meaning the rate can fluctuate based on a benchmark index.

Fixed interest rates offer predictability in your monthly payments, making budgeting easier. Variable rates, while potentially starting lower, carry the risk of increasing over time, leading to higher payments. For car loans, fixed rates are far more common and generally recommended for stability.

The Car Loan Application Process: A Step-by-Step Guide

Securing a car loan doesn’t have to be daunting. By breaking down the application process into manageable steps, you can approach it with confidence and ensure you’re making the best decisions for your financial situation. Preparation is key to a smooth and successful experience.

Step 1: Assess Your Financial Health

Before you even think about looking at cars, take a deep dive into your own finances. Check your credit score and review your credit report for any inaccuracies. Understand your current income, expenses, and existing debts. This assessment helps you determine a realistic budget for a car and how much you can truly afford for a monthly payment.

Don’t just think about the car payment; factor in insurance, fuel, maintenance, and potential registration fees. Overlooking these additional costs is a common mistake that can lead to financial strain down the road.

Step 2: Get Pre-Approved

One of the smartest moves you can make is to get pre-approved for a car loan from a bank, credit union, or online lender before you visit a dealership. Pre-approval gives you a concrete loan amount and an interest rate based on your credit profile. This transforms you into a "cash buyer" at the dealership, giving you significant negotiation power on the vehicle’s price.

Pro tips from us: Always get multiple pre-approvals. Comparing offers from several lenders allows you to see the best available interest rates and terms, ensuring you don’t settle for a less favorable deal from the dealership.

Step 3: Research and Choose Your Vehicle

With your budget and pre-approval in hand, you can now confidently research and choose the vehicle that fits your needs and financial parameters. Consider factors like reliability, fuel efficiency, safety ratings, and resale value. Don’t fall in love with a car that’s outside your established budget; stick to your limits.

Remember that the type of vehicle (new vs. used, luxury vs. economy) can also influence the specific loan terms available. Aligning your car choice with your pre-approved loan amount is crucial.

Step 4: Negotiate the Price

Once you’ve found your desired vehicle, focus on negotiating the car’s purchase price separately from the financing. With a pre-approval, the dealership knows you have financing options, which empowers you to drive a harder bargain on the car itself. Avoid discussing your monthly payment initially; instead, focus on the total out-the-door price.

Common mistakes to avoid are allowing the salesperson to bundle the car price and financing discussions. This makes it harder to identify where you might be overpaying.

Step 5: Finalize Your Loan

After agreeing on a car price, you can then compare your pre-approved loan offer with any financing options the dealership presents. Choose the option that offers the lowest APR and best terms for you. Read all documents carefully before signing. Pay close attention to the fine print, including any additional fees, warranties, or add-ons that might be rolled into the loan.

Ensure you understand the full breakdown of your monthly payments, the total amount you’ll pay over the loan term, and any prepayment penalties. Never feel rushed into signing; take your time to review everything.

Navigating Interest Rates and Fees

The true cost of your car loan extends beyond just the principal amount. Understanding the various interest rates and fees associated with car loan programs is vital for an accurate assessment of affordability and for avoiding unexpected expenses. These elements significantly impact your total repayment amount.

Annual Percentage Rate (APR) Explained

As mentioned earlier, the Annual Percentage Rate (APR) is the most comprehensive measure of the cost of borrowing. It includes not only the nominal interest rate but also other charges and fees levied by the lender, such as origination fees or documentation fees, expressed as an annualized percentage. This makes APR a more accurate tool for comparing different loan offers than just the interest rate alone.

A lower APR directly translates to a lower total cost for your loan over its entire term. Always prioritize securing the lowest possible APR when shopping for car loan programs.

Common Fees Associated with Car Loans

While the interest rate and APR are the main components, various fees can also contribute to the overall cost of your car loan. Being aware of these can help you anticipate and question them.

- Origination Fees: Some lenders charge an origination fee for processing your loan application. This fee is often a percentage of the loan amount or a flat fee.

- Documentation (Doc) Fees: Dealerships commonly charge a "doc fee" to cover the cost of preparing and processing paperwork. These fees can vary significantly by state and dealership.

- Late Payment Fees: If you miss a payment or pay late, lenders will impose a late payment fee. These can add up quickly and negatively impact your credit score.

- Prepayment Penalties: While less common with car loans, some lenders might charge a penalty if you pay off your loan early. Always check for this clause in your loan agreement, though it’s generally advisable to avoid loans with such penalties if possible.

Fixed vs. Variable Interest Rates

When it comes to interest rates, you’ll primarily encounter two types: fixed and variable. The choice between them impacts the predictability and potential cost of your loan.

A fixed interest rate means your interest rate remains constant for the entire duration of the loan. Your monthly payment for the principal and interest will stay the same, providing stability and making budgeting straightforward. For car loans, fixed rates are overwhelmingly common and generally preferred by borrowers for their predictability.

A variable interest rate, on the other hand, can fluctuate over the loan term based on changes in a benchmark interest rate (like the prime rate). While a variable rate might start lower than a fixed rate, it carries the risk of increasing, which would raise your monthly payments. Variable rates are rare for standard car loan programs but are worth understanding.

Smart Strategies for Securing the Best Car Loan

Getting a car loan isn’t just about applying and hoping for the best; it’s about strategic planning and proactive measures. Employing these smart strategies can significantly improve your chances of approval and help you secure the most favorable terms possible.

Boost Your Credit Score

Since your credit score is a primary determinant of your interest rate, taking steps to improve it before applying for a loan is incredibly beneficial. Start by checking your credit report for errors and disputing any inaccuracies. Make sure all your current bills are paid on time, as payment history is the most influential factor. Reduce your outstanding debt, especially on credit cards, to lower your credit utilization ratio.

Even a slight improvement in your credit score can move you into a better credit tier, potentially saving you hundreds or thousands of dollars in interest over the life of the loan.

Save for a Larger Down Payment

The more you can pay upfront, the less you need to borrow, which directly translates to lower monthly payments and reduced total interest paid. A larger down payment also signals financial strength to lenders, potentially earning you a lower interest rate. Aim for at least 10-20% of the car’s purchase price, if feasible.

This strategy also helps prevent you from going "upside down" on your loan, where you owe more than the car is worth due to rapid depreciation, especially common with new vehicles.

Shop Around for Lenders

Never settle for the first car loan offer you receive, whether it’s from your bank or a dealership. Actively shop around and compare offers from at least three to five different lenders, including banks, credit unions, and online lenders. Each lender has different criteria and rates, and what one offers might be significantly better than another.

The "rate shopping" period, typically 14-45 days depending on the credit scoring model, allows you to apply for multiple loans without significantly harming your credit score. All inquiries within this period for the same type of loan are usually counted as a single hard inquiry.

Consider a Shorter Loan Term

While longer loan terms offer lower monthly payments, they dramatically increase the total interest paid over the life of the loan. If your budget allows, opt for the shortest loan term you can comfortably afford. This strategy accelerates your equity building in the car and reduces the overall cost of borrowing.

For instance, a 48-month loan will almost always be cheaper in the long run than a 72-month loan for the same principal amount, even if the monthly payments are higher.

Read the Fine Print

This cannot be stressed enough: always, always read the fine print of any loan agreement before you sign. Understand every clause, fee, and condition. Look for prepayment penalties, late payment fees, and any optional add-ons that might have been included without your full understanding.

Common mistakes to avoid are only focusing on the monthly payment. While important, it’s crucial to understand the total cost of the loan, including all interest and fees. If you don’t understand something, ask for clarification. Don’t be afraid to walk away if you’re not comfortable with the terms.

Refinancing Your Car Loan: When and Why

Even after you’ve secured a car loan, your financial journey doesn’t have to be static. Refinancing your car loan can be a powerful tool to improve your financial situation, potentially saving you money or making your monthly budget more manageable.

What is Car Loan Refinancing?

Refinancing a car loan means taking out a brand-new loan to pay off your existing auto loan. Essentially, you’re replacing your old loan with a new one, ideally with more favorable terms such as a lower interest rate, a different loan term, or reduced monthly payments. The new lender pays off your original loan, and you then begin making payments to the new lender.

This process is similar to how people refinance home mortgages and can yield significant financial benefits depending on your circumstances and market conditions.

Benefits of Refinancing

There are several compelling reasons why you might consider refinancing your car loan:

- Lower Interest Rate: If your credit score has improved since you first took out the loan, or if market interest rates have dropped, you might qualify for a significantly lower APR. This directly reduces the total cost of your loan.

- Lower Monthly Payments: By securing a lower interest rate or extending your loan term (though this might increase total interest paid), you can reduce your monthly car payment. This can free up cash flow for other expenses or savings.

- Shorter Loan Term: If your financial situation has improved, you might be able to afford higher monthly payments. Refinancing to a shorter term can help you pay off your car faster and save substantially on interest, even if your original interest rate was good.

- Remove a Co-signer: If you initially needed a co-signer due to your credit, refinancing once your credit has improved can allow you to remove them from the loan, relieving them of their financial obligation.

When to Consider Refinancing

Timing is everything when it comes to refinancing. Consider this option if:

- Your Credit Score Has Improved: If you’ve been diligently making payments and managing your credit responsibly, your credit score likely has risen, making you eligible for better rates.

- Interest Rates Have Dropped: General market interest rates can fluctuate. If rates are lower now than when you first financed, you could save money.

- Your Financial Situation Has Changed: Perhaps you got a raise, paid off other debts, or simply want to free up cash. Refinancing can adjust your payments to better suit your current budget.

- You Want a Shorter Term: If you’re tired of making payments and want to pay off the car faster, refinancing to a shorter term can accelerate that goal, provided you can handle the higher monthly payments.

- You Have an Unfavorable Loan: If you regret the terms of your original loan (e.g., very high interest rate, long term), refinancing offers a second chance to get a better deal.

Understanding Car Loan Scams and Pitfalls

While most car loan programs are legitimate, the automotive financing landscape, unfortunately, is not immune to deceptive practices. Being aware of common scams and pitfalls is crucial for protecting yourself and your finances. Vigilance and informed decision-making are your best defenses.

"Yo-Yo" Financing

This scam occurs when a dealership allows you to drive off the lot with a new car, telling you the financing is approved, only to call you back days or weeks later claiming the financing fell through. They then demand you sign a new contract with worse terms (higher interest rate, larger down payment, or longer term) or return the car. By this point, you might have traded in your old car, making it harder to walk away.

Always ensure your financing is 100% finalized and signed before taking possession of the vehicle. Do not accept a "conditional delivery" unless you are fully prepared for the car to be returned.

"Spot Delivery" Scams

Similar to "yo-yo" financing, spot delivery involves taking possession of the car before the financing is truly approved. The difference is that the dealership might intentionally hold onto your trade-in or down payment check, making it difficult for you to back out if the financing terms change. They pressure you to sign a new, less favorable contract to avoid losing your trade-in or deposit.

Never leave your trade-in or down payment check with a dealership until all paperwork, including the finalized loan agreement, is signed and approved.

Hidden Fees and Add-ons

Dealerships sometimes try to increase their profit by quietly adding various products or services into your loan contract. These can include extended warranties, rust protection, paint sealant, fabric protection, GAP insurance (though this can be legitimate, compare prices), or credit life insurance. While some of these might be useful, they are often overpriced and can significantly inflate your loan amount.

Scrutinize every line item on the contract. If you don’t understand a charge or didn’t explicitly request a product, question it and insist on its removal. Remember, most add-ons are optional.

High-Pressure Tactics

Some salespeople use aggressive tactics to rush you into a decision or to accept unfavorable terms. They