Unlocking Your Dream Ride: A Comprehensive Guide to Fibre Federal Car Loans

Unlocking Your Dream Ride: A Comprehensive Guide to Fibre Federal Car Loans Carloan.Guidemechanic.com

The journey to owning a new or used vehicle is often an exciting one, filled with anticipation and the promise of new adventures on the open road. However, for many, the path to car ownership runs directly through the complex landscape of auto financing. Securing the right loan can be the difference between a smooth ride and a bumpy financial journey. This is where understanding your options, particularly those offered by member-focused institutions like Fibre Federal Credit Union, becomes paramount.

In this exhaustive guide, we’re delving deep into everything you need to know about Fibre Federal Car Loans. Whether you’re a long-time member, considering joining, or simply exploring competitive financing options, this article will serve as your ultimate resource. We’ll cover loan types, application processes, expert tips, and common pitfalls to avoid, ensuring you’re well-equipped to make an informed decision for your next vehicle purchase.

Unlocking Your Dream Ride: A Comprehensive Guide to Fibre Federal Car Loans

Why Choose a Credit Union Like Fibre Federal for Your Car Loan?

Before we dive into the specifics of Fibre Federal’s offerings, it’s crucial to understand the fundamental difference between credit unions and traditional banks. This distinction often translates directly into better value for you, the borrower.

Credit unions are not-for-profit financial cooperatives owned by their members. This means their primary goal isn’t to generate profits for shareholders, but rather to provide competitive rates, lower fees, and excellent service to their member-owners. This philosophy profoundly impacts their loan products, including auto loans.

Based on my experience in the financial sector, credit unions consistently offer a more personalized approach. Unlike large commercial banks, where you might feel like just another number, Fibre Federal, as a credit union, prides itself on building relationships. This member-centric model often results in more flexible terms and a genuine desire to help you achieve your financial goals, not just sell you a product.

Exploring the Range of Fibre Federal Auto Financing Options

Fibre Federal Credit Union understands that every car buyer’s needs are unique. That’s why they offer a comprehensive suite of auto loan products designed to fit various situations, from first-time buyers to those looking to refinance an existing loan.

Let’s break down the different types of Fibre Federal Car Loans available:

1. New Car Loans

Purchasing a brand-new vehicle is a significant investment, and securing the right financing is crucial. Fibre Federal’s new car loans are typically designed for vehicles that have never been titled or have very low mileage.

These loans often come with the most attractive interest rates due to the vehicle’s pristine condition and higher resale value, which reduces the lender’s risk. Fibre Federal provides competitive rates and flexible terms, allowing you to tailor your monthly payments to fit your budget. They understand that a new car represents not just transportation, but often a major life milestone.

When applying for a new car loan, you’ll generally find that lenders are more willing to offer longer loan terms, though it’s wise to consider the total interest paid over the life of the loan. Pro tips from us include always comparing the Annual Percentage Rate (APR) across different lenders, not just the interest rate, to get a true picture of the loan’s cost.

2. Used Car Loans

The used car market offers excellent value, and Fibre Federal provides robust financing options for pre-owned vehicles. Used car loans are designed for vehicles that have been previously owned and titled.

While rates for used cars might be slightly higher than for new cars, Fibre Federal strives to keep them competitive. Factors like the vehicle’s age, mileage, and condition will influence the loan terms and interest rate you qualify for. They often have specific guidelines regarding the maximum age or mileage a vehicle can have to be eligible for financing.

It’s important to secure pre-approval for a used car loan before you start shopping. This gives you significant leverage in negotiations, as you’ll know exactly how much you can afford and what your monthly payments will look like. This also helps you avoid common mistakes like falling in love with a car outside your budget.

3. Auto Loan Refinancing

Perhaps you secured a car loan a few years ago when your credit score wasn’t as strong, or interest rates have dropped significantly since then. Auto loan refinancing with Fibre Federal can be a smart financial move.

Refinancing involves taking out a new loan to pay off your existing car loan, ideally at a lower interest rate or with more favorable terms. This can lead to lower monthly payments, significant savings on interest over the life of the loan, or even help you adjust your loan term. Common mistakes to avoid when refinancing include not checking for any prepayment penalties on your current loan or extending the loan term so much that you end up paying more in interest overall, even with a lower rate.

Fibre Federal’s refinancing options are designed to help members improve their financial standing. If your credit score has improved, or if you’re looking to free up some cash flow, exploring refinancing with Fibre Federal is definitely worthwhile. For a deeper dive into improving your financial standing before applying, check out our article on "Boosting Your Credit Score for a Car Loan."

4. Lease Buyout Loans

For those currently leasing a vehicle, Fibre Federal also offers lease buyout loans. As your lease term approaches its end, you might find that you love your car and want to keep it. A lease buyout loan allows you to finance the purchase of the leased vehicle at its residual value.

This option can be beneficial if the market value of your leased vehicle is higher than its residual value, or if you simply prefer the convenience and familiarity of keeping your current car. Fibre Federal can help you transition from leasing to ownership smoothly, offering competitive rates for this specific type of auto financing.

Understanding Fibre Federal Car Loan Rates and Terms

Navigating car loan rates and terms can feel like deciphering a complex code. However, understanding these elements is fundamental to securing a favorable deal on your Fibre Federal Car Loan.

Factors Influencing Your Interest Rate

Several key factors determine the interest rate you’ll be offered:

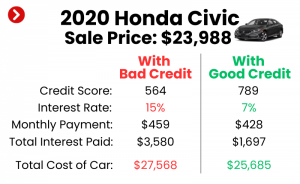

- Credit Score: This is perhaps the most significant factor. A higher credit score signals lower risk to lenders, often resulting in lower interest rates. Fibre Federal, like all lenders, uses your credit history to assess your creditworthiness.

- Loan Term: Shorter loan terms typically come with lower interest rates because the lender’s risk is spread over a shorter period. Conversely, longer terms might have slightly higher rates.

- Vehicle Type (New vs. Used): As mentioned, new cars generally command lower rates due to their higher value and perceived reliability.

- Down Payment: A larger down payment reduces the amount you need to borrow, which can lead to a lower interest rate and certainly a lower monthly payment. It also shows the lender you have skin in the game.

- Debt-to-Income Ratio: Fibre Federal will also look at your existing debts compared to your income to ensure you can comfortably manage the new loan payments.

Fixed vs. Variable Rates

Almost all auto loans, including those from Fibre Federal, come with a fixed interest rate. This means your interest rate will remain the same throughout the life of the loan, providing predictable monthly payments.

Variable rates, while common for some other loan types, are rare for car loans because they introduce uncertainty into your budget, which most car buyers prefer to avoid. The stability of a fixed rate is a significant benefit for long-term financial planning.

Loan Terms: Short vs. Long

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months).

- Shorter Terms (e.g., 36-48 months): These result in higher monthly payments but mean you pay less interest over the life of the loan and build equity faster. This is often the most financially savvy option if you can afford the higher payments.

- Longer Terms (e.g., 60-72+ months): These offer lower monthly payments, making expensive vehicles more "affordable" on a month-to-month basis. However, you’ll pay significantly more in total interest and risk owing more than the car is worth (being "upside down") as it depreciates.

Pro tips from us: Always balance the lowest possible interest rate with a loan term that comfortably fits your budget without extending it unnecessarily.

The Fibre Federal Car Loan Application Process: A Step-by-Step Guide

Applying for a car loan doesn’t have to be daunting. Fibre Federal strives to make the process as straightforward and transparent as possible. Knowing what to expect can significantly reduce stress and speed up your approval.

1. Preparation is Key: Gather Your Documents

Before you even start the application, gather the necessary documentation. This proactive step can save you time and prevent delays.

You’ll typically need:

- Proof of Identity: A valid government-issued ID (driver’s license, state ID).

- Proof of Income: Recent pay stubs, W-2s, or tax returns (if self-employed).

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Social Security Number: For credit verification.

- Vehicle Information (if you’ve chosen a car): VIN, make, model, year, and mileage.

- Membership Information: If you’re already a Fibre Federal member, have your account details ready. If not, you may need to apply for membership concurrently.

2. The Application: Online, In-Person, or Phone

Fibre Federal offers multiple convenient ways to apply for your auto loan.

- Online Application: This is often the quickest and most popular method. You can complete the application from the comfort of your home, typically available 24/7. The online portal will guide you through each step.

- In-Person: Visit a Fibre Federal branch to speak directly with a loan officer. This allows for personalized assistance and the opportunity to ask any questions you might have.

- By Phone: You can also apply over the phone during business hours, speaking with a loan specialist who can guide you through the process.

3. Credit Check & Underwriting

Once you submit your application, Fibre Federal will perform a credit check. This allows them to review your credit history, credit score, and overall financial health.

The underwriting team then assesses your application, considering all the factors discussed earlier, to determine your eligibility, the interest rate, and the loan amount you qualify for. This stage is where your preparation pays off, as complete and accurate information speeds up the review.

4. Approval & Closing

If your loan is approved, you’ll receive a loan offer outlining the terms, interest rate, and monthly payment. You’ll then proceed to the closing process, which involves signing the loan agreement.

This is the point where funds are disbursed, either directly to the dealership or to you, depending on whether you’re buying a new car or refinancing. Pro tips from us: always read the loan agreement carefully before signing, ensuring all terms match what was discussed and agreed upon.

Key Benefits of Choosing Fibre Federal for Your Auto Loan

When considering where to finance your next vehicle, Fibre Federal Credit Union presents a compelling case. Their member-first approach translates into several distinct advantages.

Here are the key benefits of securing your Fibre Federal Car Loan:

- Competitive Rates: As a not-for-profit institution, Fibre Federal can often offer lower interest rates on auto loans compared to traditional banks. This directly translates to significant savings over the life of your loan.

- Flexible Terms: They understand that one size doesn’t fit all. Fibre Federal works with members to establish loan terms that align with individual budgets and financial goals, offering a range of repayment schedules.

- Personalized Service: Unlike larger institutions, Fibre Federal prides itself on its community focus and personalized member service. You’re not just a transaction; you’re a member-owner, and their team is dedicated to guiding you through the financing process with care and expertise.

- Local Community Support: By choosing Fibre Federal, you’re investing in a local institution that often reinvests in the community it serves. This creates a positive feedback loop, strengthening the local economy.

- No Hidden Fees: Credit unions are generally known for their transparency. You can expect clear communication regarding any fees associated with your loan, with a focus on straightforward terms.

Common Mistakes to Avoid When Applying for a Car Loan

Based on my experience counseling individuals on auto financing, several common pitfalls can derail an otherwise smooth process. Being aware of these can save you money and stress.

Here are common mistakes to avoid:

- Not Checking Your Credit Score: Your credit score is the foundation of your loan application. Not knowing it means you can’t identify errors or work to improve it before applying. Get your free credit report well in advance.

- Only Getting One Quote: Never settle for the first loan offer you receive, especially from a dealership. Always shop around and compare offers from multiple lenders, including credit unions like Fibre Federal.

- Ignoring the Total Cost of Ownership: Focus solely on the monthly payment can be misleading. Consider the total interest paid, insurance costs, maintenance, and fuel efficiency. A lower monthly payment over a longer term often means a higher total cost.

- Extending Loan Terms Too Long: While longer terms mean lower monthly payments, they dramatically increase the total interest paid. They also increase the risk of being "upside down" on your loan, owing more than the car is worth.

- Falling for Dealer Financing Traps Without Comparison: Dealerships often offer convenient financing, but their rates may not always be the most competitive. Get pre-approved by Fibre Federal first, so you have a strong negotiating position.

Pro Tips for Securing the Best Fibre Federal Car Loan

Armed with knowledge about common mistakes, let’s now focus on strategies to ensure you get the most favorable terms for your Fibre Federal Car Loan.

These pro tips from us will empower you:

- Improve Your Credit Score: Start early. Pay bills on time, reduce existing debt, and dispute any errors on your credit report. A higher score translates directly to lower interest rates.

- Save for a Down Payment: Even a small down payment can make a significant difference. It reduces the loan amount, lowers your monthly payments, and can help you qualify for a better interest rate. Aim for at least 10-20% if possible.

- Know Your Budget Before Shopping: Determine how much you can truly afford for a monthly payment, considering insurance, fuel, and maintenance, before you even step onto a car lot. This prevents emotional overspending.

- Consider a Shorter Loan Term if Affordable: If your budget allows, opt for a shorter loan term. You’ll pay off the vehicle faster and save a substantial amount on interest over time.

- Get Pre-Approved! This is perhaps the most powerful tip. A pre-approval from Fibre Federal gives you a firm offer of credit, transforming you into a cash buyer. You can then focus on negotiating the best price for the car itself, knowing your financing is already secured.

- Negotiate the Car Price Separately: With pre-approval in hand, you can negotiate the car’s purchase price as if you were paying cash. Only after agreeing on the car price should you discuss any additional dealer financing options, comparing them to your Fibre Federal pre-approval.

Refinancing Your Existing Auto Loan with Fibre Federal: A Deeper Dive

Refinancing isn’t just for mortgages; it’s a powerful tool for optimizing your auto loan as well. Fibre Federal offers robust refinancing options that could save you money or improve your financial flexibility.

When is Refinancing a Good Idea?

Consider refinancing your auto loan with Fibre Federal if:

- Your Credit Score Has Improved: A better score often qualifies you for a significantly lower interest rate than when you initially took out the loan.

- Interest Rates Have Dropped: Market rates fluctuate. If current auto loan rates are lower than your existing rate, refinancing can lead to savings.

- You Want Lower Monthly Payments: By securing a lower rate or extending your loan term (use caution here), you can reduce your monthly outflow.

- You Want to Shorten Your Loan Term: If your financial situation has improved, you might be able to refinance to a shorter term, paying off the loan faster and saving on total interest, even if your monthly payment increases slightly.

- You Want to Remove a Co-signer: If your co-signer is ready to be released from the obligation, refinancing in your name alone, provided your credit qualifies, is the way to do it.

The refinancing process with Fibre Federal is similar to applying for a new loan, requiring documentation of your current vehicle and existing loan. If you’re still weighing your options between buying and leasing, our guide "Lease vs. Buy: Which Car Option is Right for You?" offers valuable insights.

Beyond the Loan: What Else Fibre Federal Offers

Fibre Federal’s commitment to its members extends beyond just competitive car loans. They offer a suite of services designed to support your complete financial well-being.

Consider these additional offerings:

- Payment Protection (GAP Insurance, Extended Warranty): These optional products can provide peace of mind. GAP (Guaranteed Asset Protection) insurance covers the "gap" between what your vehicle is worth and what you owe if it’s totaled. Extended warranties can cover unexpected repair costs after the manufacturer’s warranty expires.

- Financial Counseling: As a member-focused institution, Fibre Federal often provides access to financial education resources and counseling services to help you manage your money effectively.

- Other Banking Services: From checking and savings accounts to mortgages and personal loans, Fibre Federal can be your one-stop shop for all your financial needs, simplifying your banking life.

Frequently Asked Questions About Fibre Federal Car Loans

To provide an even more comprehensive overview, let’s address some common questions regarding Fibre Federal’s auto financing.

Q: Who is eligible for Fibre Federal membership?

A: Typically, credit unions have specific membership eligibility requirements, often based on where you live, work, worship, or if you’re related to an existing member. Check Fibre Federal’s official website for their specific eligibility criteria. It’s usually straightforward to join.

Q: Can I get a car loan with bad credit?

A: While a higher credit score yields better rates, Fibre Federal, like many credit unions, is often more willing to work with members who have less-than-perfect credit. They may offer options like a co-signer or slightly higher rates, focusing on your overall financial picture rather than just a score. It’s always best to speak directly with a loan officer.

Q: How long does the approval process take for a Fibre Federal Car Loan?

A: Often, decisions on auto loan applications can be made within a few hours to a couple of business days, especially if all required documentation is submitted promptly. Online applications can sometimes provide instant preliminary approvals.

Q: Can I apply for a loan without knowing the exact car I want to buy?

A: Absolutely! This is precisely what pre-approval is for. Fibre Federal can pre-approve you for a certain loan amount, allowing you to shop for a vehicle with confidence, knowing your financing is already in place.

Q: What happens if I miss a car loan payment?

A: Missing a payment can incur late fees and negatively impact your credit score. It’s crucial to contact Fibre Federal immediately if you anticipate difficulty making a payment. They may be able to work with you on a solution, such as a payment deferral, to avoid more severe consequences. For general information on understanding auto loan terms and consumer rights, the Consumer Financial Protection Bureau (CFPB) offers excellent resources.

Conclusion: Driving Towards Smart Auto Financing with Fibre Federal

Securing a car loan is a significant financial decision that impacts your budget for years to come. By understanding the ins and outs of Fibre Federal Car Loans, you empower yourself to make choices that align with your financial goals, rather than simply accepting the first offer. Fibre Federal Credit Union stands out as a strong contender in the auto financing landscape, offering competitive rates, flexible terms, and the personalized service that only a member-owned institution can truly provide.

Remember the key takeaways: do your research, prepare your documents, understand your credit score, and always get pre-approved before stepping onto the dealership lot. Avoiding common mistakes and leveraging expert tips will put you in the driver’s seat of your auto financing journey. Whether you’re buying new, used, or looking to refinance, exploring your options with Fibre Federal could be the smartest move you make towards unlocking your dream ride. Visit their official website or stop by a branch today to start your application and experience the credit union difference.