Unlocking Your Dream Ride: A Deep Dive into Car Loan Income Requirements

Unlocking Your Dream Ride: A Deep Dive into Car Loan Income Requirements Carloan.Guidemechanic.com

Dreaming of a new set of wheels? For many, a car loan is the bridge between aspiration and reality. But before you start test driving, there’s a crucial financial hurdle to understand: car loan income requirements. This isn’t just about having a job; it’s about proving to lenders that you have the consistent financial capacity to comfortably repay your debt.

Based on my extensive experience in the financial landscape, navigating car loan applications can feel complex. However, with the right knowledge, you can approach the process with confidence and significantly increase your chances of approval. This comprehensive guide will break down everything you need to know about income requirements, ensuring you’re well-prepared for your next vehicle purchase.

Unlocking Your Dream Ride: A Deep Dive into Car Loan Income Requirements

Why Lenders Care So Much About Your Income

Lenders are in the business of assessing risk. When you apply for a car loan, they’re essentially betting on your ability to make regular payments over several years. Your income is the primary indicator of this ability. It tells them whether you have enough money coming in to cover your living expenses, existing debts, and the new car payment.

It’s not just about the gross number; lenders delve deeper. They want to see stability, consistency, and a comfortable margin that suggests you won’t struggle financially if unexpected expenses arise. Understanding this perspective is the first step toward a successful application.

The Core Pillars: Minimum Income and Debt-to-Income Ratio

When evaluating your financial health for a car loan, lenders primarily focus on two critical metrics: your minimum income and your debt-to-income (DTI) ratio. These two figures paint a clear picture of your repayment capacity.

Minimum Income: What’s the Magic Number?

There isn’t a universal "magic number" for minimum income that applies to all car loans. This figure can vary significantly depending on the lender, the type of loan, and even the vehicle’s price. However, based on common industry practices, many lenders look for a minimum gross monthly income ranging from $1,500 to $2,000.

This minimum threshold ensures that you have a foundational income level to manage basic living expenses alongside a car payment. Some lenders might have higher requirements for more expensive vehicles or for applicants with less-than-perfect credit. Always clarify these specifics with potential lenders.

Demystifying the Debt-to-Income (DTI) Ratio

The Debt-to-Income (DTI) ratio is arguably even more critical than your minimum income. It’s a percentage that compares how much money you earn each month to how much you spend on recurring debt payments. Lenders use this ratio to determine if you can realistically afford an additional car payment.

How to Calculate Your DTI:

- Sum Your Monthly Gross Income: This is your total income before taxes and deductions.

- Sum Your Monthly Debt Payments: Include rent/mortgage, credit card minimums, student loan payments, personal loan payments, and any other recurring debt. Do not include utilities, groceries, or entertainment.

- Divide Your Total Monthly Debt Payments by Your Total Monthly Gross Income: Multiply the result by 100 to get a percentage.

Example: If your gross monthly income is $4,000 and your total monthly debt payments are $1,200, your DTI is ($1,200 / $4,000) * 100 = 30%.

Why DTI Matters:

Lenders generally prefer a DTI ratio of 36% or lower. Some might approve loans for applicants with DTI up to 43%, especially if they have excellent credit scores or a substantial down payment. A lower DTI indicates less financial strain and a greater ability to manage new debt. A high DTI suggests you’re already stretched thin, making you a higher risk.

Pro tip from us: Before even speaking to a lender, calculate your DTI. This will give you a realistic understanding of your financial standing and help you identify areas for improvement. You can then strategize to reduce your existing debt or increase your income.

Beyond the Numbers: Other Factors Lenders Consider

While income and DTI are paramount, they aren’t the only pieces of the puzzle. Lenders take a holistic view of your financial profile. Several other factors play a significant role in determining your car loan eligibility and the terms you’re offered.

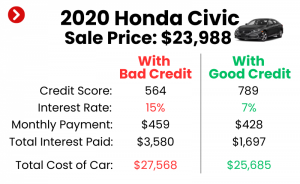

Your Credit Score: A Reflection of Financial Responsibility

Your credit score is a numerical representation of your creditworthiness. It summarizes your past borrowing and repayment behavior. A higher credit score (generally above 670 for good credit) signals to lenders that you are a responsible borrower. This can lead to better interest rates and more favorable loan terms.

Conversely, a lower credit score might result in higher interest rates or require a larger down payment to mitigate the lender’s risk. Lenders want to see a history of on-time payments and responsible credit utilization.

Employment Stability: A Sign of Consistent Income

Lenders prefer to see stable employment. This means having a consistent job for a reasonable period, typically at least six months to a year with the same employer. A long history of stable employment reassures them that your income stream is reliable and likely to continue throughout the loan term.

Frequent job changes or long gaps in employment can raise red flags, making it harder to secure a loan. If you’re self-employed, lenders will look for at least two years of consistent income history, often requiring tax returns to verify.

The Power of a Down Payment

Making a significant down payment can dramatically improve your car loan approval chances. A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the overall interest paid. It also shows the lender your commitment and reduces their risk.

Based on my experience, a down payment of 10-20% of the vehicle’s price is often recommended. For used cars, a higher percentage might be beneficial. This equity immediately puts you in a stronger position.

Loan Term and Vehicle Type: Impacting Affordability

The length of your loan (loan term) and the type of vehicle you choose directly impact your monthly payment. Longer loan terms mean lower monthly payments, but you’ll pay more in interest over the life of the loan. Shorter terms have higher monthly payments but save you money on interest.

Lenders assess whether the proposed monthly payment, combined with your existing debts, fits comfortably within your DTI ratio. A very expensive vehicle, even with a decent income, might push your DTI too high.

The Role of Co-signers or Co-applicants

If your income, credit score, or employment history isn’t strong enough on its own, a co-signer or co-applicant can be a viable option. A co-signer essentially guarantees the loan, promising to make payments if you default. This adds another layer of security for the lender.

However, choosing a co-signer is a serious decision. It impacts their credit score and financial standing, so both parties must understand the full implications. This should be considered a strategic move, not just a quick fix.

Types of Income Accepted for a Car Loan

Lenders accept various forms of income, but the documentation required will differ. Understanding what counts and how to verify it is crucial for a smooth application process.

W-2 Income (Salaried or Hourly Employees)

This is the most straightforward type of income for lenders to verify. If you’re a salaried or hourly employee, you’ll typically need to provide:

- Recent Pay Stubs: Usually, the last two to three months.

- W-2 Forms: For the past one or two years.

- Bank Statements: To show direct deposits.

Lenders appreciate the predictability and consistency of W-2 income. They can easily see your gross earnings and how often you’re paid.

Self-Employment Income

Self-employed individuals, including freelancers, independent contractors, and small business owners, often face a bit more scrutiny. Your income might fluctuate, so lenders need to see a pattern of stability. You’ll typically need:

- Tax Returns: For the past two to three years (e.g., Schedule C for sole proprietors). This is crucial for verifying consistent earnings.

- Bank Statements: Personal and/or business accounts to show income flow.

- Profit and Loss (P&L) Statements: For your business, if applicable.

Common mistakes to avoid are underestimating the documentation needed for self-employment. Ensure your financial records are meticulously organized and up-to-date.

Gig Economy Income

With the rise of the gig economy, income from platforms like Uber, Lyft, DoorDash, or Etsy is increasingly common. Lenders treat this similarly to self-employment income, but with potentially more emphasis on recent activity. You might need:

- Bank Statements: Showing regular deposits from gig platforms.

- 1099 Forms: For the past two years.

- Detailed Records: Of your earnings and expenses, as this income can be less predictable.

Consistency is key here. Lenders want to see a steady stream of income over several months, not just sporadic payments.

Other Income Sources

Several other income streams can be considered for a car loan, provided they are regular and verifiable:

- Social Security Benefits: Statement from the Social Security Administration.

- Pension or Retirement Income: Award letters or bank statements showing deposits.

- Disability Benefits: Award letters or bank statements.

- Alimony or Child Support: Court orders or separation agreements, along with bank statements showing consistent payments. Lenders cannot discriminate against these sources but may require proof of consistent receipt.

- Rental Income: Lease agreements and bank statements.

For any non-traditional income, the golden rule is verification. The more clearly you can demonstrate the regularity and amount of income, the better your chances.

How to Calculate Your Readiness for a Car Loan

Before you even fill out an application, it’s wise to conduct your own financial assessment. This proactive approach allows you to identify potential hurdles and address them, rather than being surprised by a lender’s decision.

Budgeting Before Applying

The first step is to create a detailed personal budget. List all your monthly income and all your fixed and variable expenses. This includes housing, utilities, groceries, transportation, insurance, and entertainment. Seeing where your money goes will reveal how much discretionary income you truly have for a car payment.

Pro tips from us: Be honest with yourself about your spending habits. A realistic budget is your best friend in this process.

Estimating Your Debt-to-Income (DTI) Ratio

As discussed earlier, calculate your current DTI ratio. Then, estimate what your DTI would look like with a potential car payment added to your existing debts. If the new DTI is above 36-43%, you might need to reconsider the car’s price, increase your down payment, or work on reducing other debts first.

You can use various online DTI calculators, but the manual calculation is simple enough to do yourself. This self-assessment is critical.

Using Online Calculators

Many reputable financial websites and even car dealerships offer online car loan calculators. These tools allow you to input the car price, down payment, interest rate, and loan term to estimate your monthly payment. This helps you determine what you can realistically afford.

Remember, these are estimates. Your actual interest rate will depend on your creditworthiness and the lender’s specific terms.

Strategies to Improve Your Car Loan Approval Chances

Even if your current financial situation isn’t ideal, there are actionable steps you can take to strengthen your car loan application.

Boost Your Credit Score

- Pay Bills on Time: Payment history is the biggest factor in your credit score.

- Reduce Credit Card Balances: Aim to keep your credit utilization (the amount of credit you’re using compared to your total available credit) below 30%.

- Check Your Credit Report: Obtain a free copy of your credit report from AnnualCreditReport.com (external link) and dispute any errors. This ensures accuracy.

Improving your credit takes time, so start well in advance of your car purchase.

Reduce Existing Debt

Lowering your existing debt, especially high-interest credit card debt, directly impacts your DTI ratio. Focus on paying down balances to free up more of your income. This shows lenders you’re managing your finances responsibly.

Consider making extra payments on smaller debts to eliminate them quickly, which can provide a psychological boost as well as financial relief.

Increase Your Down Payment

As mentioned, a larger down payment reduces the loan amount and the lender’s risk. If possible, save aggressively for a few months to accumulate more cash for your down payment. Even an extra few hundred dollars can make a difference.

This is a powerful way to show commitment and reduce your monthly burden.

Consider a Co-signer (Carefully)

If your credit or income is borderline, a co-signer with excellent credit and a stable income can significantly improve your chances. However, this is a serious commitment for both parties. Ensure both you and your co-signer fully understand the responsibilities involved.

Based on my experience, a co-signer should be a last resort and chosen only after open and honest communication about the risks.

Shop for Lenders and Get Pre-approved

Don’t just go with the first loan offer. Shop around and compare offers from various banks, credit unions, and online lenders. Each lender has different criteria and rates. Getting pre-approved from multiple lenders within a short timeframe (usually 14-45 days) counts as a single inquiry on your credit report, minimizing impact.

Pre-approval gives you a clear idea of what you can afford, turning you into a cash buyer at the dealership, which can strengthen your negotiating position.

Common Mistakes to Avoid When Applying for a Car Loan

Navigating the car loan process successfully also means sidestepping common pitfalls that can derail your application or cost you more money in the long run.

- Applying with Too Many Lenders at Once Outside the Shopping Window: While comparing offers is good, submitting multiple applications over an extended period can negatively impact your credit score. Group your applications within a short window.

- Underestimating Total Ownership Costs: Beyond the monthly payment, remember to budget for insurance, fuel, maintenance, and registration. Failing to account for these can lead to financial strain.

- Not Checking Your Credit Report Beforehand: Errors on your credit report are surprisingly common. Always review it and dispute inaccuracies before applying for a loan.

- Ignoring Pre-Approval: Walking into a dealership without pre-approval puts you at a disadvantage. You won’t know your true affordability, and you might be swayed by less favorable dealer financing.

- Overlooking the Fine Print: Always read the entire loan agreement. Understand the interest rate, fees, prepayment penalties (if any), and all terms and conditions before signing.

Pro Tips from an Expert

Leveraging years of financial insight, here are some final pieces of advice to empower your car buying journey:

- Conduct a Thorough Financial Health Check-up: Before you even think about a car, assess your overall financial picture. Are you saving enough? Do you have an emergency fund? A strong financial foundation makes any loan application smoother.

- Understand the "Why" Behind Every Number: Don’t just accept a rate or a term. Ask your lender to explain how they arrived at their decision. This empowers you with knowledge and helps you make informed choices.

- Negotiate Beyond the Price Tag: While the car’s price is important, also negotiate the interest rate, loan term, and any added fees. Every percentage point and every fee can add up significantly over the life of the loan.

- Prioritize Affordability Over Aspiration: It’s easy to fall in love with a car that’s just out of your budget. Always prioritize what you can comfortably afford over what you desire. Financial stress from a car payment can quickly diminish the joy of a new vehicle.

- Keep Records Meticulously: From your initial budget to your final loan documents, keep all financial records organized. This is invaluable for tax purposes, future financial planning, and any potential disputes.

Your Road Ahead: Drive with Confidence

Securing a car loan is a significant financial step, and understanding the income requirements is your first gear shift towards success. By focusing on a stable income, managing your debt-to-income ratio, building a strong credit history, and preparing all necessary documentation, you’ll present yourself as a reliable and creditworthy borrower.

Remember, preparation is key. Take the time to assess your financial health, improve where necessary, and gather all required information. With this comprehensive knowledge, you’re not just applying for a loan; you’re demonstrating your financial readiness to embark on your next automotive adventure. Drive smart, drive prepared, and enjoy the journey!

Further Reading:

- Understanding Your Credit Score Before a Loan Application (Internal Link Placeholder)

- The Ultimate Guide to Debt-to-Income Ratio (Internal Link Placeholder)