Unlocking Your Dream Ride: A Comprehensive Guide to Rhinebeck Bank Car Loans

Unlocking Your Dream Ride: A Comprehensive Guide to Rhinebeck Bank Car Loans Carloan.Guidemechanic.com

Getting behind the wheel of a new or pre-owned vehicle is an exciting prospect. For many, this dream becomes a reality through careful planning and securing the right financing. When it comes to local, reliable, and community-focused financial solutions, Rhinebeck Bank often stands out as a preferred choice for residents in the Hudson Valley and beyond.

As an expert blogger and SEO content writer, I understand the importance of making informed financial decisions. That’s why I’ve put together this super comprehensive guide to navigating Rhinebeck Bank car loans. Our goal is to provide you with an in-depth, unique, and actionable resource that helps you secure the best possible auto financing for your next vehicle.

Unlocking Your Dream Ride: A Comprehensive Guide to Rhinebeck Bank Car Loans

Why Choose Rhinebeck Bank for Your Car Loan? The Local Advantage

In a world dominated by national lenders, choosing a local institution like Rhinebeck Bank for your car loan offers distinct advantages. This isn’t just about convenience; it’s about building a relationship with a financial partner who understands your community and your needs. Based on my experience in financial content, local banks often provide a more personalized touch.

Community-Centric Approach

Rhinebeck Bank has deep roots in the communities it serves. This local focus means they often invest directly back into the region, fostering a sense of trust and reliability. When you apply for a Rhinebeck Bank car loan, you’re not just a number; you’re a valued community member.

They understand the local economy and specific financial challenges or opportunities that might impact their customers. This regional insight can sometimes translate into more flexible lending decisions compared to larger, more rigid national institutions.

Personalized Service and Support

One of the most significant benefits of working with a local bank is the personalized service. Unlike automated phone systems or generic online forms, Rhinebeck Bank typically offers direct access to loan officers. These professionals can walk you through every step of the Rhinebeck Bank car loan application process.

They are available to answer your specific questions, clarify terms, and provide tailored advice that fits your individual financial situation. This hands-on approach can be invaluable, especially for first-time car buyers or those with unique financial circumstances.

Competitive Rates and Flexible Terms

While often perceived as only for large institutions, local banks like Rhinebeck Bank frequently offer highly competitive interest rates on their auto loans. They strive to provide value to their customers to earn and retain their business within the community.

Beyond just rates, Rhinebeck Bank car loans often come with flexible repayment terms. This flexibility allows you to structure a loan that comfortably fits within your monthly budget, ensuring your vehicle purchase is sustainable in the long run.

Understanding Rhinebeck Bank Car Loan Options: Tailoring Your Financing

Rhinebeck Bank understands that one size doesn’t fit all when it comes to vehicle financing. They offer a range of car loan options designed to meet various needs, whether you’re buying new, used, or looking to refinance an existing auto loan. Knowing these options is the first step to making an informed decision.

New Car Loans

Purchasing a brand-new vehicle is an exciting milestone. Rhinebeck Bank provides competitive new car loan rates and terms to help make this dream a reality. These loans are typically for vehicles that have never been previously titled and are often purchased directly from a dealership.

New car loans often come with lower interest rates compared to used car loans, reflecting the lower risk associated with financing a brand-new asset. The longer lifespan and higher resale value of a new car make it an attractive option for lenders.

Used Car Loans

Used vehicles offer excellent value and are a popular choice for many budget-conscious buyers. Rhinebeck Bank also offers robust financing solutions for pre-owned cars, trucks, and SUVs. These loans apply to vehicles that have been previously owned and titled.

When considering a used car loan, the age, mileage, and condition of the vehicle can influence the loan terms. It’s crucial to ensure the vehicle has been thoroughly inspected to avoid unforeseen issues down the road.

Auto Refinancing Loans

Do you already have a car loan but feel like you’re paying too much in interest? Rhinebeck Bank’s auto refinancing options could be a game-changer. Refinancing involves taking out a new loan to pay off your existing one, ideally at a lower interest rate or with more favorable terms.

Refinancing can significantly reduce your monthly payments or the total amount of interest you pay over the life of the loan. Pro tips from us: if your credit score has improved since you first took out your loan, or if interest rates have dropped, refinancing is definitely worth exploring.

The Application Process: A Step-by-Step Guide to Securing Your Rhinebeck Bank Car Loan

Applying for a car loan can seem daunting, but breaking it down into manageable steps makes the process much clearer. Based on my experience, being prepared is key to a smooth and successful application. Here’s a detailed look at how to apply for a Rhinebeck Bank car loan.

Step 1: Pre-Approval – Your Smart First Move

Before you even step onto a dealership lot, getting pre-approved for a Rhinebeck Bank car loan is a smart strategy. Pre-approval gives you a clear understanding of how much you can borrow, your potential interest rate, and the estimated monthly payments. This empowers you to shop with confidence.

Having a pre-approval letter in hand effectively makes you a cash buyer. It removes the uncertainty of financing and gives you leverage in price negotiations with dealerships, as you already have your funding secured.

Step 2: Gather Your Essential Documents

When you’re ready to apply, whether for pre-approval or a direct loan, you’ll need to provide certain documents. Organizing these in advance will expedite your Rhinebeck Bank car loan application. Common mistakes to avoid are not having these documents readily available, which can cause unnecessary delays.

Here’s a typical checklist of what Rhinebeck Bank, like most lenders, will likely request:

- Proof of Identity: A valid government-issued ID, such as a driver’s license or passport. This verifies who you are.

- Proof of Income: Recent pay stubs (typically 2-3 months), W-2 forms, or tax returns (for self-employed individuals). This confirms your ability to repay the loan.

- Proof of Residency: Utility bills, lease agreements, or mortgage statements. This verifies your current address.

- Social Security Number: Used for credit checks and identification.

- Vehicle Information (if applicable): If you’ve already found your car, you’ll need details like the make, model, year, VIN, and purchase price.

Step 3: Complete the Application

You can typically complete the Rhinebeck Bank car loan application online, in person at one of their branches, or sometimes over the phone. Be thorough and accurate with all the information you provide. Any discrepancies could lead to delays or even rejection.

The application will ask for personal details, employment history, income information, and details about the vehicle you wish to purchase. If you have questions during this stage, don’t hesitate to reach out to a Rhinebeck Bank loan officer.

Step 4: Credit Review and Loan Decision

Once your application is submitted, Rhinebeck Bank will conduct a credit check. They will review your credit history, credit score, and debt-to-income ratio (DTI). This assessment helps them determine your creditworthiness and the risk associated with lending to you.

After their review, you will receive a decision. If approved, you’ll be presented with the loan terms, including the interest rate, loan amount, and repayment schedule. This is your opportunity to review everything carefully and ask any remaining questions.

Key Factors Influencing Your Car Loan Approval and Terms

Securing a favorable Rhinebeck Bank car loan isn’t just about applying; it’s about presenting yourself as a reliable borrower. Several key factors play a crucial role in determining whether your loan is approved and what interest rate and terms you’ll receive. Understanding these can help you prepare.

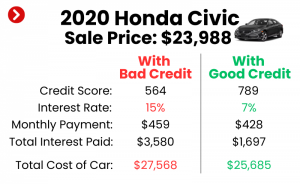

Your Credit Score: The Foundation of Your Application

Your credit score is arguably the most critical factor in car loan approval. It’s a three-digit number that summarizes your creditworthiness, based on your payment history, amounts owed, length of credit history, new credit, and credit mix. A higher score indicates lower risk to lenders.

Pro tips from us: Aim for a credit score of 670 or higher for the best chances of approval and lower interest rates. If your score is lower, consider taking steps to improve it before applying. For more insights on improving your credit score, check out our article on .

Debt-to-Income (DTI) Ratio: Can You Afford More Debt?

Your Debt-to-Income (DTI) ratio is another vital metric. It compares your total monthly debt payments to your gross monthly income. Lenders use DTI to assess your ability to manage additional monthly payments, like a car loan.

A lower DTI ratio indicates that you have more disposable income available to cover new debt obligations. Lenders typically prefer a DTI of 36% or less, though this can vary. A high DTI might signal to Rhinebeck Bank that you’re already stretched thin financially.

Income Stability and Employment History

Lenders want assurance that you have a steady and reliable source of income to make your monthly payments. A stable employment history, typically two years or more with the same employer, demonstrates reliability.

If you’ve recently changed jobs or are self-employed, you might need to provide additional documentation to prove consistent income. Rhinebeck Bank will assess your income to ensure it comfortably supports the proposed car loan payments alongside your other financial commitments.

Down Payment Amount: Reducing Your Loan Risk

Making a substantial down payment can significantly impact your Rhinebeck Bank car loan. A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the life of the loan.

Furthermore, a significant down payment signals to the bank that you are serious about your purchase and have a financial stake in the vehicle. This can make you a more attractive borrower and potentially lead to better loan terms.

Navigating Interest Rates and Loan Terms: Making the Best Choice

Understanding the interplay between interest rates and loan terms is crucial for managing the total cost of your Rhinebeck Bank car loan. These two elements directly impact your monthly payment and the overall financial burden of your vehicle purchase.

Understanding Interest Rates

The interest rate is the cost of borrowing money, expressed as a percentage of the loan amount. A lower interest rate means you pay less over the life of the loan. Rhinebeck Bank, like other lenders, determines your interest rate based on several factors, primarily your creditworthiness and the current market rates.

It’s important to differentiate between Annual Percentage Rate (APR) and the nominal interest rate. APR includes the interest rate plus any additional fees associated with the loan, giving you a more accurate picture of the total cost of borrowing.

Fixed vs. Variable Interest Rates

Most Rhinebeck Bank car loans will likely feature fixed interest rates. This means your interest rate remains the same throughout the entire loan term, providing predictable monthly payments. This stability is a significant advantage for budgeting.

While less common for standard auto loans, some financial products might offer variable rates. A variable rate can change over time, typically tied to a benchmark index. This introduces uncertainty into your monthly payments, making fixed rates generally preferred for car loans.

Choosing the Right Loan Term

The loan term is the duration over which you agree to repay the loan, often expressed in months (e.g., 36, 48, 60, 72 months). Choosing the right term involves balancing monthly affordability with the total cost of the loan.

- Shorter Terms: A shorter loan term (e.g., 36 or 48 months) usually means higher monthly payments but less interest paid over time. You pay off the loan faster and save money in the long run.

- Longer Terms: A longer loan term (e.g., 60 or 72 months) results in lower monthly payments, making the car more "affordable" on a month-to-month basis. However, you’ll pay more in total interest because you’re borrowing the money for a longer period.

Pro tips from us: Carefully consider your budget and future financial goals when selecting a loan term. While a lower monthly payment might be tempting, calculate the total interest paid to ensure you’re making a financially sound decision.

Pro Tips for a Smooth Rhinebeck Bank Car Loan Journey

Navigating the world of auto financing can be complex, but with the right approach, you can ensure a smooth and successful experience. Based on my years of observing lending practices, these pro tips can significantly enhance your journey to securing a Rhinebeck Bank car loan.

1. Know Your Budget Inside and Out

Before you even think about applying for a Rhinebeck Bank car loan, have a clear understanding of your personal finances. This means not just knowing what you can afford for a monthly payment, but what you should afford. Factor in not just the loan payment, but also insurance, fuel, maintenance, and potential registration fees.

Common mistakes to avoid are: falling in love with a car that pushes your budget to the absolute limit. This leaves no room for unexpected expenses and can quickly lead to financial stress. For a deeper dive into smart budgeting, our guide on might be helpful.

2. Boost Your Credit Score

As we discussed, your credit score is paramount. If it’s not where you want it to be, take proactive steps to improve it before applying. Pay bills on time, reduce existing debt, and avoid opening new lines of credit just before your loan application.

Even a slight improvement in your credit score can translate into a significantly lower interest rate on your Rhinebeck Bank car loan, saving you hundreds or even thousands of dollars over the loan term.

3. Don’t Settle for the First Offer

While Rhinebeck Bank strives to offer competitive rates, it’s always wise to compare. Obtain quotes from a few different lenders before committing. This helps you understand the market and ensures you’re getting the best possible deal.

However, be mindful of too many hard credit inquiries in a short period, as this can temporarily ding your score. Fortunately, credit scoring models typically count multiple auto loan inquiries within a 14-45 day window as a single inquiry.

4. Read the Fine Print Carefully

This cannot be stressed enough. Before signing any documents for your Rhinebeck Bank car loan, read every line of the loan agreement. Understand the interest rate, the full term, any prepayment penalties, and all associated fees.

If anything is unclear, ask questions. A reputable lender like Rhinebeck Bank will be happy to explain every detail until you are completely comfortable. Never sign a document you don’t fully understand.

Common Mistakes to Avoid When Applying for a Car Loan

Even the most prepared individuals can sometimes overlook crucial details when applying for a car loan. My experience has shown that avoiding these common pitfalls can save you time, money, and unnecessary stress during your Rhinebeck Bank car loan application process.

1. Not Getting Pre-Approved

One of the biggest mistakes is walking into a dealership without pre-approval. This puts you at a significant disadvantage during negotiations. Without knowing your financing limits, you might focus on monthly payments rather than the total purchase price, leading to an unfavorable deal.

Pre-approval from Rhinebeck Bank gives you a concrete budget and allows you to negotiate the car price separately from the financing. This streamlines the process and ensures you’re getting a fair deal on both fronts.

2. Focusing Solely on the Monthly Payment

While the monthly payment is important for budgeting, fixating on it exclusively can be misleading. Dealers might try to stretch out the loan term to lower the monthly payment, making the car seem more affordable. However, a longer term means you’ll pay significantly more in total interest.

Always consider the total cost of the Rhinebeck Bank car loan over its entire duration, including the principal and all interest charges. A slightly higher monthly payment for a shorter term can result in substantial savings.

3. Overlooking Additional Fees and Charges

A car loan isn’t just about the principal and interest. There can be various fees involved, such as origination fees, documentation fees, and sometimes even prepayment penalties (though less common with reputable lenders like Rhinebeck Bank).

Ensure you get a full breakdown of all costs associated with your Rhinebeck Bank car loan. These fees can add up and impact the true cost of your financing. Always ask for a clear itemized list.

4. Providing Inaccurate Information

Always be truthful and accurate on your loan application. Providing false or misleading information, even inadvertently, can lead to your application being denied. In some cases, it could even have legal consequences.

Double-check all figures, employment dates, and personal details before submitting your Rhinebeck Bank car loan application. Honesty and transparency build trust with your lender.

Beyond the Loan: What Happens After Approval?

Securing your Rhinebeck Bank car loan is a fantastic achievement, but the journey doesn’t end there. Understanding what happens next and how to manage your loan effectively is crucial for a positive financial outcome. This phase is all about responsible ownership.

Finalizing the Purchase

Once your Rhinebeck Bank car loan is approved and you’ve selected your vehicle, the next step is to finalize the purchase with the dealership or private seller. You’ll sign all the necessary paperwork, including the bill of sale and title transfer documents.

Rhinebeck Bank will then typically disburse the funds directly to the seller. Ensure all the details on the purchase agreement match your loan approval and your understanding of the transaction.

Setting Up Payments

Rhinebeck Bank will provide you with a clear repayment schedule. It’s highly recommended to set up automatic payments from your checking or savings account. This ensures your payments are made on time, every time, helping you avoid late fees and protecting your credit score.

Timely payments are critical not just for avoiding penalties, but also for maintaining a good credit history. This can be beneficial for future financial endeavors, like mortgages or other personal loans.

Managing Your Loan and Potential Early Payoff

Throughout the life of your Rhinebeck Bank car loan, you’ll receive statements detailing your remaining balance and payment history. It’s a good practice to review these periodically. If you find yourself in a better financial position, consider making extra payments towards your principal.

Paying off your car loan early can save you a significant amount in interest over time. Always check your loan agreement for any prepayment penalties, though these are rare with consumer-friendly auto loans. For general information on auto loan best practices, the Consumer Financial Protection Bureau offers excellent resources, which I often recommend to clients. .

Frequently Asked Questions About Rhinebeck Bank Car Loans

To further assist you, we’ve compiled some frequently asked questions about Rhinebeck Bank car loans. These address common queries and provide quick answers to help clarify your understanding.

Q1: What credit score do I need for a Rhinebeck Bank car loan?

A1: While there isn’t a single definitive minimum score, a credit score of 670 or higher generally increases your chances of approval and securing more favorable interest rates. Rhinebeck Bank considers various factors beyond just your score.

Q2: Can I get a Rhinebeck Bank car loan with bad credit?

A2: It can be more challenging, but not impossible. Rhinebeck Bank, being a local institution, might offer more flexibility than larger lenders. They may consider other factors like your income stability, down payment, and overall financial situation. You might be offered a higher interest rate to offset the increased risk.

Q3: How long does the Rhinebeck Bank car loan approval process take?

A3: Often, pre-approval decisions can be made relatively quickly, sometimes within one to two business days. The full approval process, once all documents are submitted, can vary but is generally efficient, especially if you’ve provided all required information upfront.

Q4: Can I finance a private party car purchase with Rhinebeck Bank?

A4: Yes, Rhinebeck Bank typically offers financing for private party vehicle purchases. The process might require additional steps, such as a vehicle inspection and title transfer verification, but it’s a common service.

Q5: What if I want to pay off my Rhinebeck Bank car loan early?

A5: Most consumer auto loans, including those from Rhinebeck Bank, do not have prepayment penalties. This means you can typically pay off your loan ahead of schedule without incurring extra fees, saving you money on interest. Always confirm this in your loan agreement.

Conclusion: Drive Towards Your Future with Confidence

Securing a Rhinebeck Bank car loan is more than just obtaining financing; it’s about partnering with a trusted local institution that understands your needs and supports your community. From understanding your options for new or used vehicles to navigating the application process and managing your loan effectively, this guide aims to equip you with all the knowledge you need.

By following our expert advice on preparation, understanding key influencing factors, and avoiding common pitfalls, you are well on your way to a smooth and successful car buying experience. With a Rhinebeck Bank car loan, you can confidently drive towards your next adventure, knowing you have a reliable financial partner by your side. Take the first step today and explore how Rhinebeck Bank can help you get behind the wheel of your dream car.