Unlocking Your Dream Ride: The Definitive Guide to Credit Scores for Capital One Car Loans

Unlocking Your Dream Ride: The Definitive Guide to Credit Scores for Capital One Car Loans Carloan.Guidemechanic.com

Securing a car loan is a significant financial step, and for many, Capital One stands out as a preferred lender. Their reputation for working with a broad spectrum of credit profiles makes them an attractive option, but understanding the role your credit score for a Capital One car loan plays is absolutely crucial. It’s not just about getting approved; it’s about securing the best possible terms that save you thousands over the life of your loan.

This comprehensive guide will demystify the entire process, diving deep into what Capital One looks for, how your credit score is evaluated, and actionable strategies to put you in the driver’s seat of your financial future. We’ll go beyond the surface, offering expert insights and practical advice to help you navigate the journey to your next vehicle with confidence.

Unlocking Your Dream Ride: The Definitive Guide to Credit Scores for Capital One Car Loans

Capital One Car Loans: A Trusted Path to Vehicle Ownership

Capital One has established itself as a major player in the auto lending landscape, known for its user-friendly pre-qualification process and willingness to consider applicants across various credit tiers. They aim to simplify car buying, partnering with thousands of dealerships nationwide. This broad accessibility is precisely why so many prospective car buyers turn to them.

Their approach often involves allowing customers to get pre-approved before even stepping foot in a dealership. This empowers buyers with real loan terms, including interest rates and maximum loan amounts, transforming what can often be a stressful negotiation into a more transparent experience. Understanding their lending philosophy is the first step toward a successful application.

The Cornerstone of Approval: Your Credit Score Explained

At the heart of any loan application, especially for a significant purchase like a car, lies your credit score. This three-digit number is a snapshot of your financial reliability, a numerical representation of your past borrowing behavior. Lenders, including Capital One, use it to assess the risk associated with lending you money. A higher score generally indicates lower risk.

While various scoring models exist, FICO and VantageScore are the most widely used. Both assess similar factors, but their calculations can yield slightly different numbers. Regardless of the model, the underlying principles remain consistent: demonstrate responsible credit management, and your score will reflect it positively.

How Your Credit Score is Calculated: A Deep Dive

Understanding the components that build your credit score is paramount to improving it. It’s not a mystery; it’s a science based on your financial history. Each element contributes a specific weight to your overall score, making some factors more impactful than others.

-

Payment History (Approx. 35%): This is the single most important factor. Consistently paying your bills on time, every time, is crucial. Late payments, especially those exceeding 30 days, can significantly damage your score and remain on your report for up to seven years.

- Based on my experience, even one missed payment can have a ripple effect, making lenders view you with more caution. Establishing a consistent track record of on-time payments is the quickest way to build or rebuild trust with creditors. Setting up automatic payments for all your bills can be a simple yet effective strategy here.

-

Amounts Owed / Credit Utilization (Approx. 30%): This refers to the amount of credit you’re using compared to your total available credit. For example, if you have a credit card with a $10,000 limit and a $3,000 balance, your utilization is 30%. Experts generally recommend keeping your credit utilization below 30% across all your accounts.

- High utilization suggests you might be over-reliant on credit, which lenders perceive as a higher risk. Even if you pay your bills in full each month, a high reported balance on your credit report can temporarily depress your score. It’s wise to keep an eye on these ratios.

-

Length of Credit History (Approx. 15%): The longer your credit accounts have been open and in good standing, the better. This demonstrates a sustained ability to manage credit responsibly over time. Newer accounts can slightly lower your average account age, which might have a minor, temporary impact.

- Avoid closing old, paid-off accounts, especially if they have a long history and no annual fees. These accounts contribute positively to the average age of your credit, which is a key stability indicator for lenders like Capital One. Consistency shows reliability.

-

New Credit (Approx. 10%): Opening multiple new credit accounts in a short period can be a red flag for lenders. Each application results in a "hard inquiry" on your credit report, which can slightly lower your score for a short time. Too many inquiries can suggest you’re desperate for credit.

- Common mistakes to avoid are applying for every store credit card offer just to get a discount. Be strategic about when and why you apply for new credit, especially in the months leading up to a major loan application. Space out your applications.

-

Credit Mix (Approx. 10%): Having a healthy mix of different types of credit, such as revolving credit (credit cards) and installment loans (mortgages, auto loans, student loans), shows you can manage various forms of debt. However, don’t open accounts just to diversify; let it happen naturally as your financial needs evolve.

- This factor is less impactful than payment history or utilization, but it still contributes to a well-rounded credit profile. Demonstrating responsible management across different credit types indicates a sophisticated approach to personal finance.

What Credit Score Does Capital One Look For? The Core Question

This is often the million-dollar question for prospective car buyers. The truth is, there isn’t one single "magic number" that guarantees approval for a Capital One car loan. Instead, Capital One, like many major lenders, employs a tiered system, evaluating applicants across a spectrum of credit profiles. They are known for being more inclusive than some traditional banks, but your score will directly influence your approval chances and, crucially, your interest rate.

Here’s a general breakdown of what you might expect, based on common credit score ranges:

-

Excellent Credit (780+ FICO / 720+ VantageScore): With excellent credit, you’re in the prime position. You’ll likely qualify for the lowest available interest rates, offering significant savings over the loan term. Capital One views you as a very low-risk borrower, making approval highly probable. You’ll have the most flexibility in loan terms and vehicle choices.

-

Good Credit (670-779 FICO / 661-720 VantageScore): This is considered a strong credit score, and you’ll still qualify for very competitive interest rates with Capital One. While they might not be the absolute lowest, they will be attractive. Approval is highly likely, and you’ll have a good range of loan options. Most car buyers fall into this category.

-

Average/Fair Credit (580-669 FICO / 601-660 VantageScore): This is where Capital One truly shines for many applicants. They are often willing to work with individuals in this range, which some other lenders might consider subprime. You can expect higher interest rates than those with good or excellent credit, reflecting the increased risk. Approval is possible, but terms might be less favorable, potentially requiring a larger down payment or a newer, less risky vehicle.

-

Subprime/Poor Credit (Below 580 FICO / Below 600 VantageScore): Even with a lower credit score, Capital One is one of the few major lenders that might still offer you a car loan. However, the terms will be significantly less attractive. Expect much higher interest rates, potentially a requirement for a substantial down payment, and possibly a need for a co-signer. The goal here is often to get approved and then rebuild credit for future refinancing opportunities.

It’s vital to remember that these are general ranges. Capital One looks at your entire financial picture, not just your score in isolation. Your income, debt-to-income ratio, and other factors play a significant role.

Beyond the Score: Other Factors Capital One Considers

While your credit score is a powerful indicator, it’s just one piece of the puzzle. Capital One takes a holistic view of your financial health to make a lending decision. Ignoring these other elements could lead to unexpected denials, even with a decent score.

-

Income and Debt-to-Income (DTI) Ratio: Capital One wants to ensure you have the financial capacity to comfortably afford your monthly car payments. They’ll look at your gross monthly income and compare it to your existing debt obligations (rent/mortgage, credit card payments, student loans, etc.). A low DTI ratio (typically below 40-45%) indicates you have sufficient disposable income.

- Pro tips from us: Calculate your DTI before applying. If it’s high, consider paying down some existing debt or looking for a more affordable vehicle to lower the potential loan amount. This proactive step can significantly strengthen your application.

-

Employment Stability: A steady job history demonstrates a reliable source of income. Lenders prefer applicants who have been consistently employed for at least a year or two, ideally in the same field. Frequent job changes might raise concerns about income consistency.

-

Down Payment Amount: A larger down payment reduces the amount you need to borrow, thereby lowering the lender’s risk. It also shows your commitment to the purchase. Capital One may require a minimum down payment, especially for applicants with lower credit scores.

- Based on my experience, even a modest down payment of 10-20% can improve your chances of approval and secure a better interest rate, regardless of your credit score. It shows financial discipline.

-

Loan-to-Value (LTV) Ratio of the Vehicle: This compares the amount you’re borrowing to the car’s actual value. If you borrow more than the car is worth (e.g., rolling negative equity from a trade-in), the LTV ratio increases the lender’s risk.

-

Vehicle Age and Mileage: Capital One, like other lenders, has limits on the age and mileage of vehicles they will finance, especially for used cars. Older, higher-mileage vehicles are considered higher risk due to potential mechanical issues and depreciation.

-

Existing Capital One Relationships: If you already have a checking account, credit card, or another loan with Capital One and have a positive payment history, this can sometimes work in your favor. It demonstrates a pre-existing, trusted relationship.

-

Recent Credit Inquiries: While a single hard inquiry for an auto loan has minimal impact, multiple inquiries within a short period (especially for different types of credit) can raise red flags. Capital One typically groups multiple auto loan inquiries within a 14-45 day window as a single inquiry, recognizing you’re rate shopping.

Pre-Qualification vs. Full Application with Capital One: Know the Difference

One of Capital One’s most consumer-friendly features is its robust pre-qualification process. Understanding the distinction between pre-qualification and a full application is vital for smart car shopping.

Pre-Qualification: Your Smart First Step

Capital One’s pre-qualification tool allows you to see if you’re likely to be approved for a car loan and, if so, what your estimated terms (interest rate, loan amount, monthly payment) would be. The key benefits are:

- Soft Credit Pull: This is a "soft inquiry" on your credit report, which does NOT impact your credit score. You can check your eligibility without any risk to your score.

- No Obligation: Pre-qualification doesn’t commit you to anything. It simply gives you an idea of what to expect.

- Empowerment at the Dealership: Walking into a dealership with a pre-approval in hand gives you significant negotiating power. You know your budget and interest rate beforehand, allowing you to focus on the car’s price, not just the monthly payment.

Pro Tip: Always pre-qualify first! This simple step provides invaluable information and protects your credit score from unnecessary hard inquiries. It sets the stage for a much smoother car-buying experience.

Full Application: The Commitment Phase

Once you find the car you want and are ready to finalize the purchase, you’ll proceed with a full application. This involves:

- Hard Credit Pull: A "hard inquiry" will be made on your credit report. This can temporarily lower your score by a few points for a short period, but the impact is usually minor.

- Detailed Information: You’ll provide more detailed financial information, including exact income verification, employment history, and possibly bank statements.

- Final Loan Offer: Based on the hard pull and verified information, Capital One will issue a final loan offer, which may be slightly different from your pre-qualification due to the full underwriting process.

Strategies to Improve Your Credit Score Before Applying

If you know you’ll be seeking a Capital One car loan in the near future, taking proactive steps to boost your credit score can yield significant rewards in the form of lower interest rates and better terms. Even a small improvement can save you hundreds, if not thousands, of dollars.

- Pay Bills On Time, Every Time: Reiterate this golden rule. Set up reminders, automate payments, or use a calendar. Consistency is key. Even utility bills, if reported to credit bureaus, can contribute.

- Reduce Credit Card Balances / Lower Utilization: Focus on paying down your credit card debt, especially those with high balances. Aim to keep your utilization below 30%, ideally below 10%, in the months leading up to your application.

- Check Your Credit Reports for Errors: Obtain free copies of your credit reports from AnnualCreditReport.com. Review them meticulously for any inaccuracies, such as incorrect late payments or accounts you don’t recognize. Dispute any errors immediately, as they can unfairly drag down your score.

- Avoid Opening New Credit Accounts: Resist the temptation to open new credit cards or take out other loans in the months before applying for your car loan. New accounts result in hard inquiries and can lower your average credit age, both of which can negatively impact your score.

- Keep Old Accounts Open (Unless They Have High Fees): As discussed, older accounts contribute to a longer credit history. If an old credit card is paid off and has no annual fee, consider keeping it open, even if you rarely use it.

- Become an Authorized User (Carefully): If a trusted family member with excellent credit adds you as an authorized user to their well-managed credit card, their positive payment history could reflect on your report. However, ensure they are responsible; their mistakes could also impact you.

Based on my experience, credit score improvement isn’t an overnight process. Aim for at least 3-6 months of consistent effort to see meaningful changes. Small, disciplined habits over time yield the best results.

What if Your Credit Isn’t Perfect? Capital One for Bad Credit

One of Capital One’s strengths is its willingness to consider applicants with less-than-perfect credit. They understand that life happens, and a low credit score doesn’t always reflect current financial stability. If your credit score falls into the average or subprime category, don’t despair, but adjust your expectations.

With lower credit scores, you should anticipate:

- Higher Interest Rates: This is the most significant consequence. Lenders charge more to offset the increased risk. While these rates will be higher, they might still be more favorable than predatory "buy here, pay here" lots.

- Larger Down Payment Requirements: Capital One may require a more substantial down payment to reduce their lending risk. This shows your commitment and reduces the loan amount.

- Limited Vehicle Choices: You might be restricted to financing older, less expensive, or higher-mileage vehicles. These cars have a lower overall loan amount, making them less risky for the lender.

- Co-signer Option: If your credit is particularly challenging, a co-signer with excellent credit can significantly boost your chances of approval and secure better terms. This person takes on equal responsibility for the loan, so choose wisely and ensure they understand the commitment.

Common mistakes to avoid are getting discouraged and accepting the first loan offer, or worse, falling for predatory lenders who charge exorbitant rates. Shop around, even with lower credit. Capital One is often a better starting point than many other options for subprime borrowers. The goal is to get approved, make consistent on-time payments, and then potentially refinance at a lower rate once your credit improves.

Navigating the Dealership with Your Capital One Pre-Approval

Having a Capital One pre-approval letter in hand transforms your car buying experience from stressful to strategic. You’re no longer walking in blind; you’re armed with crucial financial information.

- Know Your Budget: Your pre-approval tells you the maximum loan amount you qualify for. Stick to this. Don’t be swayed by offers that push you beyond your comfort zone.

- Focus on the Car Price, Not Just the Monthly Payment: Dealerships often try to negotiate based on monthly payments. With your pre-approval, you know your rate and terms. Focus intensely on getting the best price for the vehicle. Lowering the car’s price directly reduces your loan amount and, consequently, your monthly payment.

- Be Transparent, But Firm: Inform the dealership that you have external financing from Capital One. They may try to beat your rate, which can be a good thing, but always compare their offer to your Capital One pre-approval. Don’t feel pressured to accept their financing if it’s not better.

- Understand Trade-In Value Separately: Negotiate your trade-in value as a separate transaction from the car purchase. Don’t let the dealership combine them into one confusing number.

- Avoid Unnecessary Add-ons: Dealerships often push extended warranties, paint protection, and other add-ons. Consider these carefully and factor them into your overall budget. Some might be useful, but many are high-profit items for the dealership.

The Application Process: Step-by-Step Guide

The Capital One car loan application process is designed to be straightforward, whether you apply online or through a dealership.

- Online Pre-Qualification (Recommended): Start by visiting Capital One’s Auto Navigator website. Enter basic information (income, housing, desired loan amount, credit score estimate). This results in a soft credit pull and gives you immediate estimated terms.

- Find Your Car: Use the Auto Navigator tool to search for vehicles at participating dealerships that align with your pre-qualification. This ensures the car is within your approved budget and meets Capital One’s vehicle requirements.

- Visit the Dealership: Take your pre-qualification offer to the dealership. Test drive the car, negotiate the price, and finalize the details.

- Complete the Full Application: The dealership will assist you in completing the full Capital One application. This involves providing more detailed personal, employment, and financial information.

- Provide Documentation: Be prepared to provide proof of identity (driver’s license), proof of income (pay stubs, tax returns), and proof of residence (utility bill).

- Sign the Papers: Once approved, review all loan documents carefully before signing. Ensure the interest rate, loan term, and all fees match what you were promised.

Pro Tips for a Smooth Capital One Car Loan Experience

Beyond the application itself, a few expert tips can make your entire car buying journey with Capital One much smoother and more financially advantageous.

- Check Your Credit Reports Regularly: Don’t wait until you need a loan. Regularly pull your free credit reports from AnnualCreditReport.com. It helps you catch errors early and monitor your financial health.

- Understand Your Budget Thoroughly: Look beyond just the monthly car payment. Factor in insurance, fuel, maintenance, and potential registration fees. A car loan is just one part of the total cost of ownership.

- Don’t Settle for the First Offer: Even with a pre-approval, dealerships might offer their own financing. Always compare. If their offer is better, great! If not, stick with your Capital One terms.

- Read the Fine Print: This cannot be stressed enough. Understand all terms, conditions, and potential fees associated with your loan. Ask questions if anything is unclear.

- Consider GAP Insurance: If you’re putting down a small down payment or buying a car that depreciates quickly, consider Guaranteed Asset Protection (GAP) insurance. It covers the difference between what you owe on your loan and the car’s actual cash value if it’s totaled or stolen.

- Set Up Auto-Pay for Loan Payments: Once approved, immediately set up automatic payments for your Capital One car loan. This ensures you never miss a payment, protecting your credit score and saving you from late fees.

Common Mistakes to Avoid When Applying for a Capital One Car Loan

Navigating the world of auto loans can be complex, and certain missteps can cost you time, money, and credit score points. Being aware of these common pitfalls can help you steer clear of them.

- Applying to Too Many Lenders Simultaneously: While grouping auto loan inquiries is helpful, indiscriminately applying for many different types of credit at once can hurt your score and signal desperation to lenders. Be targeted in your applications.

- Not Knowing Your Credit Score (or Your Credit History): Walking into the process without knowing your credit standing puts you at a disadvantage. Always check your score and reports beforehand.

- Overlooking Pre-Qualification: Skipping the Capital One pre-qualification step is a missed opportunity. It’s a free, no-risk way to understand your options and gain negotiating power.

- Being Unprepared with Documents: Delaying your application because you can’t find pay stubs or proof of address is frustrating. Have all necessary documents ready before you apply.

- Focusing Only on the Monthly Payment: While important, focusing solely on the monthly payment can lead you to accept longer loan terms or higher interest rates, ultimately paying more over the life of the loan. Always consider the total cost.

- Ignoring the Total Cost of Ownership: Beyond the loan, remember insurance, fuel, maintenance, and potential repairs. A cheap monthly payment for a car that costs a fortune to maintain isn’t a good deal.

Conclusion: Drive Away with Confidence

Securing a Capital One car loan is an achievable goal for many, regardless of their credit standing. By understanding how your credit score impacts your eligibility and interest rates, and by diligently preparing for the application process, you empower yourself to make informed decisions. Capital One’s flexible approach, coupled with their pre-qualification tool, makes them an excellent partner on your car-buying journey.

Remember, a strong credit score is your best asset. If yours isn’t where you want it to be, take the proactive steps outlined in this guide to improve it. Even if you have less-than-perfect credit, Capital One offers pathways to vehicle ownership, providing an opportunity to rebuild your credit for the future. Approach the process with knowledge, patience, and a clear financial plan, and you’ll soon be driving away in your dream car, confidently and affordably.

Internal Links:

- Want to dive deeper into credit improvement? Read our article on How to Drastically Improve Your Credit Score in 6 Months.

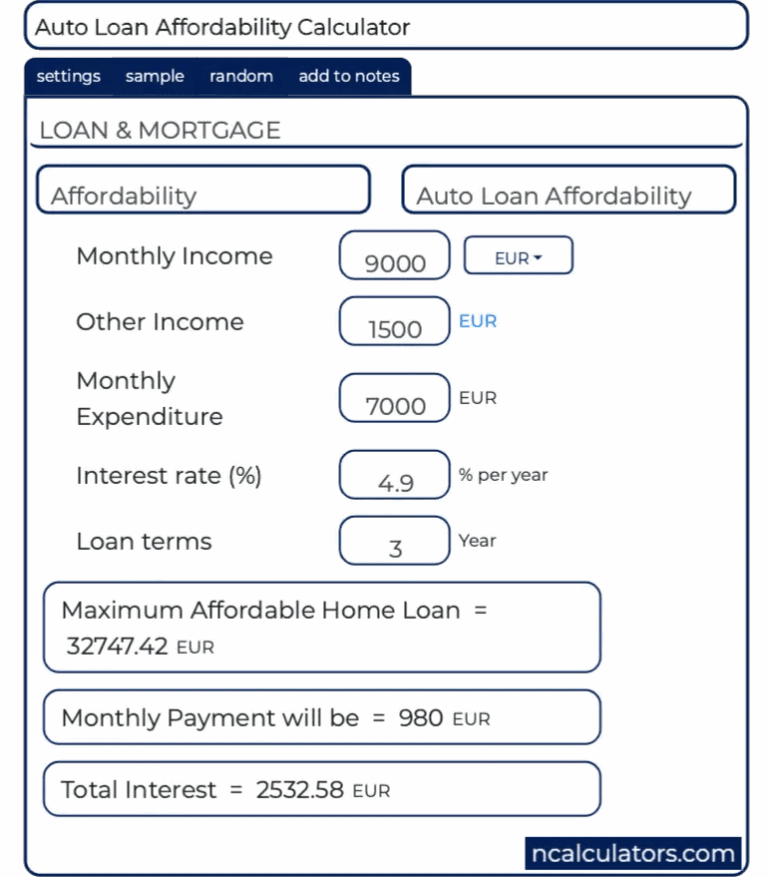

- Confused about how much car you can afford? Check out our guide to Mastering Your Debt-to-Income Ratio for Loan Success.

External Link:

- For official, personalized credit score information and reports, visit Experian’s official website.