Unlocking Your Dream Ride: A Deep Dive into the Prime Rate and Its True Impact on Car Loans

Unlocking Your Dream Ride: A Deep Dive into the Prime Rate and Its True Impact on Car Loans Carloan.Guidemechanic.com

Dreaming of a new car? Whether it’s a sleek sedan, a rugged SUV, or an eco-friendly EV, securing the right car loan is often the first step to making that dream a reality. Many aspiring car owners hear terms like "prime rate," "interest rate," and "APR" thrown around, but few truly understand how they interact and, more importantly, how they directly impact the affordability of their vehicle.

As an expert blogger and someone who has navigated the complexities of auto finance for years, I understand the critical importance of knowledge in this process. This comprehensive guide will pull back the curtain on the prime rate for car loans, dissecting its role, revealing the true drivers of your interest rate, and equipping you with the strategies needed to secure the best possible financing deal. Our ultimate goal is to empower you to drive off the lot not just with a new car, but with confidence in your financial decision.

Unlocking Your Dream Ride: A Deep Dive into the Prime Rate and Its True Impact on Car Loans

What Exactly is the Prime Rate? Demystifying the Economic Benchmark

Before we explore its connection to car loans, let’s establish a clear understanding of the prime rate itself. The prime rate is essentially the interest rate that commercial banks charge their most creditworthy corporate customers on short-term loans. It’s not a static number; it fluctuates based on broader economic conditions and, most significantly, the actions of the Federal Reserve.

The Federal Funds Rate Connection:

The Federal Reserve, often referred to as "the Fed," sets a target range for the federal funds rate. This is the rate at which banks lend money to each other overnight to meet reserve requirements. When the Fed raises or lowers this target rate, it has a ripple effect throughout the entire financial system. Banks typically set their prime rate by adding a fixed spread, usually around 3 percentage points, to the upper end of the federal funds rate target.

For instance, if the Fed’s target for the federal funds rate is 5.00-5.25%, the prime rate will likely be around 8.25%. This direct linkage makes the prime rate a key indicator of the overall cost of borrowing in the economy.

The Prime Rate and Your Car Loan: An Indirect, Yet Powerful, Influence

It’s a common misconception that car loan interest rates are directly tied to the prime rate in the same way that, say, a Home Equity Line of Credit (HELOC) or some credit card rates are. In reality, most auto loans are structured with a fixed interest rate for the entire term, and this rate isn’t directly indexed to the prime rate.

However, stating that the prime rate has no impact would be misleading. Based on my experience in observing the auto finance market, the prime rate acts as a foundational benchmark. When the prime rate shifts, it signals a broader change in the cost of borrowing money for financial institutions themselves.

Lender’s Cost of Funds:

Banks and credit unions borrow money to lend it out. If their cost of borrowing (influenced by the prime rate and federal funds rate) goes up, they will naturally pass those increased costs on to consumers in the form of higher interest rates on products like car loans. Conversely, when the prime rate falls, lenders’ costs decrease, potentially leading to more favorable rates for borrowers.

So, while your individual car loan won’t fluctuate with the prime rate after you sign the contract (unless it’s a rare variable-rate auto loan, which is uncommon), the prevailing prime rate at the time you apply significantly shapes the general interest rate environment. This is why timing your car purchase can sometimes align with more (or less) favorable market conditions.

Beyond the Prime Rate: Key Factors That Truly Shape Your Car Loan Interest Rate

While the prime rate sets the macroeconomic stage, several other critical factors play a much more direct and personal role in determining the specific interest rate you’ll be offered on a car loan. Understanding these elements is paramount to becoming an informed borrower.

1. Your Credit Score: The Undisputed Champion of Car Loan Rates

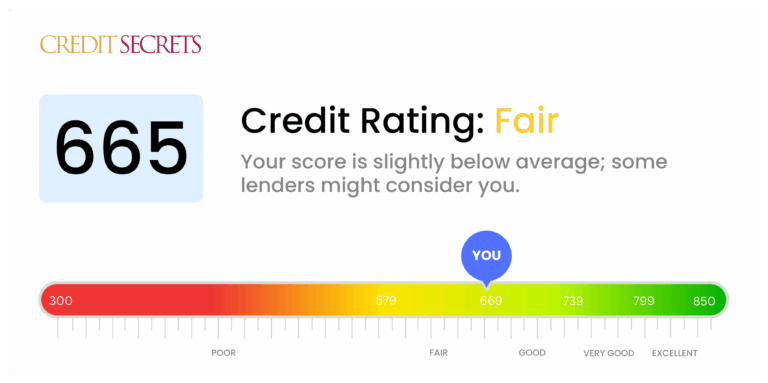

Without a doubt, your credit score is the single most influential factor in determining the interest rate you’ll receive. Lenders use your credit score as a quick and reliable indicator of your creditworthiness – essentially, how likely you are to repay your loan on time.

What Lenders Look For:

- Excellent Credit (780+ FICO): Borrowers in this range are considered low-risk and typically qualify for the lowest interest rates available, often referred to as "tier 1" rates.

- Good Credit (670-779 FICO): You’ll still qualify for competitive rates, though they might be slightly higher than those with excellent credit.

- Fair Credit (580-669 FICO): Rates will be notably higher, reflecting a moderate level of risk for lenders.

- Poor Credit (Below 580 FICO): Securing a loan can be challenging, and interest rates will be significantly elevated, sometimes in the double digits, due to the high perceived risk.

Pro tips from us: Before even stepping foot into a dealership or applying online, pull your credit report from all three major bureaus (Experian, Equifax, TransUnion). Check for errors and dispute any inaccuracies. A clean credit report can save you hundreds, if not thousands, over the life of your loan. For a deeper dive into improving your credit score, check out our guide on "Mastering Your Credit Score for Big Purchases."

2. Loan Term (Length): The Trade-Off Between Monthly Payment and Total Cost

The length of your loan, typically expressed in months (e.g., 36, 48, 60, 72, 84 months), has a dual impact on your finances.

- Shorter Terms: Often come with lower interest rates because the lender’s risk is reduced over a shorter period. Your monthly payments will be higher, but you’ll pay significantly less in total interest over the life of the loan.

- Longer Terms: While offering lower monthly payments, longer terms almost always result in higher interest rates. You’ll end up paying substantially more interest overall, and you run the risk of becoming "upside down" on your loan (owing more than the car is worth) for a longer period.

From years of observing the auto finance market, it’s easy to be swayed by a low monthly payment, but focusing solely on that can be a costly mistake. Always consider the total interest paid.

3. Loan-to-Value (LTV) Ratio / Down Payment: Skin in the Game

Your down payment directly impacts your loan-to-value (LTV) ratio, which is the amount you’re borrowing compared to the car’s value. A higher down payment means a lower LTV, which signals less risk to the lender.

Benefits of a Larger Down Payment:

- Lower Interest Rates: Lenders see less risk, so they’re willing to offer better rates.

- Reduced Loan Amount: You borrow less, meaning less interest accrues overall.

- Immediate Equity: You start with equity in your car, reducing the chance of being upside down.

- Lower Monthly Payments: A smaller loan amount naturally leads to lower monthly payments.

While 20% is often cited as an ideal down payment, even 10% or 15% can make a significant difference.

4. Vehicle Type & Age: Risk and Depreciation

The specific vehicle you choose can also influence your interest rate.

- New Cars: Generally qualify for lower interest rates due to their higher value, slower initial depreciation (compared to used cars), and manufacturer incentives.

- Used Cars: Tend to have slightly higher interest rates because they carry more perceived risk for lenders. They depreciate faster, have unknown maintenance histories, and may be harder to repossess and resell for full value if you default.

- Specific Models: Certain high-demand or luxury vehicles might have different financing options. Rarer or older cars might be harder to finance at competitive rates.

If you’re weighing the pros and cons of new versus used vehicles, our article "New vs. Used Car: Which is Right for Your Budget?" offers valuable insights.

5. Lender Type: Not All Lenders Are Created Equal

Where you get your loan can significantly impact the rate.

- Banks: Offer a wide range of loan products and competitive rates, especially for borrowers with good credit.

- Credit Unions: Often known for offering some of the most competitive rates, as they are not-for-profit organizations focused on their members. Membership requirements apply.

- Captive Finance Companies: These are financing arms of car manufacturers (e.g., Toyota Financial Services, Ford Credit). They often offer promotional rates (0% APR, low-interest deals) on new cars to boost sales, especially for well-qualified buyers.

- Online Lenders: Provide convenience and can sometimes offer competitive rates, especially if you have good credit. They’re excellent for pre-approval shopping.

Pro tips from us: Always shop around! Don’t just take the first offer from the dealership. Get quotes from at least three different lenders to compare.

6. Current Economic Conditions: The Broader Landscape

This is where the prime rate’s indirect influence comes full circle. The overall economic climate, including inflation rates, unemployment figures, and the Federal Reserve’s monetary policy, directly affects the interest rate environment.

- When the economy is strong and inflation is a concern, the Fed might raise the federal funds rate, leading to a higher prime rate and, consequently, higher car loan rates.

- Conversely, during economic slowdowns or recessions, the Fed might lower rates to stimulate borrowing and spending, which can translate to lower car loan rates.

Understanding these broader trends can help you anticipate rate movements, though timing the market perfectly is challenging. For official information on the Federal Funds Rate and its impact, you can always refer to the Federal Reserve’s official website.

Understanding Your Car Loan Offer: APR vs. Interest Rate

When comparing loan offers, you’ll encounter two key terms: the interest rate and the Annual Percentage Rate (APR). It’s crucial to understand the distinction.

- Interest Rate: This is the percentage charged by the lender for borrowing the principal amount. It represents the cost of borrowing before any additional fees are added.

- Annual Percentage Rate (APR): This is the true, total cost of borrowing money for a year. It includes the interest rate PLUS any additional fees charged by the lender (e.g., origination fees, administrative fees, sometimes even certain insurance premiums).

Why APR is the True Cost:

Always compare offers based on their APR, not just the interest rate. A loan with a slightly lower interest rate but high fees could end up being more expensive than a loan with a slightly higher interest rate but no fees. The APR gives you the most accurate picture of what you’ll actually pay.

Common mistakes to avoid are focusing solely on the advertised interest rate without asking about all associated fees. Always request the full APR.

Fixed vs. Variable Rate Car Loans: Which is Right for You?

Most car loans are fixed-rate loans. This means your interest rate, and therefore your monthly payment, remains the same for the entire duration of the loan. This predictability is highly valued by borrowers, as it makes budgeting straightforward.

Variable-rate loans are far less common for car purchases. With a variable rate, your interest rate can fluctuate over time, typically tied to an index like the prime rate. If the index goes up, your interest rate and monthly payment could increase, and vice versa.

Based on my experience, for the vast majority of car buyers, a fixed-rate loan is the safer and more sensible option. It removes the uncertainty of fluctuating payments and allows for better financial planning. Variable rates introduce a level of risk that few car buyers are comfortable with, especially given the typically short to medium terms of auto loans.

Strategies to Secure the Best Car Loan Rate

Now that you understand the factors at play, here are actionable strategies to ensure you get the most favorable terms for your next car loan.

- Check Your Credit Report and Score: As discussed, this is foundational. Get copies from all three bureaus and dispute any errors. Knowing your score allows you to gauge what rates you might qualify for.

- Get Pre-Approved: Before you even set foot on a car lot, get pre-approved for a loan from your bank, credit union, or an online lender. This gives you a concrete interest rate offer and empowers you to negotiate with the dealership’s finance department. It also sets a budget, preventing you from overspending.

- Shop Around Aggressively for Lenders: Don’t settle for the first offer. Apply to several different lenders within a short window (typically 14-45 days, depending on the credit scoring model) to minimize the impact on your credit score. Each application within this window will count as a single inquiry.

- Negotiate the Price of the Car First: Keep the car price negotiation separate from the loan negotiation. Get the best possible price on the vehicle itself before discussing financing. This prevents the dealership from "packing" the loan with extra costs or inflating the car price while giving you a seemingly good interest rate.

- Make a Substantial Down Payment: The more you put down, the less you borrow, and the lower your LTV will be. This reduces the lender’s risk and can lead to better interest rates and lower monthly payments.

- Consider a Co-signer (Carefully): If your credit isn’t stellar, a co-signer with excellent credit can help you qualify for a better rate. However, understand that the co-signer is equally responsible for the loan, and any missed payments will impact their credit as well.

- Choose a Shorter Loan Term: If your budget allows, opt for the shortest loan term you can comfortably afford. You’ll pay less interest overall, even if the monthly payment is higher.

- Pro tips from us: Don’t just focus on the monthly payment. Dealerships often try to steer conversations toward low monthly payments to make a car seem more affordable. Always ask for the total cost of the loan, including interest, and the full APR.

Common Mistakes to Avoid When Getting a Car Loan

Even informed buyers can fall into common traps. Be vigilant and avoid these pitfalls:

- Not Shopping for Rates: This is the biggest mistake. Assuming the dealership’s finance offer is the best or only option will almost certainly cost you money.

- Focusing Only on Monthly Payment: As mentioned, a low monthly payment can mask a long loan term and a high total interest cost.

- Ignoring the Fine Print: Read every line of your loan agreement. Understand all fees, prepayment penalties (rare for auto loans but possible), and specific terms.

- Extending the Loan Term Too Much: While it lowers your monthly payment, an 84-month loan means you’re paying interest for seven years and are likely to be upside down for a significant portion of that time.

- Buying More Car Than You Can Afford: Don’t let the excitement of a new vehicle lead you to commit to payments that strain your budget. Stick to your pre-determined budget.

- Rolling Over Negative Equity: If you’re trading in a car that you owe more on than it’s worth (negative equity), avoid rolling that balance into your new loan. It inflates your new loan, increases your new interest payment, and puts you even further upside down.

When to Consider Refinancing Your Car Loan

Securing a car loan isn’t a "set it and forget it" situation. There are times when refinancing could significantly improve your financial standing.

- Lower Interest Rates Are Available: If general market interest rates (influenced by the prime rate) have dropped significantly since you took out your original loan.

- Your Credit Score Has Improved: If you’ve diligently paid your bills and improved your credit score since you bought the car, you might now qualify for much better rates.

- Change in Financial Situation: Perhaps you got a raise, paid off other debts, or reduced your debt-to-income ratio, making you a more attractive borrower.

- Shortening/Lengthening the Term: You might want to refinance to a shorter term to pay off the loan faster and save on interest, or, in rare cases, extend the term for a lower monthly payment during a financial hardship (though this will increase total interest).

What we’ve seen in the industry is that refinancing can often save hundreds or even thousands of dollars over the life of a loan, so it’s always worth exploring if your circumstances have changed.

The Future of Car Loan Rates: What to Watch For

While predicting the future is impossible, staying informed about key economic indicators can give you a general sense of where car loan rates might be headed.

- Federal Reserve Policy: Keep an eye on the Federal Reserve’s announcements regarding the federal funds rate. Any changes here will directly impact the prime rate and, subsequently, the broader interest rate environment for car loans.

- Inflation Trends: High inflation often prompts the Fed to raise rates to cool down the economy, which can push car loan rates higher.

- Economic Growth/Recession Indicators: A strong economy might see stable or gradually rising rates, while a looming recession could lead to rate cuts by the Fed.

Conclusion: Drive Smart, Not Just Fast

The journey to owning a car is exciting, but the financial road can be bumpy if you’re not prepared. While the prime rate for car loans isn’t a direct, real-time determinant of your specific auto loan rate, it plays a crucial role in setting the overall economic backdrop. However, it’s your personal financial health – primarily your credit score, down payment, and chosen loan term – that will truly dictate the interest rate you receive.

By understanding these dynamics, shopping around for the best terms, and avoiding common pitfalls, you position yourself as a powerful, informed consumer. Don’t just settle for the first offer; empower yourself with knowledge and negotiation skills. Drive smart, secure the best possible financing, and enjoy your new ride with true peace of mind. Your wallet will thank you.