Unlocking Your Dream Ride: The Definitive Guide to Andigo Car Loans

Unlocking Your Dream Ride: The Definitive Guide to Andigo Car Loans Carloan.Guidemechanic.com

Buying a car is more than just a transaction; it’s an investment in freedom, convenience, and often, a significant life upgrade. For many, securing the right financing is the crucial first step on this exciting journey. In the vast landscape of auto lenders, Andigo Car Loans have emerged as a compelling option, known for their digital-first approach and connection to a network of credit unions.

As an expert blogger and professional SEO content writer who has navigated countless financial products, I understand the importance of making an informed decision. This comprehensive guide will peel back every layer of the Andigo Car Loan experience, from initial application to repayment, ensuring you have all the knowledge to drive away with confidence. We’ll explore what makes Andigo stand out, who it’s best for, and how you can maximize your chances of securing the best possible deal.

Unlocking Your Dream Ride: The Definitive Guide to Andigo Car Loans

What Exactly is an Andigo Car Loan?

Before diving into the specifics, let’s clarify what we mean by an Andigo Car Loan. Andigo is not a traditional bank or a single credit union. Instead, it’s a digital lending platform that partners with a network of credit unions across the United States. This unique structure allows Andigo to combine the technological efficiency of an online lender with the member-centric philosophy and often competitive rates offered by credit unions.

When you apply for an auto loan through Andigo, you’re essentially accessing the collective power of numerous financial institutions committed to serving their members. This model can translate into a more personalized experience and potentially better terms than you might find with larger, more impersonal lenders. It’s about leveraging technology to connect borrowers with community-focused financial solutions.

Why Andigo Stands Out for Your Auto Financing Needs

Based on my experience analyzing various lending platforms, Andigo offers several distinct advantages that make it a strong contender for your next vehicle purchase. Their approach is designed to simplify what can often be a complex and stressful process.

Firstly, the digital convenience is a major draw. In today’s fast-paced world, being able to apply for a loan, upload documents, and track your application status all from your computer or smartphone is invaluable. This eliminates the need for multiple in-person visits or lengthy phone calls, streamlining the entire experience.

Secondly, the credit union advantage cannot be overstated. Credit unions are non-profit organizations, meaning their primary goal is to serve their members, not shareholders. This often translates into lower interest rates, fewer fees, and more flexible terms compared to traditional banks. Andigo acts as a bridge, connecting you directly to these member-focused benefits.

Finally, Andigo is committed to providing competitive rates and flexible terms. They understand that every borrower’s situation is unique, and they strive to offer loan options that can be tailored to individual financial circumstances. Whether you’re buying new, used, or looking to refinance, their network aims to provide solutions that fit your budget and lifestyle.

Navigating the Andigo Car Loan Application Process: A Step-by-Step Guide

Securing an auto loan might seem daunting, but Andigo’s process is designed to be straightforward. Understanding each step can significantly ease any anxiety and help you prepare effectively. From pre-qualification to final approval, knowing what to expect is half the battle.

The journey typically begins with a pre-qualification. This initial step allows you to get an estimate of your potential loan terms without impacting your credit score. You’ll provide some basic financial information, and Andigo will give you an idea of what you might qualify for. This is a fantastic way to gauge your borrowing power early on.

Following pre-qualification, the next crucial step is pre-approval. This involves a more detailed application and a hard credit pull, which will temporarily affect your credit score. However, a pre-approval letter is incredibly powerful, as it tells dealerships you’re a serious buyer with financing already secured. This puts you in a much stronger negotiating position.

Essential Documents for Your Application

Gathering the right documents upfront can significantly expedite your application. Based on my experience, being prepared is key to a smooth process. Missing paperwork is a common reason for delays.

You’ll typically need proof of identity, such as a driver’s license or state ID. Lenders also require verification of income, which can include recent pay stubs, W-2 forms, or tax returns if you’re self-employed. These documents help confirm your ability to repay the loan.

Additionally, you’ll need residency verification, usually a utility bill or lease agreement. If you have a specific vehicle in mind, be prepared to provide details about the car, including its VIN (Vehicle Identification Number) and mileage. Having these readily available will make your online application seamless.

Completing the Online Application

The heart of the Andigo experience is its intuitive online application. This digital portal guides you through each section, ensuring you provide all necessary information. It’s designed to be user-friendly, minimizing confusion and errors.

You’ll input personal details, employment history, income information, and your desired loan amount and term. The system will prompt you to upload any required documents securely. Pro tips from us: Double-check all entries for accuracy before submitting. Even small errors can cause processing delays.

Once submitted, you’ll receive updates on your application status directly through the platform or via email. This transparency is a major benefit, keeping you informed every step of the way. You won’t be left wondering about the progress of your loan.

What Happens After You Apply?

After submitting your application, Andigo’s network of credit unions will review your information. This involves verifying your income, employment, and credit history. They’ll assess your overall financial health to determine your eligibility and the best loan terms.

If approved, you’ll receive a loan offer outlining the interest rate, term, and monthly payments. You’ll then have the opportunity to review and accept the offer. Common mistakes to avoid are rushing this step; always read the fine print and ensure you understand all the terms before signing.

Once you accept, the funds will be disbursed, either directly to you (if you’re buying from a private seller) or to the dealership. The entire process, from application to funding, is often much quicker than with traditional lenders, thanks to Andigo’s digital efficiency.

Andigo Car Loan Eligibility: Who Can Get Approved?

Understanding the eligibility criteria is crucial for anyone considering an Andigo Car Loan. While specific requirements can vary slightly between credit unions in their network, general guidelines apply. Meeting these criteria significantly boosts your chances of approval.

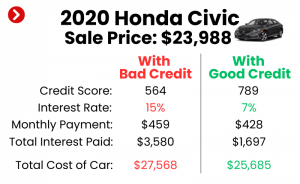

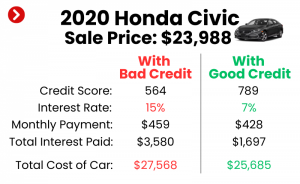

Firstly, your credit score plays a pivotal role. Lenders use your credit score as a primary indicator of your financial responsibility. A higher credit score generally translates into lower interest rates and more favorable terms. While Andigo aims to serve a broad range of borrowers, a good to excellent credit score will always be an advantage.

Your income and employment stability are also critical. Lenders want to ensure you have a steady source of income to make your monthly payments. They’ll look at your employment history, current salary, and potentially other sources of income. Consistent employment over a period demonstrates reliability.

Finally, your debt-to-income (DTI) ratio is an important factor. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates you have more disposable income to cover your new car loan payment, making you a less risky borrower. Most lenders prefer a DTI ratio below 43%.

Pro Tips for Improving Your Eligibility

If you’re worried about your eligibility, there are proactive steps you can take. Based on my experience, even small improvements can make a big difference. These strategies can not only help you get approved but also secure better terms.

Start by checking your credit report for any errors and disputing them. You can obtain a free copy annually from each of the three major credit bureaus. Paying down existing debts, especially credit card balances, can quickly improve your credit utilization ratio and boost your score. Making all your payments on time, every time, is also fundamental.

Consider making a larger down payment. A substantial down payment reduces the amount you need to borrow, making your loan more appealing to lenders and potentially lowering your monthly payments. It also demonstrates your commitment to the purchase.

If your credit isn’t stellar, exploring a co-signer option might be beneficial. A co-signer with good credit can strengthen your application, as they share responsibility for the loan. However, ensure both parties understand the full implications of co-signing.

Andigo Car Loan Interest Rates and Terms: The Financial Details

Understanding the financial specifics of your loan is paramount. The interest rate and loan term directly impact your monthly payments and the total cost of your vehicle. Andigo, leveraging its credit union network, aims to offer competitive options.

The interest rate you receive is influenced by several factors: your credit score, the loan term, the vehicle’s age and mileage, and current market conditions. Generally, borrowers with excellent credit scores qualify for the lowest rates. A shorter loan term often comes with a lower interest rate, as the lender’s risk is reduced.

It’s crucial to distinguish between the stated interest rate and the Annual Percentage Rate (APR). The APR includes the interest rate plus any additional fees associated with the loan, giving you a more accurate picture of the total cost of borrowing. Always compare APRs when shopping for loans to get the true cost.

Choosing the Right Loan Term

The loan term refers to the length of time you have to repay the loan, typically ranging from 36 to 84 months. A shorter term means higher monthly payments but less interest paid over the life of the loan. Conversely, a longer term offers lower monthly payments but results in paying more in total interest.

Pro tips from us: While lower monthly payments from a longer term might seem attractive, consider the total cost. If possible, opt for the shortest term you can comfortably afford. This saves you money in the long run and helps you build equity in your vehicle faster.

Based on my experience, striking a balance between affordable monthly payments and minimizing total interest paid is key. Use Andigo’s loan calculators to experiment with different terms and see how they impact your financial outlay. Don’t stretch your budget too thin, but also avoid unnecessarily prolonging your debt.

Beyond the Standard: Special Considerations with Andigo

Andigo’s network often caters to a variety of needs, extending beyond just new car purchases. Exploring these specialized options can broaden your financing possibilities. Understanding these nuances can save you money or provide much-needed flexibility.

Refinancing an existing car loan is a popular option that Andigo’s partners often facilitate. If your credit score has improved since you first financed your car, or if interest rates have dropped, refinancing could significantly lower your monthly payments or reduce the total interest you pay. It’s essentially replacing your old loan with a new one that has more favorable terms. For more detailed insights, you might want to learn more about Understanding Auto Loan Refinancing on our blog.

Andigo’s network also provides financing for both new and used cars. The terms and rates might differ slightly, with used car loans sometimes carrying slightly higher rates due to perceived higher risk. However, their digital platform simplifies the process for either type of vehicle. Be prepared to provide details about the specific used car, including its mileage and condition, as this affects the loan amount and terms.

While Andigo, like most reputable lenders, prefers borrowers with good credit, some credit unions in their network might offer solutions for individuals with less-than-perfect credit. These loans might come with higher interest rates or require a larger down payment, but they can be a viable path to vehicle ownership. It’s always worth exploring your options and seeing what you qualify for.

Maximizing Your Chances of Approval: Expert Strategies

Getting approved for an Andigo Car Loan isn’t just about meeting the minimum requirements; it’s about presenting yourself as the most attractive borrower possible. Drawing from my expertise, here are some strategies to significantly boost your approval odds and secure the best terms.

Firstly, diligently improve your credit score. This is the single most impactful action you can take. Pay all your bills on time, keep credit card balances low, and avoid opening new credit accounts just before applying for a car loan. A higher score directly translates to lower perceived risk for lenders. To dive deeper into this, check out our guide on Improving Your Credit Score for Auto Loans.

Secondly, understand the importance of a down payment. While some loans offer 100% financing, a down payment reduces the loan amount and shows the lender you have a financial stake in the vehicle. This can significantly increase your approval chances and potentially lower your interest rate. Aim for at least 10-20% of the car’s value if possible.

Finally, actively work on reducing your debt-to-income ratio. Before applying, try to pay off small debts or reduce recurring expenses. This demonstrates to lenders that you have ample capacity to manage a new car payment comfortably. A healthy DTI ratio signals financial responsibility and reduces lender apprehension.

Managing Your Andigo Car Loan: Post-Approval Best Practices

Getting approved for your Andigo Car Loan is a fantastic achievement, but the journey doesn’t end there. Effective loan management is crucial to maintain good financial health and ensure a smooth repayment process. Overlooking these post-approval best practices can lead to unnecessary stress or even financial penalties.

Your first step should be to thoroughly understand your payment schedule. Note your due date, the exact amount due, and the accepted payment methods. Many lenders, including those in Andigo’s network, offer auto-pay options, which can help you avoid late fees and maintain a perfect payment history. Setting up reminders is also a smart move.

Consider making extra payments whenever possible. Even small additional payments can significantly reduce the total interest you pay over the life of the loan and help you pay it off sooner. Directing extra funds towards the principal balance accelerates your equity building. This financial discipline can save you hundreds, if not thousands, in the long run.

Common mistakes to avoid are ignoring communications from your lender or letting a payment slide. If you anticipate financial hardship, contact your lender immediately. Many credit unions are willing to work with borrowers facing temporary difficulties, potentially offering deferment options or modified payment plans. Proactive communication is always better than reactive damage control.

Andigo Car Loan vs. Other Lenders: Making an Informed Choice

The auto loan market is competitive, with various players vying for your business. Understanding how Andigo Car Loans stack up against other options can help you make the most informed decision. Each type of lender has its own unique advantages and disadvantages.

Traditional banks often offer a wide range of financial products, but their car loan rates might not always be the most competitive, especially for those with less-than-perfect credit. Their application processes can sometimes be more rigid and time-consuming. However, established relationships with banks can sometimes offer convenience.

Captive lenders, such as those associated with specific car manufacturers (e.g., Toyota Financial Services, Ford Credit), often provide attractive promotional rates for new cars. These deals can be enticing, but they are typically limited to specific models and might not be available for used cars or refinancing. Their primary goal is to sell cars, not just loans.

Online-only lenders offer convenience and often quick approvals, similar to Andigo. However, they might lack the personalized service or the member-focused benefits that come with credit union affiliations. Andigo effectively blends the best of both worlds: digital efficiency with the inherent advantages of a credit union network.

Andigo’s unique position, leveraging the credit union model through a modern digital platform, often results in more competitive rates, lower fees, and a more personalized customer experience. This combination provides a strong value proposition for many car buyers seeking a fair and transparent financing solution.

Frequently Asked Questions About Andigo Car Loans

As an expert, I know that questions inevitably arise when dealing with financial products. Here are answers to some of the most common inquiries about Andigo Car Loans, providing clarity and confidence.

Can I get an Andigo loan with bad credit?

While Andigo’s network of credit unions generally looks for good credit, some partners may offer solutions for individuals with lower credit scores. These loans might come with higher interest rates or require a larger down payment. It’s always best to apply and see what options are available to you, as eligibility can vary.

How long does the approval process take?

One of the major benefits of Andigo’s digital platform is its efficiency. Many applicants receive a decision within minutes or hours after submitting a complete application. Final funding typically occurs within a few business days once all documents are verified and the offer is accepted.

What if I want to pay off my loan early?

Most auto loans offered through Andigo’s credit union network do not have prepayment penalties. This means you can pay off your loan ahead of schedule without incurring extra fees, saving you money on interest. Always confirm this detail in your loan agreement, but it’s a common feature of credit union loans.

Do they offer co-signer options?

Yes, if your credit history or income makes it difficult to qualify on your own, a co-signer with good credit can often strengthen your application. This can help you secure approval and potentially a better interest rate. Remember, a co-signer shares equal responsibility for the loan.

Drive Your Dreams: The Andigo Car Loan Advantage

Embarking on the journey to car ownership is exciting, and securing the right financing is a pivotal step. Andigo Car Loans, with their innovative digital platform and strong credit union partnerships, offer a compelling path to achieving your automotive dreams. They combine the ease of online applications with the community-focused benefits of credit unions, often translating into competitive rates and flexible terms.

Throughout this comprehensive guide, we’ve explored the intricacies of Andigo’s offerings, from their streamlined application process and eligibility criteria to the crucial financial details of interest rates and loan terms. We’ve also provided expert strategies to maximize your approval chances and best practices for managing your loan post-approval.

Based on my experience, choosing Andigo means opting for a modern, efficient, and potentially more borrower-friendly financing experience. By preparing thoroughly, understanding the process, and leveraging the tips provided, you can confidently navigate your path to a new vehicle. So, if you’re ready to hit the road in your dream car, explore what an Andigo Car Loan can do for you. Your journey to smart auto financing starts here.